- Average UK house price fell by 1.4% in the year to December

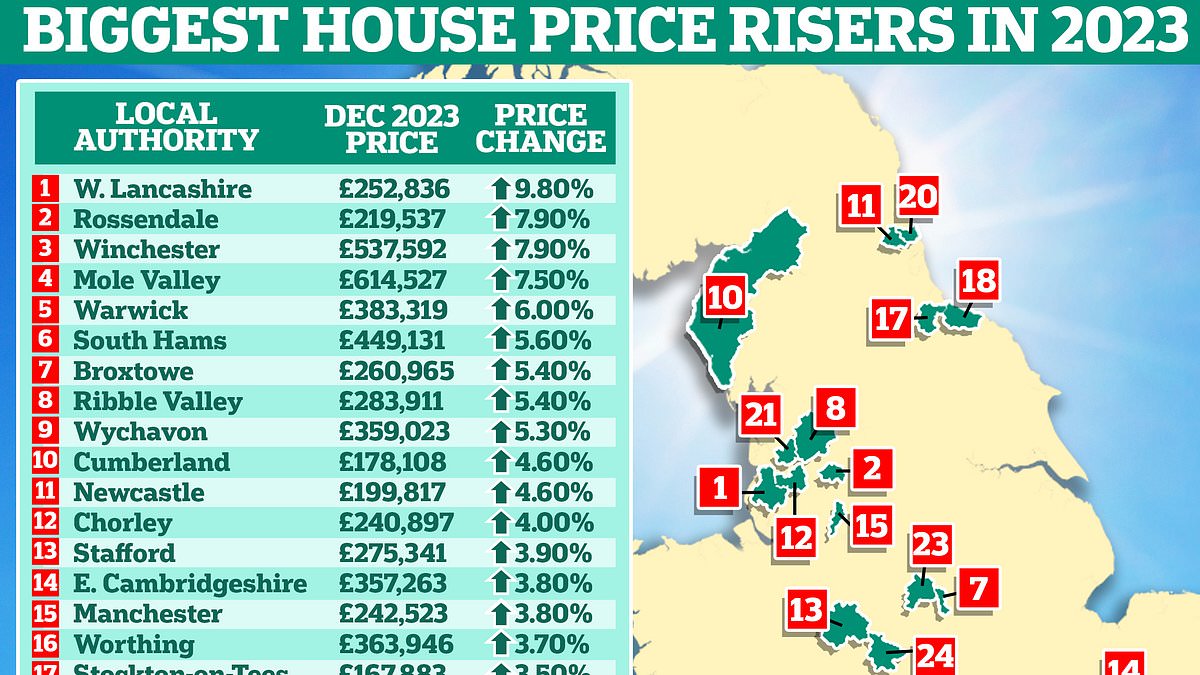

- Prices in West Lancashire up 9.8% while some London areas saw 10%-plus drops

House prices officially fell last year, according to the latest figures from the Office of National Statistics.

The ONS revealed the average UK house price slipped 1.4 per cent in the year to December, as the mortgage crunch took its toll on property sales.

It means the typical home lost £4,000 in 2023, with the average sold price coming in at £285,000.

But some locations suffered much bigger declines, with six English local authority areas seeing house price falls of 10 per cent or more.

Meanwhile, others bucked the trend with nine seeing property prices climb by 5 per cent of more.

The ONS figures are widely viewed as the most comprehensive and accurate house price index. This is because this report by the UK’s official statisticians uses Land Registry data and is based on average sold prices. However, this also means its data lags behind other indexes.

A geographical split emerged last year in the UK when it came to property prices.

England and Wales saw typical sold prices fall by 2.1 per cent and 2.5 per cent respectively in the 12 months to December.

However, in Scotland and Northern Ireland average prices actually rose by 3.3 per cent and 1.4 per cent.

Related Articles

HOW THIS IS MONEY CAN HELP

Across the country’s regions, house price changes ranged from a 4.8 per cent decline in London and a 4.6 per cent fall in the South East, to a rise of 1.2 per cent in the North West and a slight 0.3 per cent gain in the West Midlands.

But there were much greater differences between local authorities.

This stresses the all important point – the property market doesn’t move as one, but comprises thousands of localised markets, all behaving differently.

For example, average prices in West Lancashire rose by a staggering 9.8 per cent last year, with the typical home rising from £230,000 to £253,000.

In the City of London, average house prices fell by 17.8 per cent from £975,289 to £802,000.

Where house prices fell most in 2023

Some of the worst performing housing markets are to be found in London. Prices in the capital fell on average 4.8 per cent in the 12 months to December.

Average house prices in The City of London (the capital’s historic financial district) are down a whopping 17.8 per cent, according to the ONS, while the City of Westminster is down 16.1 per cent. Prices in Kensington and Chelsea are also down 13.7 per cent.

The ONS cautions against reading too much into figures for very small transaction areas, such as the City of London, as they can be skewed by a few sales.

Outside of the capital, Gosport on the south cost saw an 11.5 per cent decline in house prices. Some popular commuter hotspots also suffered, with house prices falling 11.3 per cent in Tunbridge Wells, 9.5 per cent in Welwyn and Hatfield, 9.2 per cent in Runnymede and 9.1 per cent in Surrey Heath.

Where house prices rose most in 2023

North West locations were strong performers last year, with the leading local authority area West Lancashire posting a 9.8 per cent rise in house prices.

Prices in the borough of Rossendale in the North West of England also rose by 7.9 per cent last year, according to the ONS.

Interestingly, earlier this week, Rossendale was also rated as the hottest property market of 2023 by Zoopla.

The property website revealed that some 44.2 per cent of homes there rose in value by 5 per cent or more last year – which is more than any other local authority.

At the other end of the country, Winchester and the Mole Valley, in the South, saw house price gains of 7.9 per cent and 7.5 per cent.

Will house prices rise or fall in 2024?

The ONS says average house prices actually increased by 0.1 per cent between November and December last year.

This looks rather positive given that average prices fell 0.8 per cent during the same period 12 months ago.

Last week we heard from two separate reports that the housing market may be heating up with increasing numbers of people looking to buy or sell.

The reset is quickly moving towards a recovery Jonathan Hopper, Garrington Property Finders

The latest property market survey by the Royal Institution of Chartered Surveyors (Rics) showed that estate agents and surveyors are seeing rising numbers of buyer enquiries as well as more sellers coming to market.

Meanwhile, Rightmove revealed a record number of homeowners contacted an estate agent to get their home valued in January.

Jonathan Hopper, CEO of Garrington Property Finders says: ‘The reset is quickly moving towards a recovery.

‘Crucially we’re starting to see more stock come onto the market as people who delayed their moving plans last year decide that now is the time to act before prices pick up speed again.

‘The recovery remains tentative, but there is a growing sense that 2023’s price reset is over, and that last year’s widespread price falls in England and Wales have made many areas better value.’

The renewed confidence from buyers has come alongside mortgage rates falling from their peak late last summer, with big cuts arriving in the new year.

Nicky Stevenson, managing director at national estate agent group Fine & Country adds: ‘House prices finished the year down compared to 2022, as the gap between what sellers would accept and buyers would pay for a home narrowed.

‘However, the small uptick in prices in December lends credibility to the suggestion that the property market is in a much healthier position overall than it was at the start of last year.’

Many within the property industry believe that mortgage rates have now reached levels that will encourage buyers and home movers back into the market.

Although average fixed mortgage rates remain just above 5 per cent, according to Moneyfacts, the cheapest deals are now below 4 per cent.

There is also now wide expectation that mortgage rates may fall further as the year progresses.

Jonathan Hopper says: ‘As the cost of borrowing edges down, homes are becoming more affordable.

‘With consumer inflation stuck at double the Bank of England’s target, interest rates may come down more slowly than many had hoped, but last year’s trickle of buyers has already turned into a stream.’

Stevenson adds: ‘Expectations are that rates could fall at some point this year, which will widen affordability and encourage more demand.

‘Today’s news that inflation held at 4 per cent will boost hopes that interest rates will be cut sooner than anticipated.

‘The Bank of England has also reported three consecutive monthly increases in mortgage approvals as momentum builds in the housing market.

‘This pent-up demand from buyers who paused or held off on their property search means there is growing activity on the market.’

Another factor that may support house prices is the fact the number of new homes planned by housebuilders fell by almost half last year.

Interestingly, the average price of a sold new build rose by 9.4 per cent in 2023, according to the ONS figures.

A lack of supply of new homes will likely help support prices further, according to Anthony Codling, head of European housing and building materials for investment bank RBC Capital Markets.

He adds: ‘Today’s ONS data confirms that 2023 was not the year of the house price crash and with falling inflation, falling mortgage rates and rising wages we doubt that a crash will come in 2024, and the recent words spoken, and actions taken by housebuilders confirms our view the housing market is looking up rather than down so far this year.

‘The scene is set for a recovery, and we have our fingers crossed that any moves taken by politicians this election year will help rather than hinder the housing market recovery.’

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

- Available homes for sale over 20% higher than a year ago

- Demand up 12% year-on-year, led by London and the East

- One in five sellers accepting 10%+ below asking price to secure a sale

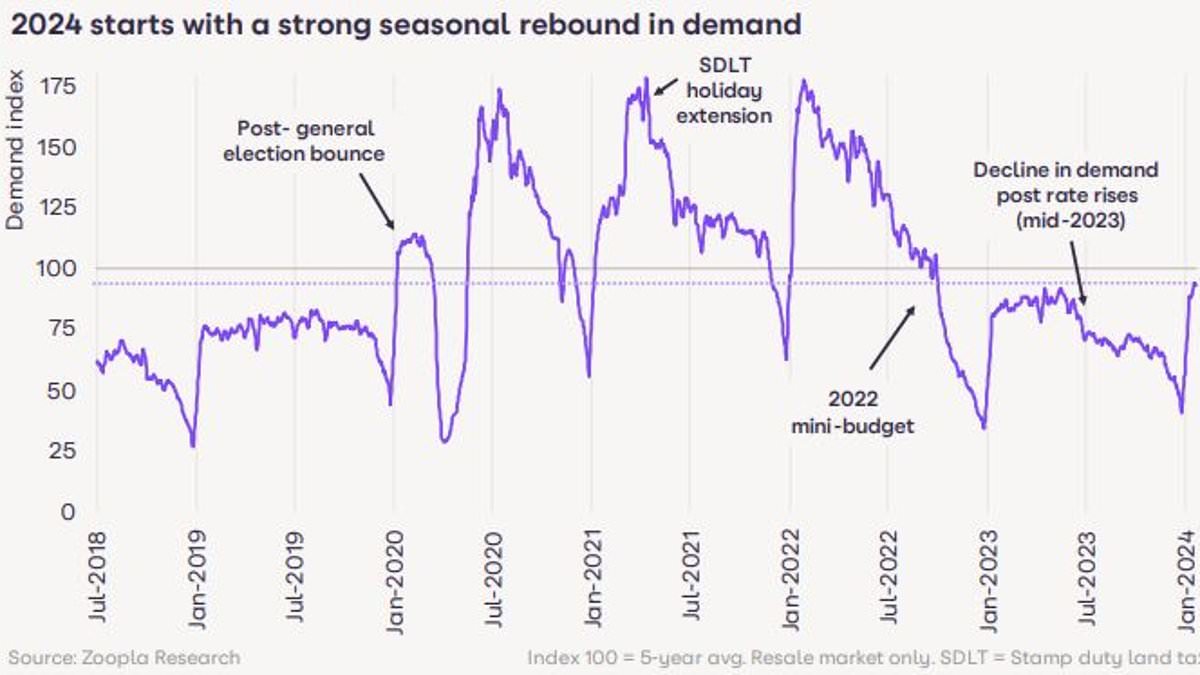

House prices fell slightly in the year to December, but the property market is now heating up on the back of falling mortgage rates according to Zoopla.

The property portal said prices fell by 0.8 per cent in the 12 months to the end of December, but more buyers and sellers were now entering the fray and an increasing number of homes were going under offer.

The month before, property prices fell by 1.2 per cent compared to a year before.

Zoopla also revealed the number of sales agreed is 13 per cent higher than last year and higher across all countries and regions.

It said buyer demand is 12 per cent higher than a year ago, though it remains 13 per cent below the five-year average.

More homes are also hitting the market, according to the property website. The number of available homes is up 22 per cent on this time last year.

The average estate agent has 28 homes for sale, which is double the low point recorded in late 2022, when there were just 14 homes per estate agent.

> Read: When will interest rates fall? Forecasts on when base rate will go down

Related Articles

HOW THIS IS MONEY CAN HELP

It’s still a buyer’s market

Despite the positive start to the year, it remains a buyer’s market, according to Zoopla.

It says a fifth of sellers are still accepting more than 10 per cent below the asking price to secure a sale. This is close to one in four across London and the South East.

Richard Donnell, executive director at Zoopla said the key trend over 2023 was sellers cutting asking prices to attract buyer interest. He said this has continued into 2024.

‘It’s a positive start to the year with all key measures of housing activity higher than a year ago,’ said Donnell.

‘The fall in mortgage rates has led to a rebound in buyer demand and sales following a weaker second half of 2023 when many movers put decisions on hold.

He added: ‘This improvement in activity will support sales volumes which, at one million, reached an eleven year low in 2023.’

‘We don’t see these trends as a precursor to higher prices in 2024 as it remains a buyer’s market.

‘Sellers looking to move should be encouraged by these early signals of activity but buyers remain price sensitive and focused on value for money.

‘Over-optimism by sellers could quickly stall the current improvement in market activity.’

Will prices fall in 2024?

Zoopla revealed that house price falls were greatest in the East of England, where prices fell by 2.5 per cent in 2023.

Meanwhile, house prices went up across Scotland, Northern Ireland and the North of England.

Looking ahead, it suggests higher levels of sales activity in early 2024, following on from the final weeks of 2023, are evidence of greater alignment between buyers and sellers on pricing.

For that reason, analysts at Zoopla argue that house prices will not fall much further.

Earlier this month, the property firm Knight Frank forecast that house prices will rise 3 per cent this year having only three months earlier predicted a 4 per cent fall by the end of 2024.

Anthony Codling, head of European housing and building materials for investment bank RBC Capital Markets said: ‘With rising wages, falling inflation, falling mortgage rates, and increasing talk of election related housing stimulus packages we expect house prices to rise in 2024.’

Tom Ashwood, managing director at London agent Tom Ashwood Real Estate says: ‘I feel the increase in buyer activity that has initially been fuelled by a reduction in mortgage rates and a lack of intent to buy through 2023 will assist in keeping asking prices fairly stable through the initial part of 2024, which will lead to more property being listed for sale.

‘If interest rates remain at a stable level and the appetite remains, we may even see an increase in house price inflation this year, particularly through the good selling time we tend to see between the Spring and Summer months.’

London market looking more affordable?

London has led the rebound in new buyer demand, up 21 per cent on this time last year.

This is perhaps because housing affordability in London is the best it has been since 2014, according to Zoopla, mainly thanks to stagnant prices and rising wages.

London house prices have risen just 13 per cent since 2016, according to Zoopla, compared to 34 per cent at a UK level.

The affordability of homes in London – as measured by a simple price-to-earnings ratio – is at its lowest since 2014.

However, London remains expensive compared to the UK average with house prices standing at 13 times earnings, down from a high of over 15 times earnings in 2016.

Zoopla’s Richard Donnell adds: ‘In London, this increased demand is evident across the market, with inner and outer London, alongside core commuter areas all registering increased demand for homes.

‘This may be an early sign that the tide is turning for the London sales market after seven years of lacklustre activity compared to the rest of the UK.’

Matt Thompson, head of sales at London estate agent Chestertons, adds: ‘2024 started with a busy property market as buyers have been motivated to either commence or finalise their property search.

‘The increasing availability of more affordable mortgage deals thereby plays a key role and will likely continue to fuel a surge in buyer activity over the coming weeks.’

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.