Vetted by HousingWire | Our editors independently review the products we recommend. When you buy through our links, we may earn a commission.

Unless you’ve been living under a rock or on a remote desert island, you’ve probably heard of ChatGPT. Chat Generative Pre-trained Transformer or ChatGPT is a chatbot developed by OpenAI that became available online on November 30, 2022. It can be a game changer for your productivity and real estate business. If you’re curious about how to use ChatGPT for real estate, read on to learn my 12 favorite applications for this innovative AI tool.

OpenAI, the company behind the scenes of ChatGPT, is in partnership with Microsoft, so we can be sure that it’s here to stay. They are already making improvements to the user interface. Until October 2023, ChatGPT could only access data up to 2021, but it can now access real-time data across the internet. However, access to real-time data and web searching are only available for Plus and Enterprise users using the GPT-4 model who have enabled “Browse with Bing”. A free version is available and has plenty of uses for agents and brokers.

12 ways to use ChatGPT for real estate agents and brokers

You may have thought to yourself, “I’m a real estate agent, not a computer programmer. How on Earth is this going to help me?” There are hundreds of ways to use ChatGPT for real estate and in your business as a real estate agent. From helping with endless writing tasks to summarizing market data, the possibilities are almost endless.

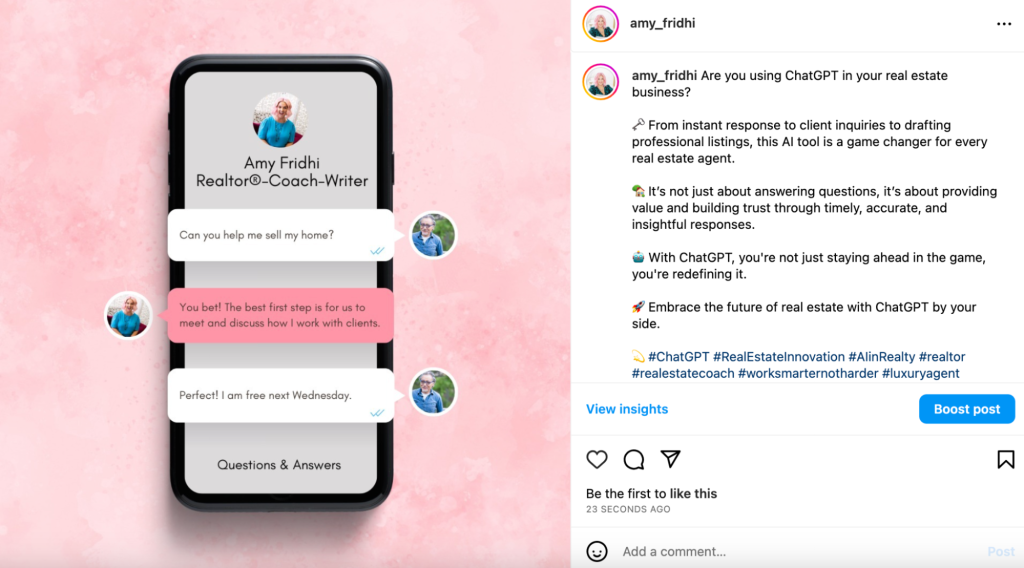

Let me introduce you to my friend Chatty. I use it so often that I have given it the nickname Chatty because I feel like she is a colleague of mine. I’ve tried many, many ways to ask ChatGPT for help. Some results have been amazing, and some were just so-so. Most recently, I used it to help me write the weekly newsletters that I send to my mailing list. Here’s the latest one I wrote about Zillow. I’ll share what I’ve learned and some helpful prompts that have worked for me.

Getting started with ChatGPT

If you’re unsure how to get started, here are three quick steps to get you going. First, go to https://chat.openai.com. Under the heading “get started” click “sign up”. Follow the prompts to use your email or sign in with your social media accounts. It’s free and easy, so why not give it a try!

1. Email campaigns

Create personalized email content for your clients, delivering valuable information and nurturing relationships. One of the great things about using ChatGPT for real estate emails is that they can really be personalized. So many of us see the generic emails that are provided by our CRMs and cringe. Make your emails convey your personal brand and messaging with help from ChatGPT.

2. Property descriptions

Generate compelling property descriptions and listings using ChatGPT, making your listings stand out in the market. We’ve all written the generic “welcome home to this stunning 3-bedroom colonial home, set on a beautifully landscaped lot, blah blah blah.” Don’t be that person. Write something that will get eyes on your listing and stop the scroll.

3. Social media posts

Create engaging social media posts and content to boost your online presence and connect with a wider audience. Facebook, Instagram, and LinkedIn are free marketing, and if you aren’t using these social media platforms as an agent, you are missing out. ChatGPT can help real estate agents quickly and easily create content ideas, captions, and hashtag lists specific to each platform.

4. Content marketing

Create blog posts, articles, and guides about various real estate topics, showcasing your industry and local area knowledge and attracting organic traffic to your website. Longer form written content such as blog posts and LinkedIn articles are part of a savvy agent’s content marketing strategy. Well-written, SEO content can help drive your website traffic, position you as a subject matter expert, and build your newsletter audience. If you aren’t a gifted writer or don’t enjoy it, let ChatGPT do the heavy lifting. I often use it to write quick and accurate social media captions. Here is one about using ChatGPT for generating auto-responses, and I used ChatGPT for the caption, talk about meta!

5. Neighborhood information

Provide clients with detailed information about local neighborhoods, schools, amenities, and other factors that influence their buying decisions. With access to real-time data, you can use ChatGPT to create neighborhood guides that list the hottest coffee shops, the greenest dog parks, and the best schools in your area.

6. Answers to common questions

Develop a comprehensive list of frequently asked questions and use ChatGPT to provide instant, accurate responses on your website or social media platforms, ensuring clients have access to the information they need. You can even take this information to create PDFs or printable resources for use at open houses.

7. Automated email responses

Set up automated email responses using ChatGPT to acknowledge inquiries and provide basic information to potential clients. Have you ever stopped to think how many times you type the same reply to someone in your business? Got a new listing and people keep asking the same questions? Automate it with Chat GPT. This can save you time and ensure a prompt response rate.

8. Market reports

Generate comprehensive market reports to share with clients, demonstrating your expertise in the local real estate market. One of the things that can help establish newer agents who don’t have a strong sales history is local market knowledge. Using ChatGPT to generate real estate information and packaging it for clients is a great way to show that you know what you’re doing and understand your market.

9. Language translation

Utilize ChatGPT for real estate transactions that may be in another language. If you are unilingual and have clients who speak a different language or who don’t speak English natively, ChatGPT can help. Your ability to provide multilingual answers and documents, and break down language barriers will help you to support a broader range of clients.

10. Create buyer and seller guides

Use ChatGPT for real estate guides. It can swiftly and accurately create detailed guides that you can provide to potential buyers or sellers. These can include to-do lists, advice, timelines, an overview of what a home inspection is, an explanation of the closing process, and FAQs. It can be totally customized to your needs as a real estate agent.

11. Write video scripts

If you like to provide video content to your clients and social media audiences, use ChatGPT to create detailed scripts for you to use. Some people are natural in front of the camera. If you are but still need a little help remembering your lines, use ChatGPT. If you aren’t and have no idea what to say, you too can use ChatGPT to draft a script for your next YouTube video, IG reel or story, or Loom explainer video that you want to share with clients.

12. Market insights

Stay updated on the latest market trends and statistics by asking ChatGPT to provide real-time data and insights. All of our associations send out monthly reports, but having more up-to-date information is much better. This data can be used just for your own reference or you can use the information to create social media posts, blog articles, or as information for your clients.

BONUS: Realtor® résumé

I may be alone in this, but I am trying hard to get Realtor® Résumés to catch on. I think the more professionally we can present ourselves as agents, the more seriously we will be taken as an industry. ChatGPT can help you to generate a résumé that highlights your skills, experience, and certifications.

Best practices for writing ChatGPT prompts

Part of the trick to getting ChatGPT to do what you want is training it. No, seriously. It needs to learn your style, and you need to give Chatty good instructions. There are some general guidelines to use for getting the best results. Don’t worry about getting things perfect the first time. Two of the tricks I’ve leveraged are refining my prompts and asking ChatGPT to regenerate the response so I can get different or better answers.

Writing good prompts for ChatGPT is essential to receive accurate and valuable responses. Here are some tips for creating effective prompts when using ChatGPT for real estate agents.

Be clear and specific

Provide clear and specific information about what you’re seeking. Instead of asking, “Tell me about the housing market,” ask, “Can you provide recent sales data for single-family homes in the 90210 ZIP code?” (Who knows what popular show that zip code is a throwback to?)

Use open-ended questions

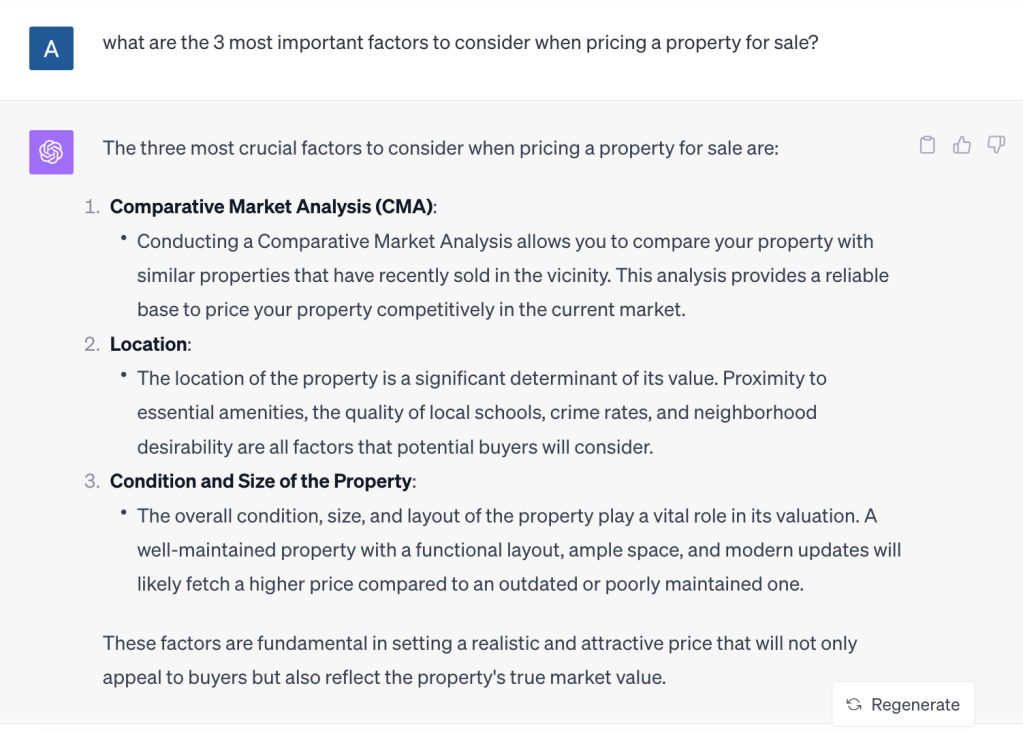

Frame questions in an open-ended manner to encourage more detailed and informative responses. For instance, ask, “What are the most important factors to consider when pricing a property for sale?” You could ask a yes or no question, but what good is that? Get as much substance and detail as you can. As an example, here’s ChatGPT’s reply to my query about home pricing:

Break down complex questions

If you have a multi-part question, consider breaking it down into multiple simpler questions. This can result in more accurate and comprehensive responses. ChatGPT has a nifty copy function (look for the little clipboard icon) so you can quickly and easily copy the results into a document to organize later.

Include context

When relevant, provide context to help ChatGPT understand the subject or background of your question. For example, “In the current seller’s market, what strategies can buyers use to negotiate better deals?”

Specify data and sources

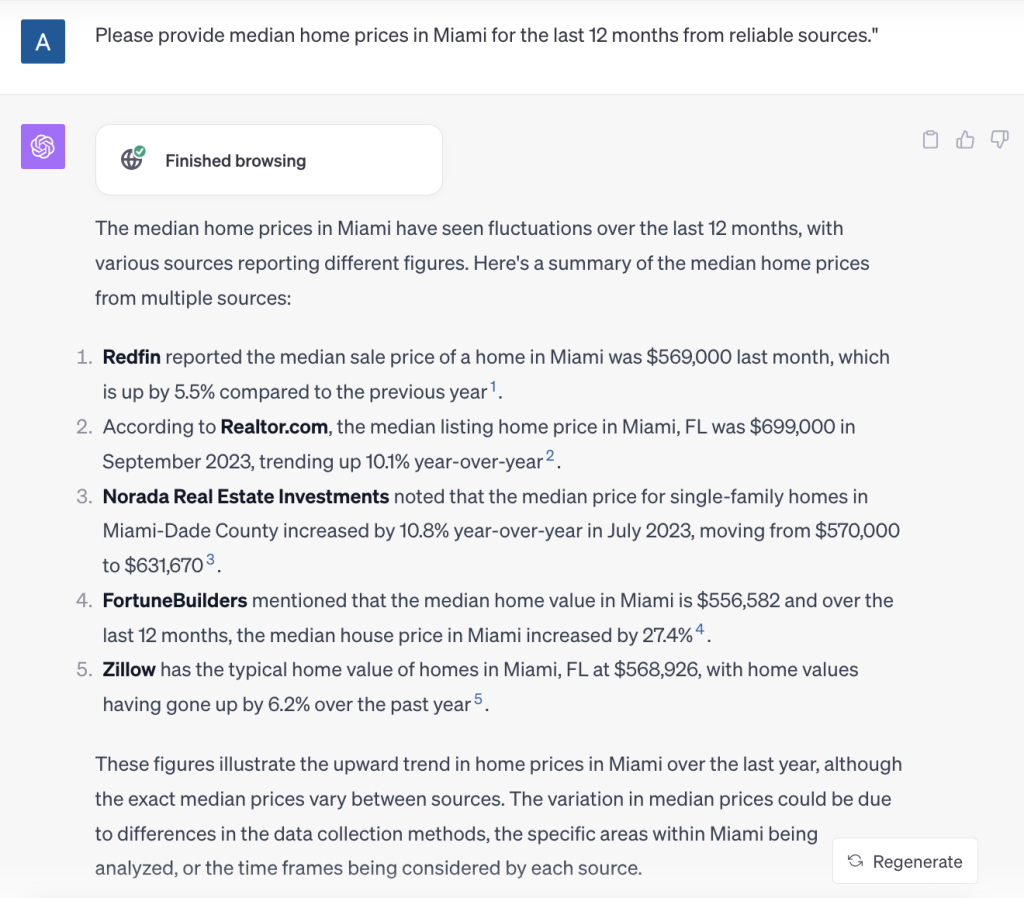

If you need data or information from a specific source, indicate it in the prompt. For instance, “Please provide median home prices in Miami for the last 12 months from reliable sources.” And if you forget to be so specific in your initial prompt, don’t hesitate to ask ChatGPT to refine the response. As an example, here’s ChatGPT’s reply to my query about Miami:

Avoid jargon

Keep in mind that not all users may be familiar with real estate jargon. Use plain language or provide explanations for complex terms when necessary. You can use industry-specific language in your prompt, but be sure the output you receive is something that can be understood by non-agents.

Test and iterate

Start with simple prompts and refine them as you gain a better understanding of how ChatGPT responds. Experiment and test different phrasings and structures to see which yields the best results. As I said before, you can’t break anything.

Request step-by-step guidance

If you want ChatGPT to help with a process, ask for step-by-step instructions. For instance, “Can you guide me through the process of creating a comparative market analysis for a property?”

SEE ALSO: How to prepare a comparative market analysis (CMA) report

Check for consistency

Ensure that the information provided in responses aligns with your knowledge and real estate standards. It is possible that ChatGPT provides a response based on the rules and practices of one state, but your state operates differently. Cross-reference with trusted sources when necessary.

Avoid leading questions

Try to keep your questions neutral and avoid leading questions that might inadvertently bias the responses. You may have certain religious or political beliefs, or even just opinions about the housing market, but try to keep those out of your prompts. You want to ensure that the output is relevant and applicable to all clients.

The full picture: ChatGPT for real estate

These are not hard and fast rules. There is no wrong way to use ChatGPT. These are recommendations that will save you some leg work and hopefully generate useful responses to use in your business. By following these guidelines, you can improve the quality and relevance of responses you receive from ChatGPT and make it a valuable tool for your real estate needs.

As creepy as it may seem, the more you use ChatGPT for real estate needs, the better she will get. She will learn your style, your voice, and how you like the information presented. And if you’re wondering why I use female pronouns for ChatGPT, it’s because she’s wicked smart and always has the answers I need.

My ChatGPT cheat sheet for real estate agents

Not sure where to start or what to ask? Use these 20 prompts with ChatGPT to create content and resources to use in your real estate business.

“Can you provide a brief overview of the factors that affect property valuations?”

“What are some effective home staging tips to make properties more appealing to potential buyers?”

“Give me insights into the current real estate market trends in [Your City].”

“What should I consider when advising a client on purchasing an investment property?”

“Can you create a guide for first-time homebuyers on the steps to purchasing a home?”

“What strategies can sellers use in a competitive real estate market to maximize their returns?”

“Assist me in writing a compelling listing description for a suburban family home with three bedrooms and a backyard.”

“Share some effective negotiation techniques for real estate transactions.”

“Explain the basic types of mortgages and their pros and cons to help me educate my clients.”

“Provide me with a list of essential questions to ask during a client consultation for home buyers.”

“Can you help me create a checklist for hosting a successful open house event?”

“Outline the legal steps required for closing a home sale in [State or Country].”

“List the amenities and public services available near [Address or Neighborhood].”

“Calculate the monthly mortgage payment for a home priced at $[Amount] with a down payment of $[Amount].”

“Compare the neighborhoods of [Location 1] and [Location 2] in terms of real estate prices.”

“Provide a list of schools and their ratings in the [specified area].”

“Create a checklist for organizing an open house at [Property Address] on [Date].”

“Estimate the cost of renovating the kitchen and bathrooms in a home located at [Address].”

“Draft a basic lease agreement for a rental property located at [Address].”

These prompts are just the tip of the iceberg. I’ve tried to cover a range of topics that can help you use ChatGPT in your business, but feel free to explore and experiment. You can’t break anything, and ChatGPT won’t get mad at you.

Work smarter, not harder

So now that you’ve gotten an overview of how to use ChatGPT, let it work for you and lessen your workload. Don’t be afraid to try new things. Soon enough, Chatty will be your best friend too.

Have a ChatGPT prompt that worked for you? Share it in the comments.

Related

Key takeaways

- Let your mortgage lender or servicer know if you’re getting a divorce.

- Your divorce mortgage options include refinancing your mortgage, selling your home or paying your ex-partner for their share of equity.

- To help you decide, calculate the amount of home equity you have, as well as any tax implications and impact to your credit.

One of the biggest decisions divorcing couples face is who gets the house in a divorce. If you’re in this situation, your options might depend on how the home is financed and titled, among other factors. Another question people might ask during a divorce is, “What are my rights if my name is not on the mortgage?” Here’s everything you need to know about how divorce impacts your mortgage.

Mortgage options when dealing with divorce

1. Refinance your mortgage

Some divorcing couples with a joint mortgage decide to refinance to a new mortgage in only one of the spouse’s names. This releases a spouse from responsibility for that mortgage when their name is removed from the loan.

However, unless that partner’s name is also removed from the title, they can still benefit from the sale and equity in the home. It’s important to not only refinance but also update the house title to reflect one owner. When only one spouse is on the mortgage but both are on the title, you’ll need a quitclaim deed to remove one spouse’s name from the title.

Keep in mind: The spouse applying for the refinance can use only their own income and credit score to qualify, warns financial advisor Jeremy Runnels, CFP, of West Coast Financial in Santa Barbara, California. Depending on current rates, you could get a much higher rate when you refinance, as well.

“The lender is going to look at the individual and make sure they’re OK having them as the sole guarantor,” says Runnels. “The issue is can you afford it, and that goes for either spouse.”

If a partner will receive alimony or spousal support, they can use that income to qualify for a refinance, as long as the divorce settlement stipulates that they will receive alimony for at least three years, says Runnels.

If the couple has equity in the home, the spouse keeping the house could alternatively apply for a cash-out refinance to pay their ex-partner their share (more on that below).

Some refinancing options you have when dealing with a divorce include:

- Conventional refinance

- Streamline refinance (for FHA, VA and USDA loans)

- Cash-out refinance

2. Sell your home

The divorce agreement might call for the sale of the home and the splitting of profits. If you go this route — and many couples do — consider the costs. These might include the Realtor’s commission, the costs of sprucing up the property to make it more attractive to buyers, real property transfer taxes and capital gains taxes.

3. Pay your ex for their share of equity

Let’s say your home is worth $300,000, and you owe $200,000 on the joint mortgage. In this case, you’d have $100,000 in equity, so you’d need $50,000 to buy out the other spouse’s share (assuming a 50/50 split).

To get the cash, you could refinance into a $250,000 loan in your name only, and use the $50,000 cash payout to settle up with your ex.

You’ll need to qualify for the refinance, however.

“Their income needs to be high enough to handle the new mortgage on their own, and the home must have the equity in it to take the cash out,” says Michael Becker, loan originator and sales manager at the Baltimore retail branch of Sierra Pacific Mortgage. “FHA and conventional cash-out refinances are capped at 80 percent loan-to-value, while you can go to 100 percent on a VA loan.”

If you want to keep the house and don’t have enough equity to do a cash-out refinance or the money to pay your ex their share, a home equity line of credit (HELOC) or home equity loan could be the solution.

“You could look at doing either a home equity loan or a home equity line of credit, as some lenders will allow you to go to 95 to 100 percent of the value of your home,” says Becker.

Important financial considerations when getting divorced

Deciding what to do with the marital home can get messy. Before diving into any particular course of action, consider the long-term impacts on your finances:

Evaluating your home equity

Whether you plan to refinance the joint mortgage or sell the home, you’ll need a professional appraisal report to determine it’s worth and any equity you might walk away with.

Sometimes, however, a couple doesn’t agree on the appraised value. This can cripple efforts to move forward and can mean spending more time and money on attorneys and appraisers. In this situation, it’s best for the parties to strive to agree on which appraiser to work with and to accept the outcome of the valuation, whatever it might be.

If you are selling the home, you might decide to split the equity (less closing costs and any repairs and improvements) or use it to pay off other debts you accrued together. Likewise, some couples include a provision in their separation agreement that they’ll accept the first offer on a home, provided it’s within a certain percentage of the list price.

Tax implications

Whether you sell the home as part of the divorce agreement or buy out your spouse’s share, capital gains taxes could come into play. This is a tax on the sale of capital assets, such as a home, when the profit exceeds a certain amount.

If you sell the home, you and your spouse might be able to deduct up to $250,000 of gain from your federal taxable income, but it applies only to the primary residence you’ve lived in for at least two of the last five years prior to the sale.

There are also tax considerations regarding alimony payments. The spouse who earns a higher income and pays alimony can’t deduct those payments from their taxable income, but the spouse receiving alimony does not have to declare it as income. (This applies to divorces finalized after Dec. 31, 2018.)

The higher-earning spouse could make a case for paying less alimony, which can lower the receiving spouse’s income to qualify for a new loan, says Runnels.

Conversely, alimony payments might hurt the payer’s income and chances for a mortgage.

“Can a spouse afford the house and all the alimony and child support payments?” says Runnels. “On the flip side, can the alimony (recipient) afford to keep the house, given they are responsible for all the expenses?”

Protecting your credit

Divorce is an emotional, often volatile event — but the worst thing divorcing couples can do is take financial revenge.

“Many times, out of bitterness, I’ve seen one or both spouses ruin the credit of the other spouse,” says Becker. “They decide that it’s the other person’s problem and refuse to pay bills that may be joint accounts. This can damage your credit greatly and keep you from being able to qualify for any mortgage for a long time.”

The bottom line: Keep paying all of your bills through the divorce process to protect your credit.

“Close your joint accounts and get your own accounts set up,” says Runnels. “If you’re arguing with your spouse over who is going to pay a bill, and you get a ding on your credit, it’s going to be harder to get a loan.”

FAQ about divorce and mortgages

-

Even if you plan to hold onto the house and pay the marital mortgage yourself, the names on the loan are ultimately the ones responsible for paying it — including your ex.

If for some reason you can’t pay the mortgage, your ex could refuse to pay it, damaging both of your credit scores and making it harder for you both to qualify for another loan. It’ll also be much more challenging to sell, gift or bequeath the home because your ex could claim some ownership of the property. In general, it’s best to take your ex’s name off the mortgage and move forward with your own, new loan.

-

It’s important to inform your mortgage lender or servicer of your divorce. This could help you avoid delinquency issues if your ex decides to stop paying the loan before the divorce agreement is finalized.

Welcome to Seattle’s real estate market, where luxury knows no bounds. This city stands out as one of the most vibrant, diverse, and notably expensive cities in the United States, particularly when it comes to buying and selling homes.

Nestled amid the stunning Pacific Northwest landscape and stunning neighborhoods, the Emerald City is no stranger to high-priced real estate. In fact, the median sale price for homes in Seattle reached $800,000 in September, nearly doubling the national median. However, these figures merely scratch the surface, as the top 5 neighborhoods boast an average median sale price of $1,867,500.

So, what makes Seattle’s most expensive neighborhoods so desirable? From the breathtaking waterfront mansions of Laurelhurst to the secluded elegance of Madison Park, Seattle’s most expensive neighborhoods offer beautiful craftsmanship architecture, unparalleled views, and lavish amenities. Join us on a journey through Seattle’s most luxurious and expensive neighborhoods, where your dream home awaits.

1. Denny Blaine

Homes for sale in Denny Blaine

Median sale price: $2,200,000

Nestled on the eastern shore of Lake Washington, this neighborhood is renowned for its stately homes, tree-lined streets, and historic architecture. The neighborhood showcases a mix of architectural styles, ranging from grand historic mansions to luxurious contemporary estates, and even modern condominiums with panoramic lake views.These homes are complemented by lush, meticulously landscaped properties, which often feature spacious yards and gardens that provide a serene retreat from the urban hustle and bustle.

What makes Denny Blaine particularly desirable is its prime location on the shores of Lake Washington, offering picturesque waterfront views, easy access to the lake’s recreational opportunities, and beautiful green spaces. The neighborhood’s leafy streets and quiet ambiance create a sense of seclusion while being just a short drive from downtown Seattle. This balance of tranquility and proximity to the city’s amenities, coupled with its stunning architecture and waterfront lifestyle, make Denny Blaine a highly sought-after community.

While Denny Blaine tops the list for most expensive neighborhood in Seattle, its median sale price is nearly 40% lower than 2022. If you’ve been eyeing a property in Denny Blaine, consider taking advantage of this opportunity.

2. Madison Park

Homes for sale in Madison Park

Median sale price: $2,050,000

Madison Park offers a blend of natural beauty and urban sophistication. Known for its proximity to Lake Washington and the inviting Madison Park Beach, this area attracts residents seeking a laid-back yet lively lifestyle. The neighborhood showcases a diverse range of home types, from historic Craftsman-style residences to modern waterfront estates, providing housing options that cater to a variety of tastes. With its tree-lined streets and an array of boutique shops, restaurants, and cafes, Madison Park exudes a friendly, small-town ambiance within the bustling city of Seattle.

Residents can enjoy a range of amenities, including lakeside activities like swimming and kayaking at Madison Park Beach, while the scenic Arboretum nearby offers walking trails and opportunities for outdoor exploration. The quaint Madison Street has a selection of charming boutique shops, renowned restaurants, and cafes.

With a limited supply of available properties, the demand from buyers looking to own a home in this lakeside neighborhood is high, pushing the median sale price up 12.3% YoY, to $2,050,000. Consequently, this surge in demand creates intense competition, multiple offers, and an upward trend in prices.

3. Portage Bay

Homes for sale in Portage Bay

Median sale price: $1,750,000

Coming in at number three for the most expensive neighborhood in Seattle is Portage Bay, a charming and picturesque neighborhood in Seattle. Nestled on Lake Union’s eastern shore, this waterfront community offers residents a unique opportunity to live in the heart of the city while enjoying a serene, waterside lifestyle. The neighborhood offers a diverse range of home types, from classic Craftsman and Tudor-style houses to modern townhouses and iconic floating homes, creating a vibrant residential tapestry.

Residents enjoy lush green spaces, including Portage Bay Park, and Lake Union’s tranquil waters for kayaking, paddleboarding, and boating, offering a dynamic juxtaposition to the city’s urban hustle. Nearby, Montlake Playfield provides additional options for outdoor activities. The neighborhood’s central location grants easy access to the University District and Capitol Hill, making shopping, dining, and cultural attractions conveniently close. Portage Bay’s city life and waterfront living makes the neighborhood an appealing choice for those who seek the best of both worlds, where the excitement of urban living coexists with lakeside relaxation and outdoor adventures.

The median sale price of Portage Bay is $1,750,000 million, up 15.5% from a year earlier. The area’s blend of urban conveniences, serene waterside living, and limited housing inventory contribute to elevated property values, attracting buyers willing to pay a premium for this unique lifestyle.

4. Laurelhurst

Homes for sale in Laurelhurst

Median sale price: $1,670,000

Laurelhurst, a prestigious and sought-after neighborhood in Seattle, is distinguished by its waterfront elegance and a strong sense of community. Perched on the shores of Lake Washington, this idyllic locale offers an array of home types, from historic Tudor and Colonial Revival mansions to modern luxury estates, all exquisitely designed to capture the natural beauty of the area.

The Laurelhurst Beach Club stands as the neighborhood’s primary attraction for those seeking a strong sense of community and the opportunity to connect with their neighbors. The club not only provides residents access to a private beach, swimming, and water sports, but it also serves as a vibrant hub for waterfront activities and community events. The proximity to the University Village shopping center and the University of Washington (often drawing UW alumni who seek to establish their roots in this welcoming community), offers convenience in daily living. The Burke-Gilman Trail is also close by and provides an opportunity for scenic walks, jogs, and bike rides.

What makes Laurelhurst particularly desirable is its serene lakeside setting, where residents can enjoy spectacular waterfront views, a strong sense of community, and an abundance of recreational opportunities.

This desirable neighborhood comes at a premium median sale price of over $1.6 million. The limited inventory and historical prestige of the area also contribute to the neighborhood’s expensive real estate market, further driving up prices.

5. Hawthorne Hills

Homes for sale in Hawthorne Hills

Median sale price: $1,667,500

Located in the northeastern part of Seattle, the Hawthorne Hills neighborhood is a secluded community known for its residential charm and scenic surroundings. Homes in Hawthorne Hills represent a mix of architectural styles, from classic mid-century designs to contemporary luxury residences, offering a variety of housing options to cater to different preferences and needs.

Residents can enjoy nearby parks, including Dahl Playfield and the scenic Magnuson Park, where families can engage in outdoor activities, picnics, and sporting events. The nearby Sand Point Country Club provides golf enthusiasts with opportunities to perfect their game on a well-regarded golf course. The University Village shopping center, located a short drive away, offers an array of shopping and dining options, making everyday conveniences readily accessible. Magnuson Park’s vast green spaces and Lake Washington’s shores provide opportunities for boating, swimming, and jogging.

Limited housing inventory plays a role in the competitiveness of Hawthorne Hills. The neighborhood’s popularity has led to a high demand for properties, leading to a median sale price of $1,667,500. Prospective buyers often face bidding wars and the need to act quickly to secure a desired property.

How to buy a home in a luxurious and expensive neighborhood in Seattle

If a home in these neighborhoods has been well maintained, has attractive outside spaces and landscaping, has been updated or maintains that vintage charm, and most importantly, is priced correctly – it will sell quickly. To secure a home in any of these neighborhoods, prospective buyers should schedule a house tour promptly, be aware of any review dates and seller inspections, and prepare an offer with good terms, only a few contingencies, and a quick close.

Understanding your competition is also a key factor for ensuring your offer stands out from the rest. Sellers often have specific needs and preferences, whether it’s prioritizing a quick close over the offer price or requiring a rent-back arrangement to secure their next home. By tailoring your offer to align with the seller’s motivations and crafting terms that cater to their unique circumstances, you can significantly enhance your chances of securing the home you desire in these highly competitive neighborhoods.

To maximize the likelihood of winning the home your heart is set on, it’s crucial to hire a dedicated real estate agent who can help you through the buying and process and who has your best interest in mind.

Buying a luxury home in Seattle, WA: final thoughts

The Seattle real estate market, while undeniably expensive, reflects the city’s unparalleled charm and beauty of life in Seattle that’s second to none, making every investment worth it. It’s true the housing market is fiercely competitive and the cost of living can be quite expensive, however, the rewards of owning a luxury home in Seattle is immeasurable — a place to call your own in one of the Pacific Northwest most luxurious neighborhoods.

If you’re buying a luxury home in Seattle, partnering with a seasoned real estate agent becomes essential in navigating the intricacies of the homebuying process. Whether you’re a seasoned Seattleite or a newcomer to the Emerald City, a Redfin Premier Agent brings invaluable knowledge and expertise to the table, guiding you through the complexities of the luxury market, including specific neighborhoods, market trends, and property values – ensuring you find a place to call your own in this extraordinary city.

Methodology: Rankings based on median home sale price data sourced from the Redfin Data Center during September 2023. Only neighborhoods with a minimum of three homes sold between July 1- September 30, 2023, were included.

Delaware may be one of the nation’s smaller states, but it certainly packs a punch in character and opportunity. From its strategic location on the East Coast and tax-friendly policies, to its vibrant communities and natural beauty, there is much to appreciate about life in the First State. However, like any location, living in Delaware has its share of drawbacks. In this Redfin article, we will look at what it’s like to call this state home, exploring the unique pros and cons of living in Delaware. So whether you’re looking for homes for sale in Wilmington, apartments in Dover, or just want to learn more about the area, join us as we embark on a journey through the First State.

Pros of living in Delaware

1. No sales tax and other great tax benefits

One of the standout advantages of living in Delaware is the absence of a state sales tax. This unique feature sets Delaware apart from many other states in the U.S. Residents of the “First State” can enjoy tax-free shopping, making their dollars stretch further and saving significantly on everyday purchases, big-ticket items, and even luxury goods. Additionally, the state does not tax Social Security income, and no inheritance or estate tax exists. These favorable tax policies contribute to a lower overall tax burden for individuals and families, offering an attractive financial incentive for those who appreciate keeping more of their hard-earned income.

2. Proximity to major East Coast cities

Delaware’s prime location on the East Coast offers a significant advantage to its residents. Positioned between the bustling urban centers of New York City and Washington, D.C., Delaware provides quick and convenient access to these metropolitan hubs’ cultural, economic, and professional opportunities. The state’s well-connected transportation infrastructure, including I-95 and Amtrak, makes commuting or weekend getaways a breeze. This geographic advantage allows Delawareans to enjoy the benefits of living in a more relaxed and affordable environment, while still having the vast array of amenities and services of major cities just a short journey away.

3. Beautiful coastal areas

The state boasts a stunning stretch of coastline along the Atlantic Ocean, featuring pristine beaches such as Rehoboth, Bethany, and Dewey Beach, each with a unique character. These coastal havens offer opportunities for sunbathing, swimming, water sports, and scenic walks along the boardwalks. Additionally, Delaware’s coastal areas are home to picturesque fishing villages like Bowers and charming beach towns, each exuding a sense of nostalgia and offering delectable seafood dining options.

4. Historic charm and cultural heritage

As one of the original 13 colonies, the state boasts a rich legacy celebrated through numerous historic sites and museums. Delaware enchants residents with its rich tapestry of history, ranging from the charming colonial-era buildings in New Castle to Dover’s pivotal role in early American history. Its charming historic districts and landmarks provide a living connection to the past, while cultural festivals, arts communities, and educational institutions help foster a dynamic appreciation for heritage.

5. Sense of community

Delaware’s residents often praise the state’s strong sense of community, fostered by numerous small towns and close-knit neighborhoods. Communities frequently unite for local events, festivals, and volunteering, reinforcing neighborly bonds and nurturing a supportive, inclusive atmosphere. The state’s modest size maintains this sense of connection even in larger cities, ensuring a network of support and meaningful relationships. This pervasive sense of belonging significantly enriches residents’ quality of life, adding to Delaware’s charm and making it an inviting place to live.

Cons of living in Delaware

1. High cost of living in certain areas

While Delaware offers diverse, appealing features, including its tax benefits and coastal beauty, it’s not without drawbacks, particularly concerning the cost of living in specific areas. Sussex County, famed for its scenic coastal communities, experiences a cost of living approximately 3% higher than the national average, driven in part by the elevated demand for housing in these picturesque towns. The state’s median sale price, at $341,500, is lower than the national median of $412,001. However, the median sale price in Lewes soars to $596,000, underscoring the considerable discrepancy in real estate costs. This higher cost of living in select areas can pose financial challenges for residents, affecting housing affordability and everyday expenses but there are many affordable places to explore.

2. Limited public transportation options

One notable drawback of living in Delaware is the limited public transportation options, particularly in some less urbanized areas. While the state’s metropolitan regions offer some public transit services, like Dover, which has a transit score of 28, the coverage and frequency of these systems can be limited. This leaves residents in more rural or suburban areas reliant on personal vehicles for commuting and daily transportation. This lack of extensive public transport can lead to increased traffic congestion, higher commuting costs, and limited accessibility for those who do not own a car.

3. Extreme weather fluctuations

Delaware’s weather patterns are characterized by extreme fluctuations, which can be a considerable con for residents. The state experiences all four seasons, but their transitions can be abrupt and unpredictable. Winters can bring heavy snowfall and cold temperatures, while summers can deliver sweltering heat and high humidity. Although often pleasant, the spring and fall seasons can also be marked by sudden weather changes, including severe thunderstorms and even hurricanes in some years. These rapid shifts can challenge planning outdoor activities and dressing for the day.

4. Coastal flooding and hurricane risks

With a significant portion of the state’s population concentrated along the Atlantic coast, Delawareans are more exposed to the potential consequences of coastal flooding and hurricanes. During hurricane season, the state faces the risk of severe storms and rising sea levels, which can lead to flooding, property damage, and displacement of residents. While the state has implemented measures and emergency response plans, including potential evacuation protocols, the recurrent threat of hurricanes can be a cause for concern, impacting both homeowners and the overall quality of life.

5. Smaller job market

The number of job openings and career advancement prospects can be more limited than larger metropolitan areas. The state’s compact size also means that commuters often look beyond Delaware’s borders for job options, adding to the complexity of the employment landscape. Consequently, career growth and industry diversity can be challenging, making it more difficult for professionals in certain fields to find their desired positions within the state.

Pros and cons of living in Delaware: Bottom line

Ultimately, the decision to call Delaware home depends on individual priorities and preferences. For some, the state’s serene coastal beauty and tax benefits may outweigh the disadvantages. For others, the challenges may weigh more heavily. Ultimately, living in Delaware balances the pros and cons to create a unique and fulfilling lifestyle in the “First State.”

What is the average salary of a real estate agent? It’s a common question that many aspiring agents and those interested in the field ask. Understanding the earning potential in real estate can help individuals make informed decisions about their career paths. In this blog post, we will delve into the topic of real estate agent salaries, exploring the factors that influence earnings and providing insights into the average income one can expect. So, if you’re curious about the financial prospects of becoming a real estate agent, keep reading to discover the average salary and more.

Understanding the Real Estate Agent Profession

Real estate agents play a crucial role in the housing market, acting as intermediaries between buyers and sellers. In this section, we will delve into what real estate agents do and highlight their importance in the market.

What Does a Real Estate Agent Do?

Real estate agents are licensed professionals who assist clients in buying, selling, or renting properties. They act as a bridge between buyers and sellers, helping them navigate the complex process of real estate transactions. Here are some key responsibilities of real estate agents:

- Property Marketing: Real estate agents use various marketing strategies to showcase properties to potential buyers. From creating attractive listings to leveraging online platforms, they work to maximize exposure and generate interest.

- Property Valuation: Real estate agents have a deep understanding of market trends and property values. They provide clients with accurate valuations to ensure fair pricing during negotiations.

- Client Representation: Real estate agents serve as advocates for their clients. They represent buyers or sellers, safeguarding their interests and negotiating on their behalf to achieve the best possible outcomes.

- Contract Negotiation: One of the most crucial roles of a real estate agent is negotiating contracts. They possess strong negotiation skills and work to secure favorable deals for their clients, whether it’s in terms of price, contingencies, or closing timelines.

Importance of Real Estate Agents in the Market

The presence of real estate agents is vital to the smooth functioning of the housing market. Here’s why they hold such significance:

- Expert Knowledge: Real estate agents have in-depth knowledge of the local market, including property prices, market trends, and neighborhood dynamics. This expertise is invaluable when making informed decisions regarding buying or selling property.

- Navigating Complex Processes: The real estate market involves complex legal, financial, and administrative procedures. Real estate agents ensure clients understand these processes and guide them through each step, reducing the potential for confusion or costly mistakes.

- Access to Networks: Real estate agents have extensive networks of industry professionals, including lenders, appraisers, and inspectors. This network enables them to provide clients with a comprehensive set of resources and services, streamlining the entire real estate experience.

- Time and Efficiency: Buying or selling property can be time-consuming and overwhelming. Real estate agents alleviate the burden by handling various tasks such as property searches, scheduling viewings, and coordinating inspections. Their expertise and efficiency save clients valuable time and effort.

- Negotiation Skills: Successful negotiation is a key attribute of a real estate agent. They possess strong negotiation skills and know the art of finding common ground between buyers and sellers. This ability helps clients achieve their desired outcomes while maintaining the integrity of the transaction.

In conclusion, real estate agents are essential professionals in the housing market. Their roles encompass property marketing, valuation, client representation, and contract negotiation. Their expertise, knowledge, and networks are invaluable assets that simplify the real estate process, ensuring clients make informed decisions and achieve their goals.

Factors Affecting the Average Salary of a Real Estate Agent

Location, Experience and Expertise, Brokerage Firm, Market Demand and Competition

As a real estate agent, your salary potential is influenced by various factors. Understanding these factors can help you make informed decisions about your career and income goals. Let’s explore the key elements that affect the average salary of a real estate agent.

Location

The location in which you work plays a significant role in determining your earning potential as a real estate agent. Real estate markets vary by region and even within cities, with some areas experiencing higher demand and property values than others. For example, agents working in popular metropolitan areas with a thriving housing market may have more opportunities to close high-value transactions and earn higher commissions.

Experience and Expertise

Gaining experience and expertise in the real estate industry can directly impact your earning potential. As you build your knowledge and reputation, you become better equipped to serve clients effectively, negotiate deals, and close sales successfully. Experienced agents often have an extensive network and a track record of successful transactions, which can lead to more referrals and repeat business, ultimately increasing their income.

Brokerage Firm

The brokerage firm you work for also affects your average salary as a real estate agent. Different firms offer varying commission structures, training programs, and support services. Some brokerages may focus on specific market segments, such as luxury properties or commercial real estate, which can impact the average price point of the transactions you handle. It’s important to research and choose a brokerage that aligns with your career goals and offers competitive compensation packages.

Market Demand and Competition

The overall market demand and level of competition in your area can significantly affect your earning potential. In a highly competitive market with limited demand, it may be more challenging to secure clients and close transactions. On the other hand, working in a buoyant market with high demand can lead to more opportunities and potentially higher commissions. Monitoring market trends and adapting your strategies accordingly can help you stay competitive and maximize your income as a real estate agent.

To summarize, the average salary of a real estate agent is influenced by factors such as the location in which you work, your experience and expertise, the brokerage firm you are associated with, and the current market demand and competition. By understanding these factors and strategically navigating the real estate industry, you can position yourself for success and increase your earning potential as a real estate agent.

National Average Salary of Real Estate Agents

Real estate agents play a crucial role in the housing market, assisting buyers and sellers in navigating the complex process of buying or selling properties. If you’re considering a career in real estate or simply curious about the earning potential in this industry, it’s important to understand the national average salary of real estate agents. In this section, we will provide you with a statistical overview, annual salary range, and average salary by state.

Statistical Overview

When it comes to real estate agent salaries, it’s helpful to look at the overall picture. According to recent industry data, the average salary of a real estate agent in the United States is around $50,730 per year. However, it’s important to note that this figure can vary significantly based on factors such as location, experience level, and the current state of the housing market.

Annual Salary Range

The annual salary range for real estate agents can be quite broad, with potential earnings spanning from the lower end to the higher end of the spectrum. On average, entry-level real estate agents can expect to earn around $25,000 to $35,000 per year, while more experienced agents and top performers have the potential to earn well into the six-figure range. It’s worth noting that these figures do not include commission, which is a significant component of many real estate agents’ income.

Average Salary by State

Real estate agent salaries can vary significantly from state to state. Factors such as the cost of living, demand for housing, and the overall state of the economy can all impact earning potential. Here’s a glimpse into the average salaries of real estate agents in a few selected states:

- California: With its booming real estate market, the average salary for real estate agents in California is higher than the national average, ranging from $65,000 to $85,000 per year.

- Texas: In a state known for its affordable housing and thriving economy, real estate agents can expect to earn an average salary of around $45,000 to $60,000 per year.

- New York: As one of the most competitive real estate markets in the country, real estate agent salaries in New York tend to be on the higher end, ranging from $75,000 to $100,000 per year.

It’s important to remember that these figures are averages and can vary depending on individual circumstances. Local market conditions, the agent’s experience and expertise, and their effectiveness in closing deals can all play a significant role in determining actual earnings.

Remember, becoming a successful real estate agent requires not only knowledge and skill but also a strong work ethic and dedication to providing excellent service to clients. While the potential for high earnings exists in this industry, it’s essential to approach it with realistic expectations and a commitment to ongoing professional development.

Additional Income Opportunities for Real Estate Agents

One of the attractive aspects of being a real estate agent is the potential for additional income opportunities. In addition to the base salary, real estate agents have the chance to earn extra commissions, bonuses, incentives, referral fees, and even partnership opportunities. Let’s take a closer look at these income avenues.

Commission Structure

Real estate agents typically operate on a commission-based structure, where they earn a percentage of the property’s sale price as their commission. The commission percentage can vary depending on various factors such as the agent’s experience, the type of property being sold, and the local market conditions.

For instance, residential real estate agents often earn commissions ranging from 2% to 6% of the sale price. Commercial real estate agents, on the other hand, may negotiate commission rates differently, such as a fixed fee or a percentage based on the value of the transaction.

This commission-based structure motivates agents to work diligently, as their income is directly tied to their sales performance. The more properties they sell, the higher their earning potential.

Bonuses and Incentives

In addition to commissions, real estate agents may have the opportunity to earn bonuses and incentives. These rewards are often based on specific achievements or milestones, such as reaching certain sales targets, closing a high-value deal, or bringing in a certain number of new clients.

Bonuses and incentives can take various forms, including cash bonuses, all-expenses-paid trips, or even luxury gifts. They serve as additional motivation for agents to excel in their work and go the extra mile to achieve exceptional results.

Referral Fees

Real estate agents can also earn income through referral fees. When an agent refers a client to another agent or broker, they may receive a percentage of the referred transaction’s commission as a referral fee.

This can be beneficial for real estate agents who have a broad network of contacts and can refer clients to other professionals in their field. It not only provides them with an additional income stream but also strengthens their professional relationships and fosters collaboration within the industry.

Partnerships

Partnering with other professionals can be another lucrative income opportunity for real estate agents. By forming partnerships with mortgage brokers, home inspectors, or property managers, agents can create a referral network where they receive a percentage of the revenue generated by their referred clients.

Partnerships can provide agents with a steady stream of passive income, as they earn a portion of the revenues generated by their partners’ services. It also allows them to offer a more comprehensive range of services to their clients, enhancing their overall value proposition.

In conclusion, being a real estate agent offers various additional income opportunities beyond the base salary. From commissions and bonuses to referral fees and partnerships, these avenues allow agents to earn more as they grow their client base, excel in their sales performance, and build strong professional relationships within the industry.

Strategies to Increase Salary as a Real Estate Agent

In the competitive world of real estate, finding ways to increase your salary is crucial for success. By implementing strategic techniques and focusing on key areas, you can maximize your earning potential as a real estate agent. Here are some effective strategies to consider:

Building a Strong Network

Building a robust network of contacts is essential for a real estate agent looking to boost their salary. Networking allows you to connect with potential clients, industry professionals, and referral sources. Here are a few tips to help you build a strong network:

- Attend industry events, conferences, and seminars to meet like-minded professionals and potential clients.

- Join local business organizations and networking groups to expand your circle of contacts.

- Utilize social media platforms, such as LinkedIn and Facebook, to connect with colleagues, clients, and industry influencers.

- Nurture relationships with past clients and ask for referrals, as word-of-mouth recommendations can be a powerful source of new business.

Expanding the Client Base

Increasing your client base is crucial for growing your income as a real estate agent. By adopting proactive strategies, you can attract more clients and close more deals. Consider the following approaches:

- Develop a strong online presence through a well-designed website and active social media presence. Optimize your online profiles and listings for search engines to attract potential clients.

- Leverage local advertising platforms, such as newspapers, magazines, and online classifieds, to reach a wider audience.

- Offer exceptional customer service to your existing clients, as satisfied clients are more likely to refer you to their friends and family.

- Collaborate with other professionals in related industries, such as mortgage brokers and interior designers, to tap into their networks and gain client referrals.

Continuing Education

Continuing education is vital in a constantly evolving real estate market. Enhancing your knowledge and skills can give you a competitive edge and open up new opportunities for higher earning potential. Consider the following options for ongoing education:

- Take advanced real estate courses and earn certifications to demonstrate your expertise in specialized areas, such as luxury property sales or property management.

- Stay up-to-date with industry trends, market conditions, and legal changes through industry publications, webinars, and conferences.

- Invest time in self-improvement by reading books on negotiation tactics, sales strategies, and personal development.

Specialization

Specializing in a specific niche can lead to increased earnings and a more targeted client base. By becoming an expert in a particular area of real estate, you can differentiate yourself from the competition. Consider the following specialization options:

- Focus on a particular property type, such as residential, commercial, or luxury properties.

- Become an expert in a specific neighborhood or market segment, allowing you to provide valuable insights to clients.

- Develop expertise in a niche field, such as investment properties, vacation rentals, or property flipping.

By implementing these strategies, you can take proactive steps to increase your salary as a real estate agent. Building a strong network, expanding your client base, continuing education, and specialization are key areas to focus on to reach your earning potential in the real estate industry.

Remember, success in real estate requires dedication, hard work, and ongoing effort to stay ahead of the competition.

Conclusion

In conclusion, the average salary of a real estate agent can vary depending on various factors such as location, experience, and market conditions. While it is challenging to determine an exact figure, data from reputable sources suggest that the average annual salary for real estate agents in the United States falls within a range of $40,000 to $60,000. However, it is important to note that top-performing agents who excel in their field have the potential to earn significantly higher incomes. As with any profession, the success and earnings of a real estate agent largely depend on their dedication, skillset, and ability to adapt to market trends. Therefore, those considering a career in real estate should be aware of the potential rewards and challenges that come with the industry.

Find topics in marketing, technology, and social media for realtors, and housing market resources for homeowners. Be sure to subscribe to Digital Age of Real Estate.

Latest posts by RealtyBiz News (see all)

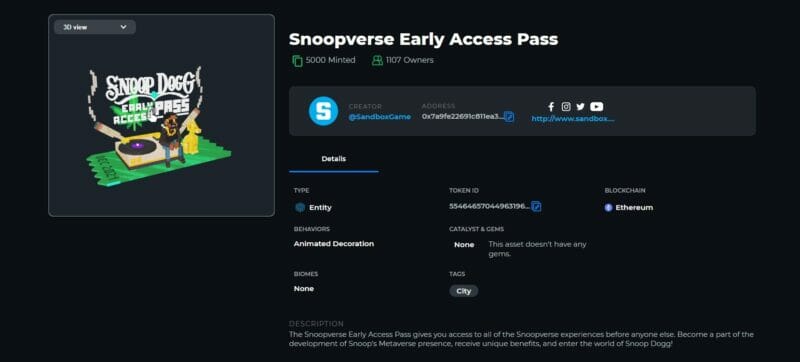

With celebrities like Snoop Dogg purchasing real estate in the metaverse, the demand for LAND on The Sandbox has soared. The famous rapper is selling parcels in “Snoopverse,” a metaverse he established on the platform where he plans to hold virtual events. Parcels of metaverse real estate near other celebrities are attracting premium rates. In fact, someone just paid $450,000 to be Snoop Dogg’s metaverse neighbor.

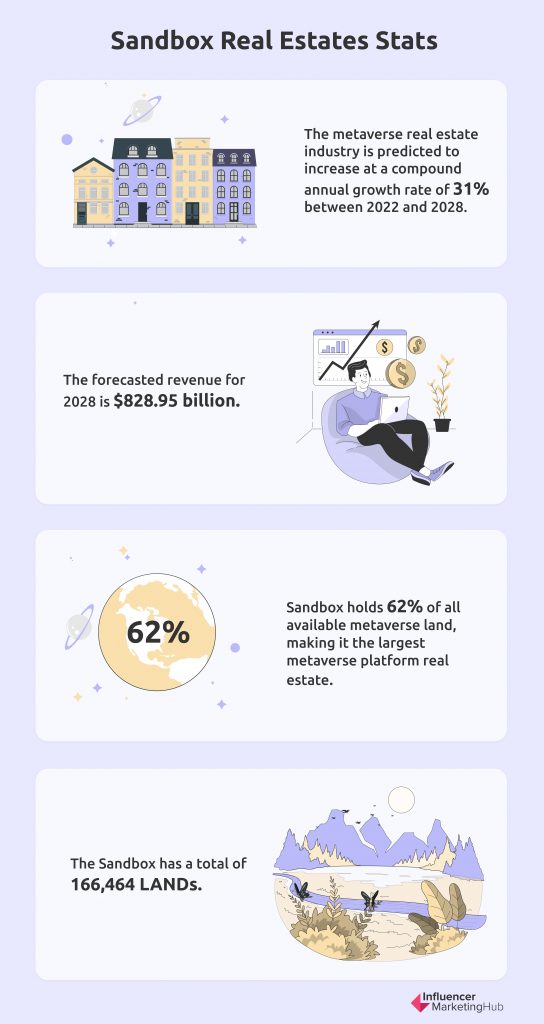

According to a report, the metaverse real estate industry is predicted to increase at a compound annual growth rate of 31% between 2022 and 2028. It will have a revenue of $828.95 billion in 2028. Metaverse real estate sales topped $85 million in January. It’s no surprise that more and more brands, game designers, and content creators are looking into the metaverse to acquire real estate, virtually in this case.

The Sandbox Real Estates: Here’s the Lay of the Land in 2024:

The Sandbox in a Nutshell

What began in 2012 as an online video game has evolved into a metaverse platform nearly a decade later. The Sandbox is a decentralized gaming ecosystem. It’s community-driven, where artists, gamers, and creators can build, trade, and distribute their assets as non-fungible tokens (NFTs). The native asset of the Sandbox virtual economy is an ERC-20 token on the Ethereum network. The Sandbox is well-known for LAND, its virtual real estate. It holds 62% of all available metaverse land, making it the largest metaverse platform real estate. $SAND, which is equivalent to $2.80, is used to purchase a LAND.

The Sandbox’s Real Estate: LANDs

LAND is the basic Sandbox unit. LAND is an ERC-721 token on the Ethereum blockchain. The LAND owner or another player authorized by the owner can terraform and alter the pre-built, preset terrain. A LAND has a width of 96 meters and a length of 96 meters. It’s a perfect square.

The Sandbox has a total of 166,464 LANDs. The public will be able to purchase 123,840 (74%) of the total tokens. The remainder will be offered as rewards to gamers, creators, or partners (16%) or kept by The Sandbox for their use (10%).

LANDs are designed to let users create and publish their own Play to Earn games. You may later monetize the game and earn money on Sandbox. You could also buy the property and rent it out. It is a great way to make passive money.

There are two types of LAND in The Sandbox: regular and premium. Houses are commonly built on regular LANDs, and there are no key partners around them. On the other hand, premium LANDs are bordered by social hubs and major partners.

As a result, premium LANDs get more traffic than regular LANDs. More traffic means more potential revenue from paid games or renting out the LAND to other developers. The increased traffic also implies that more players will see your ads on billboards. You can earn extra cash by renting out billboard space or directing people to your online store.

There are several things you can do with your LAND. You may host and play games, stake and rent the property, organize contests and giveaways, build DISTRICTs, and participate in the metaverse government.

The Sandbox’s Real Estate: ESTATEs

An ESTATE is a group of contiguous LANDs owned by one person. If you own adjacent 1×1 LANDs, you can form an ESTATE. Buyers can also purchase pre-assembled ESTATEs. These groups of LANDs are typically available in the following sizes:

Small: 9 LANDs

Medium: 36 LANDs

Large: 144 LANDs

X-Large: 576 LANDs

By combining a vast number of LANDs, you can form an extensive ESTATE, one that can be worth a fortune and turned into a money-making machine.

The Sandbox’s Real Estate: DISTRICTs

A DISTRICT is a form of ESTATE owned by more than one person. A DISTRICT has specific requirements:

- The LANDs must be next to one other.

- There must be at least two distinct owners.

- Each owner is required to stake a particular amount of SAND.

- The DISTRICT approval is put to a vote.

As a result, DISTRICTs are decentralized autonomous organizations (DAOs). Their nature allows them to attract more foot traffic. Think of a DISTRICT like Times Square in New York. It’s massive and always busy.

How to Buy LANDs

You can buy a LAND during Sandbox’s public property sales. The platform announces the sale beforehand through the platform’s official communities. You may view the available LANDs on Sandbox’s official map during public sales.

Before purchasing a LAND, you must have the following:

Sandbox account: Create an account if you don’t have one yet. You’ll need a crypto wallet like MetaMask or Arkane Crypto Wallet to link your account. Once you’ve installed your crypto wallet, go to the Sandbox login page, click the sign-in button, enter your crypto wallet, email address, and desired user ID, and click “Done.”

SAND and ETH: The Sandbox uses SAND to make purchases and trades. Because SAND runs on Ethereum, ETH is also necessary. You pay transaction fees known as blockchain gas using ETH. Both currencies need a third-party wallet. To make it easier to transact with The Sandbox Marketplace, you can use the wallet you’ve registered on your Sandbox account.

When you have an account and the necessary currencies, you can start purchasing LANDs. The Sandbox provided a walkthrough on buying LANDs. In a nutshell, these are the steps:

Step 1: Open your Sandbox account

Find the “LAND/MAP” button. It’s on the screen’s left toolbar. Click on it.

Step 2: Choose and click the LAND you want to buy

Make sure that the property is available. Regular LANDs available for purchase are gray, whereas premium LANDs on sale are yellow.

Step 3: Click on the buy button when the panel appears

The button is blue, and the panel is on the right corner of the screen. The LAND that you intend to buy will be reserved until the deal is completed, canceled, timed out (inactivity after a couple of hours), or if it failed (usually due to inadequate gas). A booked LAND turns purple.

Step 4: Confirm the deal and specify the amount of gas you want to use

At this point, your cryptocurrency wallet will appear. Enter the necessary data in the correct currency. The transaction will then be in progress. The completion time depends on the gas you spend and any blockchain congestion.

Step 5: Wait for the sale to be confirmed

You will get a notification: “Transaction Succeeded. You Own A LAND.” Another indication of a successful transaction is if the LAND you bought turns red.

Color Map Guide

Gray: Regular LANDs for sale

Yellow: Premium LANDs for sale

Purple: LANDs and ESTATEs booked by you or someone else

Red: LANDs or ESTATEs you own

Green: LANDs or ESTATEs others own

Blue: LANDs or ESTATEs owned by The Sandbox for partners and Game Maker Fund recipients

Buying LANDs Using OpenSea

If you’re unable to buy a LAND directly on The Sandbox, you can use a secondary marketplace that trades a variety of NFTs like OpenSea. To buy LANDs this way, you’ll need both an OpenSea and a Sandbox account. You have the option of choosing a payment method with OpenSea. Depending on the seller’s preference and demand, you can pay in SAND or ETH. It’s best to use the same crypto wallet on both platforms to prevent paying multiple transaction fees.

? 10 ESTATEs & 38 1×1 LANDs are now up for auction!

Head to @opensea and find your very own Mega City home in the #Metaverse!https://t.co/hYHmGIoBfZ pic.twitter.com/ewX4iUWwDH

— The Sandbox (@TheSandboxGame) April 28, 2022

To ensure that you’re buying unique, authentic LANDs on OpenSea or other secondary marketplaces, keep the following points in mind:

- The collection name has a blue verified checkmark next to it.

- The platform’s name should be “The Sandbox,” not just “Sandbox.”

- The coordinates are in the proper format.

- A “Snowflake” symbol should appear, indicating that the Metadata is frozen and the LAND for sale is kept on the decentralized server.

Secondary market LANDs will appear in your inventory on The Sandbox website as long as they are in the same third-party wallet linked to your Sandbox account when you signed up.

How to Sell LANDs

Because the Sandbox supports all forms of trading, it’s only logical that you can also sell your LANDs. You may market your LAND on The Sandbox Marketplace or third-party NFT marketplaces like Rarible and OpenSea. You will be charged a 5% transaction fee in SAND when you sell your LAND on Sandbox. In addition to the trading cost, you will be charged a gas fee if you sell your land through a third-party NFT market.

Different variables influence the price at which you can sell your LAND. For one thing, the pricing is entirely up to you. The value of your LAND will be determined by its location or how close it is to major partners. Another factor to consider is whether there are any ASSETs in the package. You must also include the properties (such as your virtual house) created on your LAND. Its size is also a strong selling point.

To be fair to you and potential buyers, do some in-depth market research before putting out the sale sign.

How to Rent LANDs

Soon, LAND owners will be able to rent out their LANDs in The Sandbox to other creators. When you rent your LAND, you also offer the renter permission to develop something on your property, such as a game. The game creator owns the whole experience that is created on a leased LAND. You have no ownership or control over the experience built on it.

What you can control is the rental price. However, it would be best if you remained competitive to keep content creators motivated to develop and sell their experiences. There are variables to consider when calculating the rental price. On top of the list is the LAND’s location. Nobody will rent your LAND if the price is too high for them to earn a profit. Like selling a LAND, if your property is near major brands or The Sandbox property, then you can have a high rental price.

The Worth of The Sandbox LAND

Whether you’re buying, selling, or renting LANDs, these three factors determine the worth of the real estate.

Location

Like in the real world, the property’s location is essential to its value. Certain areas will be more valuable and sought after than others. This is why some real estate investors typically make offers on properties that appear to be in poor condition but are in excellent locations.

The most coveted locations are typically populated by entities you’d like to be affiliated with, such as major brand territory or The Sandbox zone. These entities will generate more traffic, enhancing the value of the surrounding area.

Size

ESTATEs have four categories: small (3×3), medium (6×6), large (12×12), and XL (24×24). Snoop Dogg and Adidas have large ESTATEs, respectively. Multinational companies, like Ubisoft and Warner Music Group, typically own XL ESTATEs.

In general, the larger the ESTATE is, the higher the price to buy, sell, or rent it. And the bigger the area, the more room there is for development.

Value

The reputation of Sandbox’s collaboration and applicability is well recognized. The Sandbox has worked with some of the world’s most well-known businesses in several fields, including fashion, technology, finance, and gaming. As such, buying LANDs can be a worthy investment. The value of NFT real estate may not be as evident as that of other NFTs, but it has far-reaching effects that go far beyond primary digital assets. This area is still growing, with more to come.

The Rewards of Investing in The Sandbox Real Estate

Owning LANDs on the Sandbox will give you several opportunities to generate a steady source of revenue.

Host life experiences

LAND’s primary function allows owners to host life experiences on their property. You can host games, concerts, scenes, and art museums, to name a few. These experiences can be constructed using Sandbox’s Game Maker and then released on any of the creator’s territories.

Renting

As a LAND owner, you can rent your property to others, such as game designers and content creators, who may have missed the public sale of LANDs. When all The Sandbox’s LANDs have been bought, the demand for renting LANDs will skyrocket.

Staking

In the future, owners will be able to stake cryptocurrency on their properties for passive rewards. This includes GEMs, an ERC-20 token highly coveted by asset designers. Besides the basic staking benefits, LAND owners may exchange these GEMs. The number of LAND areas you own multiplies the SAND-ETH cash flow you give, boosting your SAND cryptocurrency earnings.

Host events and giveaways

Contests and activities may be held on LANDs, drawing many paying customers to your property. You may even charge people to have tournaments or giveaways on your LANDs to promote themselves for a fee.

Self-promotion

If you’re a business owner, content creator, artist, or marketer, you may expand your reach by promoting your brand to gamers by listing some of your ads on your LAND.

Selling ASSETs

If you decide to construct and release an experience on your land, you can add an entry charge to the cost of admission to the experience. For example, you can sell a particular ASSET related to your game, such as purchasing a unique weapon from your NFT gunnery collection.

Selling

Selling your LAND, especially if it’s near major brands, can be very lucrative. However, if you keep your LANDs for a longer period, you will most likely earn more money over time by combining the various strategies outlined above.

Final Thoughts

The metaverse is the future, and any virtual real estate investment is a win. The Sandbox’s LAND has a massive reward-to-risk ratio. There is a high likelihood that LAND prices will rise tremendously in the near future. So, if you have the resources to invest, go ahead and do it. But only after conducting an extensive study on it. Lastly, only invest what you can afford to lose.

Frequently Asked Questions

How Much LAND Is Still Available in The Sandbox?

LANDs are selling quickly. On the secondary market, OpenSea, 31,581 parcels are currently available for purchase. The cheapest parcel costs 1.648 ETH, which is around $4,773. So, if you want to buy a LAND, you still have time.

Are There Any Financial Risks?

The value of a real estate in the metaverse can fluctuate just like it does in the real world. In January 2022, a parcel of LAND was valued $14,099, up from $12,700 the previous month.

There is a financial risk here, as with any investment. So, proceed with caution. The metaverse is still in its early stages and has yet to acquire mainstream popularity. However, given the current trends, a significant drop in the price of metaverse real estate is unlikely. Even if there is, The Sandbox has a lot of potential and traction, so purchasing a LAND is worthwhile.

About the Author

Writer

Geri Mileva, an experienced IP network engineer and distinguished writer at Influencer Marketing Hub, specializes in the realms of the Creator Economy, AI, blockchain, and the Metaverse. Her articles, featured in The Huffington Post, Ravishly, and various other respected newspapers and magazines, offer in-depth analysis and insights into these cutting-edge technology domains. Geri’s technological background enriches her writing, providing a unique perspective that bridges complex technical concepts with accessible, engaging content for diverse audiences.

It’s one down, one to go for J Lo. After getting married last year and setting their sights on a newlywed home to share, Ben Affleck and Jennifer Lopez got to work offloading their separately owned properties. Most recently, the Wall Street Journal reports that Lopez found a buyer for the eight-acre Bel Air, California estate that she listed for $42.5 million in February. The French Country-style mansion ultimately sold for about $34 million—under the initial asking price, but still a very solid profit given the $28 million that the Selena star paid for the 14,000-square-foot home in 2016.

Now, Lopez just needs to sell her Manhattan penthouse, which has been off and on the market for years. That abode, located atop a 1920s Georgian-style building near New York’s Madison Square Park, was most recently listed about a month ago for a touch under $25 million. Affleck sold his East Coast-style Pacific Palisades abode for $28.5 million in October 2022 and in May, the couple spent $61 million on a contemporary Georgian-style estate in Beverly Hills. The sprawling 38,000-square-foot residence boasts a plethora of resort-like amenities, including an indoor sports complex, a hair and nail salon, a home theater, a 155-foot infinity pool, and a 12-car garage.

The buyer of the nine-bedroom Bel Air home that Lopez just sold remains unknown. “My clients fell in love with the land,” agent Lea Porter of the Beverly Hills Estates told the Journal. The plot comes complete with a sandy beach bordering a private lake, a waterfall, a putting green, a 100-seat amphitheater, a fire pit-equipped pagoda, an above-ground pool, two guest cottages, and acres of woodland laced with hiking trails.

A period building on Colmore Row that was once associated with Birmingham’s booming button manufacturing industry has been put up for sale.

MK2 Real Estate is instructed to sell 126 Colmore Row, a multi-let boutique office building, with ground-floor leisure space, on behalf of the vendor, a private property company. Offers are being sought in excess of £2.55 million, reflecting a net initial yield of 8.55 per cent.

Dating back to the early 1900s, 126 Colmore Row was designed by celebrated Birmingham architect Samuel Nathaniel Cooke, who was responsible for designing many of the city’s civic buildings, hospitals, and commercial properties, including, most notably, the original Birmingham Repertory Theatre and the Hall of Memory war memorial in Centenary Square.

Today, following a comprehensive refurbishment, 126 Colmore Row comprises circa

7,000 sq ft of high-quality office accommodation on the first to fifth floors and 2,653 sq ft of leisure space on the ground floor and basement, let to Jamaican restaurant Jamaya.

Mark Rooke, a director in MK2’s property investment team, said: “It’s not often that buildings on Colmore Row, Birmingham’s most prestigious address, come up for sale and especially not ones with such a rich history and heritage as 126 Colmore Row.

“Not only does the building offer bags of character, for savvy investors it provides significant asset management and leasing opportunities, with a number of floors still available to let.”

Nestled in the heart of New England, New Hampshire boasts a rich tapestry of history, nature, and culture. From the dense forests of the White Mountains to the serene beaches lining its modest coastline, the Granite State has long been a haven for those seeking a blend of urban sophistication and rural tranquility. Yet, like any place, New Hampshire is not without its complexities.

In this Redfin article, we delve into the ten pros and cons of living in New Hampshire, shedding light on both its idyllic charm and the challenges that come with calling it home. So whether you’re searching for homes for sale in Manchester or an apartment in Concord, read on to learn more about The Granite State.

Pros of living in New Hampshire

1. No sales or income taxes