White House press secretary Karine Jean-Pierre‘s comment about gas prices currently remaining well below their 2022 peak has sparked backlash among conservatives on social media and other users complaining that fuel is still “way overpriced.”

During a press briefing on Monday, Jean-Pierre responded to a question by a reporter asking about the increase of gas prices across the country over the last month and what the Biden administration was going to do about it.

Read more: Best Credit Cards to Save on Gas

“I don’t have any new actions to read out,” Jean-Pierre said. “I would say that gas prices remain well below their peak back in 2022, I think that’s important. The average gas price right now is cheaper than this time last year, and that’s because of what this president has been doing over the last three years.”

FREDERIC J. BROWN/AFP via Getty Images

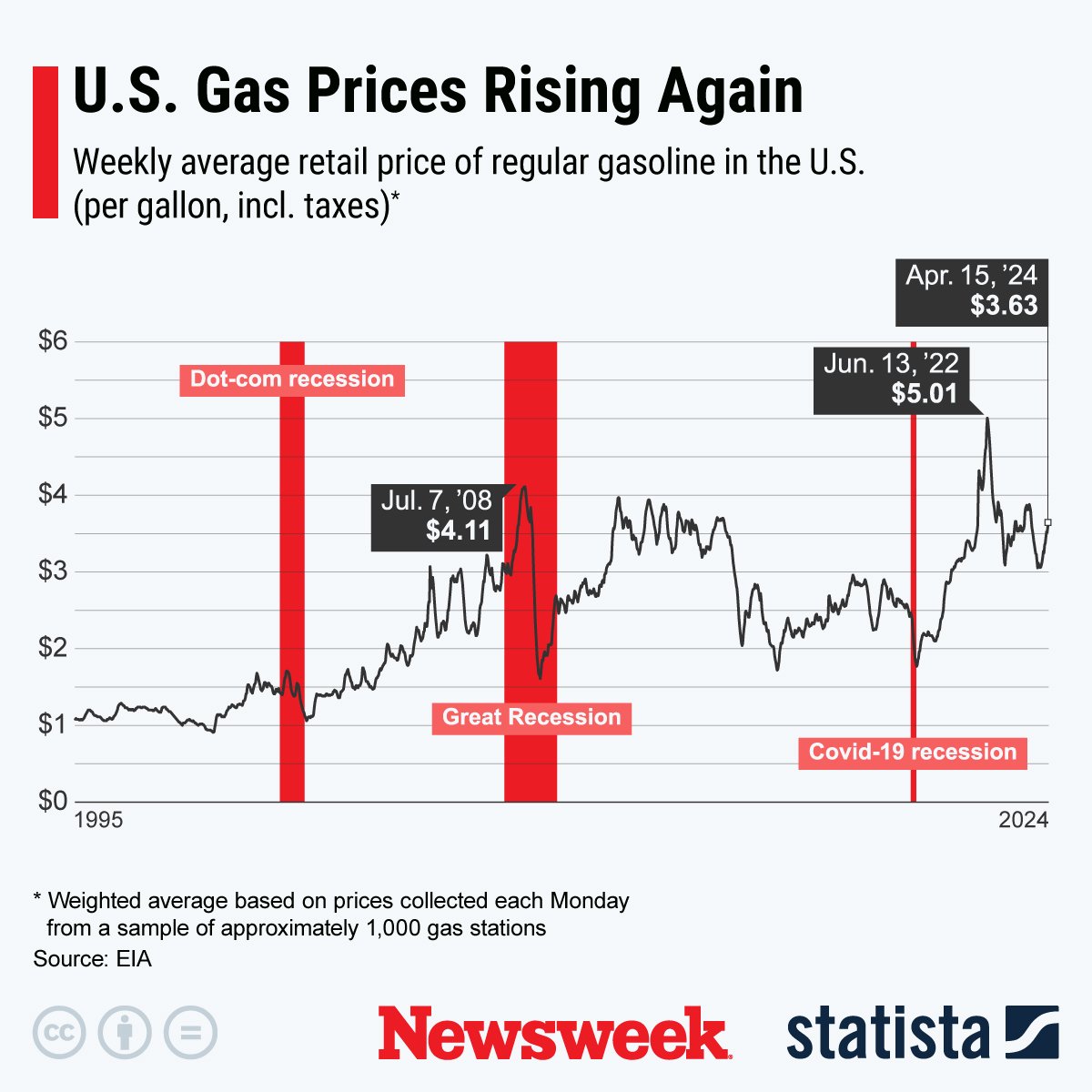

As of Tuesday, the national average price for gas was $3.644 per gallon, according to the American Automobile Association (AAA), up from $3.634 the day before and $3.608 a week before. A month ago, on March 16, the national average gas price was $3.455 per gallon. Compared to a year ago, gas prices are slightly lower: on April 16, 2023, the national average was $3.669 per gallon.

The Republican National Committee shared a clip of the press briefing on X, formerly known as Twitter, writing that “gas prices are up almost 52 percent since Biden took office.”

Another social media user on the platform wrote: “Used to be 2 bucks. Now it’s over 3 bucks. The fact that it’s not 4 bucks anymore doesn’t change the fact it’s still high.” Another wrote that gas prices were “still way overpriced.”

A user who described herself as an “old-school conservative” wrote: “Karine Jean-Pierre praises the current gas prices, even after being told they’ve gone up 20¢/gallon in just the past month. Are you impressed by gas prices under Biden?”

When Biden took office in January 2021, gas prices were an average of $2.4 per gallon across the country, according to the U.S. Energy Information Administration (EIA). By December of the same year, they had risen to over $3 per gallon, and in June 2022, they reached a peak of $5.06 per gallon due to the hardships caused in part by the Russian invasion of Ukraine.

Statista

This chart, provided by Statista, shows the weekly average retail price of regular gasoline in the U.S. (per gallon, including taxes).

Gas prices, whose vertiginous climb contributed to the rise of inflation between 2022 and 2023, have recently been climbing across the country, raising concerns that they will discourage the Federal Reserve from cutting interest rates. According to Charlie Bilello, chief market strategist at Creative Planning, gas prices have jumped by 17 percent so far this year, nearing their highest level since October 2023.

But while the rise in gas prices is bad news for U.S. drivers, their growth is not totally unexpected. It’s common for the cost of gas to increase as the weather gets warmer and people are eager to get on the road, between March and April, and peak at the beginning of summer in June.

Patrick De Haan, head of petroleum analysis at GasBuddy, wrote on X that the rise in gas prices “was completely expected and where we are today is not a surprise at all.” In its outlook for 2024, GasBuddy predicted that the highest prices this year will be reached at the peak of the summer driving season in May, with the national average potentially rising as high as $3.89 per gallon.

Newsweek contacted De Haan for comment by email on Tuesday morning.

“The record gasoline average of $5.04/gal in June 2022 will not be repeated this year, with few caveats,” De Haan said.

Uncommon Knowledge

Newsweek is committed to challenging conventional wisdom and finding connections in the search for common ground.

Newsweek is committed to challenging conventional wisdom and finding connections in the search for common ground.

Would you be willing to save a few hundred dollars on a car purchase if the seller seemed squirrely and didn’t have the title to the car?

Unfortunately, you will be on the hook for Joe Biden’s latest vote buying scheme to subsidize mortgages for houses with shaky titles.

In his State of the Union address, Biden proclaimed, “My administration is also eliminating title insurance on federally backed mortgages.” What could possibly go wrong?

Title insurance protects homeowners against financial loss if there is a defect in the title to their property.

“Wrecking ball benevolence” — my phrase in a 2004 Barron’s article that was quoted in a 2017 federal appeals court decision — leveled the housing sector.

As Rep. Patrick McHenry (R-NC), chairman of the House Financial Services Committee, declared in 2013, “Rank cronyism, Enron-style accounting and outright financial fraud made [Fannie and Freddie] so powerful and unaccountable that they were able to wreck our economy.”

Despite the debacles earlier in this century, Team Biden is championing “no clean title, no problem” mortgage loans.

Biden policymakers believe they are so smart that they can turbo-charge housing demand while removing the guardrails — and nothing bad will happen (except Biden’s reelection).

In lieu of title insurance, the Biden administration will approve granting subsidized mortgages based on “attorney opinion letters” that assert a lawyer believes someone owns a house.

Such form letters can now be purchased for $199 in some locales. This sounds on par with the $99 online deals selling “emotional support animal letters” people exploit to “prove” they need their dog, cat, kangaroo or squirrel with them at all times.

Having a page of pablum on fancy law-firm letterhead will be no competition for a clean deed — or a tangled land dispute that could go back generations.

A recent report by FundingShield found that home title fraud risk “reached an all-time high” late last year.

The title insurance waiver is part of a blizzard of housing interventions to portray Biden as a savior.

But foolish federal policies have made homes less affordable than ever before.

Subsidized mortgages helped send home prices skyrocketing in recent years, along with the Federal Reserve artificially suppressing interest rates.

Since Biden took office, the average monthly mortgage payment for new home has almost doubled, reaching $3,322 per month.

Not to worry: Uncle Joe is on the case! The White House announced on March 7 that “President Biden believes housing costs are too high.”

Biden is also pushing Congress to approve a $10,000 tax credit for middle-class, first-time homebuyers, a $25,000 handout for down payments for first-generation home buyers and a $10,000 tax credit to “middle-class families who sell their starter home, defined as homes below the area median home price in the county, to another owner-occupant.”

Why not also provide a $5,000 grant for homes with lawn signs for Democratic candidates?

Who entitled the Biden White House to pick winners and losers in the housing market?

Almost all of Biden’s housing “reforms” are in the direction of greater recklessness.

There was a brief uproar last year when Team Biden announced that home buyers with good credit scores will be forced to subsidize buyers with bad credit.

But that was only the tip of the iceberg. Author and appraiser Jeremy Bagott warns that thanks to Biden policies, Fannie and Freddie “have been pushing to eliminate critical checks and balances in a radical experiment with US taxpayers’ money and the US economy . . . scrapping or weakening long-accepted underwriting safeguards like standard FICO scoring, title insurance, mortgage insurance, downpayments and appraisals.”

Biden administration officials sanctify their power grabs by prattling about closing the racial homeownership gap.

But minorities cannot afford any more favors from Washington. The 2008 housing crash slashed in half the average net worth of black and Hispanic households, setting millions of people back an entire generation.

More families lost their homes during the 2008 housing crash than lost homes during the Great Depression in the 1930s.

Rather than waiving title insurance for federally backed mortgages, the feds should finally pull the plug on Fannie and Freddie.

Those entities have officially been in “federal conservatorship” since their 2008 bankruptcy. They should have been euthanized long ago.

Biden’s latest proposals vivify how Washington policymakers learned nothing from their previous housing debacles.

There is no reason not to expect politicians and bureaucrats to again whipsaw the housing market they claim they’re rescuing.

Unfortunately, reckless economic policies can be good politics as long as the damage does not surface until after the next election.

James Bovard’s latest book is “Last Rights: The Death of American Liberty.”

Load more…

{{/isDisplay}}{{#isAniviewVideo}}

{{/isAniviewVideo}}{{#isSRVideo}}

{{/isSRVideo}}

At different stages of the pandemic, the housing scene morphed from a buyers’ market to a sellers’ market—and sometimes back again—with lightning speed. But as of about a year now, it’s not much of a market at all since the market went into a deep freeze with historically low levels of homes changing hands. Plus, mortgage rates hit their highest level for nearly 40 years and are set to stay “higher for longer.” That’s all led to what experts have called the “lock-in effect,” and it has resulted in gridlock for months on end.

But President Joe Biden wants to get things moving. “I know the cost of housing is so important to you,” Biden said during his State of the Union address last week. “If inflation keeps coming down, mortgage rates will come down as well. But I’m not waiting.” And he’s taking action, but will it be enough?

The White House is proposing some relief for homeowners: a one-year $10,000 tax credit for middle-class, starter-home residents who feel locked in to their low mortgage rates to move to a bigger home. By White House estimates, this should open up 3 million starter homes for those desperately trying to break into the housing market.

Along with the seller tax credit, Biden proposed a swath of housing-related programs including a first-generation down payment assistance program, housing voucher program expansion, and rental assistance for low-income households.

The White House spoke to Fortune after Biden’s address, with Deputy Treasury Secretary Adewale Adeyemo saying it bluntly: “We have a supply challenge in the economy. Since the financial crisis, we’ve built too little housing here in the United States.”

He was echoing the remarks of Fed chair Jerome Powell himself, who had recently testified to Congress about the economy and concluded, “The housing market is in a very challenging situation right now.”

So will Biden’s proposals move the needle?

Not everyone is convinced that the new seller-focused tax incentive proposal will have the desired effects of making housing attainable for lower-income families and younger generations. While $10,000 will be “nothing to sneeze at” for some families who will be forced to move this year regardless of home prices and mortgage rates, it likely won’t be enough to meaningfully move the needle on transaction activity, writes Bloomberg columnist Jonathan Levin.

“The so-called ‘mortgage lock-in’ effect for existing homeowners, who enjoy low and fixed monthly payments, is still far too powerful to undo given the size of the proposed incentive,” Levin wrote.

How much does a starter home cost in the U.S.?

Housing affordability in the U.S. has gotten so bad that first-time buyers have to make 13% more than they did in 2022, according to a July 2023 Redfin report. That’s because a typical starter home in the U.S. now costs a record $243,000—which is a whopping 45% more than pre-pandemic starter home prices.

Home prices like this have left first-time homebuyers “on a wild goose chase because in many parts of the country, there’s no such thing as a starter home anymore,” Sheharyar Bokhari, Redfin senior economist, said in the report. “The most affordable homes for sale are no longer affordable to people with lower budgets due to the combination of rising prices and rising rates.”

The lock-in effect, therefore, has disproportionately affected younger generations like millennials and Gen Zers who would typically be scooping up starter homes by this time in their life. Yet these generations are still the most housing-obsessed, according to a December 2023 Bank of America report that shows some 60% of Gen Z respondents, and nearly 60% of millennials, said they think homeownership is more important than it was during their parents’ generation.

While Biden’s tax credit proposal for sellers could have the same effect as a 1.5% mortgage rate reduction, it could actually irritate one of the other major issues facing the housing market today: low inventory levels.

“This proposal would increase demand for starter homes, which are already in short supply, thereby driving up prices,” Edward J. Pinto, a senior fellow and codirector of right-wing think tank AEI’s Housing Center. “In addition, many of the 3.5 million beneficiaries would have been able to buy a home without the credit. However, since money is fungible, these families will have additional purchasing power to bid up the price of homes.”

What’s more is that the Biden tax credit could have the unintended consequence of opening up more small homes for baby boomers looking to downsize during the next few years, since the same starter homes that the household-forming fortysomethings want are also ideal for downsizing grandparents.

“There’s a big overlap between select baby boomers and select millennials,” Ali Wolf, chief economist at Zonda, a distributor of housing market data and consulting, previously told Fortune. “The key difference here is that the baby boomer will likely be able to tap home equity by selling their existing home, allowing them to perhaps make a more compelling offer on the home compared to the millennials, especially if the latter group are still renting.” In other words, baby boomers are more likely to win the housing market with more cash on hand.

Whether Biden’s housing tax credit for sellers is effective may end up being a moot point if it’s denied by Republican legislators—and it could be unlikely we’ll see meaningful change during an election year.

“It remains unclear which of these policies are most likely to succeed in Congress in this hotly contested election year,” Nick Luettke, Moody’s Analytics associate economist, said in a statement. “Housing affordability has become a key issue for Americans spanning all demographics and political divides, and housing policy has mostly remained steady in recent congressional budgets.”

The Biden administration sees a major opportunity to shrink the federal government’s sprawling real estate footprint and is making the project a top priority in its fiscal 2025 budget proposal.

The White House, in the 2025 budget plan released Monday, proposes giving the federal government’s landlord, the General Services Administration, $425 million to right-size the federal footprint and reduce long-term costs through a new “optimization program.”

The White House budget plan also calls for giving GSA “broadened authorities related to the disposal of excess property.”

“The expanded authority will allow GSA to assist agencies in identifying and preparing real property prior to the agency declaring a property excess,” the White House wrote in its budget request. “Currently, agencies do not always complete these types of activities because agencies must fund the activities from limited resources. This expanded authority will help to reduce the federal footprint by providing the funding required to assess and prepare potential excess properties for disposal, the funds will then be recovered from the proceeds of sale.”

The administration is doubling down on efforts to sell and dispose of underutilized federal buildings and land, at the urging of Congress.

An independent agency, the Public Buildings Reform Board, is also taking a closer look at the issue. Since 2019, the board has recommended underutilized, but high-value federal properties for GSA to sell. GSA, so far, has sold 10 PBRB-recommended properties.

GSA, in a press release Monday, said the $425 million real estate optimization fund would allow the agency to “reconfigure and renovate federal buildings to better utilize space and to expedite the disposition of unneeded federal facilities.”

The agency added that the optimization fund would help GSA make better use of existing federal building space, and reduce spending on leased office space.

GSA Administrator Robin Carnahan said in a statement Monday that the budget plan “reflects critical, targeted investments that will accelerate GSA’s efforts to right-size the real estate portfolio,” and if implemented by Congress, “these sound investments will yield big returns for taxpayers.”

The administration’s budget proposal would also give GSA full access to revenues and collections in the Federal Buildings Fund, where it deposits rent payments collected from agencies using GSA-owned properties.

Congress since 2011 has diverted about $1 billion each year from the Federal Buildings Fund to cover other agencies’ budgets.

GSA officials have told lawmakers that siphoning off these funds has delayed investments in federal buildings, and limited opportunities for agencies to consolidate office space.

The Federal Buildings Fund is GSA’s primary source of maintenance, repair, and construction funding for buildings that it owns.

“The FBF has hit a tipping point with a growing backlog of deferred maintenance and an increasing number of missed opportunities to consolidate from leases into more cost-effective federally-owned space – particularly given the unique opportunity to re-shape the federal footprint and optimize building utilization,” the budget proposal states.

The White House estimates that nearly $13 billion in agency rental payments, over the past 15 years, were never appropriated by Congress.

“At the same time, the GSA inventory of federally owned buildings is seeing an increase in deferred maintenance while experiencing cost increases year over year for unfunded projects,” the budget proposal states. “This year, the budget again proposes a reform to ensure that all agency rental payments can be used for construction and maintenance and repair, as intended, rather than merely sitting unavailable for use in the fund.”

The budget would also build on GSA’s announcement last November to put 23 additional federal properties through its disposition process.

GSA expects the properties, once offloaded, would eliminate up to 3.5 million square feet and would save the federal government $1 billion over 10 years.

The White House also proposes giving GSA $10 million in 2025 to set up an Electric Vehicles Fund to support the government-wide adoption of electric vehicles and electric vehicle supply equipment.

“The Electric Vehicles Fund (EVF) enables [GSA] to support the Administration’s goal of electrifying the Federal fleet by providing the mechanism for GSA to procure zero emission vehicles and the associated charging infrastructure on behalf of federal agencies,” the White House wrote in its budget plan.

Funding for new FBI headquarters

The Biden administration is also asking for $3.5 billion for a new FBI headquarters in Greenbelt, Maryland.

GSA selected Greenbelt from a list of three final sites last November, but agency watchdogs are reviewing the decision, at the urging of Virginia lawmakers and FBI Director Chris Wray.

The White House wrote that the FBI’s current headquarters, the J. Edgar Hoover building in downtown D.C., “can no longer support the long-term mission of the FBI.”

“Major building systems are near end-of-life and structural issues continue to mount, making the current building unsustainable,” the budget proposal states.

The Biden administration expects the FBI headquarters in Greenbelt will accommodate at least 7,500 FBI employees.

GSA and the FBI are looking for a federally owned site in D.C. to accommodate an additional 750-1,000 FBI personnel who would support day-to-day FBI engagement with the Justice Department, Congress and the White House.

“The administration plans to use existing balances in the FBI’s account previously appropriated for the new headquarters effort to build out a downtown D.C. location to support the FBI’s mission,” the budget states.

To support the funding for a new FBI headquarters, the Biden administration proposes setting up a Federal Capital Revolving Fund.

Under this proposal, Congress would appropriate the total amount of money needed for the project upfront. GSA would then repay the revolving fund, over the course of 15 years, by taking out about $233 million each year from the Federal Buildings Fund.

“The administration’s FCRF proposal provides a new budgetary mechanism to fully fund the costs of very large civilian real property capital projects that are difficult to accommodate in the annual appropriations process,” the budget states.

Congress already gave $645 million in prior year appropriations to support the construction of a new, suburban FBI headquarters.

Copyright

© 2024 Federal News Network. All rights reserved. This website is not intended for users located within the European Economic Area.

For days before his State of the Union address last week, there were whispers that Joe Biden would make a major push to expand the nation’s housing supply—a possibility that worried the yes-in-my-backyard activists who push for more construction in communities across the country. Political polarization in the United States has grown so dire that getting the president on your side can backfire. The morning of the speech, the White House rolled out some modest proposals, but fortunately for the activists, Biden himself offered only brief, mild comments on the subject, which were inevitably overwhelmed by commentary on more contentious issues.

“Many YIMBYs breathed a sigh of relief that Biden didn’t polarize the issue,” Brian Hanlon, the CEO of the advocacy group California YIMBY, told me, referencing political-science research indicating that if a president takes a strong public stand on an issue, people from the other party are less likely to back it.

A lot of causes—including immigration reform, vaccination, Ukraine funding, and, most recently, in vitro fertilization—have supporters across the ideological spectrum but nevertheless have become mired in red-blue polarization, blocking what could be bipartisan legislation to address major issues facing Americans. In Congress, lawmakers regularly work together across the aisle, but on one condition: The issue in question can’t be too politically salient—that is, the type of issue that voters really care about. This is why Congress can pass laws about subsidizing semiconductors but not laws addressing immigration.

For groups that want to get their priorities enacted, the question is how to gain enough attention without getting caught up in the polarization vortex. And no movement is walking this tightrope more precariously than the YIMBYs—who typically favor easing restrictions on housing development.

Their movement was born in San Francisco, a city where the last Republican elected official left office in 2014 after serving on the Bay Area Rapid Transit Board of Directors. But as the housing-affordability crisis spread to cities and states across the nation, so too has the network of activists, lawyers, elected officials, and policy wonks. That movement has now taken root not just in liberal enclaves such as San Francisco and Portland, Oregon, but also in Salt Lake City and Whitefish, Montana.

Over time, YIMBY tactics have shifted from lobbying city councils and town zoning boards one by one to pushing governors and legislatures to ease zoning rules and other housing-supply constraints across entire states. Henry Honorof, the director of a loose national coalition of pro-housing groups, told me that no state has passed pro-housing legislation without bipartisan support. Even in solidly blue California, Democratic YIMBYs need Republican converts. Helpfully, making housing more affordable appeals to equity-minded leftists, while deregulating the private market appeals to property-rights-loving conservatives.

The greatest fear of many pro-housing advocates is that their issue will be caught in the cross fire of the presidential election. It has happened before.

In 2020, then-President Donald Trump tried to activate NIMBYism in the electorate. In an August 2020 Wall Street Journal op-ed co-authored with his secretary of housing and urban development, Trump warned that the “left wants to take [the] American dream away from you” by pushing for “high-density housing.” He escalated these attacks on Twitter, on the campaign trail, and even, obliquely, on the debate stage. Yet Republicans and Democrats did not sort themselves into NIMBY and YIMBY camps, at least in part because news outlets and voters were so focused on COVID-19 that housing policy got little attention.

Over the past four years, as the affordability crisis has worsened, the YIMBYs have gained ground. In conservative Montana, an anti-California message spurred lawmakers into passing pro-development bills; in Washington State, ambitious proposals were passed in the name of affordability and racial equity. But members face pressure on both sides to abandon ship. How long can they hold on?

One reason the YIMBY movement has remained bipartisan is that it’s decentralized. But the gang gets together periodically for a national conference amusingly called “YIMBYtown”—the rare place where you might find socialists, centrist economists, and Trump-supporting elected officials all in the same room, working toward the same goal. But when I attended this year’s event, in Austin, Texas, some cracks in the coalition were showing.

The most explosive moment came at a panel about housing affordability in Texas. On stage was Brennan Griffin, an official at the progressive nonprofit Texas Appleseed. He was flanked by conservatives: On one side sat Judge Glock, a director at the conservative Manhattan Institute who has called for clearing homeless encampments; on the other was Cody Vasut, a Republican state representative who also works as the director of litigation at the conservative Texas Public Policy Foundation.

Early in the panel, the heckling started: “Why should we believe that any of these people in here care about affordable housing in Austin?” a protester named Cynthia Vasquez asked. She and a handful of others started walking through the event room, handing out flyers that accused the moderator and one of the panelists of “criminalizing unhoused people” and faulted four local progressive city-council members for associating with conservatives. They were met with some derision as mumbles of “Oh, boy” and “There you go” filtered through the room.

When I spoke with the protesters, they cited concerns that included rising property taxes for low-income homeowners if development pressure increased in East Austin and the lack of affordable-housing mandates in the recent upzoning proposals supported by local YIMBYs. But they were also clearly galled by the mere fact that the conference was claiming to work on housing affordability while joining with conservatives.

The protesters themselves would certainly not consider themselves YIMBYs, but a handful of conference participants were visibly affected by their display. Just as Trump in 2020 was threatening the coalition from the right, the protest in Austin pointed to perhaps the greater threat: The coalition could fall apart starting from the left. During the question-and-answer period that followed the protest, one audience member asked panelists to discuss the concerns about displacement that low-income residents of many communities express. “The people who are screaming and hollering, they’ve got real fears,” Denzel Burnside, the executive director of the North Carolina advocacy group WakeUP Wake County, said—to applause from much of the crowd.

After the conference, Dan Reed, the regional policy director for the D.C. urbanist group Greater Greater Washington, published a brief blog post expressing misgivings about the prominent role played by Montana’s Republican governor, Greg Gianforte, and urging fellow housing advocates to do better. Even as YIMBYs were notching up wins in Montana, Reed noted, state lawmakers expelled a trans colleague from the floor. By highlighting conservatives such as Gianforte, Reed argued, the movement “feeds the perception” that it’s for “white libertarian bros.”

And yet, when I talked with Burnside immediately after the disrupted panel, he expressed no misgivings about joining with conservatives on housing policy. “I’m in the South, red state,” he said. “This can be a bipartisan issue.” For a former minister who has worked to enact progressive policy change in conservative states, compromise is a way of life. “I’m always trying to find the ecumenical, theological, philosophical position of welcoming the neighbor,” Burnside explained. “Even if that neighbor does not look like me. Even if that neighbor doesn’t think like I think … I got my patch, you got your patch, but in order for us to become a whole carpet we gotta find some places that we weave in the middle.”

One thing that helps bind an ideologically diverse pro-housing movement is that everyone in a community suffers when housing prices soar. Checking Zillow is a nonpartisan activity. The other thing keeping the coalition together is that, well, it’s barely a coalition at all. YIMBYs work in the context of their own states and cities. No national group dictates the bills they support or the messages they send.

Burnside’s group in North Carolina is part of a burgeoning national federation called the Welcoming Neighbors Network, a group that has deliberately tried to maintain a low profile while connecting local independent groups with research, organizing, and policy assistance as needed. Honorof, the director of the network, told me that, wherever members are working on housing matters with allies on the right or on the left, “there’s a very explicit understanding that we’re not talking about anything else.”

This approach is possible only because two things can be true at once: Housing is important, and housing isn’t everything.

Christian Solorio is a 34-year-old progressive former state representative in Arizona who works as an architect by day and serves on the board of two pro-housing organizations in his state in his free time. As we sat together in Austin, he was waiting for updates about the state Senate vote for the Arizona Starter Homes Act, a bill that would prevent cities with populations exceeding 70,000 from requiring large lot sizes and large square footage, and from imposing other regulations that push houses to be more expensive.

The bill has received bipartisan support and bipartisan opposition. It passed the House with 15 Democrats and 18 Republicans voting for it, while 13 Democrats and 13 Republicans voted against it. The Senate was similarly divided. Solario recounted that the bill’s passage in the House coincided with a heated partisan debate over an anti-immigration bill that Democratic Governor Katie Hobbs has already promised to veto. How did Democratic legislators go from arguing about the most divisive border-state issue to crossing the aisle and voting with their opponents on a Republican-led pro-housing bill? Because that’s how politics works.

That doesn’t mean the bill will become law. Hobbs told reporters she’s still considering whether or not to sign the Arizona Starter Homes Act, noting that she prefers legislation with support from local jurisdictions, and this bill has been opposed by the local-government lobby. Either way, the political price is low. In a state as divided as Arizona, where the last gubernatorial election was between Hobbs and the right-wing firebrand Kari Lake, no one’s switching their votes over zoning policy.

Not even die-hard YIMBYs. “I’m a Democrat; I voted for the governor,” Solorio told me. “And if she ended up being the biggest NIMBY in our state, I’d still vote for her reelection because zoning, even though I’m one of the biggest zoning-reform advocates in the state … still doesn’t rise high enough for me to flip my vote.”