Mega projects in the region and property development in the hospitality industry are driving demand for experienced professionals in the UAE’s property and construction sector, according to recruitment specialists.

The most sought-after professionals are those with experience in the design and planning stages of a project through to delivery, the Hays 2023 GCC Salary Guide says.

“Certain areas were busier than others – real estate development in the hospitality industry maintained a steady pace throughout the year,” says Aaron Fletcher, senior manager of construction, property and engineering at Hays.

“Additionally, design consultancies were busy recruiting staff to meet project demand in Saudi Arabia and the UAE.”

About a quarter (24 per cent) of construction, property and engineering professionals in the UAE changed roles in 2022, compared with 23 per cent who started a new job in 2021, Hays reports.

The jobs market in the UAE, the second-largest Arab economy, has made a strong recovery from the coronavirus-induced slowdown on the back of the government’s fiscal measures.

The majority of companies in the Emirates plan to hire new employees for the remainder of the year and wages are expected to increase by just under 2 per cent in 2023, according to the Cooper Fitch Salary Guide 2023.

More than half of all companies (57 per cent) expect to increase salaries this year, according to the Cooper Fitch survey, which polled business leaders at 300 companies in the GCC.

With hiring on the increase in the UAE’s property and construction sector, what are the most sought-after jobs and how much do they pay?

Read on to find out – and check out our comprehensive UAE salary guide 2023 slide show below for a snapshot of your sector.

Which property jobs are in demand?

As with previous years, construction delivery roles, including project/construction directors and senior managers, will be required in 2023, according to the Hays salary guide.

Much of this demand will come from the flagship big projects in Saudi Arabia – such as Red Sea Global, Neom, the Diriyah Gate Development Authority and Roshn – that have progressed further in their construction stages, the consultancy estimates.

“For new giga-projects at the design and planning stages, architectural designers and urban planners will be required,” it says.

“Additionally, due to a talent shortage, development directors/managers and candidates who have experience implementing digital technology, especially building information management, will be highly sought-after.”

Recruiter Michael Page says in its 2023 UAE Salary Guide that positions in demand in the UAE’s property and construction sector include project directors and development, real estate asset, leasing, and property and facilities managers.

What job skills are employers looking for?

Experience in managing projects from inception through to handover is desirable, according to Hays.

Employers look for stability and a proven track record of end-to-end project management, the recruiter says.

Equally, as projects evolve, progress and sometimes change direction, a flexible attitude towards work is essential. Employers are increasingly seeking out candidates with a “start-up mentality” that are willing to go above and beyond to deliver, Hays says.

Meanwhile, Michael Page cites real estate consultancy, development and real estate asset management as sought-after roles in the UAE.

Some of the stats behind the UAE’s hiring boom

“There is a shortage of talent across the GCC for the major real estate consultancies and Big Four organisations offering real estate advisory services such as valuations, development advisory, transaction advisory and more,” it says.

“Major projects have been announced across the region and these companies are busier than ever.”

Organisations are also expanding their project portfolios across the GCC as they looking for new project opportunities to add to their portfolios.

Therefore, development professionals with extensive experience in the initial phases of development such as market research, feasibility and business development are in high demand, Michael Page explains.

“Organisations are also looking to enhance their real estate portfolios. Announcements from key players in the sector with plans to expand portfolios, refurbish or convert assets to meet the market demands has been a common theme,” it says.

“Property and asset management specialists are in demand to support plans to enhance or reposition current portfolios and offer strategic advice to future projects.”

Are salaries expected to rise in the property sector?

Professionals within the property and construction sector feel positive about their pay for this year, with 73 per cent expecting their salary to increase, Hays finds.

Equally, 76 per cent of employers expect rates of pay within their organisation to increase.

However, with employers in the GCC increasingly offering more sustainable salaries and, instead, opting to sell themselves as an employer of choice, the average expected salary increase is 5 per cent or less, according to Hays.

“Employees with high-level responsibilities and strong individual performance are most likely to have their pay increase request approved,” the recruiter says.

Design consultancies are busy recruiting staff to meet project demand in Saudi Arabia and the UAE

Aaron Fletcher, senior manager of construction, property and engineering at Hays

What other benefits can employees expect?

Retaining talent has become a top priority in the property and construction sector and organisations are addressing this with consistent promotions, clear lines of career development, full bonus payouts and competitive salaries, according to Michael Page.

“It is a great opportunity for international candidates with these skill sets considering a move to the GCC,” it says.

Developers, property consultancies and construction specialists have been recruiting in large volumes, making the market extremely competitive for employers in terms of securing and retaining top talent, the consultancy says.

“Salaries have increased, benefits are becoming more versatile and people now desire flexible working, such as work-from-home policies,” it says.

“Some employers are meeting the markets’ demands; however, many are still operating like pre-Covid times.”

When budgets are limited, organisations must look at their incentives and the candidate motivations, Michael Page recommends.

In a market where candidates’ priorities have changed and family and wellness have become the priority, organisations must learn to accommodate this to remain competitive, the consultancy says.

Aside from the salary and benefits package, the availability of career development opportunities and work-life balance (including flexible working options) are the most important factors for employees when considering a new role, Hays reports.

Employers that want to retain staff should focus on upskilling and reskilling their existing workforce by providing ongoing professional development, it suggests.

What are the highest-paying jobs in the property and construction sector?

Development and design

Chief development officer: Dh126,000 ($34,300) to Dh252,000 a month

Executive director of development: Dh84,000 to Dh158,000

Executive director of design: Dh76,000 to Dh122,000

Director of development: Dh53,000 to Dh90,000

Director of design: Dh53,000 to Dh90,000

Director of urban planning: Dh53,000 to Dh90,000

Senior development manager: Dh41,000 to Dh69,000

Senior design manager: Dh38,000 to Dh64,000

Senior urban planning manager: Dh37,000 to 61,000

Design manager: Dh26,000 to Dh47,000

Development manager: Dh26,000 to Dh47,000

Urban planning manager: Dh26,000 to Dh42,000

Construction and project management

Chief projects officer: Dh102,000 to Dh214,000

Executive director of project delivery: Dh73,000 to Dh125,000

Director of infrastructure: Dh61,000 to Dh88,000

Commercial director: Dh61,000 to Dh87,000

Director of project controls: Dh60,000 to Dh79,000

Director of construction: Dh53,000 to Dh73,000

Project director: Dh53,000 to Dh73,000

Senior project manager: Dh37,000 to Dh53,000

Senior commercial manager: Dh36,000 to Dh53,000

Senior manager of project controls: Dh36,000 to 52,000

Project manager: Dh21,000 to Dh37,000

Construction manager: Dh21,000 to Dh37,000

Commercial manager: Dh20,000 to Dh36,000

Project controls manager: Dh20,000 to Dh35,000

Sales and post construction

Executive director of sales: Dh78,000 to Dh115,000

Executive director of asset management: Dh78,000 to Dh105,000

Executive director of facilities management: Dh61,000 to Dh97,000

Director of asset management: Dh63,000 to Dh84,000

Director of sales: Dh58,000 to Dh78,000

Director of leasing: Dh47,000 to Dh73,000

Senior asset manager: Dh53,000 to Dh68,000

Director of facilities: Dh37,000 to Dh58,000

Asset manager: Dh26,000 to Dh42,000

Property manager: Dh21,000 to Dh42,000

Facilities manager: Dh21,000 to 42,000

Leasing manager: Dh21,000 to Dh37,000

Sales manager: Dh21,000 to Dh37,000

Real estate consultant

Surveyor: Dh18,000 to Dh28,000

Consultant – advisory: Dh18,000 to Dh28,000

Manager – valuations/advisory: Dh30,000 to Dh35,000

Contracting

Project /commercial director: Dh60,000 to Dh80,000

Project /commercial manager: Dh35,000 to Dh55,000

Civil engineer: Dh15,000 to Dh25,000

Architect: Dh15,000 to Dh30,000

Source: Cooper Fitch and Michael Page

Updated: August 01, 2023, 6:09 AM

How To Sell A House With A Mortgage

Before you can sell a house with a mortgage, there are certain requirements you must meet. First, your mortgage is a legal obligation, so you must satisfy it if you sell the house. In other words, you can’t sell the house and not pay off the mortgage. You must clear up any liens on the property before you sell.

If you’re selling a home with a mortgage, there are specific steps you must take in a specific order to ensure you satisfy your legal obligations.

Let’s take a closer look at the steps and the order you’ll need to take them in.

1. Get A Payoff Quote

The first step to selling a house with a mortgage is to get a payoff quote. This will tell you how much you must pay your lender to satisfy your mortgage agreement and release the lien.

If you’re moving to a new mortgage lender, they’ll likely request the payoff quote for you. However, you can contact your current loan servicer and ask for a payoff quote if they don’t. Some lenders even have automated phone or online systems that make getting a quote even easier.

Your payoff quote will include not only your mortgage balance, but also any applicable fees or mortgage insurance balances, and the date when the quote expires. If you aren’t sure of your closing date, make sure to add a few buffer days into your request. This will help avoid any per diem interest charges if you go past the deadline for your payoff quote so you don’t underpay.

2. Determine Home Equity

You’ll want to know how much home equity you have. It could help you when you buy your next home or otherwise invest the money from your home sale. Some homeowners invest the entire amount of their current home equity in their new home. Others invest some of the profit but keep the rest liquid.

What you do depends on what mortgage you qualify for and how much money you have saved for your down payment.

Home Investment Equity

Home investment equity is the equity you’ve gained in the home caused by an increase in the market value. For example, say you bought your home for $150,000, and now it’s worth $250,000. So, you earned $100,000 in equity in the home just by the house appreciating. You didn’t necessarily have to do anything to earn this equity.

Earned Equity

Earned equity is the equity you invest in the home yourself like the money you pay upfront for your down payment. So, for example, if you put 20% down on a $150,000 home, you have $30,000 in instant equity.

You also increase your equity each month as you make principal payments toward the loan. That means every time you make your monthly mortgage payments, you’re actually increasing your home equity. This lowers how much you owe and increases the difference between the home’s value and your mortgage balance.

Paying any windfalls or large amounts of money you earn toward your mortgage also increases your earned equity. Every dollar you pay toward the home’s principal increases your equity.

3. Market And Sell Your Home

Once you know what you owe, it’s time to put your house on the market. You’ll need to price your home to make sure your asking price can cover your loan balance. A REALTORⓇ or real estate agent will know the local market and can help you price your home competitively.

They can help you set an asking price and ensure you get the best offers on your home. Hopefully, this will help you repay your mortgage balance and fees – and also make a profit.

4. Repay Your Mortgage Lender

Once you know how much you owe and your home sale has gone through, you’ll need to pay off your mortgage lender. Your primary mortgage lender has the first lien position on your home and therefore gets paid first. Make sure you have an accurate payoff quote and follow up to satisfy the debt.

If there are remaining days of unpaid interest, make sure you pay them as quickly as possible to pay your loan off in full.

5. Pay Off Additional Loans, Second Mortgages And Liens

If your home has any other liens, you must also pay them off. Liens stay with the home, not the person. This means if you didn’t clear any outstanding liens on the property, the buyer might not be able to close on the home. In addition, mortgage lenders require a clear title which isn’t possible with outstanding liens.

Common loans and liens you might have on your property include:

Keep in mind that loans like home equity loans and HELOCs are considered second mortgages. Any loan that is secured by your home adds a lien to your property that will need to be paid when you sell your house.

You’ll want to make sure to ask for documentation once each loan or lien is paid in case you need to provide proof of payment in the future.

6. Cover Fees And Closing Costs

You’ll likely have transaction fees and closing costs if you sell a house with a mortgage or without one. While you won’t pay as many closing costs as the buyer, you can expect to cover expenses including real estate agent’s commission, title policy fee, and, in some cases, prorated property taxes. The funds can come directly from the proceeds of the sale if you’re receiving enough to cover your mortgage amount, liens and closing costs.

7. Keep Remaining Funds

Once you pay off all liens on the home, including the first mortgage, any second mortgages or HELOCs, and any other outstanding liens, the remaining funds go to you, the seller. If you choose to reinvest the funds in your next home, it’s a great way to start homeownership with equity by making a large down payment. Making a down payment of 20% or more can help you avoid private mortgage insurance (PMI) and build home equity.

After all your transactions are completed, you’ll receive either a wire or check for the remaining amount. Once the money is yours you can use it any way you like, as an emergency fund, renovating your new home or even saving towards retirement.

ATLANTA, July 25, 2023 /PRNewswire/ — North Highland, the leading change and transformation consultancy, has been named a top consulting firm in the UK by Consultancy.uk. The firm received a variety of platinum, gold and silver rankings in 17 service and industry-based categories.

Consultancy.uk compiled the ranked list based on research conducted in various areas, including capability assessments, industry recognition, reputation, analyst benchmarks, thought leadership, as well as survey insights from executives, consultants, clients and graduates.

North Highland received the following recognitions:

- Platinum: Process Management & Project Management

- Gold: Change Management, Data Science, Digital, Human Resources, Management, Supply Chain, Banking, Financial Services, Healthcare, Hospitality & Travel, Pharma & Life Sciences, Retail and Transport & Logistics

- Silver: Outsourcing & Shared Services

“Being named a Top Consulting Firm is a direct testament to our ability to deliver transformation services across geographies and industries,” said Anthony Shaw, managing director and EMEA business leader. “We strive to deliver the utmost client satisfaction, and to do so, we operate as one internationally connected firm with about a third of our business in the UK. This is all possible due to the growth and efforts taking place amongst our UK team.”

To review this year’s list of Top Consulting Firms in the UK, grouped by expertise, visit https://www.consultancy.uk/rankings/2023.

About North Highland

North Highland makes change happen, helping businesses transform by placing people at the heart of every decision. It’s how lasting progress is made. With our blend of workforce, customer, and operational expertise, we’re recognized as the world’s leading transformation consultancy. We break new ground today, so tomorrow is easier to navigate. Founded in 1992, North Highland is regularly named one of the best places to work. We are a proud member of Cordence Worldwide, a global network of truly connected consultancy firms with the ability to think and deliver together. This means North Highland has more than 3,500 experts in 50+ offices around the globe on hand to partner with you.

For more information, visit www.northhighland.com or connect with us on LinkedIn, Twitter, Instagram, and Facebook.

Media contact:

Courtney James

Director PR

(+1) 404-850-2806

[email protected]

SOURCE North Highland

Interestingly, if he makes this election in the future, he can elect to treat the condo as his principal residence for up to four years before he moved into it, which may wipe out all but one year of taxation divided by the total years you all own the property.

Does an owner pay capital gains tax for moving into a rental property?

It depends on the steps taken. Liljana, I think your son can make a 45(3) election in the future. Although you and your husband could as well, it may lead to more tax later on your home. You might need to pay some capital gains tax now on the condo’s change in use to personal use. You might also need to pay more tax later on the subsequent appreciation as well from the time your son moved into it to the time you transfer it to him or sell it, or upon the second death of you and your husband. This appreciation will also be taxable, assuming you want to preserve your principal residence exemption for your house.

You’re 2 minutes away from getting the best mortgage rates in CanadaAnswer a few quick questions to get a personalized rate quote*You will be leaving MoneySense. Just close the tab to return.

You can claim a property that your child lives in as your principal residence if it is legally or beneficially yours. But this has tax implications for your own home.

Ask MoneySense

I bought a condo in 2006 in another province for my daughter to live in. It’s registered in my name. I also have a house in another province. I am planning to sell the condo my daughter lives in very soon. Can I claim capital gain exemption in the condo she lived in all these years?

—Bill

Capital gains tax when selling a home your child lives in

Canadian taxpayers may be eligible to claim the principal residence exemption when they sell real estate. Since 2016, real estate transactions have been under more scrutiny with the Canada Revenue Agency (CRA) since taxpayers now need to report all sales on their tax returns, even if the sale is of a tax-free principal residence.

The definition of principal residence for tax purposes

According to the CRA, in order for a property to qualify as a principal residence, it must be:

- A housing unit, which can include a house, a condo, a cottage, a mobile home, a trailer, a houseboat, a leasehold interest in a housing unit, or a share of the capital stock of a co-operative housing corporation;

- Owned by the taxpayer, jointly or otherwise, legally or beneficially;

- Ordinarily inhabited in the year by the taxpayer, their spouse or common-law partner, their former spouse or former common-law partner, or child.

There can be nuances in the principal residence guidelines that may impact your ability to qualify for the exemption. Some examples are if your home was rented out or used for business purposes, if the acreage is significant, or if you owned another property during the same years that you owned the property in question and claimed the principal residence exemption for it.

Legal versus beneficial ownership of a property

An important nuance for you, Bill, is whether your daughter beneficially owned the property. If she did—meaning you were on title, but it was technically hers—she may be able to claim the principal residence exemption herself. This could be the case if she paid all of the ongoing expenses, amongst other criteria. But then the question may be where did the down payment come from, and if the property was in fact beneficially your daughter’s, but legally in your name, why did the two of you not put it in her name in the first place?

Tax Implications Of Selling A House In A Trust

Before we get deeply into the implications of selling a house in a trust, it’s worth noting the different types of taxes that come into play.

- Capital gains tax: Capital gains taxes are paid on profits from the sale of assets, including homes. It’s worth noting that there is an exemption on taxes for a certain amount of profit if you meet the qualifications. This could come into play if a living grantor is selling out of a revocable trust.

- Estate taxes: Estate taxes are paid out of the accounts of the deceased. If the heirs decided to sell the family home, the profits would go into the estate, which would also be responsible for the taxes.

- Inheritance tax: Some states charge what’s referred to as an inheritance tax. Instead of or in addition to taxes being paid by the estate, the individual or group inheriting the property pays a tax on the value.

- Stepped-up basis: Stepped-up basis is a tax advantage you can sometimes allow yourself after inheriting property. The idea is that when you sell the property after taking a step up in basis, the value of that property is based on what it was worth when you inherited it rather than what it was worth when the person you inherited from bought the property. This can decrease your tax liability.

While there are all these tax items to think about, who pays the taxes and when can depend on how the trust is set up. Let’s run through a couple scenarios.

If the home is in a revocable trust when sold, tax liability is pretty easy. When selling a home that’s within a trust, the grantor (seller) is taxed on the capital gains (profits) they make on the house sold. The theory here is that because the trust was revocable, the grantor never relinquished the asset and would owe the tax liability.

On the other hand, what happens if the trust is already being paid out based on either the passing of the grantor or the appropriate amount of time passing under the terms of the trust? Who is taxed on the sale of the home? The answer to this can depend upon how the trust is set up.

If the documentation underlying the trust permits the trustee to reinvest the profits from the sale of any assets back into the principal and they choose to do so, the tax on that capital gain is charged to the trust itself. Income tax on estates and trusts is reported on Form 1041.

On the other hand, if the trustee is regularly passing all gains to the beneficiary, the beneficiary gets taxed on those gains. If you’re unsure how the tax should be handled in your situation, be sure to speak to an estate planning attorney and/or tax professional. With that, let’s dig in a little deeper on each of the tax considerations listed earlier.

Capital Gains Tax

The basics of capital gains tax are easy to explain, but the application is a little more complicated. At its most basic level, capital gains tax works like this:

If you bought a home for $500,000 and sold that later for $700,000, you would owe capital gains tax on your $200,000 profit. The tax rate you can expect to pay will vary based on how long you held the property as well as your income.

However, there’s an exemption for those who have used a property as their primary residence and owned it for 2 out of the last 5 years. Although you have to own the home and live in it as your main residence, those can be separate 2-year periods. The amount of the exclusion can be up to $250,000 filing as an individual or $500,000 if married filing jointly.

Estate Tax

As mentioned above, when the proceeds of the sale of a home after the grantor’s death are reinvested in the trust rather than being passed through as income, the estate pays the tax. It’s worth noting that the threshold rates for the different capital gains tax brackets are different for estates and trusts than they are for individuals.

The capital gains tax is still paid, but it’s out of the proceeds of the trust so that beneficiaries don’t have to deal with it.

Inheritance Tax

Some states charge an inheritance tax. This may be along with or instead of an estate tax. Whereas an estate tax is charged against the remaining assets of the deceased, an inheritance tax is charged to the heirs or beneficiaries. Tax rates and exemptions vary quite a bit from state to state. Consult a tax advisor regarding your situation.

Stepped-Up Basis Tax Rules

When you inherit property, it’s generally eligible for a step up in basis. This means that if your parents bought a property for $150,000 and it was worth $300,000 when you inherited it, the capital gains taxes you paid when you sold the property would be based on the $300,000 value at the time of the passing rather than when they bought the property.

However, when you inherit it as part of a trust, it depends on whether the trust was revocable or irrevocable at the time of the person’s passing. If it was revocable, there is a step up in basis because they retained control and could’ve pulled that out of the trust at any time.

If the property was transferred to an irrevocable trust prior to death, there’s no step up in basis because it’s not part of the estate for tax purposes. This is true even though the grantor is responsible for the taxes on the property until it’s passed to the beneficiary under the terms of the trust, even if that only happens after the death of the grantor.

Try to picture the top-selling real estate agent in the world. Are you thinking of a New Yorker in a skyscraper who has befriended a bunch of investment bankers? Perhaps a shady Londoner steering oligarchs to multimillion-dollar mansions? Whoever you’re imagining, it’s probably not someone like Ben Caballero. Little about Caballero’s aesthetic screams world-class: The...

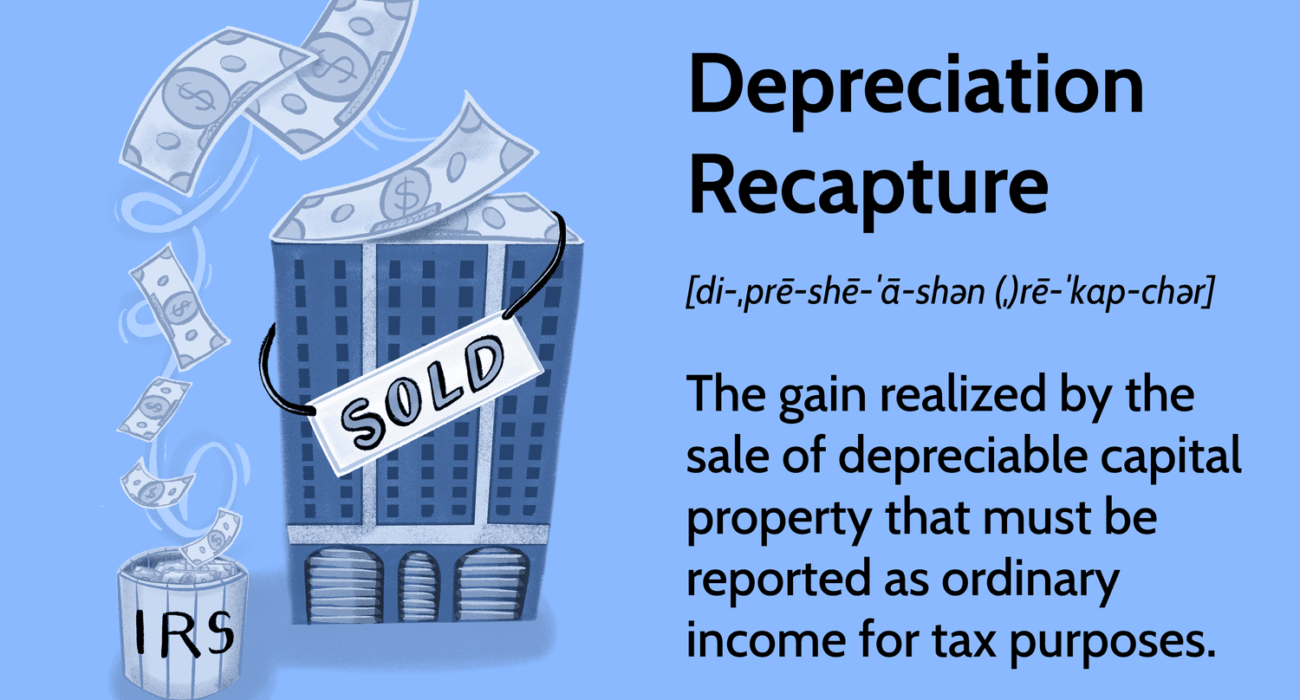

What Is Depreciation Recapture?

Depreciation recapture is the gain realized by the sale of depreciable capital property that must be reported as ordinary income for tax purposes. Depreciation recapture is assessed when the sale price of an asset exceeds the tax basis or adjusted cost basis. The difference between these figures is thus “recaptured” by reporting it as ordinary income.

Depreciation recapture is reported on Internal Revenue Service (IRS) Form 4797.

Key Takeaways

- Depreciation recapture is a tax provision that allows the IRS to collect taxes on any profitable sale of an asset that the taxpayer had used to previously offset taxable income.

- Depreciation recapture on non-real estate property is taxed at the taxpayer’s ordinary income tax rate, rather than the more favorable capital gains tax rate.

- Depreciation recaptures on gains specific to real estate property are capped at a maximum of 25%.

- To calculate the amount of depreciation recapture, the adjusted cost basis of the asset must be compared to the sale price of the asset.

Understanding Depreciation Recapture

Companies account for wear and tear on property, plant, and equipment through depreciation. Depreciation divides the cost associated with the use of an asset over a number of years. The IRS publishes specific depreciation schedules for different classes of assets. The schedules tell a taxpayer what percentage of an asset’s value may be deducted each year and the number of years for which the deductions may be taken.

For tax purposes, annual depreciation expense lowers the ordinary income that a company or individual pays each year and reduces the adjusted cost basis of the asset. If the depreciated asset is disposed of or sold for a gain, the ordinary income tax rate will be applied to the amount of the depreciation expense previously taken on the asset.

Depreciation recapture is a tax provision that allows the IRS to collect taxes on any profitable sale of an asset that the taxpayer had used to previously offset their taxable income. Since depreciation of an asset can be used to deduct ordinary income, any gain from the disposal of the asset must be reported and taxed as ordinary income, rather than the more favorable capital gains tax rate.

Depreciable capital assets held by a business for over a year are considered to be Section 1231 property, as defined in Section 1231 of the IRS Code. Section 1231 is an umbrella for both Section 1245 property and Section 1250 property. Section 1245 refers to capital property that is not a building or structural component. Section 1250 refers to real estate property, such as buildings and land. The tax rate for the depreciation recapture will depend on whether an asset is a section 1245 or 1250 asset.

Examples of Depreciation Recapture

Section 1245 Depreciation Recapture

The first step in evaluating depreciation recapture is to determine the cost basis of the asset. The original cost basis is the price that was paid to acquire the asset. The adjusted cost basis is the original cost basis minus any allowed or allowable depreciation expense incurred. For example, if business equipment was purchased for $10,000 and had a depreciation expense of $2,000 per year, its adjusted cost basis after four years would be $10,000 – ($2,000 x 4) = $2,000.

For income tax purposes, the depreciation would be recaptured if the equipment is sold for a gain. If the equipment is sold for $3,000, the business would have a taxable gain of $3,000 – $2,000 = $1,000. It is easy to think that a loss occurred from the sale since the asset was purchased for $10,000 and sold for only $3,000. However, gains and losses are realized from the adjusted cost basis, not the original cost basis. The reasoning for this method is that the taxpayer has benefited from lower ordinary income over the previous years due to annual depreciation expenses.

Gains and losses are realized from the adjusted cost basis, not the original cost basis.

The realized gain from an asset sale must be compared with the accumulated depreciation. The smaller of the two figures is considered to be the depreciation recapture. In our example above, since the realized gain on the sale of the equipment is $1,000, and accumulated depreciation taken through year four is $8,000, the depreciation recapture is thus $1,000. This recaptured amount will be treated as ordinary income when taxes are filed for the year.

Instead, assume the equipment in the example above was sold for $12,000. In that case, the entire accumulated depreciation of $8,000 is treated as ordinary income for depreciation recapture purposes. The additional $2,000 is treated as a capital gain, and it is taxed at the favorable capital gains rate. There is no depreciation to recapture if a loss was realized on the sale of a depreciated asset.

Unrecaptured Section 1250 Gain

Depreciation recapture on real estate property is not taxed at the ordinary income rate as long as straight-line depreciation was used over the life of the property. Any accelerated depreciation previously taken is still taxed at the ordinary income tax rate during recapture. However, this is a rare occurrence because the IRS has mandated all post-1986 real estate be depreciated using the straight-line method.

Part of the gain beyond the original cost basis is taxed as a capital gain and qualifies for the favorable tax rate on long-term gains, but the part that is related to depreciation is taxed at the unrecaptured gains section 1250 tax rate specific only to gains on real estate property. The unrecaptured section 1250 tax rate is currently capped at 25%.

For example, consider a rental property that was purchased for $275,000 and has an annual depreciation of $10,000 ($275,000 / 27.5 years allowed by IRS for rental property). After 11 years, the owner decides to sell the property for $430,000. The adjusted cost basis then is $275,000 – ($10,000 x 11) = $165,000. The realized gain on the sale will be $430,000 – $165,000 = $265,000. The unrecaptured section 1250 gain can be calculated as $10,000 x 11 = $110,000, and the capital gain on the property is $265,000 – ($10,000 x 11) = $155,000.

Let’s assume a 15% capital gains tax and that the owner falls in the 32% income tax bracket. Unrecaptured section 1250 gains are limited to 25%. The total amount of tax that the taxpayer will owe on the sale of this rental property is (0.15 x $155,000) + (0.25 x $110,000) = $23,250 + $27,500 = $50,750. The depreciation recapture amount is, thus, $27,500.

How Do You Calculate Depreciation Recapture?

Depreciation recapture is calculated by subtracting the adjusted cost basis from the sale price of the asset. The adjusted cost basis is the original price paid to acquire the asset minus any allowed or allowable depreciation expense incurred. If, for example, the adjusted cost basis is $2,000 and the asset is sold for $3,000, there is a gain of $1,000 to be taxed. The rate it will be taxed depends on the taxpayer’s income tax rate and whether the asset is real estate.

How Is Depreciation Recapture Treated?

Depreciation recapture is treated as ordinary income and taxed as such. With real estate, it’s a little more complicated. The gain beyond the original cost basis is taxed as a capital gain, whereas the part that is related to depreciation is taxed at the unrecaptured gains section 1250 tax rate, which is capped at 25%.

How Can I Avoid Depreciation Recapture?

Depreciation recapture can be quite costly when selling something like real estate. Other than selling the property for less, which isn’t a favorable option, ways around it could include using the IRS Section 121 exclusion or passing the property to your heirs. If you find yourself in this position, speak to an expert before acting.

The Bottom Line

Depreciation recapture offers the IRS a way to collect taxes on the profitable sale of an asset that a taxpayer used to offset taxable income. While owning the asset, the taxpayer is permitted each year to expense its declining value to reduce the amount of income tax owed. However, if that asset is later sold, the IRS may be able to claw some of that money back.

Depreciation recapture is calculated by subtracting the adjusted cost basis, which is the price paid for the asset minus any allowed or allowable depreciation expense incurred, from the sale price. It only applies when an asset is sold for more than its adjusted cost basis and is taxed differently depending on the type of asset. Depreciation recapture on non-real estate property is taxed at the taxpayer’s ordinary income tax rate. Depreciation recapture on gains specific to real estate property, on the other hand, is capped at a maximum of 25%.

Apartment blocks and office buildings in Ho Chi Minh City’s eastern area. Photo by VnExpress/Quynh Tran

While the secondary market for apartments in Ho Chi Minh City has been in free fall for a year now, primary market prices only began to decline last quarter.

Property consultancy CBRE Vietnam said in a report that the average price in the primary market dropped to below VND60 million per square meter, down 4.8% from the first quarter.

This is the first decline in the last five years, according to the report.

Some high-end projects in the city’s east are trying to sell apartments at VND35-65 million per square meter as against VND50-75 million in previous months.

According to property consultancy DKRA Group, the primary market declined due to promotions, incentives and gifts offered by developers in May and June, but the number of transactions was down to a 10th from a year earlier.

Two projects in Binh Tan and Binh Chanh in HCMC have recently cut prices from previous rounds of sales.

They are also offering to pay 8% interest on bank loans for buyers for 18-24 months.

Meanwhile, the secondary market continued to decrease, with the average price falling by 4% from the first quarter and 5% for the year.

In the luxury and high-end segments, mainly in Thu Duc City, prices are down 20-30% for the year.

Colliers Vietnam said the apartment market remained quiet in the first half of the year.

David Jackson, its CEO, said not many affordable apartment projects were launched in HCMC during the period, and their prices remained “too high” for low-income earners.

In the secondary market, many people sold out at lower prices to cut their losses, he said.

Duong Thuy Dung, executive director of CBRE Vietnam, expected banks to reduce loan interest rates in the second half.

There could be positive signals in the market in the final months of the year with the speeding up of public spending and efforts to remove legal obstacles plaguing the real estate market, she added.

According to a calculation made by the idealista research office, Italy’s leading real estate portal, the purchase price of a house is equivalent to an average of 11.9 years’ rent in Italy. The number of rentals required to buy a home is one of the indicators that can most help to assess whether one market may be more attractive than another to rent or buy a home.

It is purely indicative and does not pretend to solve the perennial dilemma of what is more convenient between renting and buying, as a number of factors affect this choice, such as individual preferences, time expectations, fixed mortgage costs and taxes.

That being said, a comparison of purchase prices and rental costs shows that the more rental annuities are needed to pay for the house, the more attractive it will be for the tenant to settle in it without buying. On the contrary: the lower the ratio between the average sale price per square metre and the average monthly rental per square metre, the more attractive it will be to buy.

If many years of rent are required to purchase, it means sales prices are high compared to rental prices; and vice versa – if few years are required, sales prices are low compared to rental prices.

The index must be assessed on a case-by-case basis, as each city presents a different scenario.

When comparing sale and rent prices, we see that the highest index is in the city of Sienna, with 22.8 years, followed by Cuneo (21.9 years), Trento (21.7) and Venice (21.2), while in Matera it is 20.6 years. All the other main towns require less than 20 years of rent to buy a house, but in almost all of them, they exceed the national average of 11.9 years. Only five cities rank below this threshold: Brindisi (11.6 years), Rovigo (11.2) Trapani (10.8), Syracuse (10.5), Biella (9.8).

In large cities such as Milan, the purchase price is the equivalent of 18.8 years of rent, while in Rome and Naples it is 17.8 and 17.3 respectively.

Washington, D.C. – Today the Consumer Federation of America (CFA) is releasing a new report – “A Surfeit of Real Estate Agents: Industry and Consumer Impacts” – that uses industry sources to document the costs to industry and to consumers of too many residential real estate agents. More than 1.5 million residential agents (including brokers) compete for home sales usually totaling 5 to 6 million annually.

Those costs include:

- economic inefficiencies including an inordinate time spent by agents finding clients,

- relatively low incomes of many full-time agents,

- frustration by these agents and by many consumers who must deal with inexperienced agents,

- reinforcement of relatively high and uniform commission rates, and

- damage to the reputation of the industry.

“A large majority of practicing real estate agents have recently received their license or work part-time,” said Stephen Brobeck, a senior fellow at CFA. “These agents usually charge the same commission rates as experienced, full-time agents yet in general offer worse service and deprive experienced agents of needed clients.”

In examining home sales in three cities– Jacksonville (FL), Minneapolis (MN), and Albuquerque (NM) — the study found that marginal agents (with five or fewer sales a year) received an estimated 25-30 percent of commission income. According to data collected by the industry from Realtors in 2021:

- the median net income of all sales agents was $25,000,

- the median net income of sales agents with less than two years experience was $7,800, and,

- the median net income of all brokers and associate brokers was $57,100.

The report documents complaints by many experienced, full-time agents of the incompetence and/or inattention of other agents that also harm consumers. And it emphasizes that because of the “surfeit of agents,” real estate agents and brokers feel financial and/or peer pressure to keep commission rates relatively high.

“Without 5-6 percent rates, even fewer agents would survive financially in today’s marketplace,” said Brobeck. “Ironically, relatively high rates attract new entrants into the industry, increasing competition for clients and reducing individual income for all.”

The report raises the question of whether the industry should make greater efforts to ensure the competence and commitment of new agents. Such efforts could include more stringent entry requirements and required mentoring of new agents. A future CFA report will address in depth these two issues.