Inflation is not only cramping Americans’ food and energy budgets, but it’s taking a bite out of the housing market. The combination of high interest rates and high prices continues to stifle the residential real estate market. The latest data shows mortgage applications have dropped for three straight weeks, while the average rate on a 30-year fixed mortgage has risen to 6.82%, up more than a half-percent from a year ago. At the same time, the average home price in the U.S. is at a record high. “Taking into account mortgage rates, incomes, and house prices, affordability right now is strained at the worst levels in about four decades,” says Lance Lambert, CEO of the real estate analytics firm ResiClub, in a recent interview with Fox Business.

With limited supply keeping prices elevated and the Federal Reserve keeping interest rates high to counter inflation, the market is caught in the perfect storm for buyers and sellers. “A lot of home buyers can’t get in, and a lot of home sellers can’t sell and buy something else because they can’t afford those new monthly payments,” says Lambert.

Faced with this latest economic challenge in an election year, the Biden administration is doing what it does best: blaming someone else. The same administration that tried to blame high gas prices on greedy gas station owners, and high food prices on ‘price-gouging’ corporations, is now blaming high home prices on…you guessed it…greedy real estate agents. “They’re scapegoating,” says Lambert. “They act like lowering commissions would improve housing affordability…you know, going after soccer moms making $60,000 a year, because that’s the only job that works around their kids’ schedule.”

Rather than attacking realtors, the administration should be implementing policies to increase housing supply and reduce inflation, according to Lambert. “Putting in tax policy that works for new construction and not against new construction, lower fees on homebuilding, all the boring stuff that would increase supply in the long-term…that is what would improve housing affordability,” he says.

If you’re thinking of buying a home, there’s no day like today to make the move, says Barbara Corcoran.

The rate on the benchmark 30-year fixed mortgage declined slightly to 6.79% last week, well below October’s peak of 7.79%, according to Freddie Mac. For homebuyers, the prospect of waiting for lower borrowing cost might seem awfully enticing.

But Corcoran, Shark Tank star and founder of the Corcoran Group, begs to differ.

In a conversation on Yahoo Finance Live, Corcoran cautioned lower rates could bring more buyers into the market, boosting competition and sending already lofty prices “through the roof.”

“If interest rates come down another point by year end, everybody and their mother and their in-laws are going to look for a new house, and the competition’s gonna be so fierce that house prices will have to go up,” Corcoran said.

Home prices grew at a record pace in January, as more buyers came off the sidelines. And that fierce competition has led to an eruption of bidding wars, which often drives prices even higher.

National Association of Realtors (NAR) data shows that during the first month of the year, the typical seller received 2.7 offers, and 16% of homes sold over the asking price.

An important contributor to all of this is an inventory crunch. In 2023, existing home sales hit the lowest level since 2005, as would-be sellers who are locked into low mortgage rates stayed put.

“There is such a shortage of houses right now, so prices have gone up despite everybody singing the blues,” Corcoran said. “It happened simply because there are a lot of buyers and not enough houses available.”

Supply is slowly improving. New listings jumped 3.8% in February to the highest level in 17 months, while the total supply of homes for sale rose to the highest level in a year, according to Redfin.

It’s a sign buyers and sellers are getting more comfortable with higher mortgage rates, says Lawrence Yun, NAR’s chief economist.

“More people are adjusting to the new normal for mortgage rates, which appears to be between 6% and 7%,” Yun said on Yahoo Finance Live. “There is a sizable group of delayed sellers who have been postponing, and they will begin to list their property.”

While more new listings signals good news for buyers, a dramatic improvement in inventory may take some time. Top economist Mark Zandi warned the market’s recovery will take “several years” to materialize.

“We can say with strong conviction that the housing market in terms of home sales and demand has probably bottomed,” Zandi explained. “Everything indicates [the 30-year mortgage rate] will likely go to 6% rather than 8%, and if that’s the case, we should start to see improvement, but this is a process.”

So what should you do if you’re on the sidelines, hoping for mortgage rates to drop or more home to come on the market? Corcoran’s advice is simple: Don’t wait. She advises that “right now” is always the best time to buy, and to give yourself an edge in a tight market, “write a love letter” to the owners of the house you’re eyeing.

“Run into a community, see which houses you like and leave love notes on every door,” said Corcoran, who suggested crafting a personal message around what you like about the home, even if it’s not for sale.

“It works. The last four houses I bought were not on the market. I just picked out the house I like best and eventually the people called [back],” she said.

Seana Smith is an anchor at Yahoo Finance. Follow Smith on Twitter @SeanaNSmith. Tips on deals, mergers, activist situations, or anything else? Email seanasmith@yahooinc.com.

-

Zillow reported that a wave of new inventory hit the market in February.

-

New listings of existing homes on Zillow jumped 21% year-over-year last month.

-

The data suggest the “lock-in” effect and frozen housing market are softening.

High mortgage rates, elevated home prices, and tight inventory have kept many Americans sidelined from the housing market since the pandemic.

However, the “lock-in” effect — current owners being unwilling to move or refinance at higher rates — is showing signs of easing as more sellers begin to put their homes up for sale. Zillow data out Thursday showed new listings of existing homes jumped 20.8% in February compared to the same time in 2023, and climbed 20.3% month-over-month.

Not only that, but homeowner surveys suggest an increasing share of homeowners expect to sell in the next three years, which suggests some households may be done waiting for rates to drop before they wade back into the market.

Zillow reported that total inventory in February climbed 3.4% from January and that there were 12% more active listings last month compared to a year ago.

Inventories grew the most in Dallas (38.8%), Tampa (30.7%), and Orlando (29.5%), and rose in 33 of the largest 50 US markets.

On Thursday rates on the average 30-year fixed mortgage edged higher to to 7.02%.

Even if mortgage rates decline this year, strategists at Capital Economics aren’t anticipating a meaningful uptick in homebuying activity. In fact, they don’t foresee an end in sight for rising prices in the near term, forecasting a 5% jump in house prices in 2024, above the consensus 3%.

“Even if mortgage rates fall to 6% as we expect, mortgage rate ‘lock in’ will continue to curb home moves,” the strategists said. “As a result, we only anticipate a trickle of new resale supply coming onto the market over the next few years.”

Read the original article on Business Insider

There are more sellers putting their homes on the market but the outlook remains cautious because of ongoing uncertainty around interest rate cuts, surveyors have warned.

Over a fifth, 21%, of property professionals reported new selling instructions are rising rather than falling, marking the strongest reading since October 2020, the Royal Institution of Chartered Surveyors (RICS) said.

On average, estate agents’ branches had 42 properties, the highest number recorded by RICS since February 2021, with those surveyed noting an increase in market appraisals during the month, compared with the same period last year.

Sarah Coles, Yahoo Finance UK columnist and head of personal finance at Hargreaves Lansdown, warned that despite the encouraging figures, the property market might still be struggling.

“The housing market inspired more confidence in February, as buyers slowly resurfaced, and optimism rose among estate agents. However, given the broader picture, there’s still a risk that February may not have been flying after all. It could just have been falling with style,” she said.

The proportion of UK mortgages in arrears has risen to its highest level since 2016 as households continue to struggle with high interest rates.

The value of outstanding mortgage balances with arrears increased by 9.2% between October and December from the previous quarter, to £20.3bn, and was 50.3% higher than a year earlier, according to Bank of England data.

“There’s also less positive news from the mortgage market in recent weeks. Many of those agreeing sales at the moment will have agreed their mortgages back when rates were slightly lower. Since then, the market has reassessed the chances of an imminent rate cut, and put mortgage rates up.

“The average 2-year rate dropped from 5.93% on the 2 January to 5.56% at the end of the month, according to Moneyfacts. However, by the end of February, the average 2-year mortgage rate was back up to 5.75%. It could stifle demand as the impact feeds into the market,” Coles added.

Across the UK, new buyer inquiries grew for the second month in a row, with a net balance of 6% of professionals reporting a rise rather than a fall.

Most areas of the UK have shown a recovery in buyer interest over the past two months, the report said.

However, home sales were broadly flat in February, with a balance of 3% of professionals reporting a decline rather than an increase.

Simon Rubinsohn, RICS chief economist, said: “The February RICS survey provides some grounds for encouragement around the sales market with not just buyer interest staying positive for the second successive month, but also the uplift in new instructions to agents.”

Looking ahead, the sales expectations for the near term are positive and sales activity is expected to gain further momentum over the year ahead, the report said.

Markets are now pricing in three 0.25% cuts from the Bank of England by the end of the year, having forecast just short of three full cuts before the data came out.

In the lettings market, tenant demand continues to rise but at a more modest pace than previously, according to RICS.

At the same time, however, landlord instructions are still dwindling. Professionals were expecting rents to move higher over the months ahead, albeit at a slower rate.

Tom Bill, head of UK residential research at estate agent Knight Frank, said: “The economic data has fluctuated since Christmas but the direction of travel for the housing market is up.”

Watch: House prices are up, Nationwide says

Download the Yahoo Finance app, available for Apple and Android.

Affiliate links for the products on this page are from partners that compensate us (see our advertiser disclosure with our list of partners for more details). However, our opinions are our own. See how we rate mortgages to write unbiased product reviews.

Mortgage rates initially ticked up a little bit following the release of Tuesday’s slightly hotter-than-expected Consumer Price Index data. But they’ve since trended back down and remain well below last month’s levels. Rates are still expected to go down this year.

Last month, average 30-year mortgage rates rose to 6.52%. So far this month, they’ve been trending a bit lower, and they could drop below 6% by the end of the year, according to Fannie Mae’s latest forecast.

But mortgage rates probably won’t drop substantially until we get more data showing that inflation is continuing to slow.

In February, prices rose 3.2% year over year, according to the Bureau of Labor Statistics. This is a slight uptick from the previous month, which showed prices rising 3.1% on an annual basis.

Federal Reserve officials want to see more data that inflation is coming down before they start lowering the federal funds rate. Once we get closer to a likely Fed cut, mortgage rates should start to fall.

Right now, investors still believe the Fed could start cutting rates as soon as June, according to the CME FedWatch Tool. So we could see mortgage rates go down in just a few months.

Mortgage Rates Today

| Mortgage type | Average rate today |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mortgage Refinance Rates Today

| Mortgage type | Average rate today |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Mortgage Calculator

Use our free mortgage calculator to see how today’s mortgage rates will affect your monthly and long-term payments.

Mortgage Calculator

$1,161

Your estimated monthly payment

- Paying a 25% higher down payment would save you $8,916.08 on interest charges

- Lowering the interest rate by 1% would save you $51,562.03

- Paying an additional $500 each month would reduce the loan length by 146 months

By plugging in different term lengths and interest rates, you’ll see how your monthly payment could change.

Mortgage Rate Projection for 2024

Mortgage rates increased dramatically for most of 2023, though they started trending back down in the final months of the year. As the economy continues to normalize this year, rates should come down even further.

In the last 12 months, the Consumer Price Index rose by 3.2%, a significant slowdown compared to when it peaked at 9.1% in 2022. This is good news for mortgage rates — as inflation slows and the Federal Reserve is able to start cutting the federal funds rate, mortgage rates are expected to trend down as well.

For homeowners looking to leverage their home’s value to cover a big purchase — such as a home renovation — a home equity line of credit (HELOC) may be a good option while we wait for mortgage rates to ease. Check out some of the best HELOC lenders to start your search for the right loan for you.

A HELOC is a line of credit that lets you borrow against the equity in your home. It works similarly to a credit card in that you borrow what you need rather than getting the full amount you’re borrowing in a lump sum. It also lets you tap into the money you have in your home without replacing your entire mortgage, like you’d do with a cash-out refinance.

Current HELOC rates are relatively low compared to other loan options, including credit cards and personal loans.

When Will House Prices Come Down?

We aren’t likely to see home prices drop anytime soon thanks to extremely limited supply. In fact, they’ll likely rise this year as mortgage rates drop.

Fannie Mae researchers expect prices to increase 3.2% in 2024, while the Mortgage Bankers Association expects a 4.1% increase in 2024.

Lower mortgage rates will bring more buyers onto the market, putting upward pressure on prices. But prices aren’t currently expected to increase as much as they have in recent years.

Fixed-Rate vs. Adjustable-Rate Mortgage Pros and Cons

Fixed-rate mortgages lock in your rate for the entire life of your loan. Adjustable-rate mortgages lock in your rate for the first few years, then your rate goes up or down periodically.

So how do you choose between a fixed-rate vs. adjustable-rate mortgage?

ARMs typically start with lower rates than fixed-rate mortgages, but ARM rates can go up once your initial introductory period is over. If you plan on moving or refinancing before the rate adjusts, an ARM could be a good deal. But keep in mind that a change in circumstances could prevent you from doing these things, so it’s a good idea to think about whether your budget could handle a higher monthly payment.

Fixed-rate mortgage are a good choice for borrowers who want stability, since your monthly principal and interest payments won’t change throughout the life of the loan (though your mortgage payment could increase if your taxes or insurance go up).

But in exchange for this stability, you’ll take on a higher rate. This might seem like a bad deal right now, but if rates increase further down the road, you might be glad to have a rate locked in. And if rates trend down, you may be able to refinance to snag a lower rate

How Does an Adjustable-Rate Mortgage Work?

Adjustable-rate mortgages start with an introductory period where your rate will remain fixed for a certain period of time. Once that period is up, it will begin to adjust periodically — typically once per year or once every six months.

How much your rate will change depends on the index that the ARM uses and the margin set by the lender. Lenders choose the index that their ARMs use, and this rate can trend up or down depending on current market conditions.

The margin is the amount of interest a lender charges on top of the index. You should shop around with multiple lenders to see which one offers the lowest margin.

ARMs also come with limits on how much they can change and how high they can go. For example, an ARM might be limited to a 2% increase or decrease every time it adjusts, with a maximum rate of 8%.

-

Mortgage rates eased for the first time in five weeks, Freddie Mac said Thursday.

-

At the same time, newly listed homes climbed 13% year-over-year in the four weeks to March 3.

-

Easing affordability and improving inventory suggests a gradual thawing of the market.

The US housing market has been mostly frozen since the pandemic boom, but fresh data out Thursday suggests signs of a spring thaw.

Freddie Mac reported that rates on the most popular home loan fell for the first time in five weeks to hit 6.88%, down from 6.94% the prior week. At the same time, the number of newly listed homes in the four weeks to March 3 spiked 13% compared to one year ago.

Easing borrowing costs and an uptick in available inventory together offer a welcome signal for Americans seeking homes. It also points to a softening of the “lock-in” effect — current owners being unwilling to move or refinance at higher interest rates — that’s kept housing market activity muted. It wasn’t long ago that house hunters and current owners could lock in a 3% rate on their mortgage.

Indeed, an uptick in demand was evident in Freddie Mac’s latest report, as mortgage applications rose for the first time in six weeks amid the dip in rates.

“Mortgage rates continue to be one of the biggest hurdles for potential homebuyers looking to enter the market,” Sam Khater, Freddie Mac’s chief economist, said in a statement. “It’s important to remember that rates can vary widely between mortgage lenders so shopping around is essential.”

Mortgage rates have dipped this week amid the renewed outlook for rate cuts this year, as Fed Chair Jerome Powell testified to Congress that the central bank is still looking to loosen monetary policy in 2024.

Meanwhile, Realtor.com on Tuesday reported that February saw 339,370 homes for sale, roughly an 11% increase compared to the same month in 2023. While that’s still about 17% below pre-pandemic levels in 2019, the upward trend is there.

However, Capital Economics strategists wrote earlier in the week that easing mortgage rates won’t be enough to spark a meaningful, lasting rebound in home demand. The research firm expects house prices to climb 5% in 2024, which is above the consensus forecast of 3%.

“Even if mortgage rates fall to 6% as we expect, mortgage rate ‘lock in’ will continue to curb home moves,” Capital Economics strategists wrote in a note. “As a result, we only anticipate a trickle of new resale supply coming onto the market over the next few years.”

Read the original article on Business Insider

-

Easing mortgage rates won’t fully unwind the “lock in” effect, Capital Economics said.

-

Home moves and market activity will remain muted even if borrowing costs become more attractive.

-

Rising buyer demand and low inventory will drive prices 5% higher this year, the firm said.

The frozen US housing market may not fully thaw for years to come, according to Capital Economics.

Since the pandemic housing boom, a combination of near-7% mortgage rates, low inventory, and high home prices has created a “lock-in” effect, making current homeowners unwilling to move because it would require taking on a new, higher mortgage rate. That in turn keeps many buyers and sellers from participating in the market.

In a note Tuesday, the firm said easing mortgage rates won’t be enough to spark a meaningful uptick in homebuying activity, and that there’s no end in sight for rising home prices.

“Even if mortgage rates fall to 6% as we expect, mortgage rate ‘lock in’ will continue to curb home moves,” Capital Economics strategists said. “As a result, we only anticipate a trickle of new resale supply coming onto the market over the next few years.”

Capital Economics forecasts a 5% rise in house prices this year, higher than the consensus 3% jump. In the research group’s view, housing market activity will remain muted as competition for homes stays tight and affordability remains historically low.

The strategists expect mortgage rates, too, will continue to trend above pre-pandemic levels. Easing Fed interest rates and reduced market uncertainty could help bring mortgage rates to 6.5% by the end of 2024, and 6.0% by the end of 2024.

That said, Capital Economics doesn’t expect dramatic changes as far as how much it costs Americans to afford monthly home payments.

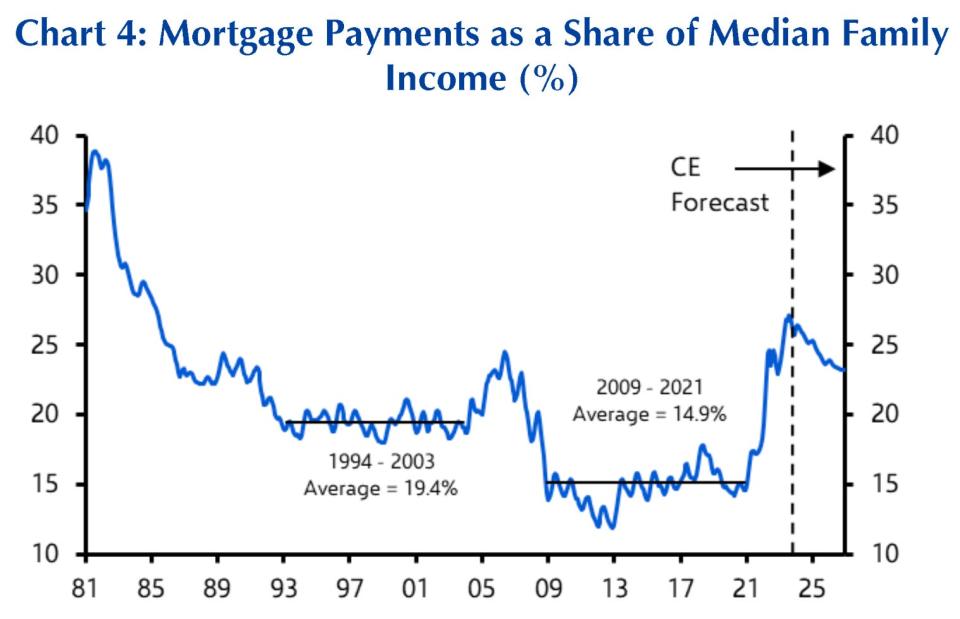

Mortgage payments as a share of income hovers at 25.7% currently, and the strategists said that could fall to 23.1% by the end of next year, as illustrated in the chart below.

“The bigger picture is that the market will remain practically frozen,” the Capital Economics team said. “The biggest constraint on activity in recent years has been the lack of available homes for sale due to mortgage rate ‘lock-in.’ We don’t expect that to change much.”

Read the original article on Business Insider

After nine months of steadily increasing housing prices in the U.S., price growth has now decreased for the second month in a row.

Housing prices were on the rise for a long stretch of nine months in 2023 — until November. That month’s small drop of 0.2 percent continued into December: S&P CoreLogic’s latest Case-Shiller U.S. National Home Price NSA Index, released February 27, 2024, reports that home-price growth dropped in December 2023 by 0.4 percent. In fact, 17 of the 20 major metro markets measured by Case-Shiller reported month-over-month price decreases.

Case-Shiller Index still up compared to last year

While the month-over-month numbers show a slight decrease, the index is still up by 5.5 percent from last December. The 10- and 20-city composites each also rose year-over-year, by 7.0 percent and and 6.1 percent respectively.

“U.S. home prices faced significant headwinds in the fourth quarter of 2023,” said Brian D. Luke, head of commodities, real & digital assets at S&P DJI, in a statement. “However, on a seasonally adjusted basis, the S&P Case-Shiller Home Price Indices continued its streak of seven consecutive record highs in 2023. Looking back at the year, 2023 appears to have exceeded average annual home price gains over the past 35 years.”

Regional fluctuation continues

“All 20 markets reported yearly gains for the first time this year,” Luke said, with 10 of 20 markets beating prior records in December. San Diego led the pack with an 8.8 percent year-over-year increase, followed by an 8.3 percent gain in both Los Angeles and Detroit. The next highest gains were reported in Chicago, up 8.1 percent, and Charlotte, up an even 8 percent. Despite the top-performing market being in the West, the Midwest and Northeast were the best-performing regions with 6.7 percent gains each.

The Fed and the housing market

The Federal Reserve’s aggressive moves to combat inflation — with 10 consecutive rate hikes over 2022 and 2023 — have put upward pressure on mortgage rates. While the Fed doesn’t directly set mortgage rates, the mortgage market’s interpretations of the central bank’s moves influence how much you pay for your home loan.

The long period of low mortgage rates following the Great Recession came to an end in 2022. In June 2022, rates topped 6 percent for the first time since 2008. The upward trend continued through October, when rates hit a 23-year high of 8 percent. “The house price decline came at a time where mortgage rates peaked,” Luke noted last month.

Steve Reich, division president at Go Mortgage in Pennsylvania, highlights the impacts that these trends have on the housing market. “As the Fed worked to get inflation under control, higher interest rates tempered what many homebuyers could afford and, in turn, softened home sales,” he said in a statement.

Higher rates also exacerbate the housing shortage, stopping many homeowners from selling when they otherwise might — and thus keeping those homes off the market and out of the supply of available housing.

— Mark Hamrick, Bankrate Senior Economic Analyst

“The remarkable rise in mortgage rates is acting as a kind of golden handcuffs,” says Mark Hamrick, Bankrate’s senior economic analyst. Higher rates are “limiting the desire and some of the ability of people to move out of the homes they currently own. That further pressures housing inventory, adding insult to supply injury.”

However, rates have begun trending back downward. As of February 21, 2024, the average 30-year mortgage rate sat at 7.13 percent.

What it means for homebuyers and sellers

The current market has proved challenging on both sides of the real estate transaction — and unless we see a significant drop in either home prices or mortgage rates, both buyers and sellers will need to go with the flow. “For prospective sellers, the new status quo dictates they remain flexible on price, given the extraordinary challenges posed by the sharp increase in mortgage rates,” Hamrick says.

“Those who are very motivated to purchase a home should be prepared for the sticker shock associated with the increased expense of financing the purchase,” he continues. “Part of the flexibility that may be required includes seeking a possible downgrade of footprint or quality of home, along with the neighborhood, in order to achieve an affordable purchase.”

Both buyers and sellers will want to keep a very close eye on mortgage rates in the coming months. “With home prices edging down for both the fourth quarter and December, it seems increases may have crested for now,” said Robert Frick, corporate economist with Navy Federal Credit Union. However, he continued, “If mortgage rates dip this year as expected, price increases may again revive as home demand improves.”

Reich emphasizes that buying a home in today’s market, while difficult, is still possible. “The average time active listings stay on the market is getting longer, resulting in a slightly less competitive market,” he says. National Association of Realtors data proves that out: The median days-on-market length was 36 days in January, up both month-over-month and year-over-year, which gives buyers more time to make an informed, well-considered decision. “And that’s good news for homebuyers who are still in the game.”

Almost as soon as home prices began their unprecedented climb in 2020, doomsayers began warning of a looming crisis. The housing market, they claimed, was a bubble destined to burst.

A litany of supposed catalysts was going to send prices into a tailspin: the “Airbnbust,” the sudden surge in mortgage rates, a flood of grifters and hucksters looking to make a quick buck in real estate. Bubble watchers forecast chaos, then sat back and waited. And waited. And waited.

I’ve spent the past few years asking experts a simple question: Has the housing market reached bubble territory? The answer remains a resounding no. More than three years after prices started to soar, the only thing that’s gone bust is the gloomy predictions. Despite some cooling in a handful of overheated markets such as Charlotte, North Carolina, and Austin, the median home-sale price increased by a respectable 4% nationwide in 2023, Redfin reported. The price for a typical home has risen by more than 47% since late 2019, according to the S&P CoreLogic Case-Shiller National Home Price Index, a closely watched measure of housing costs.

But maybe I’ve been posing the wrong question all along. The B-word implies an impending pop, a point when the combination of greedy speculation, unscrupulous behavior, and soaring prices brings everything crashing down. Barring a large-scale economic disaster, there’s no pop in sight.

The staggering jump in home prices is concerning, to be sure. But it’s a function of a severe lack of supply, not a byproduct of investors swarming the market or shady lenders artificially juicing demand. Those looking for parallels to 2008 are grasping at straws — homeowners are in far better financial shape than they were the last time prices cratered, and homebuilders, rather than flooding the market with new properties, aren’t keeping pace with the sheer volume of millennials suddenly consumed by dreams of backyards and picket fences.

So if you’ve been waiting — maybe even cheering — for prices to plummet: Don’t hold your breath.

Warning signs

A funny thing about bubbles is they don’t fall neatly into a single definition. Ask a dozen economists to sketch out their criteria, and you’ll probably get 12 different answers. But Mike Simonsen, the president of the housing research firm Altos Research, offered a useful way to think of a bubble’s life cycle in a post on X, formerly Twitter, late last year (which I’ve slightly paraphrased):

1. You got rich! Good for you! You did the hard work and got in early.

2. Hm. It seems like everyone is getting rich?

3. Wait. That asshole?! That guy is not smart, maybe even criminal.

4. Pop.

For a time, it seemed like the housing market was doing a speedrun through Simonsen’s checklist. There were the runaway prices: Before the pandemic, you could buy a median-price home in Las Vegas for about $281,300, according to Redfin. Good luck finding that kind of deal now — even with a dip from pandemic highs, the cost of a typical house there has swelled to $422,000, an eye-watering 50% increase. Similar stories have played out in Miami (70%), Boise, Idaho (40%), and Dallas (36%). The typical household would have to spend nearly 34% of its income to afford major homeownership expenses such as mortgage payments and property taxes, according to the data firm Attom, the highest percentage since 2007 and well beyond the 28% debt-to-income ratio that’s typically preferred by lenders.

Then there were the people getting rich. Speculators were using supercheap loans to buy homes, expecting to profit by selling to an even bigger fool; home flippers, aspiring megalandlords, and Airbnb owners flaunted their debt-funded miniempires on TikTok; and seemingly everyone was signing up to be a real-estate agent. Even usually buttoned-up real-estate professionals were giving off bubble vibes: High-flying mortgage companies threw lavish parties featuring bands such as Imagine Dragons, while Zillow, the ubiquitous home-search site, morphed into one of the country’s biggest homebuyers — even though its acquisition math didn’t add up.

All the signs seemed to point to a bubble, and there were plenty of people predicting the “pop” was coming: In late 2022, the prominent Wall Street economist Ian Shepherdson forecast home prices to fall by as much as 20% the following year. Goldman Sachs expected a more modest, but still significant, decline of up to 10% from the peak. Countless headlines wondered whether home values were set to crash. Even Federal Reserve Chair Jerome Powell, whose every word threatens to move markets, said at a Brookings Institution event in 2022 that housing was in a “bubble” during the pandemic, with “prices going up at very unsustainable levels.”

But there was no pop, no sudden collapse in home prices. Even with mortgage rates tripling and buyers retreating, values held up.

The gloomy oracles could even point to an instigator of the coming collapse. The Fed, led by Powell, began raising interest rates in spring 2022 to fight inflation, sending mortgage rates shooting upward. Mortgage rates kept rising through most of 2023, eventually reaching a 20-year high in October of nearly 8%, up from less than 3% during the depths of the pandemic in 2020 and 2021. Suddenly it wasn’t so cheap to borrow money, making it tougher for reckless investors to enter the market. Speculation is the oxygen for a market-frenzy fire, Rick Palacios Jr., the director of research and managing principal at John Burns Research and Consulting, told me. By hiking rates, the Fed cut off the air supply.

But there was no pop, no sudden collapse in home prices. Even with mortgage rates tripling and buyers retreating, values held up. To understand why, you have to look at the fundamentals — the deep-seated reasons all the “Bubble Boys,” doomsayers, and fear-mongering headlines are dead wrong.

Debunking the bubble

Rising prices, no matter how steep, aren’t enough to constitute a bubble. Prices also need to diverge from the fundamentals, or the basic components of supply and demand, that determine how much things cost. If the run-up in prices defies logical explanation or obscures sketchy business practices, watch out. In the years leading up to the global financial crisis, for instance, lenders came up with creative ways to boost demand: They devised predatory mortgages that left borrowers on the hook for impossibly high payments once their teaser rates expired and handed out so-called NINJA loans (no income, no job, and no assets). If you owned a home at that time, you might’ve felt like the only direction its value could go was up.

The recent housing-bubble theory was always going to age poorly because of one fact: The pandemic soaring prices were justified. Prices didn’t spiral out of control because we built too many homes or made it too easy to borrow money, like in 2008; they took off because there simply weren’t enough homes for all the creditworthy people who wanted to buy them.

It’s a savagely unhealthy housing market. But it’s also a market that just had too many people chasing too few homes.

For home prices to suddenly crash, there would have to be a pool of desperate sellers looking to offload their homes on the cheap — or, worse, losing them to the foreclosure process. Sure, speculators were loud and proud about their get-rich-quick schemes, but they were a vocal minority. And regular homeowners have “never looked this good” when it comes to their financial and credit health, Logan Mohtashami, the lead analyst at HousingWire and an outspoken critic of bubble alarmists, told me. Less than 4% of outstanding mortgages were delinquent at the end of the third quarter last year, according to the Mortgage Bankers Association, a near-record low. In the fourth quarter of 2023, the median credit score for people getting a new mortgage was a stellar 770, according to the Federal Reserve Bank of New York. (Lenders typically consider a score above 700 to be a marker of future success for a borrower.) Almost 79% of homeowners with a mortgage have locked in a rate below 5%, a Redfin analysis of data from the Federal Housing Finance Agency found. In the history of rates, that’s a pretty incredible deal. And nearly 40% of homeowners don’t even have to stress about mortgage payments at all, according to census data — they own their homes free and clear.

Rather than facing a housing bubble, we’re staring down an entirely different crisis: a supply shortage that has regular buyers fighting just to break into the market. US homebuilders spent the decade after the global financial crisis building at about half the rate of the three decades prior, contributing to the housing crunch. Various estimates have pegged the national housing shortage anywhere between 2 million and 6 million homes. The supply constraint hit right as millennials, the largest living generation in the US, reached their prime homebuying years. Add in people’s sudden desire for a bigger house or a place of their own in the heat of the pandemic, and the recent surge in home prices seems less bubbly and more logical. The lack of inventory is the reason prices didn’t suddenly drop, even when mortgage rates shot up. Sure, buyers pulled back. But sellers pulled back even more, leaving the supply-demand imbalance in place.

“It’s a savagely unhealthy housing market,” Mohtashami told me. “But it’s also a market that just had too many people chasing too few homes.”

Staying high

It’s tempting to look for echoes of 2008 in today’s housing market. You might even be inclined to cheer on a crash in prices — all the better for everyone who feels locked out of homeownership. But cycles rarely repeat in the same way, Selma Hepp, the chief economist at CoreLogic, told me. Anything that could incite a housing crash probably wouldn’t leave average consumers in a position to suddenly pounce on all that excess inventory.

Fannie Mae now projects a modest 3.2% increase in home prices this year and a jump in home sales, along with a decline in mortgage rates. Goldman Sachs predicts a 5% rise in home prices. John Burns Research and Consulting doesn’t publish an exact forecast of home prices, but Palacios told me the firm expected to see a similar increase in the “low single digits.”

Perhaps the biggest threat to the housing market at large is a severe economic slowdown, one in which many people lose their jobs and can’t pay their mortgages. It’s notoriously difficult to estimate where the economy is headed, but right now, it’s roaring along, especially compared with other rich countries. Things aren’t perfect, but the vibes are definitely up. And even if the economy does take a turn, a run-of-the-mill recession probably wouldn’t be enough to topple the housing market. Things would have to get so bad that banks would be forced to walk away from the mortgage-lending space almost entirely, as they did during the foreclosure crisis. If the market is cratering and nobody can get a mortgage to put a floor on prices, “that’s where you get pretty meaningful declines in asset prices,” Palacios said.

There’s a silver lining baked into all this: Prices aren’t poised to drop, but the days of skyrocketing valuations appear to be behind us, Mohtashami told me. The housing market is far from balanced, but we’re at least heading in that direction.

After the past few years, the lingering fears of a sudden fallout are just a distraction from the bigger issues at hand. The bubble debate was fun; now it’s time to put it to bed.

James Rodriguez is a senior reporter on Business Insider’s Discourse team.

UK house prices rose for the fourth consecutive month in January to the highest level since October 2022 as falling mortgage rates boosted the market.

Average house prices increased to £291,029 in January, which was £3,900 more than last month, according to the Halifax house price index.

The survey showed that property values increased by 1.3% in January compared to the previous month.

Compared to the same month last year, property prices grew by 2.5%, which was the highest annual growth since January 2023.

It was the fourth monthly gain in a row after six consecutive falls before that.

Read more: What is the First Homes scheme and who is eligible?

Halifax mortgage director, Kim Kinnaird, said: ““The recent reduction of mortgage rates from lenders as competition picks up, alongside fading inflationary pressures and a still-resilient labour market has contributed to increased confidence among buyers and sellers. This has resulted in a positive start to 2024’s housing market.

“However, while housing activity has increased over recent months, interest rates remain elevated compared to the historic lows seen in recent years and demand continues to exceed supply. For those looking to buy a first home, the average deposit raised is now £53,414, around 19% of the purchase price. It’s not surprising that almost two thirds (63%) of new buyers getting a foot on the ladder are now buying in joint names.”

In London, the average price was down 0.4% year-on-year at £529,528, bucking the wider trend of growth.

Northern Ireland recorded the strongest growth across all the nations or regions within the UK – house prices here increased by 5.3% on an annual basis.

Properties in Northern Ireland now cost on average £195,760, which is £9,761 higher than the same time in January 2023.

Read more: State pension age needs to jump to 71, says think tank

Scotland and Wales both saw growth, 4% on an annual basis to £206,087 and £219,609 respectively. North West (3.2%), Yorkshire and Humber (2.8%), North East (2.0%) and East Midlands (0.5%) also recorded house price increases over the last year.

The South East fell the most last month when compared to other UK regions, with homes selling for an average £379,220 (-2.3%), a drop of £8,866.

Alice Haine, personal finance analyst at Bestinvest by Evelyn Partners, the wealth manager, said: “Interest rates have remained on pause at a 16-year high of 5.25% since August 2023 and, with inflation expected to retreat rapidly in the coming months, cuts are expected as soon as the summer.

“The improving outlook has resulted in better mortgage rates and affordability levels for first-time buyers and those looking to refinance.”

The increase in house prices for a fourth month in a row puts Britain about halfway towards a 3% increase in house prices this year already, according to economists.

Andrew Wishart, senior property economist at Capital Economics, said: “The Halifax index has a track record of being quick to respond to changes in mortgage rates, so the large increases of 1.1% in December and 1.3% in January reflect the swift drop in the average quoted mortgage rate from 5% in November to about 4.5% in January.

“Fixed mortgage rates are unlikely to fall any further in the near term, which will restrain future monthly gains in the Halifax index.”

The average rate on a two-year fixed deal this week stood at 5.55% while for a five-year deal, rates came down to 5.09%, according to figures from Uswitch.

Sarah Coles, Yahoo Finance UK columnist and head of personal finance at Hargreaves Lansdown, said: “We’re still a long way from a sellers’ market, but if you have been trying in vain to persuade buyers to see your home for months, it’s a really positive development. However, sellers shouldn’t get carried away with pricing, because this bounce may not last.”

Watch: How much money do I need to buy a house?

Download the Yahoo Finance app, available for Apple and Android.