The spring real estate market is in full swing and homes are going up for sale – but they’re staying there for longer in a handful of US cities.

In a smattering of metro cold spots – dotted throughout Texas, Florida, Louisiana, New York and West Virginia – homes are staying on the market for an average of more than 60 days, according to new data from Realtor.com.

Across the board, homes spent a median of 50 days on the market in March.

‘Some of these markets are perennially slow-moving,’ said Danielle Hale, chief economist at Realtor.com. ‘They tend to be smaller markets that are not on the radar of most buyers.’

In all of the areas where homes were spending longer on the market, there was also a notable increase in inventory year-on-year, according to data for March.

Huntington in West Virginia had among the coolest property markets in March, with homes remaining up for sale for an average of 66 days

Housing inventory surged by 130 percent in Punta Gorda, Florida. And in Cape Coral and Naples, both also in Florida, inventory was up 101 and 82 percent, respectively.

The areas with stagnating markets also often offer more affordable options, with nine out of the twelve metros boasting median list prices below the national average of $424,900.

For example, the most budget-friendly among them, Huntington, West Virginia, has a median list price of just $179,950.

Interestingly, eight of the twelve metro areas are located along the Gulf of Mexico, making them prone to storm-related risks. Some are still dealing with the aftermath of hurricanes and soaring interest costs as a result.

‘In some cases, homes in these areas are at risk of flooding and other hazards, leading to rising insurance costs,’ said Hale.

According to real estate agent Karen Brown of Michael Saunders & Company on the Florida Gulf Coast, Punta Gorda is suffering in the wake of Hurricane Ian in 2022.

‘Cleanup efforts are ongoing, and residents are still navigating insurance claims,’ Brown told Realtor.com.

1. Lafayette, Louisiana

Median days on the market in March: 69 (tie)

Median home list price in March: $259,250

In Lafayette, Louisiana, homes were on the market for a median of 69 days

2. Punta Gorda, Florida

Median days on the market: 69 (tie)

Median home list price: $419,000

3. Brownsville, Texas

Median days on the market: 68 (tie)

Median home list price: $308,000

In Brownsville, at the southernmost tip of Texas, on the northern bank of the Rio Grande, homes were on the market for a median of 68 days

4. Utica, New York

Median days on the market: 68 (tie)

Median home list price: $239,900

5. New Orleans, Louisiana

Median days on the market: 67

Median home list price: $329,000

6. Crestview, Florida

Median days on the market: 66 (tie)

Median home list price: $644,000

7. Huntington, West Virginia

Median days on the market: 66 (tie)

Median home list price: $179,950

In Huntington, West Virginia, homes were on the market for a median of 66 days

8. Waco, Texas

Median days on the market: 66 (tie)

Median home list price: $345,000

9. Longview, Texas

Median days on the market: 64 (tie)

Median home list price: $305,500

10. Naples, Florida

Median days on the market: 64 (tie)

Median home list price: $849,000

In Naples, Florida, homes were on the market for a median of 64 days. The median house price was significantly higher than elsewhere on the list

11. Cape Coral, Florida

Median days on the market: 64 (tie)

Median home list price: $474,100

12. Baton Rouge, Louisiana

Median days on the market: 64 (tie)

Median home list price: $305,000

In Baton Rouge, Louisiana, homes were on the market for a median of 64 days

Home prices have doubled in less than ten years in 68 of the 100 largest cities in the US, a sobering new study shows.

And in some major American cities, the cost of the average property has doubled in as little as five years.

In Detroit, home prices were half of what they are now as recently as 2019, data from real estate marketplace Point2 reveals.

Home prices in Miami and Tampa, Florida, have doubled since 2018, as they have in Baltimore, Maryland, and Spokane, Washington.

Buyers in Irvine, California – the most expensive housing market in the study – have seen average home prices double from an already steep $750,000 to $1.5 million in just seven years.

A storm of high inflation and interest rates, tight supply and surging demand has meant that the national median home price has yo-yoed toward around twice what it was a decade ago.

The cost of the average home in the US has gone up from around $200,000 to around $400,000.

According to Point2, a common home appreciation theory is that residential properties tend to double in value in about 10 years.

In the so-called ‘Motor City’ Detroit, one of the reasons that house prices have risen twofold in half this amount of time is because they have been historically low compared to the national average.

House prices in the city have been among the fastest-growing in the US in recent years, as the city bounces back from the mortgage crisis which left some homes virtually worthless.

Less than two decades ago, one in five houses stood empty in the city with foreclosures mounting and properties on deserted streets being sold for $1.

The crisis and the demise of the big carmakers – which had previously made Detroit an industrial powerhouse – drove millions from their homes.

But as the car industry – this time with a focus on electric vehicles – begins to pick up speed again, house prices have risen rapidly.

House prices in Detroit have been among the fastest-growing in the US in recent years, as the city bounces back from the mortgage crisis which left some homes virtually worthless

At the start of 2019 you could buy a home in Detroit for $40,000, according to Point2.

Now, according to listings website Realtor.com, the median home listing price in the city is $89,900.

Despite the short-term price surge, Detroit still remains among the more affordable of the major cities in the US.

Detroit was lagging behind other cities in terms of house price growth, according to CoreLogic chief economist Selma Hepp, so some of this growth is catch-up.

Similarly, data shows that prices also doubled quickly in Spokane, where not that long ago, in March 2018, a home cost just $184,500 – compared to $371,000 today.

Spokane has seen house prices surge as Americans have moved to the city amid investor interest and urban revitalization efforts.

And some people who fled to so-called pandemic ‘boomtowns’ such as Boise, Portland and Austin, later moved to Spokane in search of cheaper housing – which has driven up prices further.

Prices also doubled quickly in Spokane, where not that long ago, in March 2018, a home cost just $184,500 as compared to $371,000 today

According to Point2, home prices have accelerated just as dramatically in Miami, as well as in Tampa, amid a surge of new residents.

The past six years were enough for homes to double in cost to about half a million dollars in both cities.

Prices in all five of the largest markets in Florida – including Jacksonville, Orlando, and St. Petersburg – have doubled in just six to eight years.

Arizona is in a similar position – with seven large cities doubling in price between six and seven years.

Prices increased twofold in booming Scottsdale, where the average home costs a huge $837,500 compared to $416,000 at the end of 2017.

Phoenix has also seen a surge in home prices – which local incomes can barely keep up with.

Home prices have surged dramatically in Miami amid a surge of new residents

House prices in Tampa, Florida, have doubled in the last six years according to Point2

It comes as separate data shows the US housing market gained a huge $2 trillion in value in the last year alone, amid a historic shortage of homes for sale.

Soaring mortgage rates mean many Americans locked into lower deals have stayed put, leading to a significant inventory shortage.

This, in turn, has meant home values have continued to rise, pricing many Americans out of the market entirely.

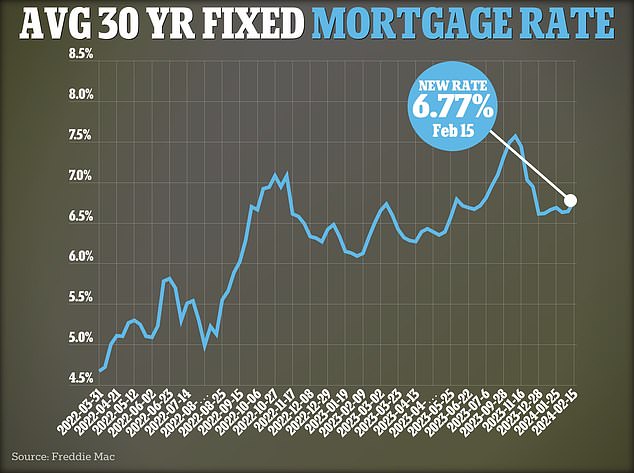

While mortgage rates had been slowly declining in the first months of this year, the average 30-year fixed rate deal is beginning to creep up again.

Following data released earlier this week which showed inflation remains stubborn, the average 30-year mortgage deal rose to 6.88 percent, according government-backed lender Freddie Mac.

America has a record number of ‘million-dollar cities’ – where the average house price now exceeds six figures, new data shows.

In total 550 US cities have an average property price of $1 million or above, up by 59 from this time last year.

The data from property portal Zillow lays bare how red-hot America’s real estate landscape remains after years of consistent growth.

California alone counts 210 ‘million-dollar cities’ – the highest of any US state and an increase of 12 from last year.

It was followed by New York, New Jersey and Florida which count 66, 49 and 32 respectively.

California alone counts 210 ‘million-dollar cities’ – the highest of any US state and an increase of 12 from last year. Pictured: a San Francisco home on the market for $1.49 million

In total 550 US cities have an average property price of $1 million or above. Pictured: a San Francisco home on the market for $1.49 million

The growth of luxury real estate has largely outstripped the general housing market, Zillow’s research shows.

While typical US home values have grown 4.2 percent compared to last year, those in ‘million-dollar cities’ had seen an average year-on-year increase of 4.6 percent.

New Jersey has experienced the biggest increase in cities where home values are over $1 million. It added 14 to its state in the last year.

Meanwhile New York, San Francisco, Los Angeles and Boston were the four metro areas with the highest amount of ‘million-dollar cities.’

It comes as America’s so-called ‘frozen’ property market shows signs of thawing as the number of new listings advertised on Zillow increased 20 percent between January and February.

Soaring mortgages have created a ‘lock-in effect’ as homeowners are reluctant to trade in the cheap 30-year fixed deals they secured before rates started rising.

Data from Government-backed lender Freddie Mac shows the average rate on a 30-year fixed mortgage is now 6.79 percent.

This is more than double where they were three years ago when they were hovering at 3.17 percent.

New York, San Francisco, Los Angeles and Boston were the four metro areas with the highest amount of ‘million-dollar cities.’ Pictured: a $1 million home currently for sale on Zillow in Boston, MA

An LA home for sale for $1.49 million on Zillow

The New York metro area had the largest amount of ‘million-dollar cities.’ Pictured: a $1.5 million apartment for sale in Manhattan’s Lenox Hill

It means a buyer purchasing a $400,000 property today faces monthly payments of $2,474. This analysis assumes a 5 percent downpayment.

However, had they bought in March 2021, this figure would be just $1,637 – a difference of $800 per month.

Yet a recent report by Zillow suggested housing activity was starting to uptick again.

Homes that sold in February spent an average of 17 days on the market – slower than during the homebuying frenzy of 2021 and 2022 but still much faster than pre-pandemic.

Experts are divided over where the housing market is now headed after they have remained surprisingly resilient.

Last week Shark Tank star Barbara Corcoran predicted even the smallest drop in mortgage rates would cause property values to shoot up.

She told Fox Business: ”If rates go down, just another percentage point, prices are going to go through the roof.

‘Everyone will come out and buy. There are probably 10 buyers on the sidelines [for each home on the market] waiting for interest rates to come down,’ she continued. ‘So everybody’s going to charge the market.’

Contrastingly, analyst Meredith Whitney recently told DailyMail.com that prices would soon fall as more and more Baby Boomers start to downsize -and free up inventory.

Whitney – who earned the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crash – said: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

Shark Tank star Barbara Corcoran has revealed when housing prices will go ‘through the roof’.

The self-made real estate millionaire said a fall in interest rates is key – to lower the cost of borrowing and attract buyers who will bid up prices.

The ‘magic number’ is a fall of 1 percent to take mortgage rates under 6 percent.

‘If rates go down, just another percentage point, prices are going to go through the roof,’ Corcoran said in a Fox Business interview Wednesday.

‘Everyone will come out and buy. There are probably 10 buyers on the sidelines [for each home on the market] waiting for interest rates to come down,’ she continued. ‘So everybody’s going to charge the market.’

As of latest data from government-backed lender Freddie Mac from March 21, the average 30-year fixed rate mortgage is 6.87 percent.

That is down from the 8 percent rates seen in October last year, but still double the historically low rates of around 3 percent seen during the pandemic.

What is needed to get the mortgage rate to fall below the 6 percent that Corcoran sees as ‘the magic number that people get juicy about’?

While the Federal Reserve does not directly set mortgage rates, the benchmark borrowing rate it sets does indirectly influence the amount Americans pay on a loan to purchase a home.

Mortgage rates track the pattern of 10-year Treasury Yields, which are determined by a range of factors including inflation, economic growth and the Fed’s benchmark funds rate.

The Federal Reserve left interest rates unchanged for the fifth consecutive meeting earlier this month, keeping benchmark borrowing costs at a 23-year high between 5.25 and 5.5 percent.

The Fed‘s series of aggressive rate hikes were intended to pour cold water on rampant inflation, which peaked at 9.1 percent in June 2022.

At its latest meeting, Fed policymakers penciled in three quarter-percentage point cuts by the end of the year – but did not commit to a date when it might start decreasing rates.

If interest rates fall, this will then have an impact on mortgage rates.

But Corcoran warned Americans that instead of getting a cheaper deal when rates come down, the housing market may actually heat up.

Corcoran warned Americans that if interest rates come down, it will mean house prices will go up even further as demand to buy suddenly soars

As of latest data from government-backed lender Freddie Mac from March 21, the average 30-year fixed rate mortgage is 6.87 percent

‘If you wait for interest rates to come down by another point, I don’t think you’ll gain, I think you’ll wind up paying more because I wouldn’t be surprised if real estate went up by another 8 or 10 percent if interest rates come down another point,’ she said.

Elevated mortgage rates and a historic shortage of homes for sale has meant that house prices are already high – pricing many Americans out of the market.

In 2023 alone, the US housing market gained $2 trillion in value.

Corcoran’s comments come after a survey from real estate listings company Realtor.com revealed that the majority of homebuyers would need mortgage rates to dip to 5 percent before they followed through on a purchase.

Some 72 percent of potential home buyers said pulling the trigger would be feasible if mortgage rates dropped below 5 percent

According to the survey of 5,000 US consumers, conducted during the first week of November when rates were at their highest, about 18 percent of Americans said they were waiting for rates to fall below 7 percent.

If they dropped below 6 percent, an additional 22 percent of respondents said they would buy a home.

But the vast majority – some 72 percent – said rates would need to go below the ‘magic’ mortgage rate of 5 percent before they would sign on the dotted line for a home.

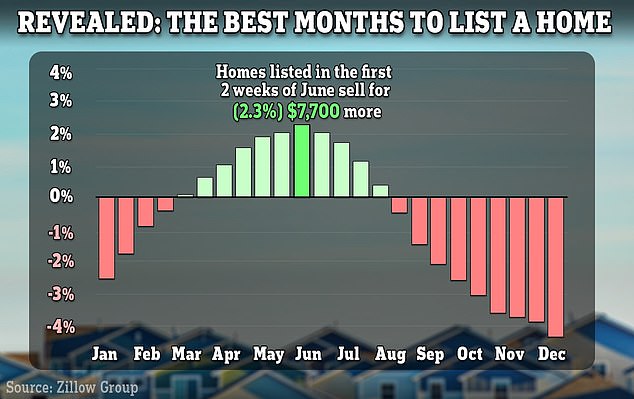

- Research shows homes listed in the first fortnight of June attract price premium

- Sellers stand to make an extra $7,700 on a typical property, Zillow claims

- Experts say America’s property market is finally showing signs of thawing

- Sellers could also see a big drop in costs after the trade body for realtors last week agreed to eliminate a notorious commission scheme

Homeowners looking to sell up may wish to wait until the summer if they want to maximize their profits.

New analysis by property portal Zillow shows home listed in the first two weeks of June typically sell for $7,700 more than they would do otherwise.

By comparison, sellers risk shaving more than 4 percent off their asking price if they wait until December.

The findings of the report are another reason to hold off selling for now – it emerged last week that commission fees charged by real estage agents are set to drop in the summer.

The housing market historically always heats up in the spring and summer months as parents want to relocate ahead of the next schoolyear.

New analysis by property portal Zillow shows home listed in the first two weeks of June typically sell for $7,700 more than they would do otherwise

Sellers’ homes also benefit from fresh flowers and greenery after the winter.

Amanda Pendleton, a home trends expert at Zillow, told CNBC: ‘It’s sort of an ideal time for both buyers and for sellers, and that’s why we just see a lot more activity that time of year.’

Experts claim Americans frozen property market is finally showing signs of thawing. A report by Redfin found the number of new listings jumped 14.8 percent compared to a year ago – the largest annual increase since May 2021.

Prior to the pandemic, May was the hottest month to list a property. However, a volatile mortgage market saw this pushed back to June last year.

According to Zillow’s data, homes listed in the first fortnight of June 2023 sold for 2.3 percent more than average. It equates to a $7,700 boost on an average home.

Prime selling months vary slightly by city though, researchers noted.

For example, in New York, homes listed in the first half of July tended to attract a 2.4 percent premium – or $15,500 in real terms.

Meanwhile sellers in Los Angeles should strike in the first half of May to benefit from a 4.1 percent premium on their home listing. It works out at $39,300 extra.

Prior to the pandemic, May was the hottest month to list a property. However, a volatile mortgage market saw this pushed back to June last year

America’s property market has all but frozen in response to soaring mortgage rates deterring owners from moving.

The average rate on a 30-year fixed-rate home loan is now 6.74 percent, according to Government-backed lender Freddie Mac.

This is almost double where they were in March 2022 when they were hovering at 3.76 percent.

It means a buyer today purchasing a $400,000 home faces paying around $700 per month on their mortgage than had they bought two years ago. This analysis assumes a 5 percent downpayment.

Rising rates have created a ‘lock-in effect’ whereby buyers do not want to give up their cheap deals.

America’s property market has been all but frozen as a result. In the first week of March, applications to purchase a home were 11 percent lower than the same period a year ago, according to the Mortgage Bankers’ Association.

Research out in February revealed the ‘magic’ mortgage rate that will kickstart the housing market.

A majority of prospective home buyers say they would finally follow through with the purchase of a home if rates dipped below 5 percent, according to a new survey by Realtor.com.

There was more good news for sellers last week. They could see a BIG drop in selling costs after realtors agreed to eliminate notorious commission scheme and pay $418 million damages in landmark legal settlement.

Meanwhile, millions of homebuyers could soon be in line for a $10,000 tax credit under sweeping reforms of the housing market proposed by President Biden during his State of the Union address.

I’m struggling with the idea of selling a rental property that has both a high monthly maintenance fee and a high mortgage rate. The costs to keep this house are currently higher than the monthly income it generates.

I recently refinanced in order to pull out $100,000, so now I owe $420,000 on the property, which is worth approximately $750,000.

My recent refinancing increased my mortgage rate from 5.14% to 7.9%, essentially eating up all my cash flow.

I’m on the fence. Should I sell, or should I refinance for a better rate to free up cash flow?

Losing Money Fast

‘The Big Move’ is a MarketWatch column looking at the ins and outs of real estate, from navigating the search for a new home to applying for a mortgage.

Do you have a question about buying or selling a home? Do you want to know where your next move should be? Email Aarthi Swaminathan at TheBigMove@marketwatch.com.

Dear Losing,

The fact that you’re bleeding money from this rental is not good. You need to either bring down your interest rate or raise rents so you can turn a profit in order to make it a worthwhile investment. But keep in mind that many people are sitting on the sidelines waiting for interest rates to fall, so you might not get your desired price if you decide to sell.

Your mortgage rate is likely the biggest reason your monthly costs have jumped so much. Rates are expected to fall to around 6% or lower by the end of the year. You could refinance then, but do the math to see if it’s worth it.

You’ve already been through the wringer with refinancing, and you likely paid various application, appraisal, attorney and origination fees — in addition to closing costs — to extract that $100,000. All of that is expensive, and now you’re thinking of going through it again.

Even if you refinance again at a lower rate, would that be enough to make a profit? Were you able to turn a profit on that property when rates were at 5%? If not, would you be able to raise rents for your current tenants or perhaps find new tenants who would be able to pay more? And is the house in need of repairs or upgrades?

Unless you can make a profit on the property in the next couple of years, there’s little reason for you to hold onto it, unless you believe that it’s in an area that will experience a significant appreciation in value — you’d want to see appreciation of 20% or more, given the fees you would have to pay upon selling.

Part of your retirement plan

At the same time, a second property is nearly always a good investment. Do you think there will be considerable demand for the rental in the medium to long term? Is it in an area where you might be able to find tenants who would pay enough to cover your costs in the near term so you can at least break even? If so, it’s a good idea to try to hold onto the property, especially if it’s part of your retirement plan.

Provided that you have enough savings to help you get through this current era of 7% rates, and you have the money to refinance down the road to get your monthly costs down to a level where you can have a healthier cash flow, it may be worth keeping the home.

Selling isn’t an easy or simple decision. Because this is not your primary home, you’ll need to factor in the capital-gains taxes you would have to pay, along with 6% in real-estate commissions.

If you do decide to sell at some point in the future, you could roll that money into another like-kind property in order to qualify for a 1031 exemption, in addition to a lower rate.

The bottom line: You need to think like a real-estate investor and leave emotion out of this decision. If the property is not making money or it’s not going to at least break even at some point, you have your answer. But keep in mind that the real-estate market can surprise on the upside and that once you sell the home, you will not be able to take back that decision.

By emailing your questions, you agree to having them published anonymously on MarketWatch. By submitting your story to Dow Jones & Company, the publisher of MarketWatch, you understand and agree that we may use your story, or versions of it, in all media and platforms, including via third parties.

The US housing market gained a huge $2 trillion over the last year, amid a historic shortage of homes for sale.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023, up from $474,740 a year earlier.

According to Redfin analysis of more than 90 million homes across the country, the total value of US residential real estate increased 5.3 percent from a year earlier to $47.5 trillion in December.

While soaring mortgage rates mean housing demand is sluggish, home values continue to rise, pricing many Americans out of the market.

In the last two years, the housing market has gained $5.6 trillion, Redfin found.

However a disparity remains across the US. While affordable East Coast and Midwest metros saw the biggest rise in home values in the last year, so-called pandemic ‘boomtowns’ have seen the largest decline.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023. The biggest rises were on the east coast of America

Scroll down for the full list of metros with the biggest price rises.

According to Redfin, there are three major reasons why home values are continuing to rise.

Many homeowners are locked into ultra-low mortgage rates from previous years, meaning they are hesitant to put their houses on the market.

With supply tighter than demand, buyers are competing for a limited pool of homes. That is propping up values for both properties that are already for sale, and those that could hit the market in the future.

The total value of US homes was nearing a trough at the end of 2022, which is part of the reason year-over-year growth at the end of 2023 was so large, it added.

It is typical for home values to cool in the winter, but they experienced an abnormally large slowdown in 2022 as the shock of surging mortgage rates sent a freeze through the housing market.

While America grapples with a housing shortage, it is also continuing to build homes, which contributed to the gain in total home values last year, Redfin said.

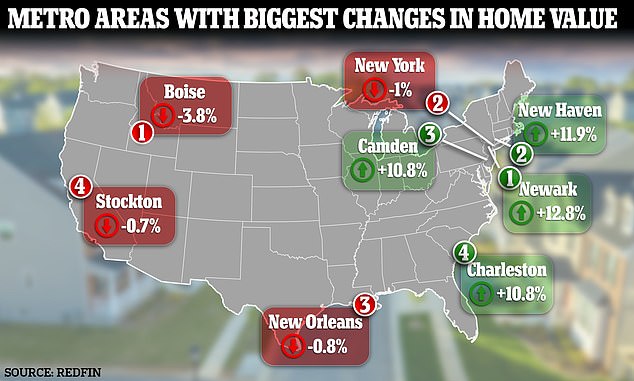

Home values in Newark, New Jersey, saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion.

Next come two other East Coast metros, New Haven, Connecticut, and Camden, New Jersey. Homes in New Haven gained 11.9 percent in value to $86.5 billion, while properties in Camden went up by 10.8 percent to $153 billion.

Home values in Newark, New Jersey , saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion

Fixed 30-year mortgage rates are now hovering around 6.9 percent, according to Government-backed lender Freddie Mac

Charleston, South Carolina, ranked fourth – with values increasing by 10.8 percent to $188.5 billion.

Next are three Midwestern metros, Elgin, Illinois, Grand Rapids, Michigan and Milwaukee, Wisconsin.

Places like Newark and Camden are likely seeing home values jump in part because they are attracting demand from people who are priced out of New York and can now work remotely, Redfin said.

Midwestern metros like Milwaukee and Grand Rapids are experiencing home value gains for a similar reason.

They are affordable, and when mortgage rates and home prices are elevated, demand for affordable homes goes up.

‘America’s homeowners are sitting pretty. They’re holding a massive amount of housing wealth, despite lackluster demand from buyers, because home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao.

‘Prospective buyers aren’t as lucky. The combination of elevated mortgage rates, high home prices and a limited pool of homes for sale means homeownership is about as unaffordable as ever.’

But not every homeowner has seen their property increase in value.

‘Home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao

Four metros saw declines in overall home value, according to Redfin.

Pandemic ‘boomtown’ Boise, in Idaho, saw prices decline 3.8 percent to a total of $123.9 billion and New York saw prices fall 1 percent to $2.4 trillion.

New Orleans prices went down 0.8 percent to $124 billion and homes in Stockton, California, lost 0.7 percent in value – falling to a total of $109.2 billion in value.

The metros with the smallest increases were Philadelphia, at 0.3 percent, Honolulu, at 0.8 percent, Austin, Texas, at 1 percent, Denver at 1.3 percent and Riverside, California at 1.6 percent.

Most of these metros have something in common, said Redfin, which is that they have become unaffordable for many homebuyers. This means that there is a cap on demand, so home values no longer have much, if any, room to rise.

New York, Honolulu, Riverside and Denver all have median home sale prices of at least $550,000 – well above the national median.

And in Boise and Austin, which also have median sale prices above the national level, many people are priced out because an influx of out-of-towners caused home values to skyrocket during the pandemic.

But some experts predict that there will be a shift in the housing market in some parts of the US in 2024, driven by a surge in Baby Boomers downsizing into smaller properties.

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’ after she correctly predicted the 2008 financial crash, said house prices in some states will fall this year.

So-called pandemic ‘boomtown’ Boise, Idaho, saw prices decline 3.8 percent to a total of $123.9 billion in December 2023 – the most of any metro

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’, said house prices in some states will fall this year

This, in turn, will free up inventory and bring costs down for first-time buyers.

Whitney said homes in New York, New Jersey and Ohio will see a fall in prices. By comparison, homes in Texas, Tennessee and Utah will remain strong, she said.

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

The numbers: Home prices in the 20 biggest U.S. metros rose for the 11th month in a row and hit a record high amid a persistent shortage of resale homes for sale.

The S&P CoreLogic Case-Shiller 20-city house price index rose 0.2% in December compared to the previous month.

Home prices in the 20 major U.S. metro markets were up 6.1% in the last 12 months ending in December.

A broader measure of home prices, the national index, rose 0.2% in December and was also up 5.5% over the past year. All numbers are seasonally adjusted.

The 20-city and the national index are at an all-time high.

Key details: San Diego posted the biggest year-over-year home-price gains in December. Prices were up 8.8%.

All 20 major markets reported yearly gains for the first time in 2023, S&P said.

Home prices rose the slowest in Portland, increasing by 0.3%.

| Cities | Change from last year |

| Atlanta | 6.3% |

| Boston | 7.2% |

| Charlotte | 8% |

| Chicago | 8.1% |

| Cleveland | 7.4% |

| Dallas | 2.1% |

| Denver | 2.3% |

| Detroit | 8.3% |

| Las Vegas | 4.2% |

| Los Angeles | 8.3% |

| Miami | 7.8% |

| Minneapolis | 2.9% |

| New York | 7.6% |

| Phoenix | 3.8% |

| Portland | 0.3% |

| San Diego | 8.8% |

| San Francisco | 3.2% |

| Seattle | 3% |

| Tampa | 4.1% |

| Washington | 5.1% |

| Composite-20 | 6.1% |

A separate report from the Federal Housing Finance Agency also showed home prices rose 0.1% in December from the last month, and were up 6.6% in the past year.

The FHA also noted that the housing market has experienced annual home price growth every quarter since the start of 2012.

The median price of a resale home was $382,600 in December 2023, and a newly built home was $413,200.

Big picture: Even though rates went to 8% in 2023 and dried up demand, that did not push down home prices significantly, per the Case-Shiller index. However early analysis of the data indicates that some markets are seeing home price declines.

But with the 30-year dropping below 7% in December, home prices may see a boost as demand picks up. And with a persistent and severe shortage of homes for sale, home prices could be pressured upwards again.

What S&P said: “Looking back at the year, 2023 appears to have exceeded average annual home price gains over the past 35 years,” Brian D. Luke, head of commodities, real & digital assets at S&P Dow Jones Indices, said in a statement.

“While we are not experiencing the double-digit gains seen in the previous two years, above-trend growth should be well received considering the rising costs of financing home mortgages,” he added.

And the company said it was able to see the early impact of higher rates on home prices. “Increased financing costs appeared to precipitate home price declines in the fourth quarter, as 15 markets saw lower values compared to September,” Luke noted.

Americans are staying in their homes before selling up for twice as long as they did in 2005 – and baby boomers are to blame.

The typical homeowner spends 11.5 years in their house today, up from 6.5 years two decades ago, according to a new report by Redfin.

Researchers said the trend is being driven by older homeowners who are not ‘financially incentivized’ to move. A lack of homes on the market pushes up prices.

It comes after former Oppenheimer analyst Meredith Whitney told DailyMail.com that the house prices will finally start to decline as more seniors start downsizing – thereby freeing up homes.

According to Redfin’s analysis of US Census Bureau data, homeowner tenure peaked at 13.4 years in 2020.

The typical homeowner spends 11.5 years in their house today, up from 6.5 years two decades ago, according to a new report by Redfin

It comes after former Oppenheimer analyst Meredith Whitney, pictured, told DailyMail.com that the house prices will finally start to decline as more seniors start downsizing – thereby freeing up homes

The analysis also found that millennials were more likely to stay in their homes for shorter periods, in part because they change jobs more frequently than older generations.

Two in five baby boomers – those born between 1946 and 1964 – have lived in their home for 20 or more years.

By comparison, less than 7 percent of millennials – born between 1981 and 1996 – have lived in their home for ten years or longer.

The report notes: ‘Most – 54 percent – of baby boomers who own homes own them free and clear with no outstanding mortgage.

‘For that group, the median monthly cost of owning a home – which includes insurance and property taxes among other things – is just over $600.

‘Nearly all boomers who do have a mortgage have a much lower rate than they would if they sold and bought a new home with today’s 7 percent-ish rates.’

But researchers noted that older homeowners ‘hanging onto their homes’ is ‘an obstacle for young first-time buyers trying to break into the market.’

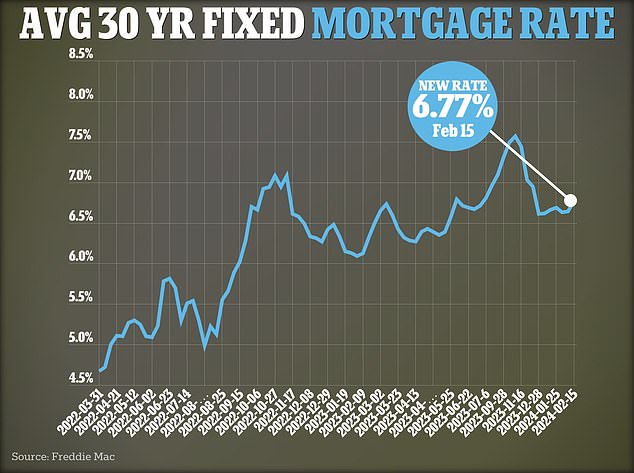

The average rate on a 30-year fixed home loan reached 6.77 percent, up from 6.64 percent last week, according to figures from Government-backed lender Freddie Mac

The findings echo comments made by Whitney, an analyst who was dubbed the ‘Oracle of Wall Street’ after she accurately predicted the 2008 financial crisis.

Her research shows that around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

However she claims a significant upheaval is in-store as more of these older owners start to sell up – freeing inventory and bringing prices down.

Whitney told DailyMail.com: ‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

During the pandemic the median US house price ballooned from $303,465 in March 2020 to $402,045 by December 2023, Redfin figures show.

Many families were embroiled in a so-called ‘race for space’ as they looked for bigger homes and gardens to spend lockdown. A widespread shift to working-from-home also unchained workers from their city center properties.

But house prices have remained elevated ever since – despite mortgage rates soaring in response to the Federal Reserve‘s funds rate reaching a 22-year high.

The average rate on a 30-year mortgage is currently hovering at 6.77 – around double what they were two years ago, figures from Government-backed lender Freddie Mac show.

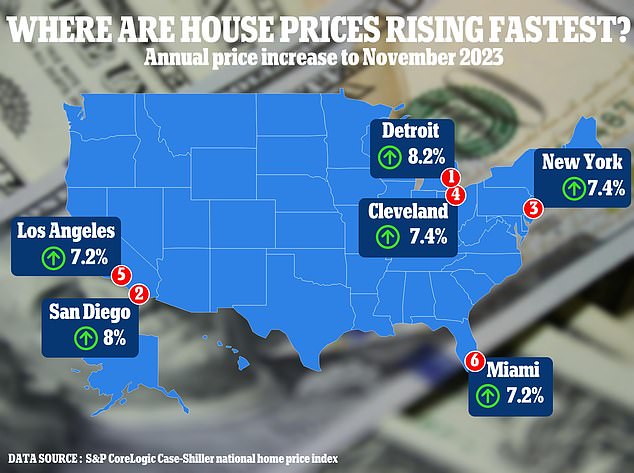

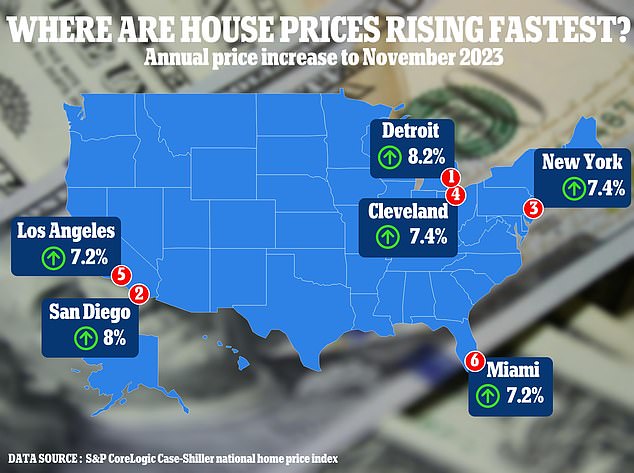

In the year to November 2023, property prices in Detroit increased 8.2 percent, according to latest data from the leading measure of US house prices

A recent report by CoreLogic shows how property prices have shot up in certain US metros

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

She notes that in the last decade homeowners have built up $21 trillion in equity in their homes – so any price falls is unlikely to seriously harm them.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

- Meredith Whitney accurately predicted the 2008 financial crisis

- Now she claims US housing market is in the midst of a major shift

- It marks a reversal of the pandemic-inspired housing boom

America’s real estate landscape is in the midst of a major upheaval that will make homes more affordable to first-time buyers, claims a former Oppenheimer analyst.

Meredith Whitney earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis.

Now she claims house prices are on the brink of decline after the pandemic inspired a real estate boom that saw the average property shoot up over $100,000 in value in less than four years.

However, she said the trend will be geo-specific with the likes of New York, New Jersey and Ohio worst-affected. By comparison, homes in Texas, Tennessee and Utah are among the states set to remain strong.

The shift will be driven by a surge in Baby Boomers downsizing into smaller properties – freeing up inventory and bringing costs down for first-time buyers, Whitney said.

Meredith Whitney, pictured, earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis

In the year to November 2023, property prices in Detroit increased 8.2 percent, according to latest data from the leading measure of US house prices

A recent report by CoreLogic shows how property prices have shot up in certain US metros

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

During the pandemic the median US house price ballooned from $303,465 in March 2020 to $402,045 by December 2023, Redfin figures show.

Many families were embroiled in a so-called ‘race for space’ as they looked for bigger homes and gardens to spend lockdown. A widespread shift to working-from-home also unchained workers from their city center properties.

But house prices have remained elevated ever since – despite mortgage rates soaring in response to the Federal Reserve’s funds rate reaching a 22-year high.

The average rate on a 30-year mortgage is currently hovering at 6.77 – around double what they were two years ago, figures from Government-backed lender Freddie Mac show.

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Whitney told DailyMail.com: ‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later’

The average rate on a 30-year fixed home loan reached 6.77 percent, up from 6.64 percent last week, according to figures from Government-backed lender Freddie Mac

Data from Redfin shows that the typical US homeowner now spends twice as long in their properties as they did in 2005.

Today an owner can expect to spend 11.9 years in the same property, compared to 6.5 years two decades ago.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

She notes that in the last decade homeowners have built up $21 trillion in equity in their homes – so any price falls is unlikely to seriously harm them.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

‘But New York, New Jersey, Ohio and Illinois will see an outmigration of population meaning there will be no growth in their housing markets.’