The US housing market gained a huge $2 trillion over the last year, amid a historic shortage of homes for sale.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023, up from $474,740 a year earlier.

According to Redfin analysis of more than 90 million homes across the country, the total value of US residential real estate increased 5.3 percent from a year earlier to $47.5 trillion in December.

While soaring mortgage rates mean housing demand is sluggish, home values continue to rise, pricing many Americans out of the market.

In the last two years, the housing market has gained $5.6 trillion, Redfin found.

However a disparity remains across the US. While affordable East Coast and Midwest metros saw the biggest rise in home values in the last year, so-called pandemic ‘boomtowns’ have seen the largest decline.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023. The biggest rises were on the east coast of America

Scroll down for the full list of metros with the biggest price rises.

According to Redfin, there are three major reasons why home values are continuing to rise.

Many homeowners are locked into ultra-low mortgage rates from previous years, meaning they are hesitant to put their houses on the market.

With supply tighter than demand, buyers are competing for a limited pool of homes. That is propping up values for both properties that are already for sale, and those that could hit the market in the future.

The total value of US homes was nearing a trough at the end of 2022, which is part of the reason year-over-year growth at the end of 2023 was so large, it added.

It is typical for home values to cool in the winter, but they experienced an abnormally large slowdown in 2022 as the shock of surging mortgage rates sent a freeze through the housing market.

While America grapples with a housing shortage, it is also continuing to build homes, which contributed to the gain in total home values last year, Redfin said.

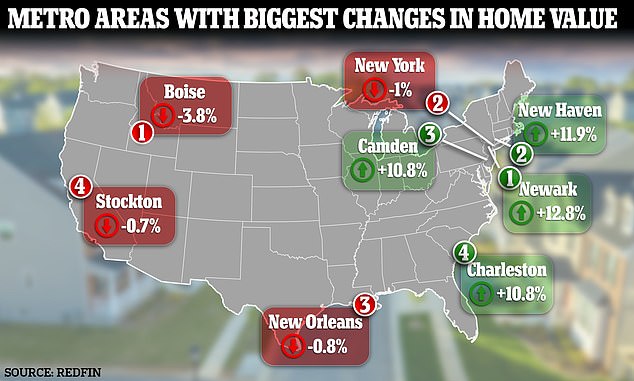

Home values in Newark, New Jersey, saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion.

Next come two other East Coast metros, New Haven, Connecticut, and Camden, New Jersey. Homes in New Haven gained 11.9 percent in value to $86.5 billion, while properties in Camden went up by 10.8 percent to $153 billion.

Home values in Newark, New Jersey , saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion

Fixed 30-year mortgage rates are now hovering around 6.9 percent, according to Government-backed lender Freddie Mac

Charleston, South Carolina, ranked fourth – with values increasing by 10.8 percent to $188.5 billion.

Next are three Midwestern metros, Elgin, Illinois, Grand Rapids, Michigan and Milwaukee, Wisconsin.

Places like Newark and Camden are likely seeing home values jump in part because they are attracting demand from people who are priced out of New York and can now work remotely, Redfin said.

Midwestern metros like Milwaukee and Grand Rapids are experiencing home value gains for a similar reason.

They are affordable, and when mortgage rates and home prices are elevated, demand for affordable homes goes up.

‘America’s homeowners are sitting pretty. They’re holding a massive amount of housing wealth, despite lackluster demand from buyers, because home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao.

‘Prospective buyers aren’t as lucky. The combination of elevated mortgage rates, high home prices and a limited pool of homes for sale means homeownership is about as unaffordable as ever.’

But not every homeowner has seen their property increase in value.

‘Home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao

Four metros saw declines in overall home value, according to Redfin.

Pandemic ‘boomtown’ Boise, in Idaho, saw prices decline 3.8 percent to a total of $123.9 billion and New York saw prices fall 1 percent to $2.4 trillion.

New Orleans prices went down 0.8 percent to $124 billion and homes in Stockton, California, lost 0.7 percent in value – falling to a total of $109.2 billion in value.

The metros with the smallest increases were Philadelphia, at 0.3 percent, Honolulu, at 0.8 percent, Austin, Texas, at 1 percent, Denver at 1.3 percent and Riverside, California at 1.6 percent.

Most of these metros have something in common, said Redfin, which is that they have become unaffordable for many homebuyers. This means that there is a cap on demand, so home values no longer have much, if any, room to rise.

New York, Honolulu, Riverside and Denver all have median home sale prices of at least $550,000 – well above the national median.

And in Boise and Austin, which also have median sale prices above the national level, many people are priced out because an influx of out-of-towners caused home values to skyrocket during the pandemic.

But some experts predict that there will be a shift in the housing market in some parts of the US in 2024, driven by a surge in Baby Boomers downsizing into smaller properties.

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’ after she correctly predicted the 2008 financial crash, said house prices in some states will fall this year.

So-called pandemic ‘boomtown’ Boise, Idaho, saw prices decline 3.8 percent to a total of $123.9 billion in December 2023 – the most of any metro

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’, said house prices in some states will fall this year

This, in turn, will free up inventory and bring costs down for first-time buyers.

Whitney said homes in New York, New Jersey and Ohio will see a fall in prices. By comparison, homes in Texas, Tennessee and Utah will remain strong, she said.

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

- Meredith Whitney accurately predicted the 2008 financial crisis

- Now she claims US housing market is in the midst of a major shift

- It marks a reversal of the pandemic-inspired housing boom

America’s real estate landscape is in the midst of a major upheaval that will make homes more affordable to first-time buyers, claims a former Oppenheimer analyst.

Meredith Whitney earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis.

Now she claims house prices are on the brink of decline after the pandemic inspired a real estate boom that saw the average property shoot up over $100,000 in value in less than four years.

However, she said the trend will be geo-specific with the likes of New York, New Jersey and Ohio worst-affected. By comparison, homes in Texas, Tennessee and Utah are among the states set to remain strong.

The shift will be driven by a surge in Baby Boomers downsizing into smaller properties – freeing up inventory and bringing costs down for first-time buyers, Whitney said.

Meredith Whitney, pictured, earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis

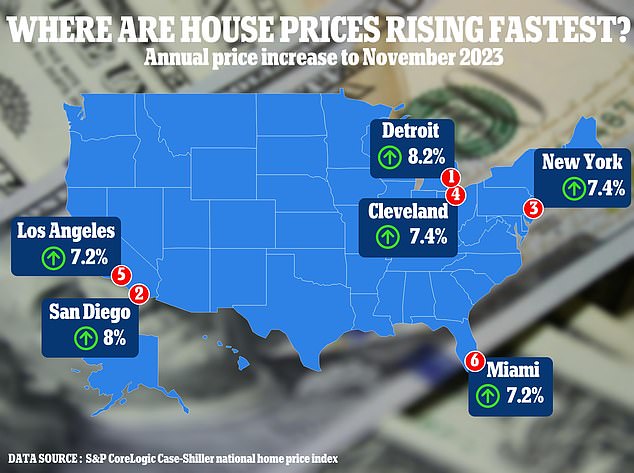

In the year to November 2023, property prices in Detroit increased 8.2 percent, according to latest data from the leading measure of US house prices

A recent report by CoreLogic shows how property prices have shot up in certain US metros

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

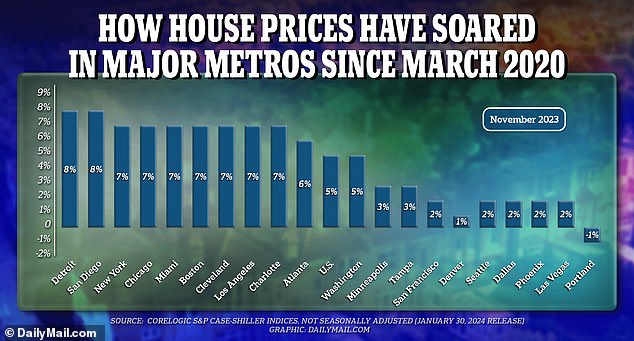

During the pandemic the median US house price ballooned from $303,465 in March 2020 to $402,045 by December 2023, Redfin figures show.

Many families were embroiled in a so-called ‘race for space’ as they looked for bigger homes and gardens to spend lockdown. A widespread shift to working-from-home also unchained workers from their city center properties.

But house prices have remained elevated ever since – despite mortgage rates soaring in response to the Federal Reserve’s funds rate reaching a 22-year high.

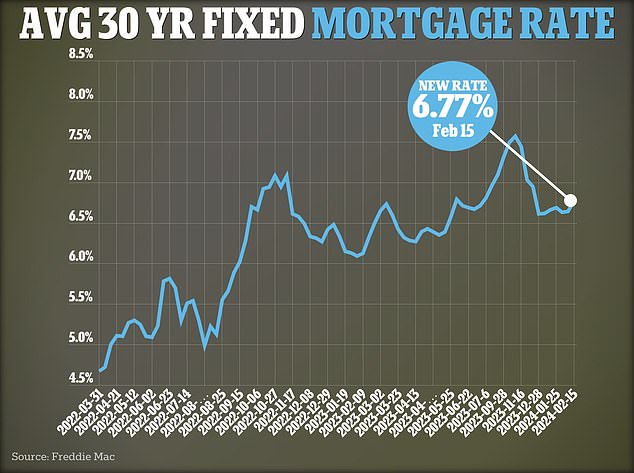

The average rate on a 30-year mortgage is currently hovering at 6.77 – around double what they were two years ago, figures from Government-backed lender Freddie Mac show.

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Whitney told DailyMail.com: ‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later’

The average rate on a 30-year fixed home loan reached 6.77 percent, up from 6.64 percent last week, according to figures from Government-backed lender Freddie Mac

Data from Redfin shows that the typical US homeowner now spends twice as long in their properties as they did in 2005.

Today an owner can expect to spend 11.9 years in the same property, compared to 6.5 years two decades ago.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

She notes that in the last decade homeowners have built up $21 trillion in equity in their homes – so any price falls is unlikely to seriously harm them.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

‘But New York, New Jersey, Ohio and Illinois will see an outmigration of population meaning there will be no growth in their housing markets.’

Higher rents and food prices boosted overall U.S. inflation in December, a sign that the Federal Reserve’s drive to slow inflation to its 2% target will likely remain a bumpy one.

What You Need To Know

- Higher rents and food prices boosted overall U.S. inflation in December, a sign that the Federal Reserve’s drive to slow inflation to its 2% target will likely remain a bumpy one

- Overall prices rose 0.3% from November and 3.4% from 12 months earlier

- Those gains exceeded the previous 0.1% monthly rise and the 3.1% annual inflation in November

- Excluding volatile food and energy costs, though, so-called core prices rose just 0.3% month over month, unchanged from November’s increase

Thursday’s report from the Labor Department showed that overall prices rose 0.3% from November and 3.4% from 12 months earlier. Those gains exceeded the previous 0.1% monthly rise and the 3.1% annual inflation in November.

Excluding volatile food and energy costs, though, so-called core prices rose just 0.3% month over month, unchanged from November’s increase. Core prices were up 3.9% from a year earlier, down a tick from November’s 4% year-over year gain. Economists pay particular attention to core prices because, by excluding costs that typically jump around from month to month, they are seen as a better guide to the likely path of inflation.

Overall inflation has cooled more or less steadily since hitting a four-decade high of 9.1% in mid-2022. Still, the persistence of still-elevated inflation helps explain why, despite steady economic growth, low unemployment and healthy hiring, polls show many Americans are dissatisfied with the economy — a likely key issue in the 2024 elections.

In a statement, President Joe Biden praised the positives from Thursday’s report while acknowledging that there is more work to be done when it comes to lowering consumer prices across the board.

“Today’s report shows that we ended 2023 with inflation down nearly two-thirds from its peak and core inflation at its lowest level since May 2021,” the president said. “We saw prices go down over the course of the year for goods and services that are important for American households like a gallon of gas, a gallon of milk, a dozen eggs, toys, appliances, car rentals, and airline fares.”

“Despite what many forecasters were predicting a year ago, inflation is down while growth and the job market have remained strong,” he hailed. “The economy has created more than 14 million jobs since I took office, and wealth, wages, and employment are higher now than under my predecessor.”

“But there is much more work to do to lower costs for American families and American workers,” Biden admitted. “That’s why I’m taking action to bring down the price of insulin, prescription drugs, and energy, eliminating hidden junk fees companies use to rip you off, and calling on large corporations to pass on savings to consumers as their costs moderate.”

The Federal Reserve, which began aggressively raising interest rates in March 2022 to try to slow the pace of price increases, wants to reduce year-over-year inflation to its 2% target level.

Overall, the progress against inflation has been significant. A year ago, the 12-month rise in the consumer price index was 6.5% — way down from a four-decade high of 9.1% in June 2022 but still painfully high. And wage gains have outpaced inflation in recent months, meaning that Americans’ average after-inflation take-home pay is up.

There are solid reasons for optimism that inflationary pressure will continue to recede in the coming months.

The Federal Reserve Bank of New York reported this week, for example, that consumers now expect inflation to come in at just 3% over the next year, the lowest one-year forecast since January 2021. That’s important because consumer expectations are themselves considered a telltale sign of future inflation: When Americans fear that prices will keep accelerating, they will typically rush to buy things sooner rather than later. That surge of spending tends to fuel more inflation.

But that nasty cycle does not appear to be happening.

And when Fed officials discussed the inflation outlook at their most recent meeting last month, they noted some hopeful signs: An end to the supply chain backlogs that had caused parts shortages and inflation pressures and a drop in rent costs, which is beginning to spread through the economy.

Many economists have suggested that slowing inflation from 9% to around 3% was easier to achieve than reaching the Fed’s 2% target could prove to be.

The December U.S. jobs report that was issued last week contained some cautionary news for the Fed: Average hourly wages rose 4.1% from a year earlier, up slightly from 4% in November. And 676,000 people left the workforce, reducing the proportion of adults who either have a job or are looking for one to 62.5%, the lowest level since February.

That is potentially concerning because when fewer people look for work, employers usually find it harder to fill jobs. As a result, they may feel compelled to sharply raise pay to attract job-seekers — and then pass on their higher labor costs to their customers through higher prices. That’s a cycle that can perpetuate inflation.