Every week, Mansion Global poses a tax question to real estate tax attorneys. Here is this week’s question.

Q: My company is temporarily relocating me to Shanghai for two years. I’m thinking about buying a home there, but does it make sense to do so if I’m going to sell the property when I move back?

Tax-wise, it’s not necessarily a good idea to buy a home in Shanghai for a two-year period unless you believe home prices there will rise significantly, said Michael W. Galligan, partner in the Trusts & Estates Department of Phillips Nizer LLP in New York City.

Buying a home in Shanghai will mean that you will need to file tax returns in both the U.S. and China, Mr. Galligan said. Therefore, tax compliance becomes considerably more complicated and costly.

More:How Does a Foreign Buyer Get Around the Residency Requirements of Certain Countries?

Advertisement – Scroll to Continue

Also, you may not get full credit for the China tax when you pay your U.S. taxes, he pointed out. And finally, it’ll be incumbent upon you to make sure you understand all the tax aspects of buying in China and retain competent Chinese tax advisers and tax preparers.

Then, when you are ready to sell your home in Shanghai, you will likely be subject to both capital gains tax in China (currently 20%) and in the U.S. (as much as 20%), Mr. Galligan said.

In the U.S., you may also have to pay the 3.8% Medicare tax, also known as the Net Investment Income Tax (NIIT), and any state income tax on the profit from the sale of the home. NIIT kicks in when modified adjusted gross income is $200,000 or more for single taxpayers or $250,000 for married couples filing jointly.

State income tax applies while you were in China if you were a resident of a U.S. state that has a state income tax, or you sell the home during a year that you establish residence in such a state, Mr. Galligan explained.

It’s worth noting, he said, that if you opt not to go to China and instead buy a house in the U.S. and then selling it after the same two-year period, the taxes would be similar to what you’d pay on a home in Shanghai if you’d bought and relocated there.

More:What are the Top Tax Concerns When Flipping a Home in the U.S.?

But that shouldn’t rule out buying the property in Shanghai. If real estate prices there are expected to rise over the next two years, a home purchase may be “an opportunity to earn some U.S. tax-free income,” said Jenny C. Lin, principal of Lin Tax Law in Walnut Creek, California.

Just as taxpayers in the United States can keep as much as $250,000 tax free in profits from the sale of their principal residence stateside through the home sale gain exclusion, so, too, can Americans who sell their homes abroad. “There is no requirement that the principal residence be located in the United States,” Ms. Lin said.

To claim this exclusion, the taxpayer must have owned and used the property as their principal residence for an aggregate of two years or more, she said.

A married couple filing a joint tax return doesn’t have to pay taxes on the first $500,000 from the sale of their home if they used the property as their principal residence and if neither spouse had used this exclusion within two years, Ms. Lin said.

More:What Could Be the Implications of Trump’s Tax Code Proposals on Global Investment?

If the home is sold before the two-year mark, because of health reasons or certain other unforeseen circumstances, partial exclusions may apply, she noted.

“You may not necessarily receive a credit or offset of $1 U.S. tax for every $1 dollar equivalent of tax that you pay to China,” Mr. Galligan said. So before buying, have your U.S. accountant or tax preparer run a draft calculation to verify whether your U.S. credit would fully offset the Chinese tax, and be sure to consult with a professional in China.

“The rules and requirements are complex,” Ms. Lin said, emphasizing the importance of working with a tax return preparer knowledgeable about income and information reporting involving cross-border situations. “U.S. taxpayers are required to report income on a worldwide basis and may also be required to report certain foreign assets or transactions.”

Therefore, buying and selling a home in Shanghai “is a lot of trouble to go through unless you think the market for residential properties [there] is going to significantly appreciate over the two-year period and that the likely profit makes all these steps worthwhile,” Mr. Galligan said.

Email your questions to editors@mansionglobal.com. Check for answers weekly at www.mansionglobal.com.

So you’re thinking about buying a vacation property. I’ve owned a vacation property since 2007 and don’t recommend doing so. However, let me introduce a vacation property buying rule to follow so you don’t get in trouble like me.

The vacation property buying rule to follow is to buy a vacation property for lifestyle first, income and returns second. In other words, don’t buy a vacation property as an investment with potential positive. Buy a vacation property because you think it will bring joy in your life. If you think this way, then you will enjoy your vacation property more.

I also wouldn’t buy a vacation property until after your first kid turns three either. Before kids, you should be free to vacation anywhere in the world untethered. Once your kid turns three, s/he will remember and appreciate your vacation property more.

A Hot Tub Encounter At My Vacation Property

Back in February 2017, during a hot tub party at my vacation property at Everline Resort at Palisades Tahoe (Resort At Squaw Creek), I got to know a fellow owner who retired five years ago as a partner from a major law firm. We got to talking about the roller coaster ride we’ve had since purchasing our vacation properties 10 and 9 years ago, respectively.

He told me something surprising after I asked him somewhat jokingly what he plans to do with his property now that global warming was over. After all, Lake Tahoe got a record ~23 feet of snow in #Janburied 2017 and is shaping up to have a great 2020-2021 season.

He said, “Just continue to enjoy it. If you look at the latest listing prices, we’re back to even after an almost 50% fall. But I’d never sell because the property is worth an insignificant amount as a percentage of my net worth today. I’ll just leave the property to my kids to enjoy.“

Given this was a hot tub party, and not a personal finance 1X1 consulting session, I didn’t dig deeper into his finances. But given the retired lawyer was 20 years my senior with adult children, I realized I had just “seen the future.”

Vacation Property As A Percentage Of Net Worth

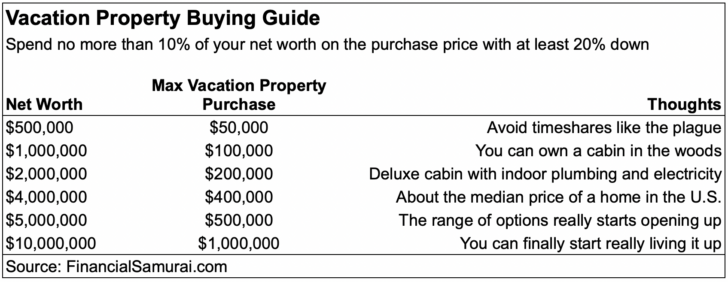

My vacation property buying rule centers around limiting the purchase price based on a percentage of your net worth.

When I bought my vacation property in 2007, the purchase price was equal to roughly 25% of my net worth. In 2017, using the same purchase price, my vacation property was worth about 8% of my net worth. And in 2020, my vacation property is worth around 5% of my net worth. With each decline as a percentage of my net worth, I’ve felt better.

By the time I’m 63 years old in 20 years like the law partner I met at the hot tub, the property should be worth just less than 2% of my net worth and completely paid off.

Any asset that’s worth less than 10% of your total net worth starts feeling like a relatively insignificant amount of money. Think about it.

Your 10% asset could lose 100% of its value, and you’d still have 90% of your net worth intact. This is one of the reasons why my 1/10th rule for car buying has been a popular guideline because it helps protect consumers from their spendy selves.

Bright Side Of Spending So Much

I so happened to spend a significant 25% of my net worth on my Lake Tahoe vacation property right before financial armageddon hit in 2008-2009. Despite saving 15% off the original asking price, this was still one of the most ill-timed purchases ever.

But if I had spent just 10% of my net worth on the property, I probably wouldn’t have lost more than an hour’s worth of sleep over my purchase. I certainly would have been bummed to see my property’s value go down so much. However, it wouldn’t have been so bad because I knew I could make up for the loss after saving 50% of my income for one full year.

There’s a positive side to spending too much of my net worth on a vacation property at a bad time. Because I did, I started Financial Samurai in 2009 due to all the pain of losing so much. Ah, thank goodness for always having a positive mindset!

Hopes And Dreams Of Owning A Vacation property

What the ex-law partner said about passing his property down to his children really spoke to me since when I first wrote this post in February 2017, I was expecting to have a son in April 2017.

Given his daughters are now 26 and 28, and he bought his condo 10 years ago, he lamented that he never got to spend as much quality time up in Tahoe with his family as he hoped. As teenagers, his daughters wanted to hang out with their friends somewhere else instead.

Related: A Massive Generational Wealth Transfer Is Why Everything Will Be OK

Since first coming up to Squaw in 2001, I’ve always imagined it to be a place where I could take my kids during their school holidays.

During summer vacation, we can go hiking, mountain biking, boating, river rafting, kayaking, and water skiing.

During winter break, we can go sledding after seeing who made the best snow angels. Lake Tahoe is magical.

Of course, not everything goes according to plan, but I’m someone who has the patience to think in 10-year increments. After all, I spent 11 years at my last firm and I’ve consistently written on Financial Samurai since 2009.

Further, I’m now a varsity boys tennis coach because I want to see what it’s like working with teenagers at least 14 years before having one of my own! Perhaps through this new job, I can figure out a better way to relate to my future teenager so he will want to spend time with his old man.

A Vacation Property For Family

The value of my vacation property will personally skyrocket if I’m able to fulfill my vision of hanging out with my little one(s) up at The Resort. Neither he nor I would have a care in the world.

When he grows up to be an adult, he and his old man can carve down the leisurely blue run and talk our own stories as we soak our aching muscles in the outdoor hot tub.

Hopes and dreams are what make owning a vacation property worth it. The kids had a magical time swimming in the pools, going down the water slide, soaking in the hot tub, and running around on the grounds. Then we went hiking in the mountains as well.

The only downside was that our car got damaged while being valet parked! Oh well. I’m glad we own a used car that isn’t too expensive.

A Vacation Property Buying Rule To Follow

If you can view your vacation property as an investment in lifestyle instead of as a financial investment, you’ll find your asset much more rewarding.

In order to never have your vacation property feel like a burden, heres my vacation property buying rule: spend no more than 10% of your net worth on a vacation property purchase price (not downpayment). For example, if you net worth is $3 million, spend no more than $300,000 on a vacation property.

I feel so much better now that my vacation property is worth less than 10% of my net worth versus when it was 25% of my net worth.

If you foresee a rapid increase in your income and net worth, then you can probably stretch your vacation home budget to 25% of your net worth. But I don’t recommend doing so based on all the worry and stress I had to go through. Buying a vacation property for enjoyment and then constantly worrying about whether it will financially ruin you is counterproductive.

Finally, before buying a vacation property, make sure you calculate how much you’ll actually be able to use the vacation property a year. Run a cost of ownership comparison to the cost of simply renting a nice place anywhere you want.

Overestimating the usage time is quite common. The reality is that most people can only take off at most 4 – 6 weeks a year. Only if you’re unemployed, financially independent, or have a location independent business can you truly maximize your vacation property.

Wait Until You Are A Millionaire Before Buying A Vacation Property

If I followed this vacation property buying guide, I wouldn’t have foolishly bought a $715,000 vacation property in 2007. At the time, my net worth was about $2,200,000, which meant I was spending 35% of my net worth on a vacation property. After my net worth declined to $1,500,000 a couple years later, the vacation property I had bought accounted for almost 50% of my net worth!

If you’re super-bullish on your career and income, then you can certain spend a greater percentage of your net worth on a vacation property. However, I would try to maintain disciplined. A vacation property is generally a terrible investment. It is better to just rent and go on unique adventures instead.

My vacation property buying guideline essentially says you shouldn’t even consider buying a vacation property until your net worth is at least $3,000,000, where real millionaire status begins.

It’s been an amazing financial run since 2009. I’m sure some of you are far richer at this point in life than you could have ever imagined. Just make sure you follow my vacation property buying rule and stay disciplined.

Invest In Real Estate More Strategically

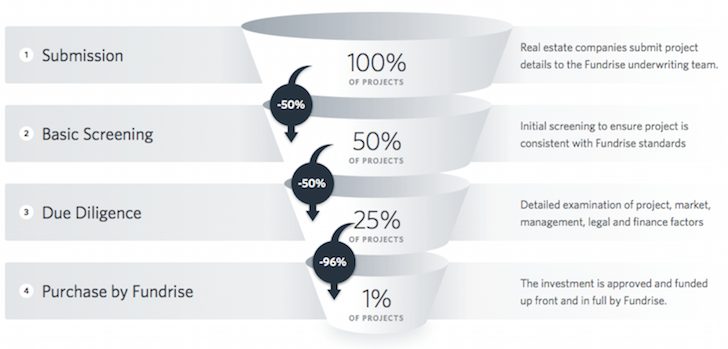

Owning a vacation property is more a lifestyle choice and less of a good investment choice. If you want to make money in real estate, take a look at Fundrise, one of the largest real estate crowdfunding platforms that has investment opportunities all around the country. It has over $3.3 billion in managed assets for over 500,000 investors.

With only an investment minimum of $10, you can dollar-cost average into residential and industrial real estate in the Sunbelt, where valuations are lower and yields are higher. Fundrise is a sponsor of Financial Samurai and Financial Samurai is a six-figure investor in Fundrise.

If you are an accredited investors and want to invest in individual real estate opportunities mostly in 18-hour cities, check out CrowdStreet. 18-hour cities are secondary cities with lower valuations, higher rental yields, and potentially higher growth due to job growth and demographic trends.

I personally have $954,000 in real estate crowdfunding in markets outside of expensive San Francisco, Honolulu, and New York City. It feels great to earn income passively and diversify my real estate holdings.

Vacation Property Update 2024.

I finally took my boy and wife up to our vacation property for the first time in July 2019 and it was magical! Then I took my son and my 10-month-old daughter again in late October 2020 and it was also pretty nice. Here’s what it was like taking a vacation during a pandemic.

Then in April 2024, I took the family up to our place in Lake Tahoe on an epic family ski vacation. The value of our vacation property has increased tremendously now that we have kids. I can’t wait to go up there for 12-14 years while the kids are still living at home.