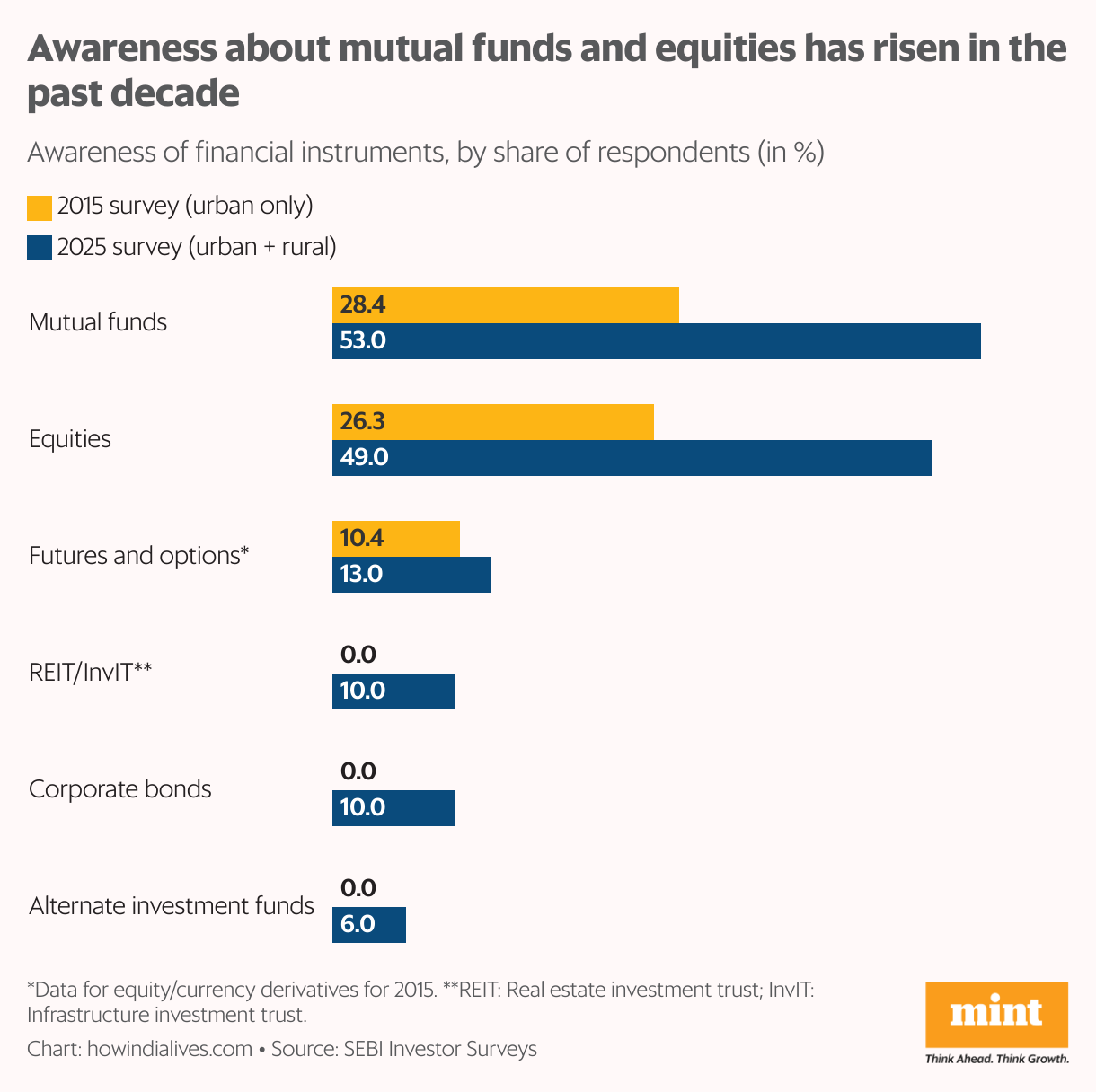

A decade ago, a similar survey found that just 28.4% of respondents were aware of mutual funds. This was only for urban residents. If the rural population were included, the number would have been lower. However, awareness does not necessarily translate into actual investments—only 9.5% of Indians invest in securities market products.

Growing awareness

The Securities and Exchange Board of India (Sebi) surveyed around 53,000 respondents—investors and non-investors—in both rural and urban areas. In terms of headline numbers, 53% of the survey respondents were aware of at least one securities market product, with urban areas registering a much higher rate of 74%, compared with 56% in rural areas. Among securities products, awareness of mutual funds was highest at around 53%, followed by equities at 49% (26% among urban residents in 2015). Awareness of more specialized products, such as futures and options, or real estate investment trusts (REITs), is understandably lower, at 13% or below.

One difference between the 2025 survey and the 2015 one was that the earlier one also asked respondents about more traditional investment products, such as bank deposits, post office schemes, and even gold and real estate. As expected, there was a sharp difference—close to 100% awareness of concepts like bank deposits (urban residents only) versus mutual funds, at just 28.4%.

Awareness, not action

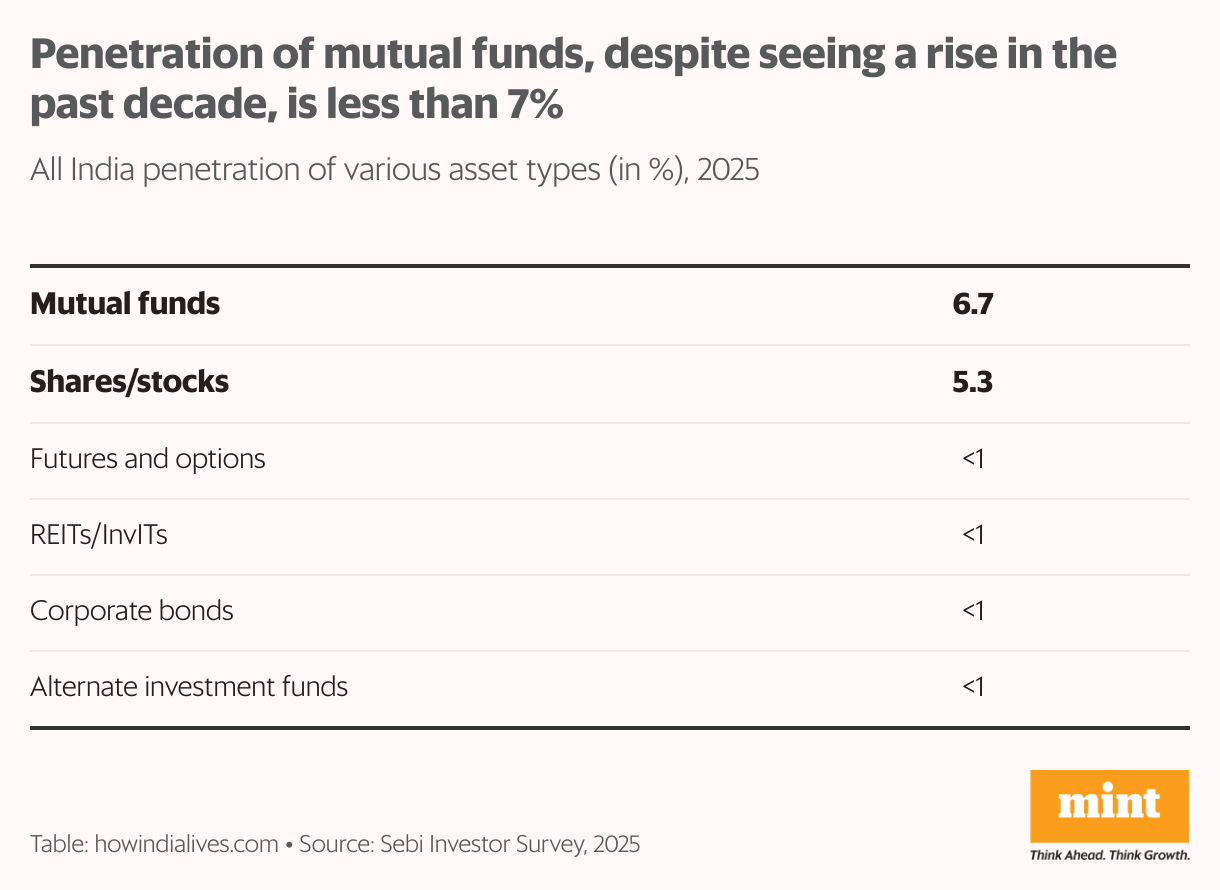

The major challenge has been penetration, as only 9.5% of respondents invested in some securities product. “Higher awareness is not translating into penetration,” the survey noted. Only 6.7% of the population actually invests in mutual funds, and 5.3% in equities. For the remaining instruments, which are either higher up the risk chain or more complex to understand, it is less than 1%.

Penetration (defined as investment in at least one product) in the top nine metros was 23%, against just 6% for rural areas as a whole. Education levels affect product uptake: 27% of postgraduates have invested in at least one securities product, while the uptake falls to 19% among graduates. Uptake at an overall level has progressed at a slow pace. Ten years ago, among urban residents, investment in mutual funds was 9.7% and equities 8.1%; adjusted for rural areas, the gains would be significantly lower. Worse, of the 9.5% overall who are invested, only about three-fifths are active investors.

Low-risk appetite

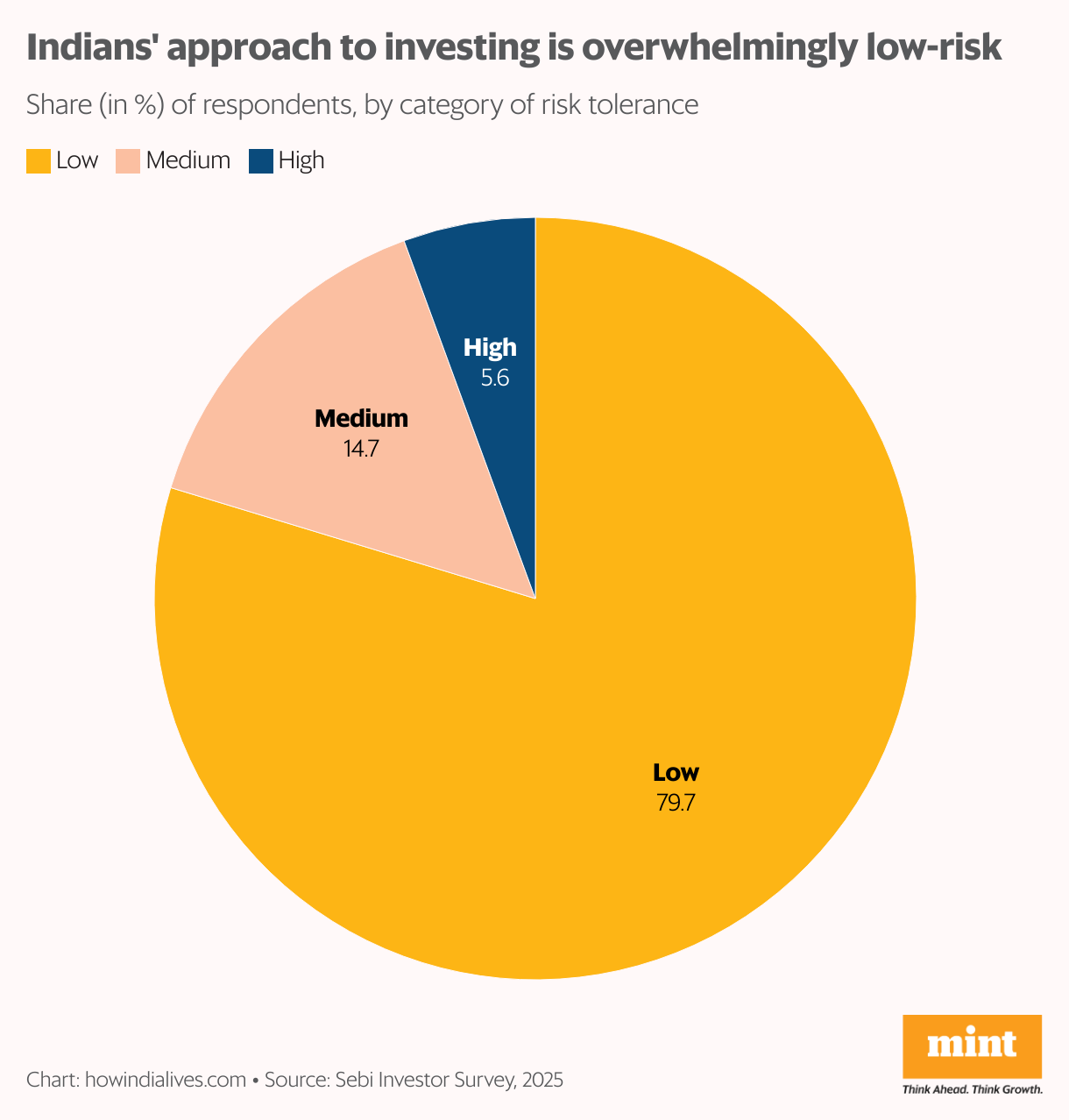

Of the 53% of the population who are non-investors, but aware of securities market products, above a fifth said they “intend” to invest in such a product over the next year. The challenge is risk tolerance. Securities market products, as opposed to relatively “safe” products like bank deposits or post office deposits, carry an element of risk. This is possibly one reason why mutual funds or equities see relatively low levels of investment in spite of widespread awareness.

The Sebi survey indicates that nearly 80% of the population has a low risk tolerance when it comes to investing. Risk tolerance is tied to various factors, such as education, but it is also an issue of income security. For example, salaried individuals showed a higher uptake of securities products than the self-employed (23% vs 17%). According to the survey, the attitude of such investors is “preservation of capital (amount invested) is more important to me than returns, and I need to have good but stable and reliable returns with minimal losses”.

Safe than sorry

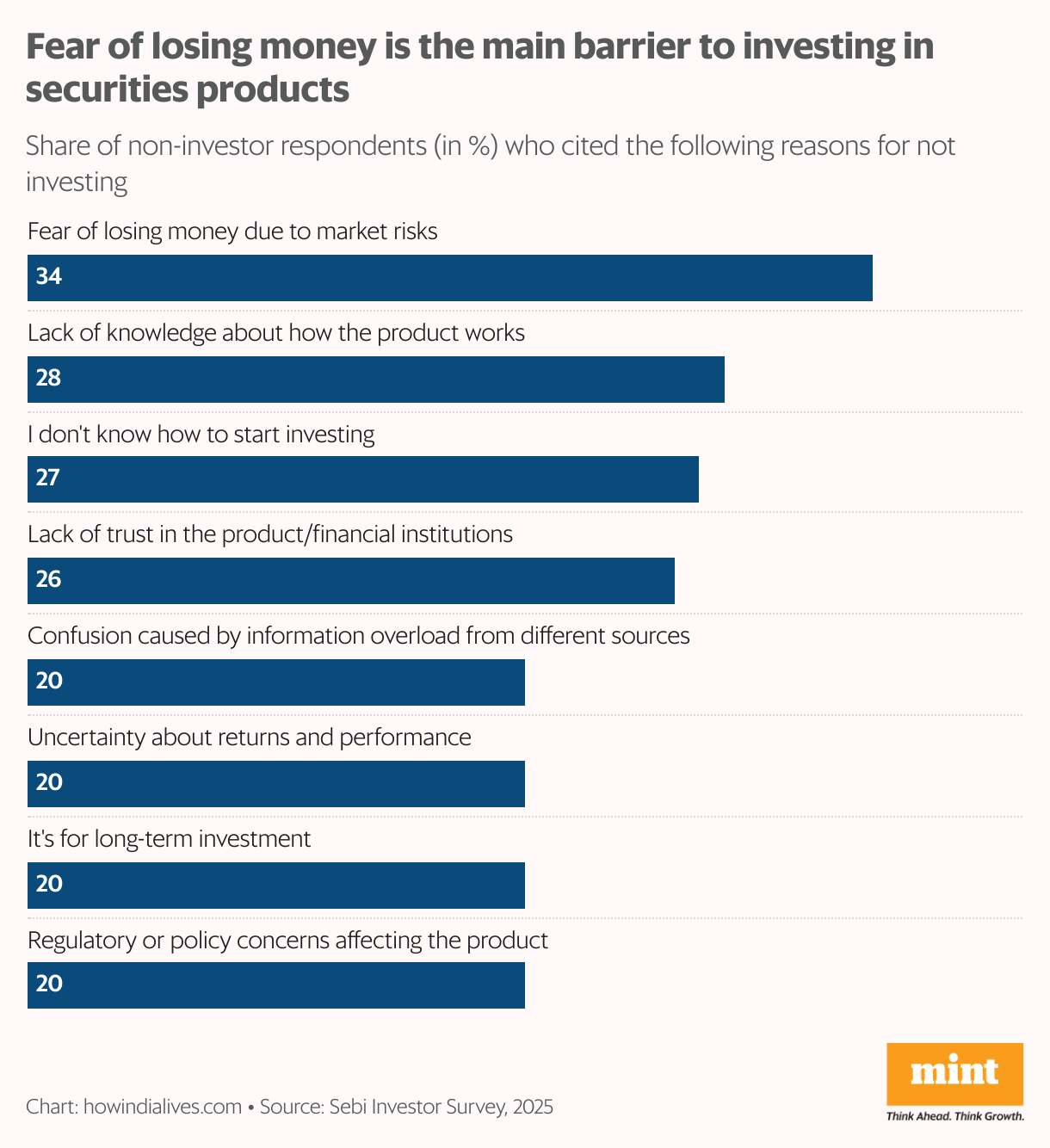

The survey asked respondents to choose specific reasons for not investing in securities market products. In line with their low risk tolerance, 34% of investors cited fear of losing money due to market risks as the reason. The next biggest barrier cited by investors was the lack of knowledge on how to start investing, followed by a lack of trust in the product or the financial institution selling it.

This risk aversion has remained relatively unchanged over the past decade. The 2015 survey described how investors associated the word risk with different meanings. “A direct question on perception of risk highlights the risk aversion among Indian investors. When the word ‘risk’ is mentioned, ‘danger’ is the first word that comes to the mind of 33% of investors, and 23% think of ‘loss’, and yet another 20% think of it as ‘uncertainty’. Perceptions that risk can be thrilling (16%) or can lead to opportunities (8%) are limited to less than a quarter of the investor base,” the survey had noted.

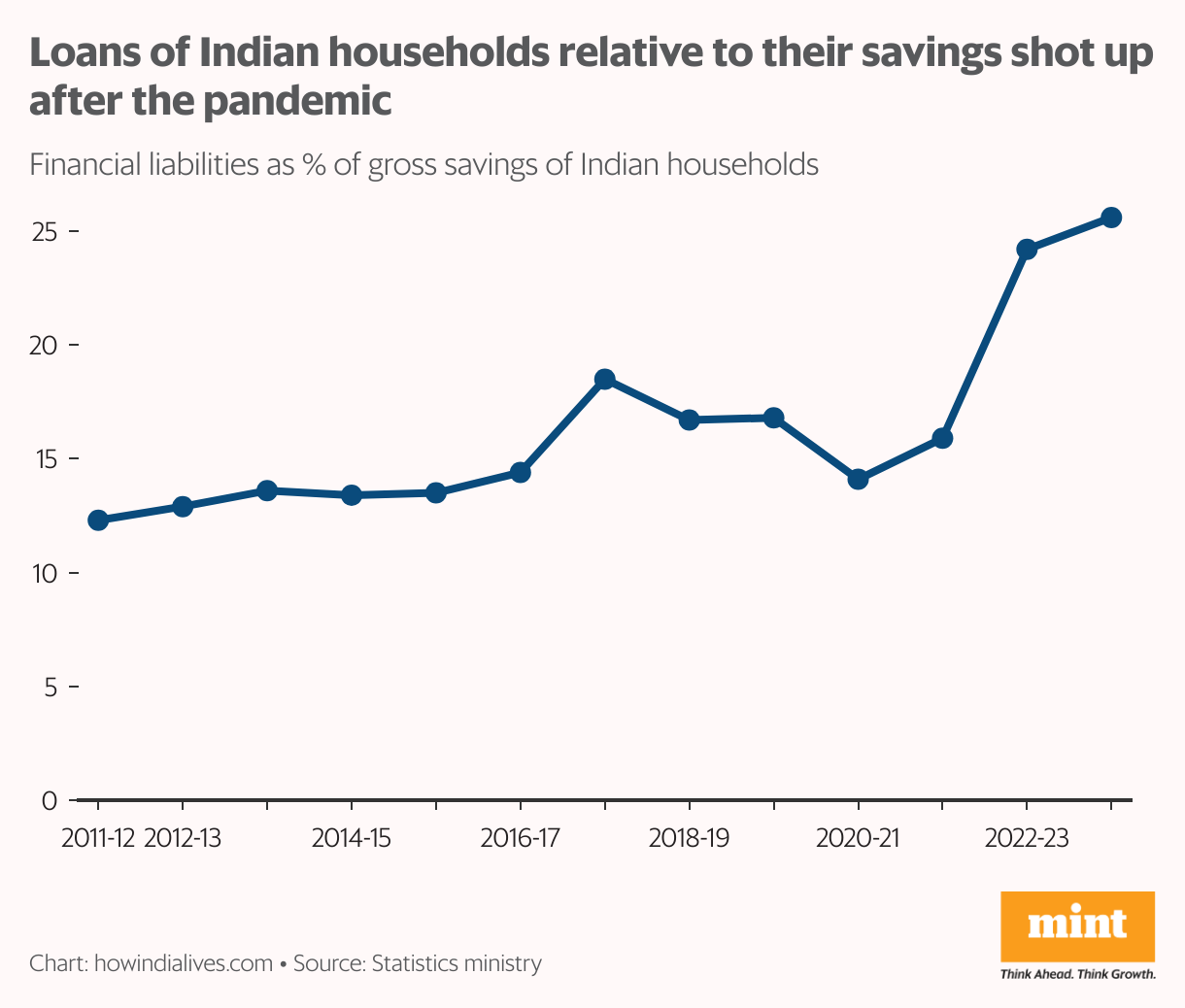

The loan factor

Rather than something that Indian investors are inherently prone to, risk aversion is also a result of the macroeconomic environment. Even among respondents with disposable income, it is highly likely that they have become more risk-averse, rather than less, over the last decade. This is because financial liabilities, as a share of physical savings (for example, real estate or land) or financial savings (such as bank deposits or mutual funds), have risen sharply from 12% in 2011-12 to 26% in 2023-24.

What does this imply? Financial liabilities are largely loans, entailing a fixed outgo over their tenure. If the share of such fixed commitments rises as a share of the amount available to save, this has two effects. One, a greater share of incomes goes towards servicing loans than investing. Two, even with the surplus left after servicing EMIs, protection of capital and relatively safe returns could become a greater priority than investments in instruments that promise higher returns but come with risk and uncertainty.

www.howindialives.com is a database and search engine for public data.

{kind=link}