Key Takeaways

- The House Price Index (HPI) tracks the movement of single-family house prices in the U.S., published by the Federal Housing Finance Agency.

- HPI data, sourced from Fannie Mae and Freddie Mac, helps estimate changes in mortgage defaults, prepayments, and housing affordability.

- Rising house prices can boost the economy by creating jobs and increasing consumer spending, while falling prices can reduce confidence and lead to economic downturns.

- The HPI differs from the S&P CoreLogic Case-Shiller index as it includes refinancing appraisals and provides wider coverage of home price trends.

- HPI reports exclude data from non-conforming sources like Veterans Affairs or FHA loans, focusing on conventional conforming mortgages.

What Is the House Price Index (HPI)?

The House Price Index (HPI) measures changes in home prices across the U.S. housing market. It is published by the Federal Housing Finance Agency (FHFA) and is an important economic indicator, helping track home price trends, analyze mortgages, and predict market movements. The HPI is based on data collected from Fannie Mae and Freddie Mac, which helps ensure accurate and reliable information.

How the House Price Index (HPI) Measures Housing Trends

The HPI is pieced together by the FHFA. Data is compiled by the FHFA using information supplied by the Federal National Mortgage Association, typically known as Fannie Mae, and the Federal Home Loan Mortgage Corporation, commonly known as Freddie Mac.

The HPI is based on transactions involving conventional and conforming mortgages on single-family properties. It is a weighted repeat sales index, measuring average price changes in repeat sales or refinancings on the same properties.

An HPI report is published every quarter in addition to a monthly report. Data is compiled by reviewing mortgages purchased or securitized by Fannie Mae and Freddie Mac.

0.2%

The increase in the HPI in April 2024 from the previous month. Home prices increased 6.3% on an annual basis from April 2023.

The Economic Impact of the House Price Index (HPI)

The HPI is one of many economic indicators that investors use to keep a pulse on broader economic trends and potential shifts in the stock market.

The rise and fall of house prices can have big implications for the economy. When prices increase, more jobs are created, confidence rises, and consumer spending goes up. This paves the way for greater aggregate demand, boosting gross domestic product (GDP) and overall economic growth.

When prices fall, the opposite tends to happen. Consumer confidence is eroded, and the companies profiting from the demand for real estate lay off staff. This can sometimes trigger an economic recession.

Comparing the HPI and S&P CoreLogic Case-Shiller Home Price Indexes

The HPI is one of many trackers of home prices. Some of the most well-known alternatives are the S&P CoreLogic Case-Shiller Home Price Indexes.

These indexes use different data and methods, leading to varying results. For example, the HPI weighs all homes equally, while the S&P CoreLogic Case-Shiller indexes are value-weighted.

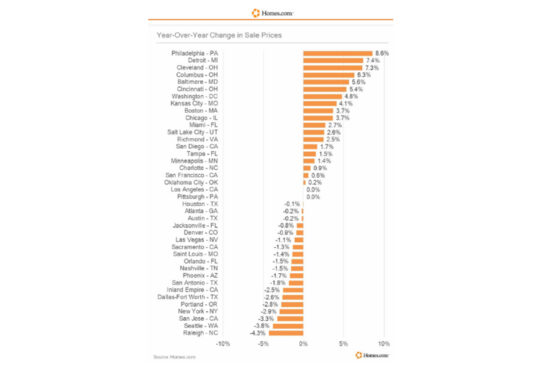

While the Case-Shiller indexes only use purchase prices, the all-transactions HPI includes refinancing appraisals as well. The HPI also provides wider coverage. The U.S. CoreLogic S&P Case-Shiller index rose by 1.2% between March 2024 and April 2024. It increased by 6.3% on an annual basis between April 2023 and April 2024.

The Role of Fannie Mae and Freddie Mac in HPI

The HPI measures average home price changes using mortgages purchased or secured by Fannie Mae or Freddie Mac. That means loans and mortgages from other sources, such as the United States Department of Veterans Affairs and the Federal Housing Administration (FHA), do not feature in its data.

Fannie Mae

Fannie Mae is a government-sponsored enterprise (GSE) that is listed on the public market yet operates under a congressional charter. The company’s goal is to keep mortgage markets liquid. It does this by purchasing and guaranteeing mortgages from the actual lenders, such as credit unions, and local and national banks—Fannie Mae cannot originate loans directly.

The FNMA expands the liquidity of mortgage markets and facilitates homeownership for low-, moderate-, and middle-income Americans by creating a secondary market. Fannie Mae was created in 1938 during the Great Depression as part of the New Deal.

Freddie Mac

Like Fannie Mae, Freddie Mac, or the FHLMC, is also a GSE. It purchases, guarantees, and securitizes mortgages to form mortgage-backed securities (MBS). It then issues liquid MBS that generally carry a credit rating close to that of U.S. Treasuries.

Freddie Mac can borrow at lower interest rates than other institutions due to its U.S. government ties.

How Do You Tell If a House Is a Good Price?

To determine if a house is a good price, you can check the sale prices of recently sold properties in the neighborhood, compare the price with other properties for sale in the market, speak with a real estate agent, and consider the appreciation value.

Should I Offer the Full Asking Price on a House?

Knowing whether or not you should offer the full asking price on a house will come down to a few factors. One of the main factors is whether the property being sold is in a buyer’s market or a seller’s market. If it is a seller’s market, you may have to offer the full asking price or above, whereas in a buyer’s market, you may be able to offer a lower price. If you need to offer the full asking price or more, it is generally recommended to offer 1% to 3% more.

What Brings Down the Value of a House?

Many factors bring down the value of a house, such as any new planned construction in the area that would be seen as less than desirable, such as a highway. Foreclosures in the neighborhood would bring down prices, as well as the increased likelihood of natural disasters in the area or a greater impact due to climate change. Even rising interest rates can bring down the value of a house, as the increase in mortgage rates makes homes more expensive, which reduces the demand.

The Bottom Line

The HPI is an important economic indicator that tracks changes in single-family home prices. It shows broader trends in the housing market and economy. Published by the FHFA, it uses data from Fannie Mae and Freddie Mac, and is used by investors to understand shifts in consumer confidence, GDP, and job growth. Changes in home prices can affect employment, spending, and overall economic health. Watching HPI trends can give insights into mortgage affordability, market demand, and the state of the economy.

{kind=link}