exclusive

The family of five relocated from Knoxville to New York three months ago — itself a move that’s typically made in reverse — settling into a four-bedroom Park Slope apartment.

OLGA GINZBURG FOR THE NEW YORK POST

In a pre-war Brooklyn building, Lisa Miller cheerfully opens the door in khakis and a white-laced top with socks on — no shoes from the outside allowed in, especially on the day of a torrential April downpour.

From the entry, Miller — a photographer and content creator — waves to her neighbor. She and her family already seemed acclimated to Park Slope and the people in it, despite the short time they’ve lived there.

The Millers have called a roughly 1,100-square-foot unit their home for just three months after giving up their spacious life in Knoxville, Tennessee. It’s a move not typically heard of, and particularly in the wake of 2020 uprooting the lives of many New Yorkers who headed in directions south seeking fewer restrictions, safety and cheaper prices. In 2024, the move in the opposite direction certainly goes to show that, for those seeking opportunities in a bustling atmosphere — such as this brood — New York’s still got it.

But despite the change in location, the family brought a sense of home and charm with them. Upon entering the four-bedroom, two-bathroom apartment, a whiff of a fresh ocean breeze scent fills the air — with Miller noting it’s one of Anthropologie’s popular Capri Blue candles.

Furniture and other items of decor are intricately placed throughout the railroad residence, as if this space has already been inhabited for years, not months.

“It’s my OCD,” Lisa told The Post of their new home already being perfectly furnished.

It’s a move that also shows will — an attribute that ties her family of five together.

During the pandemic and its aftermath, New York City witnessed a significant departure of residents. Between April 2020 and July 2022, the population of the Big Apple plummeted by nearly half a million individuals, constituting a 5.3% decline and erasing nearly three-quarters of the growth achieved in the preceding decade.

Factors attributed to the mass exodus the Concrete Jungle saw included high crime rates, affordability and space.

By contrast, the South grew during COVID, and accounted for a whopping 87% of the nation’s growth in 2023, though it holds just 39% of the population. Tennessee, North Carolina and Florida in particular have all received a number of new residents since the coronavirus years, and continue to do so.

Recent data also shows the family’s home of Knoxville, known as an up-and-coming city, is one of the fastest-growing mid-size cities in America.

More Americans are moving from large metropolitan areas to mid-size cities; Knoxville was among the top destinations, with 70% of moves inbound in 2023, according to a recent study released by Mayflower Transit.

And as opposed to Brooklyn, Knoxville offers the prime perk of space.

“In Knoxville, we had a full office, a studio, a dining room and an eat-in kitchen,” said Miller. “So by not having those things, that was probably a good 1,200 square feet there that we weren’t going to use anymore.”

Miller, along with her husband, Dusty, and their three children — 15-year-old daughter, London, and sons Cooper, 12, and Luke, 11 — signed the lease in November, though they didn’t actually move in until a month later.

The benefits of the move immediately became apparent.

“Our family has grown closer together since being here because we’re not going 100 different ways,” Miller said. “We’re all here together and there’s not as many people that we know here.”

Miller’s upbringing was somewhat different to the other kids she grew up up with, having moved from foster home to foster home.

“I grew up in a lot of really traumatic situations,” Miller said. “And so I always romanticized the city as this dream place. I was a creative as a kid. I drew, I sang, I didn’t start doing photography and decorating and stuff until I was older, but I’ve always been super creative and kind of saw New York as the stage for whatever that looks like for me . . . my whole life was like, ‘I’m going to live there.’”

Entering the cozy living room, neutral and color tones mix with an oversize couch to fit the whole family and a touch of vintage charm. Dusty, who works as a Department of Defense contractor, along with their daughter, London, join in on the conversation.

“I’m eating my way across the city and when we first moved here, adapting wasn’t as difficult as I thought it was going to be, because I told Lisa it was kind of like when I was in college,” Dusty said. “I lived in downtown Knoxville. You would park a car and leave it there for a month. You walk to class, you’d walk to get food . . . So when we first got here, I said, ‘It’s just like being in college all over again.’”

What initially motivated them to make this big move: London and her aspirations as a dancer.

“I love it here,” London said, adding that she took delight in dancing at Manhattan’s famed Alvin Ailey.

“We had never even talked about the possibility of moving here, until she spent last summer here, at the Joffrey Ballet,” Lisa Miller added. “She did summer intensive, and they offered her a permanent spot. The option was for her to come here on her own. We are very tight-knit family. That was not ever really an option.”

The move was also beneficial for Lisa and Dusty’s youngest son, who has autism.

“For a child like Luke, who is high-functioning on the autism spectrum, with some learning difficulties and social difficulties, we just could not find a fit for him in Knoxville,” Miller said. “The way people receive and accept him here is different than in Tennessee. We already feel like he is surrounded by support and people who see him as being different as something special and good.”

Despite each person admitting that leaving family and friends behind was the most difficult part of the transition, they have found New York to be its own support system in many other ways. What’s more, they can thrive in a beautifully decorated space.

For her part, Miller adds that her inspiration of creating the interior was to do the opposite of what was trendy.

“Years ago, I did home decor influencing on Instagram,” she said. “And, embarrassingly, it was like the farmhouse era. Everything was so trendy and so when we kind of started over, I was like, ‘I don’t want to follow a trend. I really want to just put things on the wall that are purposeful and meaningful.’”

One wall in her living room is adorned with vintage frames of black and white photography, and the images are pictures of her family she took herself. The wall also included a map of Knoxville, paying homage to the only other place they’ve all really ever known.

Each bedroom is decked with its own flare and style. Luke’s room displays his favorite collectible trinkets. Cooper opted for a basketball hoop as the centerpiece. London’s room has bohemian energy, with blue and green tones.

Still, there are some quotidian nuisances. The family sees grocery shopping in the Concrete Jungle taking some time to get used to. Unlike in Knoxville, they cannot just load up a shopping cart full of groceries into the trunk of their car.

There is also using the subway as their main mode of transportation, instead of the convenient car, and having to find more affordable options for meals.

Meanwhile, they are no longer homeowners. Instead of a reasonable mortgage, they are now spending more than $5,000 per month on rent.

“I think the trade off for what we were looking for, which were creative opportunities, was knowing that we wouldn’t be owning a home,” Miller said. “That’s not going to make sense to everyone. And that’s fine, because the beauty of life is that we all get to do what we want.”

And so, a fresh start for 2024 is already off to a roaring start.

“We have been in Tennessee for almost 40 years. My whole life. So it’s been neat to kind of go and experience, you know, the exact opposite,” Dusty added.

Load more…

{{/isDisplay}}{{#isAniviewVideo}}

{{/isAniviewVideo}}{{#isSRVideo}}

{{/isSRVideo}}

A DISABLED man was instructed to immediately leave his home after it was sold from under him, allegedly without warning.

Archie Robinson from Memphis, Tennessee is one of numerous homeowners whose homes were sold by Shelby County at auction during the pandemic.

The County foreclosed the properties because the owners were behind on tax bills.

“Some young lady served me some papers stating that someone had bought the home, and why was I here? And who was I?” the 54-year-old told WMC-TV in 2022.

“I was like – I’ve been here basically all my life.”

Robinson inherited his childhood home when his mother, who was behind on her property taxes, died.

However, the property was then sold in a tax sale in February 2021 by the Shelby County Trustee’s Office.

This action is taken so the money owed to the county, in this case, $5,000, can be paid back from the sale.

Robinson was sick and bedridden in 2021 when he received an eviction notice telling him to vacate the property “immediately” and claims he had no idea his home had been sold.

“I asked, ‘How could you sell my property without me knowing?'” Robinson said.

“He said ‘Well, we sent out notices,’ “I said, ‘Well, I haven’t received any notices.'”

Under state laws, homeowners whose properties are set to undergo tax sales must be notified.

Shelby County uses certified mail which must be signed by the homeowner or another authorized individual to prove receipt of the notice.

However, during the pandemic, the U.S. Postal Service allowed carriers to sign the notices instead of the homeowners with the words “COVID” or “C-19.”

Shelby County Trustee Regina Morrison Newman told the news outlet that Robinson signed three certified mail notices, though he denies this.

However, she did not dispute the fact that thousands of homeowners may not have been correctly informed of a tax sale.

“Our return receipts for 30,000 pieces of certified mail came back marked COVID, so we could not prove to the courts that anybody received that mail or that due process was provided,” Newman told the County Commission in October 2020.

Despite this, the Trustee’s Office auctioned off nearly 1,700 homes between August 2020 and February 2021.

During this period there was a ban on federal eviction and mortgage foreclosure.

According to the analysis done by the University of Memphis Institute for Public Service Reporting in a joint investigation with WMC-TV, the majority of these properties were empty but over 400 seemed to be occupied at the time.

When faced with eviction, owners are either forced to move somewhere else quickly or cough up the money to repurchase their homes.

How can your home be sold without your consent?

Your home can be sold from under you for various reasons – here are three key things to look out for:

Tax Sale

- A Tax sale is the sale of property by a governmental entity to recover unpaid taxes by the owner who has reached a certain point of delinquency in their owed payments.

- Before a tax sale takes place, there is a right-of-redemption period where the owner can pay off their debt and reclaim their home.

- Each state has different laws surrounding tax sales but in most areas, the basic requirement is that adequate notice is given to the owner to pay the outstanding money, and any sale must be open to the public.

Foreclosure

- Foreclosures can take place when lenders take control of a property after borrowers have failed to make their repayments.

- Borrowers will receive a Notice of Default, triggering the foreclosure process.

- Homeowners in HOA communities can also see their homes foreclosed by their HOA for falling behind on fees.

- This means that even if you keep up with mortgage repayments, you could still lose your home if your HOA has a lien on your property.

- When such a foreclosure takes place, the sale price only needs to be enough to cover the HOA debt meaning that properties can be sold for much less than they are worth.

Property Fraud

- Criminals can sell or mortgage homes by pretending to be the owner by using a fake or stolen ID.

- Typical targets for property fraud include absent owners like landlords, owners who live abroad, and sole owners of unmortgaged homes.

- The U.S. Sun previously reported on a man whose vacation home worth $300,000 was sold by criminals for just $9,000 – they even had the deed to the property.

Newman defended the actions of the Trustee’s Office by arguing to the news outlet that the addresses of the homes set for tax sale were published in the Memphis Daily News.

It is a state requirement to put the addresses in a newspaper that is in general circulation as well as putting them on the Public Notice Tennessee website.

However, the news outlet was told by several homeowners, including Robinson, that they had never heard of or seen the Memphis Daily News.

A former attorney from Newman’s office spoke to the news outlet about the issue.

Jack Turner explained that homeowners can come forward to claim that they did not receive proper notice of the sale of their homes.

“Somebody may challenge a tax sale after the fact and say they were never given notice and the courts will have to decide whether the notice was sufficient or not,” said Turner.

“If that happens, they’re still going to have back taxes due, but it might set aside a tax sale.”

Turner added that before he left his position at Newman’s office, it was still receiving certified mail that was signed by postal workers, not homeowners, while tax sales continued to go through.

“I can just tell you my experience being there: the goal is to get taxes paid so county services can be provided,” Turner said.

Robinson was forced to borrow money to redeem his property and keep his childhood home.

“I guess I’m one of the fortunate ones if you’d like to look at it like that,” he said.

However, due to this drastic action, he is now behind on his property taxes once again.

Taking legal action to claim that he did not receive proper notice of the tax sale would take even more money from his dwindling funds.

“I can’t imagine not having any place to live or having to depend on someone else for my wellbeing, especially after working so hard and now being disabled,” he said.

The U.S. Sun has contacted the Shelby County Trustee Office for comment.

Knoxville, Tennessee, March 07, 2024 (GLOBE NEWSWIRE) — Sell My House Fast, a home-buying company specializing in providing fast and efficient solutions for individuals who need to sell their homes promptly, is excited to announce the launch of its customer-centric solution that helps homeowners sell their property in the greater Knoxville, Tennessee, area.

The simple and effective customer-centric solution by Sell My House Fast LLC is to offer homeowners the option to sell their property for cash, no matter the state or situation of the home. With the company emphasizing its team’s commitment to clarity, dependability, and fairness, this unique approach allows fewer complications and expenses for individuals searching for a swift and lucrative way to sell their homes.

“Are you looking to sell your home quickly and hassle-free for all cash? You’ve come to the right place because we buy houses for cash,” said a spokesperson for Sell My House Fast LLC. “Above all, at Sell My House Fast, we specialize in providing fast and efficient solutions for homeowners who need to sell their properties promptly. Whether you’re facing foreclosure, relocating, going through a divorce, or simply want to move on from your property, we’re here to help.”

Empowering homeowners with an easy selling approach, Sell My House Fast differentiates itself by removing the common obstacles faced when selling a property, such as the need for significant repairs, prolonged wait times, and the unpredictability of the real estate market. The home buying company enables sellers to transition from their properties promptly, presenting fair cash offers without the requirement for any remodeling or fixes. This method not only saves time but also lessens the financial strain on homeowners, presenting an appealing option for many.

With the understanding that every homeowner’s situation is distinct, Sell My House Fast tailors its services to meet the individual needs of its clients. Whether it’s facing foreclosure, handling a challenging inheritance, moving for work, or simply wishing to sell quickly for cash without making repairs, Sell My House Fast solves these problems. Their motto, “We buy houses in any condition,” highlights their dedication to providing flexible options that cater to the varied needs of homeowners in Knoxville.

What truly distinguishes Sell My House Fast in Knoxville’s from other Real Estate Investors in the scene is the company’s efficiency in closing deals and its firm commitment to integrity and transparency. Customer reviews often praise the home buying expert’s professionalism, equitable dealings, and smooth process of transactions. This reputation for excellence reflects the company’s dedication to simplifying the selling experience for homeowners.

Beyond purchasing properties, Sell My House Fast shows a deep commitment to the Knoxville community. By offering a dependable route for homeowners to sell quickly, the reliable property company contributes to the local real estate market’s vitality and growth. Every time Sell My House Fast buys an investment property, approximately 40+ jobs are created while providing an updated house for a family. This dedication goes further into revitalizing neighborhoods and building community spirit by investing in properties that require care, thus benefiting the broader community.

For homeowners in Knoxville looking to sell their houses quickly, efficiently, and without the typical hassles of the real estate market, Sell My House Fast provides an unmatched service. The company’s slogan, “We Buy Houses,” signifies an easy process for a home owner, establishing Sell My House Fast LLC as a leader in the home buying industry. Continuing to offer expert services in the Knoxville area, the home buying company guarantees a further commitment to excellence, integrity, and the welfare of the communities it serves.

More Information

For more details about Sell My House Fast LLC, please visit https://sellmyhousefastknoxvilletn.com/ or freely contact them at the address and phone number provided.

CONTACT: Sell My House Fast LLC 201 N Weisgarber Rd Knoxville Tennessee 37919 United States 865-234-9585 https://sellmyhousefastknoxvilletn.com/

America’s real estate market is steeped in uncertainty as soaring mortgage rates effectively freeze buyer activity.

It has left many questioning: is property still a good investment?

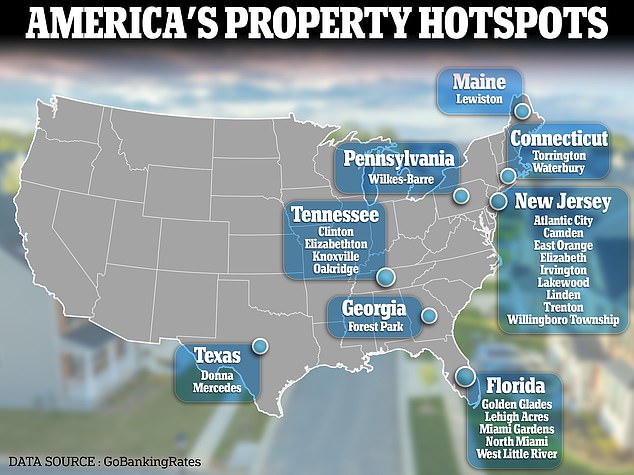

But a new study by GoBankingRates claims to shed light on the areas that are most likely to help owners get the best returns.

Researchers analyzed the average house price – as recorded by Zillow – in major US metros as of January 2024 and established where prices have risen quickest in the past five years.

Their findings show that Atlantic City, New Jersey, is the best place to gain value on a property. The average home in the area costs $218,761, having shot up 102 percent in price since 2019 and 16 percent in the last year alone.

A new study by GoBankingRates claims to shed light on the areas that are most likely to help owners get the best returns

It was followed by Waterbury, Connecticut, where the typical home costs $249,073, up 15 percent from last year and 100 percent from five years ago.

The top five was rounded out by Lewiston, Maine, Mercedes, Texas, and Torrington, Connecticut.

By comparison, the national average home value in the US in January 2024 was $343,951, up 50 percent from 2019 and 3 percent from last year.

New Jersey was the state to appear most prominently on the list, with nine of the 25 places ranked located in the Garden state.

It was followed by Florida and Tennessee which had four cities each on the list.

Notably no cities in New York or California made the top 25. The rankings were compiled by combining the percentage changes in each city in one year and in the last five years.

The findings come after a separate report by property portal Redfin found the US housing market had gained $2 trillion in value over the last year.

Redfin’s analysis of more than 90 million homes across the country found the total value of residential real estate had increased 5.3 percent to $47.5 trillion in December.

However, experts have repeatedly sounded the alarm over a real estate ‘correction’ which will see house values fall somewhat after ballooning during the pandemic.

Former Oppenheimer analyst Meredith Whitney – who has been dubbed the ‘Oracle of Wall Street’ after predicting the 2008 financial crash – told DailyMail.com that house prices would start to fall as Baby Boomers begin downsizing.

She said: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’, said house prices in some states will fall this year

Mortgage rates are hovering close to 7 percent – almost double where they were two years ago

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

The average rate on a 30-year fixed-rate home loan is now 6.94 percent, according to Government-backed lender Freddie Mac. It is almost double what they were two years ago.

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Data from Redfin shows that the typical US homeowner now spends twice as long in their properties as they did in 2005.

Today an owner can expect to spend 11.9 years in the same property, compared to 6.5 years two decades ago.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

| City | Average house price | % change in 1 year | % change in 5 years |

|---|---|---|---|

| Atlantic City, New Jersey | $218,761 | 16% | 102% |

| Waterbury, Connecticut | $249,073 | 15% | 100% |

| Lewiston, Maine | $274,687 | 14% | 91% |

| Mercedes, Texas | $123,572 | 13% | 92% |

| Torrington, Connecticut | $255,834 | 14% | 81% |

| Irvington, New Jersey | $359,441 | 10% | 101% |

| Elizabeth, New Jersey | $498,548 | 15% | 75% |

| Knoxville, Tennessee | $341,351 | 12% | 88% |

| Camden, New Jersey | $115,800 | 12% | 85% |

| Trenton, New Jersey | $307,421 | 12% | 84% |

| Oakridge, Tennessee | $285,447 | 11% | 92% |

| East Orange, New Jersey | $425,011 | 11% | 90% |

| Golden Glades, Florida | $490,839 | 11% | 86% |

| Willingboro Township, New Jersey | $303,989 | 10% | 92% |

| West Little River, Florida | $401,228 | 12% | 84% |

| Lakewood, New Jersey | $402,932 | 13% | 75% |

| Donna, Texas | $131,471 | 11% | 84% |

| Wilkes-Barre, Pennsylvania | $137,986 | 10% | 87% |

| Forest Park, Georgia | $177,414 | 5% | 114% |

| Clinton, Tennessee | $287,509 | 11% | 82% |

| Miami Gardens, Florida | $449,676 | 11% | 81% |

| North Miami, Florida | $473,109 | 10% | 84% |

| Linden, New Jersey | $497,627 | 13% | 71% |

| Lehigh Acres, Florida | $312,991 | 9% | 90% |

| Elizabethton, Tennessee | $203,565 | 12% | 74% |

The US housing market gained a huge $2 trillion over the last year, amid a historic shortage of homes for sale.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023, up from $474,740 a year earlier.

According to Redfin analysis of more than 90 million homes across the country, the total value of US residential real estate increased 5.3 percent from a year earlier to $47.5 trillion in December.

While soaring mortgage rates mean housing demand is sluggish, home values continue to rise, pricing many Americans out of the market.

In the last two years, the housing market has gained $5.6 trillion, Redfin found.

However a disparity remains across the US. While affordable East Coast and Midwest metros saw the biggest rise in home values in the last year, so-called pandemic ‘boomtowns’ have seen the largest decline.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023. The biggest rises were on the east coast of America

Scroll down for the full list of metros with the biggest price rises.

According to Redfin, there are three major reasons why home values are continuing to rise.

Many homeowners are locked into ultra-low mortgage rates from previous years, meaning they are hesitant to put their houses on the market.

With supply tighter than demand, buyers are competing for a limited pool of homes. That is propping up values for both properties that are already for sale, and those that could hit the market in the future.

The total value of US homes was nearing a trough at the end of 2022, which is part of the reason year-over-year growth at the end of 2023 was so large, it added.

It is typical for home values to cool in the winter, but they experienced an abnormally large slowdown in 2022 as the shock of surging mortgage rates sent a freeze through the housing market.

While America grapples with a housing shortage, it is also continuing to build homes, which contributed to the gain in total home values last year, Redfin said.

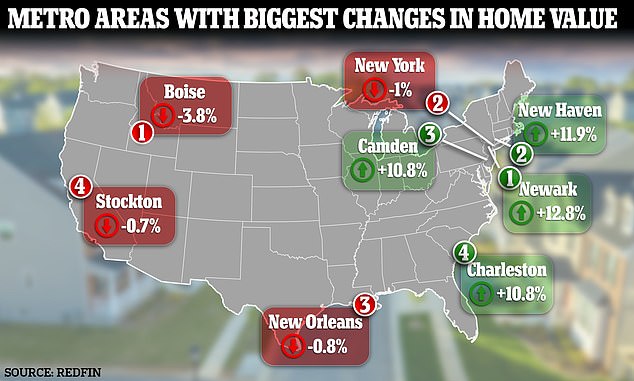

Home values in Newark, New Jersey, saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion.

Next come two other East Coast metros, New Haven, Connecticut, and Camden, New Jersey. Homes in New Haven gained 11.9 percent in value to $86.5 billion, while properties in Camden went up by 10.8 percent to $153 billion.

Home values in Newark, New Jersey , saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion

Fixed 30-year mortgage rates are now hovering around 6.9 percent, according to Government-backed lender Freddie Mac

Charleston, South Carolina, ranked fourth – with values increasing by 10.8 percent to $188.5 billion.

Next are three Midwestern metros, Elgin, Illinois, Grand Rapids, Michigan and Milwaukee, Wisconsin.

Places like Newark and Camden are likely seeing home values jump in part because they are attracting demand from people who are priced out of New York and can now work remotely, Redfin said.

Midwestern metros like Milwaukee and Grand Rapids are experiencing home value gains for a similar reason.

They are affordable, and when mortgage rates and home prices are elevated, demand for affordable homes goes up.

‘America’s homeowners are sitting pretty. They’re holding a massive amount of housing wealth, despite lackluster demand from buyers, because home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao.

‘Prospective buyers aren’t as lucky. The combination of elevated mortgage rates, high home prices and a limited pool of homes for sale means homeownership is about as unaffordable as ever.’

But not every homeowner has seen their property increase in value.

‘Home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao

Four metros saw declines in overall home value, according to Redfin.

Pandemic ‘boomtown’ Boise, in Idaho, saw prices decline 3.8 percent to a total of $123.9 billion and New York saw prices fall 1 percent to $2.4 trillion.

New Orleans prices went down 0.8 percent to $124 billion and homes in Stockton, California, lost 0.7 percent in value – falling to a total of $109.2 billion in value.

The metros with the smallest increases were Philadelphia, at 0.3 percent, Honolulu, at 0.8 percent, Austin, Texas, at 1 percent, Denver at 1.3 percent and Riverside, California at 1.6 percent.

Most of these metros have something in common, said Redfin, which is that they have become unaffordable for many homebuyers. This means that there is a cap on demand, so home values no longer have much, if any, room to rise.

New York, Honolulu, Riverside and Denver all have median home sale prices of at least $550,000 – well above the national median.

And in Boise and Austin, which also have median sale prices above the national level, many people are priced out because an influx of out-of-towners caused home values to skyrocket during the pandemic.

But some experts predict that there will be a shift in the housing market in some parts of the US in 2024, driven by a surge in Baby Boomers downsizing into smaller properties.

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’ after she correctly predicted the 2008 financial crash, said house prices in some states will fall this year.

So-called pandemic ‘boomtown’ Boise, Idaho, saw prices decline 3.8 percent to a total of $123.9 billion in December 2023 – the most of any metro

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’, said house prices in some states will fall this year

This, in turn, will free up inventory and bring costs down for first-time buyers.

Whitney said homes in New York, New Jersey and Ohio will see a fall in prices. By comparison, homes in Texas, Tennessee and Utah will remain strong, she said.

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

Tennessee’s luxury real estate market is a testament to the state’s rich history, vibrant culture, and stunning natural beauty. From the rolling hills of Nashville to the charming elegance of Memphis and the picturesque landscapes of Chattanooga, Tennessee offers an array of high-end properties that embody the essence of Southern luxury living.

In this Redfin article, we’ll unveil 5 of the most expensive homes for sale by Redfin, offering a glimpse into the epitome of luxury living in the Volunteer State.

1. All-brick luxury on a serene cul-de-sac

5217 Apple Mill Ct, Brentwood, TN 37027

Listed by Mike Estes

Priced at $2,149,000

Luxury awaits in this meticulously maintained all-brick home on a quiet cul-de-sac. Enjoy beautiful hardwood floors, a chef’s kitchen with quartz counters, and a recently renovated primary suite with a custom closet and spa-like bath. The spacious back patio offers privacy in your fenced yard. This home blends convenience with elegance.

2. Luxury living in the Hunt Club

100 Walting St, Gallatin, TN 37066

Listed by Hope Geyer

Priced at $969,900

This 4 bed, 3.5 bath home on a premium corner lot boasts an open floor plan, engineered hardwoods, and custom millwork. The great room with gas fireplace connects to a chef’s kitchen with granite countertops and a walk-in pantry. The main floor includes an owner’s suite, ensuite, formal dining, and utility room. Upstairs, find two bonus rooms, two bedrooms, and ample storage. Relax on the covered patio, enjoy the oversized 3-car garage, and explore nearby walking trails.

3. The tranquility of country living

4416 Gosey Hill Rd, Franklin, TN 37064

Listed by Mike Estes

Priced at $1,150,000

Exquisite 120-year-old farmhouse, set on 5.8 serene acres, fully renovated for modern living. Open concept with beautiful hardwood floors, quartz countertops, and stainless steel appliances in the kitchen. Vaulted ceilings, original exposed beams in the Great Room, and abundant windows create a bright, welcoming atmosphere. Enjoy the natural beauty of your private sanctuary with a creek, pastures, and wooded trails. Perfect for horses and ATV enthusiasts.

4. Three-bedroom gem near McFee Park

12618 Brass Lantern Ln, Knoxville, TN 37934

Listed by Gina McMullen

Priced at $919,900

Exceptional three-bedroom, three-bath home with a bonus room in Farragut, near McFee Park. Former “Model” home with premium features, upgraded amenities, and meticulous design. Hardwood flooring on the first floor, primary bedroom on the main level with spa-like bath and walk-in closet. Serene privacy with wooded backyard. Gourmet kitchen with 42-inch cabinets, stainless steel appliances, gas cooktop, large island, granite countertops, and stylish backsplash. Cozy gas fireplace in the great room with built-in shelving and a 12-foot coffered ceiling. Bonus room with its own bathroom for versatile use. Enjoy outdoor living on the screened porch. Ideal north-south exposure for balanced natural light.

5. Exceptional lakefront home

5601 Brights Pike, Russellville, TN 37860

Listed by Gina McMullen

Priced at $1,295,000

Exceptional custom-built Cape Cod style lakefront home on 23 acres with a year-round lake view and over 350 feet of shoreline, just minutes from Morristown. This 4-bedroom, 3-bath home boasts solid Mahogany and leaded glass French doors that open into a spacious living room with views of your private oasis.

Top-notch fixtures include 3/4” Brazilian cherry wood floors. The kitchen features solid cherry cabinets, granite countertops, stainless steel appliances, an induction cooktop, wine cooler, pot filler, dual KitchenAid steam ovens, and a Bosch built-in espresso machine. The primary bedroom offers a luxurious en-suite marble bathroom with heated floors, a spa tub, walk-in shower, rain shower, and dual vanities.

Thinking about buying or selling a luxury home in Tennessee?

Whether you’re in the market for an upscale property in the Volunteer State, exploring the highlighted listings mentioned earlier, or contemplating the sale of your high-end residence, a Redfin Premier agent is ready to guide you through the entire process. Armed with extensive real estate knowledge and a profound understanding of the local market, your Premier agent serves as your indispensable partner in securing the best deal as a buyer or maximizing your profit as a seller of luxury real estate in Tennessee.

Americans are staying in their homes before selling up for twice as long as they did in 2005 – and baby boomers are to blame.

The typical homeowner spends 11.5 years in their house today, up from 6.5 years two decades ago, according to a new report by Redfin.

Researchers said the trend is being driven by older homeowners who are not ‘financially incentivized’ to move. A lack of homes on the market pushes up prices.

It comes after former Oppenheimer analyst Meredith Whitney told DailyMail.com that the house prices will finally start to decline as more seniors start downsizing – thereby freeing up homes.

According to Redfin’s analysis of US Census Bureau data, homeowner tenure peaked at 13.4 years in 2020.

The typical homeowner spends 11.5 years in their house today, up from 6.5 years two decades ago, according to a new report by Redfin

It comes after former Oppenheimer analyst Meredith Whitney, pictured, told DailyMail.com that the house prices will finally start to decline as more seniors start downsizing – thereby freeing up homes

The analysis also found that millennials were more likely to stay in their homes for shorter periods, in part because they change jobs more frequently than older generations.

Two in five baby boomers – those born between 1946 and 1964 – have lived in their home for 20 or more years.

By comparison, less than 7 percent of millennials – born between 1981 and 1996 – have lived in their home for ten years or longer.

The report notes: ‘Most – 54 percent – of baby boomers who own homes own them free and clear with no outstanding mortgage.

‘For that group, the median monthly cost of owning a home – which includes insurance and property taxes among other things – is just over $600.

‘Nearly all boomers who do have a mortgage have a much lower rate than they would if they sold and bought a new home with today’s 7 percent-ish rates.’

But researchers noted that older homeowners ‘hanging onto their homes’ is ‘an obstacle for young first-time buyers trying to break into the market.’

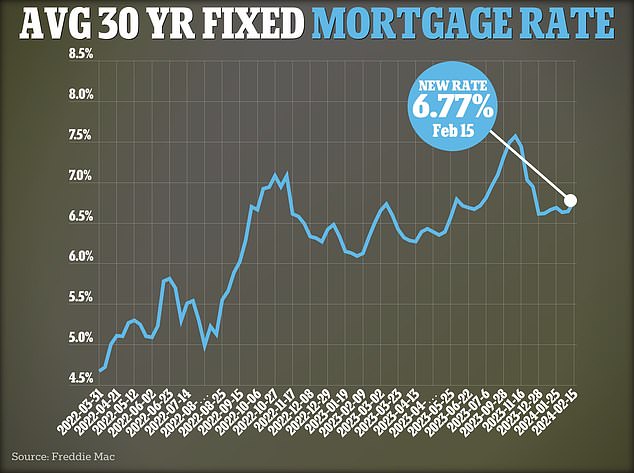

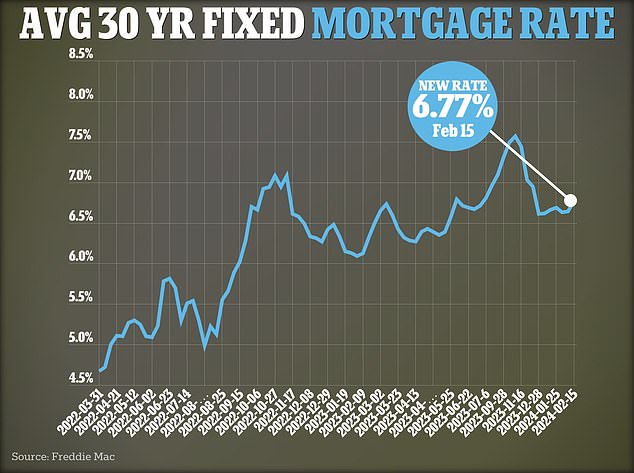

The average rate on a 30-year fixed home loan reached 6.77 percent, up from 6.64 percent last week, according to figures from Government-backed lender Freddie Mac

The findings echo comments made by Whitney, an analyst who was dubbed the ‘Oracle of Wall Street’ after she accurately predicted the 2008 financial crisis.

Her research shows that around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

However she claims a significant upheaval is in-store as more of these older owners start to sell up – freeing inventory and bringing prices down.

Whitney told DailyMail.com: ‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

During the pandemic the median US house price ballooned from $303,465 in March 2020 to $402,045 by December 2023, Redfin figures show.

Many families were embroiled in a so-called ‘race for space’ as they looked for bigger homes and gardens to spend lockdown. A widespread shift to working-from-home also unchained workers from their city center properties.

But house prices have remained elevated ever since – despite mortgage rates soaring in response to the Federal Reserve‘s funds rate reaching a 22-year high.

The average rate on a 30-year mortgage is currently hovering at 6.77 – around double what they were two years ago, figures from Government-backed lender Freddie Mac show.

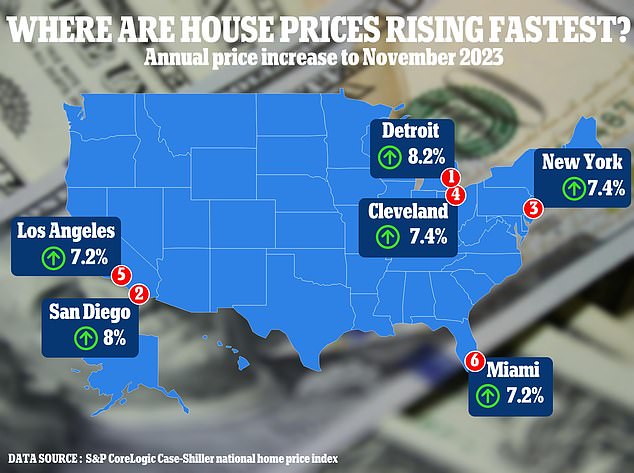

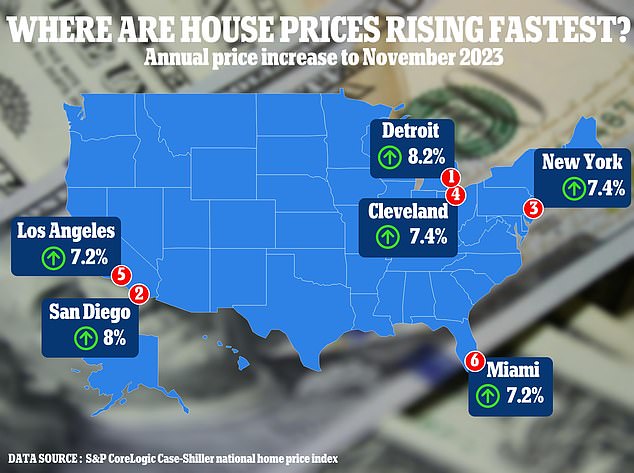

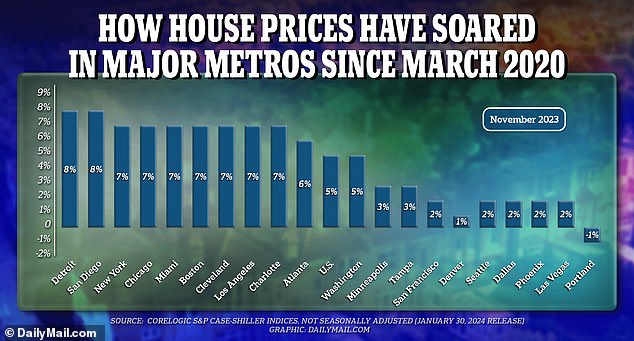

In the year to November 2023, property prices in Detroit increased 8.2 percent, according to latest data from the leading measure of US house prices

A recent report by CoreLogic shows how property prices have shot up in certain US metros

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

She notes that in the last decade homeowners have built up $21 trillion in equity in their homes – so any price falls is unlikely to seriously harm them.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

- Meredith Whitney accurately predicted the 2008 financial crisis

- Now she claims US housing market is in the midst of a major shift

- It marks a reversal of the pandemic-inspired housing boom

America’s real estate landscape is in the midst of a major upheaval that will make homes more affordable to first-time buyers, claims a former Oppenheimer analyst.

Meredith Whitney earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis.

Now she claims house prices are on the brink of decline after the pandemic inspired a real estate boom that saw the average property shoot up over $100,000 in value in less than four years.

However, she said the trend will be geo-specific with the likes of New York, New Jersey and Ohio worst-affected. By comparison, homes in Texas, Tennessee and Utah are among the states set to remain strong.

The shift will be driven by a surge in Baby Boomers downsizing into smaller properties – freeing up inventory and bringing costs down for first-time buyers, Whitney said.

Meredith Whitney, pictured, earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis

In the year to November 2023, property prices in Detroit increased 8.2 percent, according to latest data from the leading measure of US house prices

A recent report by CoreLogic shows how property prices have shot up in certain US metros

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

During the pandemic the median US house price ballooned from $303,465 in March 2020 to $402,045 by December 2023, Redfin figures show.

Many families were embroiled in a so-called ‘race for space’ as they looked for bigger homes and gardens to spend lockdown. A widespread shift to working-from-home also unchained workers from their city center properties.

But house prices have remained elevated ever since – despite mortgage rates soaring in response to the Federal Reserve’s funds rate reaching a 22-year high.

The average rate on a 30-year mortgage is currently hovering at 6.77 – around double what they were two years ago, figures from Government-backed lender Freddie Mac show.

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Whitney told DailyMail.com: ‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later’

The average rate on a 30-year fixed home loan reached 6.77 percent, up from 6.64 percent last week, according to figures from Government-backed lender Freddie Mac

Data from Redfin shows that the typical US homeowner now spends twice as long in their properties as they did in 2005.

Today an owner can expect to spend 11.9 years in the same property, compared to 6.5 years two decades ago.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

She notes that in the last decade homeowners have built up $21 trillion in equity in their homes – so any price falls is unlikely to seriously harm them.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

‘But New York, New Jersey, Ohio and Illinois will see an outmigration of population meaning there will be no growth in their housing markets.’