The Federal Reserve has once again hit the pause button in its war on inflation. After raising rates 11 times in 2022 and 2023, the central bank has been standing pat. Following the Fed’s March 20 meeting, its second of 2024, Chairman Jerome Powell held steady again, announcing no change in interest rates for the time being.

The Federal Reserve and the housing market

Earlier in the inflationary cycle, the Fed had enacted increases of as much as three-quarters of a point. Now that inflation is down to 3.2 percent — not too far off from its official target of 2 percent — that round of tightening appears to be over. Housing economists are now looking to when the anticipated rate cuts will begin.

“Additional rate hikes no longer appear to be part of the conversation — it is all about the pace of cuts from here,” says Mike Fratantoni, chief economist at the Mortgage Bankers Association. “This is good news for the housing and mortgage markets. We expect that this path for monetary policy should support further declines in mortgage rates, just in time for the spring housing market.”

In an effort to rein in inflation, the Fed boosted interest rates aggressively in 2022 and 2023, including a single jump of three-quarters of a percentage point. The hikes aimed to cool an economy that was on fire after rebounding from the coronavirus recession of 2020. That dramatic recovery has included a red-hot housing market characterized by record-high home prices and microscopic levels of inventory.

However, for months now the housing market has shown signs of cooling. Home sales have dropped sharply, and appreciation slowed nationally. Home prices are not driven solely by interest rates but by a complicated mix of factors — so it’s hard to predict exactly how the Fed’s efforts will affect the housing market.

Higher rates are challenging for both homebuyers, who have to cope with steeper monthly payments, and sellers, who experience less demand and lower offers for their homes. After hitting 8 percent last fall, mortgage rates have dipped back down a bit. As of March 20, the average 30-year rate stood at 7.07 percent, according to Bankrate’s national survey of lenders — certainly a welcome turnaround.

How the Fed affects mortgage rates

The Federal Reserve does not set mortgage rates, and the central bank’s decisions don’t move mortgages as directly as they do other products, such as savings accounts and CD rates. Instead, mortgage rates tend to move in lockstep with 10-year Treasury yields.

A slowing economy and an easing of inflation pressures are the prerequisites for lower mortgage rates.

— Greg McBride, Bankrate Chief Financial Analyst

“Mortgage rates don’t take direct cues from the Fed and will instead respond to the outlook for the economy and inflation,” says Bankrate chief financial analyst Greg McBride. “A slowing economy and an easing of inflation pressures are the prerequisites for lower mortgage rates.”

Still, the Fed’s policies set the overall tone for mortgage rates. Lenders and investors closely watch the central bank, and the mortgage market’s attempts to interpret the Fed’s actions affect how much you pay for your home loan. The Fed bumped rates seven times in 2022, a year that saw mortgage rates jump from 3.4 percent in January all the way to 7.12 percent in October. “Such increases diminish purchase affordability, making it even harder for lower-income and first-time buyers to purchase a home,” says Clare Losey, an economist at the Austin Board of Realtors in Texas.

What will happen to the housing market if interest rates rise?

There’s no doubt that record-low mortgage rates helped fuel the housing boom of 2020 and 2021. Some think it was the single most important factor in pushing the residential real estate market into overdrive.

When mortgage rates surged higher than they had been in two decades, the housing market slowed dramatically. And now, while sales volume remains slow, prices are volatile: Home prices declined for seven straight months through January 2023, then rose for nine straight months before finally starting to tick back down again in November, according to the Case-Shiller U.S. National Home Price NSA Index. They’re now rising again: the nationwide median existing-home price for January, normally a very slow month for real estate, was $379,100, according to the National Association of Realtors — up more than 5 percent year-over-year and surprisingly close to NAR’s all-time-high median price of $413,800.

Yet, in the long term, home prices and home sales tend to be resilient to rising mortgage rates, housing economists say. That’s because individual life events that prompt a home purchase — the birth of a child, marriage, a job change — don’t always correspond conveniently with mortgage rate cycles.

History bears this out. In the 1980s, mortgage rates soared as high as 18 percent, yet Americans still bought homes. In the 1990s, rates of 8 percent to 9 percent were common, and Americans continued snapping up homes. During the housing bubble of 2004 to 2007, mortgage rates were high, yet prices soared.

So the current slowdown may be more of an overheated market’s return to normalcy rather than the signal of an incipient housing crash. “The combination of elevated mortgage rates and steep home-price growth over the past few years has greatly reduced affordability,” Fratantoni says.

But if mortgage rates keep pulling back, affordability will become less of a factor. For instance, borrowing $320,000 at the mid-March rate of 6.84 percent translates to a monthly principal-and-interest payment of $2,094, according to Bankrate’s mortgage calculator. Borrowing the same amount at 8 percent translates to a monthly payment of $2,348. That’s a difference of more than $250 per month, or just over $3,000 a year.

A continued decline in mortgage rates could create a new challenge, though: It will likely draw new buyers into the market, a surge that could further intensify the ongoing shortage of homes for sale.

Next steps for borrowers

Here are some pro tips for dealing with elevated mortgage rates:

- Shop around for a mortgage. Savvy shopping can help you find a better-than-average rate. With the refinance boom considerably slowed, lenders are eager for your business. “Conducting an online search can save thousands of dollars by finding lenders offering a lower rate and more competitive fees,” McBride says.

- Be cautious about ARMs. Adjustable-rate mortgages may look tempting, but McBride says borrowers should steer clear. “Don’t fall into the trap of using an adjustable-rate mortgage as a crutch of affordability,” he says. “There is little in the way of up-front savings, an average of just one-half percentage point for the first five years, but the risk of higher rates in future years looms large. New adjustable mortgage products are structured to change every six months rather than every 12 months, which had previously been the norm.”

- Consider a home equity loan or HELOC. While mortgage refinancing is on the wane, many homeowners are turning to home equity lines of credit (HELOCs) to tap into their home equity. The rationale is simple: If you need $50,000 for a kitchen renovation and you have a mortgage for $300,000 at 3 percent, you probably don’t want to take out a new loan at 7 percent. Better to keep the 3 percent rate on the mortgage and take a HELOC — even if it costs 10 percent.

You finally own your home free and clear. And now, you want to put that ownership stake to use. Is this even possible?

Fortunately, the answer is yes. You can take equity out of your home even after your mortgage is paid off. One of the easier ways to do so is to sell your home, but there are also financial products that allow you to extract equity from your paid-off home quickly without having to pick up and move.

Each has its pluses and minuses. So let’s look at the options.

Can you take equity out of a paid-off house?

“It is definitely possible to take equity out of your home after you’ve paid off a previous mortgage,” says Jeffrey Brown, branch manager with Axia Home Loans in Bellevue, Wash. “Assuming you qualify, you can access that equity at any time.”

Actually, those means of access are pretty much the same for a paid-off house as for one that still has a mortgage on it. You can take equity out of your home using one of these tools:

- home equity loan

- home equity line of credit (HELOC)

- reverse mortgage

- cash-out refinance

- shared equity investment

When should you tap equity on a paid-off house?

Why would anyone pursue fresh financing after finally paying off a mortgage? Well, why not? Your home is an asset, and you can make it work for you. And when you own it free and clear, its tappable potential is at its greatest (see Pros, below).

Viable reasons abound for borrowing against your ownership stake, from funding a major home improvement project to investing in a business to purchasing more property. Or, frankly, for whatever you need. However, since your home will serve as the collateral for the debt, you should be judicious in how you tap it. Two good rules to follow: Use your equity in ways that improve your finances or work as an investment and don’t take out more than you can afford to lose.

How to get equity out of a paid-off house

Cash-out refinance on a paid-off home

Let’s say you were still paying off your mortgage, had adequate equity and needed cash. You’d likely do a cash-out refinance, which typically has a relatively lower interest rate compared to other types of loans.

You can do the same now, even though you’ve paid off your mortgage. You’ll simply take out a new mortgage and pocket the equity in the form of cash at closing. As with any refinance, however, you’ll be on the hook for closing costs, which can run 2 percent to 5 percent of the amount you’re borrowing and any escrow payments.

“A cash-out refinance generally results in the lowest interest rate and offers the highest loan amounts you can borrow,” says Matt Hackett, operations manager for Equity Now, a mortgage lender headquartered in Mamaroneck, New York. “It can be a fixed- or adjustable-rate loan, and it is fairly straightforward to apply and qualify for.”

Home equity loan on a paid-off home

Alternatively, you could apply for a house-paid-off home equity loan.

Like a cash-out refinance, a home equity loan is secured by your property (the collateral for the loan) and enables you to extract a large amount of equity because you have no other debt attached to the residence. You’ll also likely need to pay closing costs, and as with any mortgage, you risk losing your home if you can’t pay it back.

The upsides: Home equity loans typically come with fixed interest rates, which are usually much lower than personal loan rates. Plus, if you use the money on home improvements, you can deduct the interest on your taxes.

HELOC on a paid-off home

Many homeowners like the flexibility of a home equity line of credit (HELOC), which works more like a credit card you can use when you need it.

“HELOCs come with adjustable interest rates, often based on the prime rate,” says Hackett. “They offer the opportunity to draw funds and pay back funds during the initial draw period, which is more flexible than a standard first mortgage.”

What’s more, you’re only responsible for repaying the amount you use versus the fixed obligation of a cash-out refinance or home equity loan, says Vikram Gupta, executive vice president and head of home equity for PNC Bank.

Do read the fine print of your agreement, though. “Additionally, some HELOCs may have various fees associated with them such as annual fees, early closure fees, and origination fees, so borrowers should pay close attention to these when evaluating their total financing costs,” says Gupta.

On the downside: HELOCs aren’t as easily attainable — you need a strong credit score — and, given their fluctuating interest rates, can mean variable monthly repayments.

Reverse mortgage on a paid-off home

If you’re 62 or older, you could be eligible for a reverse mortgage. This financing vehicle gets you regular payments from a mortgage lender in exchange for your home’s equity.

“A reverse mortgage can be a great way for seniors to access the equity in their homes to pay for monthly living expenses and keep them living independently, especially if they don’t have monthly income in retirement,” says Brown.

Reverse mortgages have pros and cons, though. You’ll still need to keep up with homeowners insurance, property tax and HOA dues payments to avoid foreclosure, and there’s a limit to how much money you can get. You can’t let the home fall into disrepair either — you’ll still be responsible for maintenance.

Most of all: “It’s important for the borrower’s survivors to understand that the entire [reverse mortgage] balance, plus interest and fees, is due if the borrower passes away,” says Gupta. “The borrower’s house may need to be sold if their estate cannot repay the reverse mortgage loan.”

Shared equity agreement on a paid-off home

With a shared equity agreement — a relatively new method of liquidating equity — you’ll sell a portion of your future home equity in exchange for a one-time cash payment.

“The details on how this works and what it costs will vary from investor to investor,” says Andrew Latham, CFP, CPFC, content director and managing editor for SuperMoney.com. “Let’s say you have a property worth $600,000 with $200,000 in equity built up. A home equity investor might offer you $100,000 for a 25 percent share in the appreciation of your home.”

If your home’s value increases to $1 million after 10 years — the typical term for a home equity investment — you’d have to return the $100,000 investment plus 25 percent of the appreciation, which in this case would be $100,000. You’d also need to return the investment plus the share of appreciation if you sell the home.

“The advantage here is that you can tap into your home’s equity without getting into debt,” says Latham, “and there are no monthly payments, which is a great plus for homeowners struggling with cash flow.”

In effect, you’ll have a silent partner in your home, so you’ll need to be comfortable with that and the rights that partner has to protect their investment.

Pros of tapping equity on a paid-off house

Easier to get approved

On the plus side, it can be relatively easy to qualify for a home equity loan on a paid-off house since you already have a solid track record of paying off your first mortgage, which likely means you’re older and have good credit and possibly a higher income. This ups your creditworthiness as a borrower, making you a preferred candidate to lenders and lowering the interest rate you’ll pay.

You also won’t have to worry about the size of your ownership stake or loan-to-value ratio — two other criteria that lenders look at, and that affect how much you’re able to borrow.

No-strings money

Furthermore, you can use your equity for any reason. Most lenders won’t care, for instance, if the money will be put toward funding retirement, seeding a new business or making a down payment on an investment property.

“Many seek to pay for their children’s educational expenses, fund their retirement or pay for an unexpected medical emergency like cancer care for a loved one,” says Kelly McCann, an attorney specializing in construction and real estate with Burnside Law Group in Portland, Ore.

Avoid capital gains taxes

In addition to being able to use the money for nearly any purpose and being more likely to qualify, tapping into your home equity also has the potential to save you money on your income tax.

“It may be smarter to tap into your equity than selling your home and downsizing,” says McCann. “If you have capital gains on your home of more than $250,000 (or more than $500,000 if you are a married couple) you must pay taxes on that gain after the sale of your home. However, if you borrow against your home by, for example, taking out a home equity loan, you don’t have to pay taxes on the loan proceeds — you get the money tax-free.”

Cons of tapping equity on a paid-off house

Risk of losing your home

Of course, if you choose a form of financing wherein your home is used as collateral, like a cash-out refinance or home equity loan, there’s always the risk that you could lose your home if you can’t repay.

Upfront expenses

While they often carry lower interest rates than unsecured loans, home equity products aren’t free. Most have upfront expenses and many of those good old closing costs that you remember all-too-well from your first mortgage. You’ll have to come up with the funds to pay for expenses like origination fees and a home appraisal, to name a few. The whole process could be paperwork-heavy and time-consuming, too.

Being frivolous with funds

You’ve got a tempting chunk of change there in your home. But you’ve worked long and hard to acquire this asset, so don’t blow it on one-time, discretionary expenses. Buying a car (a depreciating asset), paying for a wedding or taking a vacation — these are not-so-good reasons to deplete your equity stake.

How much equity am I able to cash out of my home if it’s fully paid off?

Even if your home mortgage has been paid in full, which means you have 100 percent equity, you cannot borrow all of that money. Generally, lenders allow for borrowing up to 80 to 85 percent of a home’s appraised value. That means if your home is worth $500,000 you may be able to access as much as $425,000 of that equity. However, the specific limit also varies by lender.

Bottom line on getting equity out of a paid-off home

Determining whether it makes sense to pull equity out of a house you’ve already paid off really comes down to your unique circumstances and financial picture, as well as your short- and long-term goals. It’s also important to consider whether you’d be able to make the payments on the loan if your financial circumstances were to change unexpectedly.

“Homeowners should ask themselves: ‘What is the purpose of the funds needed?’ They also need to assess their individual financial situations to ensure they have the cash flow to pay off the loan in the future, particularly as they approach retirement,” says Gupta.

If you decide to proceed, make sure to practice the due diligence you would apply to any other financial transaction—shop around with several lenders and find the best terms for your needs.

FAQs

-

A home equity line of credit, or HELOC, is typically the most inexpensive way to tap into your home’s equity. When opening a HELOC, you only pay interest on the money you actually use. As an added bonus, when using a HELOC, you won’t pay all the closing costs that come with a home equity loan or a cash-out refinance on a paid off home.

-

Lenders typically look for credit scores of at least 620 on home equity loan applications. You’ll qualify for an even better rate with a score of 700 or above.

Key takeaways

- While your home’s value is determined by many factors, some home improvements could help increase its worth.

- There are multiple ways to pay for upgrades, including cash-out refinancing, a home equity loan or home improvement loan.

- If you plan to sell your home, it’s important to determine not just how much improvements will cost, but how much of that cost you’ll recoup.

8 ways to increase the value of your home

The value of your home can increase or decrease due to any number of factors, including variables out of your control like conditions in your local housing market. Still, you can try to up your home’s value with strategic upgrades. Here are some ideas:

1. Clean and declutter

To help boost the value of your home, begin by decreasing the amount of stuff that’s inside it. Cleaning and decluttering are relatively inexpensive tasks, even in bigger homes. Professionally cleaning a four-bedroom home averages between $200 and $225, according to HomeAdvisor.

Of course, you could save money by doing the work yourself. Start by going through cabinets and closets and making donation piles. Then clean out drawers and other storage areas, making sure you’re not keeping anything you don’t need or want.

2. Add usable square footage

Homes are valued and priced by the livable square feet they contain, and the more livable square feet, the better, says Benjamin Ross, a Realtor and real estate investor based in Corpus Christi, Texas.

Adding a bathroom, a great room or another needed space to a home can increase function and add value. A separate in-law suite can also be a smart idea.“Most homes do not have this feature,” says Ross, “so adding one sets you apart from the competition when it is time to sell.”

The cost of an addition varies, but typically ranges from about $22,200 to $81,800, according to HomeAdvisor, with an average cost of $50,305.

3. Make your home more energy-efficient

Projects that lower utility bills can increase the value of your home. Installing a smart thermostat, for example, helps improve efficiency and save money, says Scott Ewald, director, Brand and Content marketing at Trane, an HVAC company.

“The right smart thermostat will allow a homeowner to control their home’s climate from anywhere, giving them the power to manage energy costs regardless of whether they are sitting on the couch or away on vacation,” says Ewald. “Such investments in home tech — particularly when connected to the HVAC, which is the largest mechanical system in the home — provides a strong selling point and highlights the home’s overall comfort, functionality, energy efficiency and convenience.”

It can cost between $175 to $1,000 to make this quick upgrade, according to HomeAdvisor, or an average of about $350.

Other ways to improve your home’s efficiency and value include replacing old, leaky windows, installing energy-efficient home appliances and adding insulation to your home.

4. Spruce it up with fresh paint

A fresh coat of paint can make even dated exteriors and interiors look fresh and new.

Begin by repainting any rooms with an “odd” color scheme, says Timothy Wiedman, a former professor and personal finance expert who has flipped homes over his career. For example, did you let your then-11-year-old daughter paint her bedroom hot pink 16 years ago? If so, that’s a good place to start.

The cost of an interior painting project ranges between roughly $970 and $3,000, with a national average of $1,988, according to HomeAdvisor. Your exact painting budget will depend on room size. HomeAdvisor pegs painting a bathroom — usually the smallest room in the house — somewhere between $150 and $300, while a 330-square-foot living room might cost as much as $2,000.

An exterior paint job, on the other hand, will cost much more, with prices ranging from $1,810 to $4,505 (the national average is just over $3,000).

If you just want to repaint a door or a single room, doing it yourself could cost you between $200 and $300. For bigger jobs, though — especially exterior ones — hiring a painter might be worth it, given that professionals can buy paint at wholesale prices, know what sort of finishes to use and are more adept at scaling ladders.

5. Work on your curb appeal

From power washing your driveway to mowing the lawn, improving curb appeal can make a big difference in your home’s value.

Upgrading your landscape can go an especially long way, says Joe Raboine, vice president of Design at Oldcastle APG, a manufacturer of exterior building products. Some ideas: a fresh walkway, shrubs, planters, mulching or even a new patio or outdoor kitchen.

6. Upgrade your exterior doors

Also in the vein of curb appeal, replacing an old front door can work wonders, says Wiedman. In the late ’90s, he and his wife replaced an old, ugly door with a solid mahogany door with a frosted, oval piece of lead glass. He stained the door himself to save money, and the result was “simply stunning.”

Don’t forget the garage doors, too, says Randy Oliver, president of Hollywood-Crawford Door Company. At a 102 percent return on investment, you’ll get back more than you spend, according to Remodeling.

“The front of the home is the first thing you, your neighbors and prospective buyers will see,” says Oliver. “Garage doors often take up the most amount of space on the front of your home, so installing a modern glass panel door or a rustic wood door will dramatically improve your home’s appearance.”

7. Give your kitchen an updated look

Many buyers zero in on the kitchen as the central feature of a home, so if yours is outdated, it can ultimately affect how much you garner from a sale. Likewise, if you aren’t able to utilize your kitchen fully due to layout, space or other concerns, you won’t be maximizing the space.

This project, though, will require a lot of money, and you likely won’t get every dollar you invest back. The average complete kitchen renovation costs around $80,000, and a homeowner would likely get around $60,000 of value when it’s time to sell, according to the National Association of Realtors. Midrange or modest upgrades actually offer a better ROI than the most elaborate ones.

If updating your entire kitchen is too big of an undertaking, a minor remodel could still have an impact on your home’s value — think coordinating appliances and installing modern hardware on your cabinets. Talk with a real estate agent about what makes the most sense and what will command the most dollars from prospective buyers.

8. Stage your home

If you’re planning to list your home for sale, consider skipping cosmetic home improvements and go with a home staging service instead.

Staging costs about $1,800 on average, according to HomeAdvisor, but the cost varies based on your needs and home. Staging services range widely, from decluttering and depersonalization (for example, removing family photos or specific decor) to bringing in rented furnishings and repainting. Simply put, the more work involved to stage it, the more expensive the production will be. A real estate agent can help you determine which staging services would make the most impact on your home’s value.

Reasons to increase your home value

Your home is likely one of your largest assets, so increasing its value contributes to your overall net worth. Raising your home’s value has other benefits, as well, such as:

- Aesthetics and function: From reclaiming storage space for a bedroom to installing more modern tile in the bathroom, cosmetic upgrades can not only up the enjoyment and use factors, but also add value to your home.

- More profit when you sell: Whenever you decide to sell, a higher home value could translate to bigger upside.

- More tappable home equity: If you need cash, you can leverage your home’s equity — more so the more your home is worth.

- Some protection from market swings: If your home has a higher value, you might be able to guard against major dips in the housing market.

- No more mortgage insurance: If you’re paying mortgage insurance premiums, having your home reappraised at a higher value could eliminate that cost.

Home improvement statistics

- The top three projects on homeowners’ minds in 2024: routine maintenance, interior painting and installing new appliances, according to Angi.

- Homeowners spent an average of $13,667 on home improvements in 2023, according to Angi.

- Twenty-five percent of Americans have delayed home improvements and renovations due to the current state of the economy, according to a Bankrate survey.

How to pay for home improvements to increase value

Personal loan

Personal loans allow you to borrow a fixed amount at a fixed interest rate. These loans are unsecured, meaning you don’t have to put your home or other property up as collateral. Many personal loan lenders allow you to borrow as much as $35,000 for home improvements — sometimes more, depending on your credit and other factors.

Home equity loan or HELOC

Home equity loans are similar to personal loans in that you receive a lump sum of cash at a fixed interest rate and fixed monthly payment. Home equity lines of credit, or HELOCs, work like credit cards and come with variable rates.

These borrowing options require you to put your home up as collateral to qualify. No matter which option you go with, the interest might be deductible if you use the money to make eligible home improvements.

0% APR credit card

If you need to borrow a small amount of cash for your home improvement plans, you might be able to skip the loan and go with a 0% APR credit card instead. Many cards have no interest payments on balances for up to 18 months, which can be ideal if you have a smaller-scale project in mind. A credit card can also work well if you’re able to pay your contractor with it.

Just remember: If you don’t pay your balance off by the time your zero-percent APR offer ends, your card’s interest rate will reset to a higher variable rate, costing you more.

Cash-out refinance

If you have substantial equity in your home and want to do a major renovation, a cash-out refinance could provide you with the funds you need, albeit with a new loan at a potentially higher rate. The refinancing process is just as paperwork-heavy as taking out a mortgage, too, and you’ll need to pay closing costs.

FAQ

-

Different renovations can have varying degrees of impact on your home’s value. Replacing your garage door, for example, might not add as much value as replacing all of the windows with more energy-efficient panes.

-

There are financing options that allow you to buy a home and pay for renovation expenses at the same time. For example, the Fannie Mae HomeStyle loan bundles the money you need to buy a new property and the money you need for renovations into one loan. The maximum you can borrow is 75 percent of the as-completed value of the home after the renovation. FHA 203(k) loans are also designed to cover renovations when buying a home, although there are some additional limitations with this route: A 203(k) loan can’t cover luxury add-ons like a swimming pool or outdoor fireplace.

-

You can make some major upgrades to your home with a $100,000 budget. For example, you might be able to convert your attic into living space or add a standard bathroom, mudroom or sunroom. No matter what you decide to do to your home, you can stretch that $100,000 further by focusing on more affordable materials – think standard materials and finishes instead of custom choices.

-

Establish your goals. For example, is the renovation so you can enjoy the home for the foreseeable future, or are you aiming to increase the value and sell it in hopes of turning a profit? Then, create an outline of everything you want to accomplish, and get quotes from multiple contractors for the cost and timeline. You don’t have to go with the cheapest option; go with the one that is most reputable. Before you go too far down the path to starting the project, make a plan for what you’re going to do during the renovation. Will you be able to live there during the construction, or do your plans call for gutting the home? If you need to relocate for part of the project, it’s important to figure out how to minimize those short-term living costs.

Real estate commissions have survived the rise of the Internet and decades of attacks from disruption-minded discounters. But a flood of legal challenges to the existing brokerage model poses a new threat to the status quo.

An industry-shaking lawsuit making its way through the federal court system could upend the long-established way of paying commissions — namely, the custom of home sellers footing the bill for both their own agent and their buyer’s. This typically totals 5 to 6 percent of the home’s sale price, taking away a hefty chunk of the seller’s proceeds. In October 2023, a federal jury in Missouri found that the National Association of Realtors (NAR), along with several large brokerages, conspired to inflate Realtors’ commissions.

How might real estate commissions change?

It’s unclear exactly how or when that verdict will affect commissions, but the case’s price tag alone — $1.8 billion in damages, with the potential of billions more — is roiling the industry. Some predict big changes: One possibility is that home sellers will no longer pay both the listing agent and the buyer’s agent, so homebuyers who want representation might have to pay their own agents separately.

“The Missouri verdict and other court cases may lead to a revolution in our industry, not just reform,” Glenn Kelman, CEO of brokerage firm Redfin, told investors in a recent earnings call.

“The bulwark is falling apart,” said Brad Case, a housing economist at Middleburg Communities who has also worked for mortgage giant Fannie Mae and the Federal Reserve. “The Realtors have held this situation together for 100 years, but it’s not tenable for the long term.”

Some see the federal verdict as a sign that the real estate industry finally will have to give in to pressures for discounts. Others say it will be years before the verdict will translate to savings for homebuyers or sellers. Stephen Brobeck, senior fellow at the Consumer Federation of America, expects commissions will ultimately fall below 4 percent, maybe even to 3 percent. But he doesn’t see that happening anytime soon.

“Any change is going to happen slowly,” Brobeck said. “The old guard is going to try to keep the old rates.”

How much do commissions cost?

If a homeowner sells a property for $400,000, about average for existing homes in the United States, a 5 percent commission amounts to $20,000. That amount is then split between the seller’s own agent and their buyer’s agent (which hardly matters to the seller, who still has to pay the full amount regardless).

Long ago, 6 percent was the going rate for real estate commissions; 3 percent to each agent. But after decades of competition and regulatory scrutiny, the typical commission now is slightly less than 5 percent, according to data from Anywhere Real Estate, the parent of Coldwell Banker, Century 21 and other large real estate brands. In its filings with securities regulators, publicly traded Anywhere reports that its average commission “side” — half the commission — is currently about 2.4 percent.

While commissions briefly rose during the Great Recession and again in 2023, rates in general have been falling steadily for decades. For Realtors, this decline in commission rates has been offset by rising home prices: They’re getting a smaller piece of the pie in terms of their percentage-based fee, but the pie is getting bigger.

About the NAR lawsuit

In the case that went to trial in 2023, Missouri home sellers alleged antitrust violations by NAR and four major brokerages: Keller Williams, Anywhere, RE/MAX and HomeServices of America. Anywhere and RE/MAX settled before trial — paying $83.5 million and $55 million in damages, respectively — while the other defendants opted to take their chances in the courtroom.

The jury ruled against the industry, and a judge ordered NAR and the two remaining brokerage firms to pay $1.8 billion in damages to home sellers. That figure could eventually balloon to $5 billion.

Keller Williams has since settled as well, for $70 million, while NAR and the remaining defendant are appealing. But if the verdict stands, it could mean that a home seller would no longer be required to pay the agent who represents their buyer.

Keep in mind:

If the verdict stands, home sellers might no longer be required to pay the agents who represents their buyers.

The success of the Missouri suit, filed on behalf of hundreds of thousands of home sellers in that state, has spawned similar legal complaints in Texas, Florida, Pennsylvania and elsewhere. However, it could be years before those suits are settled and the fallout comes into focus.

Other dramas

NAR is also facing other headwinds in addition to the antitrust lawsuit and related cases. A sexual harassment scandal led to the resignation of the organization’s then-president in 2023, and the organization’s next president and longtime CEO have since stepped down as well.

All the drama has created unease and unrest in the ranks. Redfin cut ties with the trade group, requiring many of its brokers and agents to cancel their memberships, and other brokerages have followed suit. In addition, two influential real estate agents have announced the launch of a competing trade group, known as the American Real Estate Association (AREA).

One of the new group’s cofounders, Jason Haber — a broker/agent at Compass in New York City and an outspoken NAR critic — described AREA as an alternative, not a replacement. “We’re not trying to replace NAR. We’re not trying to replicate NAR,” he said. “They have a 108-year head start.”

A ‘perfectly competitive’ industry?

The residential real estate industry long has presented a dichotomy. On the one hand, it has essentially controlled the marketing of properties for sale through a nationwide network of multiple listing services (MLSs). That reality has led to grumblings about collusion and price-fixing, along with scrutiny from the U.S. Department of Justice.

On the other hand, real estate sales is a relatively easy business to get into, as evidenced by NAR’s membership rolls of more than 1.5 million agents. To earn a real estate license, an agent typically needs to take a couple of classes and pass a state exam. No college degree is required, and the costs of entry are modest.

Lawrence Yun, NAR’s chief economist, points to these low barriers to entry as evidence that competition is alive and well: “Real estate is a perfectly competitive industry,” Yun said during the organization’s annual conference in November.

Brobeck, the consumer advocate, disagrees with that assessment. “It’s not a free market right now,” he said. “There’s intense competition for clients. But there’s no competition on rates. In a normal marketplace, you compete based on marketing, but also on the price you charge.”

Meanwhile, the industry mantra long has held that commissions are negotiable, suggesting that sellers and buyers call the shots when it comes to how much they pay agents. In practice, though, consumers buy or sell a home only once every 5 to 10 years, and many aren’t knowledgeable enough about the process to successfully negotiate the rate down.

“Consumers are at a disadvantage,” Brobeck said. “They buy and sell homes infrequently, and they’re mostly concerned about sale price and timing.”

Historically, discounters have not succeeded

For decades, detractors have predicted the demise of real estate commissions. These fees were sure to go the way of stockbrokerage commissions and travel agency fees, the naysayers said. Instead, real estate commissions have proven stubbornly resilient.

It’s not for a lack of trying. Many disruptors have seen commissions as a problem to be solved, but most have fallen short of reshaping the industry.

In the early 2000s, for instance, a splashy discounter known as YourHomeDirect (and later Foxtons) offered 2 percent commissions in New York and New Jersey. But after advertising heavily and gaining market share, it ultimately collapsed.

A decade later, London-based Purplebricks pushed into the U.S., wooing sellers with a flat fee of $3,200. It, too, overestimated demand and pulled out of the U.S. market in 2019.

One high-profile discounter, Seattle-based Redfin, has achieved greater staying power. It launched as a cheaper alternative to traditional brokers and touted listing fees of just 1 percent, although it has since shifted to focusing on 1.5 percent listing fees.

How home sellers can save on commission

If you’re not keen on paying 5 or 6 percent of your home’s sale price, here are some alternative options:

- Go it alone: Sell your home without an agent in a “for sale by owner” transaction. Between July 2022 and June 2023, 7 percent of home sales were sold by owners without the help of an agent, according to NAR data. But selling without professional help is a lot of work to do on your own, and it only saves you one agent’s commission — you’ll still have to pay your buyer’s agent.

- Negotiate: If you don’t want to go it alone, ask agents about their commission rates upfront and compare the terms of each person you talk to. If you think the fee is too high, see if they’re willing to lower it. If both agents in the transaction are from the same brokerage, you might have more leverage to negotiate.

- Hire a discount agent: A low-commission real estate agent will likely charge much less than a traditional agent would — usually 1 to 1.5 percent of your home’s sale price. (However, you might not receive the personalized attention you would with a traditional Realtor.) There are also brokerages and agents who work on a flat-fee basis, earning a preset amount on the sale rather than a percentage of the sale price.

- Sell to a cash-homebuying company: These companies, which often advertise “we buy houses,” pay in cash, close quickly and typically charge no fees. However, if you sell this way you’re likely to get a lower price for your home than you would with a traditional sale.

A home equity line of credit (HELOC) on an investment property is a loan taken out against a piece of real estate that you use to earn income or a financial return. So, instead of taking out a HELOC on the property where you actually reside, a HELOC on an investment property leverages a place where you do not live as collateral to borrow money.

While many borrowers have been interested in HELOCs over the past two years, HELOCs on investment properties aren’t nearly as common — or as easy to get. The vast majority of HELOCs are taken out against primary residences; lenders are more comfortable with a loan against the actual roof over your head because they know you’ll prioritize repaying that loan.

However, some lenders do offer HELOCs on investment properties. Here’s how they work, and how to decide if they’re a good strategy for your financing needs.

How do you get a HELOC on an investment property?

Getting a HELOC is similar to getting a mortgage (in fact, HELOCs are a type of second mortgage). Here’s how the application process works.

1. Know your finances.

Before you apply for a home equity line of credit, you’re going to want to estimate how much equity you have. Property values have continued rising this year – albeit more slowly than they had been during the peak of the pandemic – so you’ll want to get a sense of what your property is worth versus how much, if any, you have left to pay on the first mortgage. The difference between how much you owe and the investment property’s fair market value equals, roughly, the amount of your equity stake. In ascertaining the value, you might want to consult a real estate professional who specializes in similar properties to issue a broker price opinion on yours.

2. Shop around to find the best deal.

Shopping around for a HELOC on an investment property is going to be more limited than for the regular, residence-based variety: There simply aren’t as many lenders that offer these lines of credit. Still, there are always choices, and it’s always important to compare. Try to find at least three lenders, and try to suss out how practiced they are in this sort of HELOC. Look at the APR that each lender offers, and be sure to scrutinize the fine print to understand whether there are additional fees such as a penalty for closing the line of credit early.

3. Apply.

When you’re ready to officially apply for a HELOC, be prepared for the kind of complete under-the-hood type of financial scrutiny you would receive with any type of request to borrow a sizable chunk of money. A lender will look at your credit score, your debt load, your cash flow, your cash reserves and every other detail about your finances to determine a) whether they will loan you the cash and b) how much they’re going to charge you to borrow it. The lender will also probably do an appraisal of your property, which sets the official value on it. In determining its worth, they’ll look at its condition and also the amount and sort of income it generates.

4. Close.

Closing on a HELOC is typically a much faster process than closing on a traditional mortgage. Some lenders will close in as little as three days, and you can access the cash within a week.

What are the pros and cons of getting a HELOC on an investment property?

Pros

- Cheaper than many other forms of borrowing: The interest rates on HELOCs are often lower compared to other forms of financing like credit cards and personal loans. (You’ll likely pay a bit more because it’s tied to an investment property, however — more on that below.) A HELOC might also be simpler and cheaper to obtain than a business or commercial property loan.

- Less risk for you: Taking out a HELOC on an investment property might feel a bit safer than a HELOC on your primary residence. If you default on the line of credit, at least the home you live in won’t be subject to foreclosure.

- A flexible way to access cash: You can continually draw from the HELOC during the initial draw period, so it’s often a good fit for fluctuating or longer-term expenses like renovation projects.

- Cheap initial payments: With most HELOCs, you only need to pay interest during the draw period. Paying back the principal starts during the repayment period.

Cons

- Limited availability: Not many lenders offer HELOCs on investment properties.

- Higher rates: An investment property is inherently riskier than a primary residence: You don’t live in it, which means you aren’t as impacted if you lose it. That means that lenders charge higher rates for any type of financing attached to one, including a HELOC. For example, at this writing,TD Bank’s lowest available APR on HELOCs for investment properties is more than 1 percentage point higher than a HELOC on a primary or secondary home.

- Extra fees: Most HELOCs come with an annual fee and an early cancellation or termination fee if you close the line within the first two or three years.

- Negative equity concerns: Real estate doesn’t always appreciate, and if your property loses value, you could wind up underwater (owing more on a property than it’s worth).

HELOC requirements for investment properties vs. primary residences

| Investment properties | Primary residences | |

|---|---|---|

| Credit score minimum | Generally 700 | 650-680 |

| Debt-to-income (DTI) maximum | 43% (can depend on anticipated rental income) | 43% to 50% |

| Loan-to-value (LTV) maximum | 80% | 85% |

When is it a good idea to use a HELOC on an investment property?

Using a HELOC on an investment property can be an easy way to access cash that will generate a return. For example, you might use the funds from the HELOC to buy another property that can act as an additional investment, without depleting your savings. Or you might use the funds to upgrade or expand your property, making it more attractive to prospective tenants and enhancing its revenue stream. HELOCs are an especially good idea when you want to use the funds on the real estate itself — especially because there are tax benefits (see below).

Are you able to deduct a HELOC on your taxes?

Tax advantages are one of the pluses of HELOCs. You might be able to deduct the interest paid on a HELOC, including a HELOC on an investment property, so long as the funds were used to build, improve or repair the real estate backing the loan in some way. Remodeling the premises, upgrading the HVAC system, constructing a new wing, or even buying an adjacent lot could all count as tax-deductible improvements.

You can’t deduct all of the interest, however. With HELOCs, you can only deduct the interest actually accrued on withdrawn funds (not on your total line of credit). Depending on your filing status, overall you can deduct up to $750,000 (if married filing jointly) or $375,000 (single or filing separately) of interest on combined debt, including any mortgages on your primary residence. You must also itemize deductions on your tax return.

What are the alternatives to using a HELOC on an investment property?

- Cash-out refinance: With a cash-out refinance, you’ll refinance the loan on your investment property to a higher amount — provided you have enough equity — and take the difference in cash. Some savvy real estate investors use this method to continuously add new properties to their portfolio mix. However, this strategy might not work as well today, with mortgage interest rates having gone up.

- HELOC on your home: If you can’t find a lender willing to extend a line of credit on your investment property, you might want to consider taking out a HELOC on your primary residence. This means your home is on the line, however, if you can’t repay what you borrow. You might not be able to get as sizable a loan, however, and you won’t be able to deduct any interest (because the loan’s backed by your home, not the investment property).

- Personal loan: Depending on your debt load, you might be able to take out an unsecured personal loan as a lump sum. The interest rates on these can be much higher if your credit isn’t the best, however, and you’ll need to start repaying what you borrowed right away.

- Small business loan: If you have set up a company to own/operate your investment property, consider comparing small business loans or line of credit to access the funds you need. The interest rates on these loans will likely be higher than that of a personal HELOC, and you’ll have to start full repayments right away or make more frequent payments (in the case of the line of credit). But if you have a solid business plan you can show to a lender that documents your strategy for expanding your real estate investment portfolio, this can be another viable option.

The bottom line on using a HELOC on an investment property

Opening a HELOC on an investment property can be a savvy financial move, particularly if your need for funds is real estate–related. You can leverage the property to improve the property — and its income-generating or appreciation potential. Plus, you may be able to score some tax benefits.

However, a HELOC on an investment property isn’t all upside: Rates are higher than some other types of financing — including residential-property HELOCs — and you need to have pretty solid financials. Also, the availability is limited to a small number of lenders.

So you’ve realized a profit on your investments? Buckle up and get ready to report your transactions to the Internal Revenue Service (IRS) on Schedule D and see how much tax you owe.

But it’s not all bad news. If you lost money, this form helps you use those losses to offset any gains or a portion of your ordinary income, reducing the taxes you owe. And if you profited from your transactions, Schedule D helps ensure you don’t overpay Uncle Sam for your gains.

What is a Schedule D?

Schedule D is an IRS tax form that reports your realized gains and losses from capital assets, that is, investments and other business interests. It includes relevant information such as the total purchase price of assets, the total price those assets were sold for and whether those assets were held for the long term (more than a year) or short term (less than a year).

Who has to file a Schedule D?

You’ll have to file a Schedule D form if you realized any capital gains or losses from your investments in taxable accounts. That is, if you sold an asset in a taxable account, you’ll need to file. Investments include stocks, ETFs, mutual funds, bonds, options, real estate, futures, cryptocurrency and more. Those who have capital losses that they’re carrying over from previous tax years will want to file Schedule D so that they can take advantage of the tax benefit.

Others will need to file Schedule D as well. Those who have realized capital gains or losses from a partnership, estate, trust or S corporation will need to report those to the IRS on this form. Those with gains or losses not reported on another form can report them on Schedule D, as can filers with nonbusiness bad debts. Those with like-kind exchanges and installment sales may need to answer questions about their transactions on Schedule D.

How you report a gain or loss and how you’re taxed

The two-page Schedule D, with all its sections, columns and special computations, looks daunting and it certainly can be.

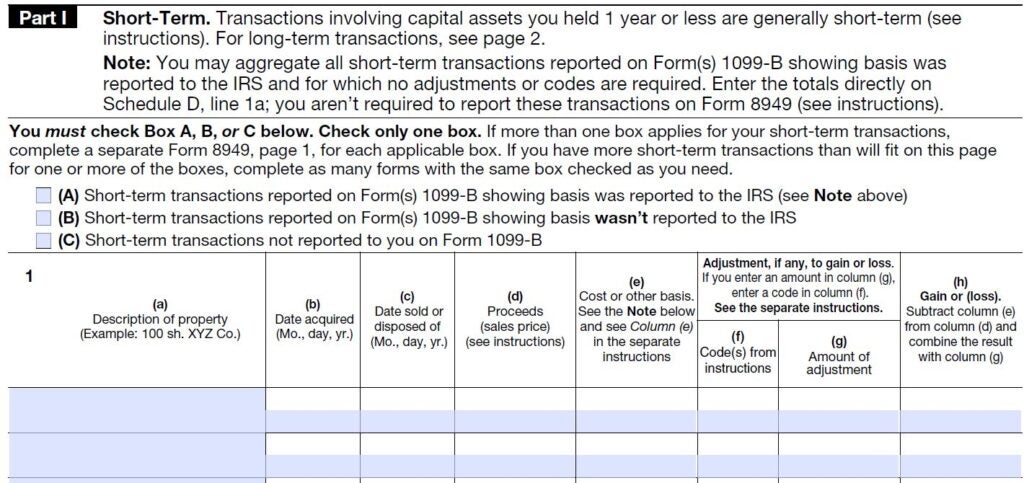

To start you must report any transactions first on Form 8949 and then transfer the info to Schedule D. On Form 8949 you’ll note when you bought the asset and when you sold it, as well as what it cost and what you sold it for. Your purchase and sales dates are critical because how long you hold the property determines its tax rate.

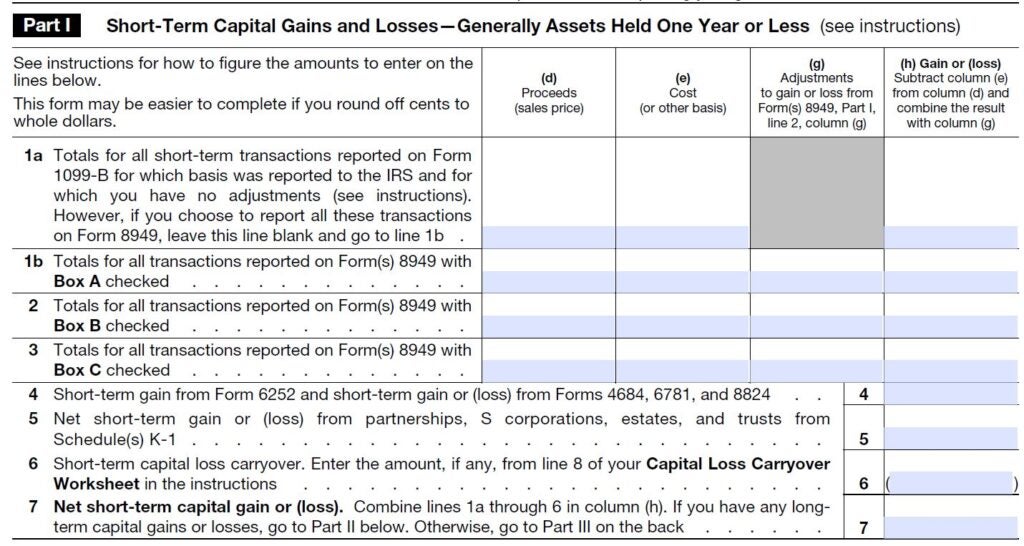

If you owned the asset for a year or less, any gain would typically cost you more in taxes. These short-term sales are taxed at the same rate as your regular income, which could be as high as 37 percent on your 2023 tax return. Short-term sales are reported in Part 1 of the form.

However, if you held the property for more than a year, it’s considered a long-term asset and is eligible for a lower capital gains tax rate — 0 percent, 15 percent or 20 percent, depending upon your income level. Sales of long-term assets are reported in Part 2 of the form, which looks nearly identical to Part 1 above.

Detail your transactions

Once you determine whether your gain or loss is short-term or long-term, it’s time to enter the transaction specifics in the appropriate section of Form 8949. All transactions require the same information, entered in either Part 1 (short term) or Part 2 (long term), in the appropriate alphabetically designated column. For most transactions, you’ll complete:

(a) The name or description of the asset you sold

(b) When you acquired it

(c) When you sold it

(d) What price you sold it for

(e) The asset’s cost or other basis

(h) The gain or loss

Total your entries on Form 8949 and then transfer the information to the appropriate short-term or long-term sections of Schedule D. On that tax schedule you’ll subtract your basis from the sales price to arrive at your total capital gain or loss, as in the sample below.

Schedule D also asks for information on some specific transactions that do not apply to all taxpayers, such as installment sales, like-kind exchanges, commodity straddles, sales of business property and gains or losses reported to you on Schedule K-1.

Check out the complete list and if any of these apply to your tax situation, it probably would be wise to turn Schedule D and the rest of your tax paperwork over to a professional. These are complicated matters, and it can be easy to make a mistake even with the best intentions.

Schedule D also requires information on any capital loss carry-over you have from earlier tax years on line 14, as well as the amount of capital gains distributions you earned on your investments.

You may be able to avoid filing Schedule D, if one of the two situations below applies to your return:

- If distributions, line 13, are your only investment items to report, you don’t have to fill out Schedule D; they go directly on your 1040 or 1040A return.

- You also can escape Schedule D if your only capital gain is from the sale of your residence. As long as you meet some basic residency requirements and your home-sale profit is $250,000 or less ($500,000 for married-filing-jointly home sellers), it’s not taxable and you don’t have to tell the IRS about it here or on any other form.

Total your transactions

Once you’ve filled in all the short-term and long-term transaction information in Parts 1 and 2, it’s time to turn over Schedule D and combine your asset-sale details in Part 3. This section essentially consolidates the work you did earlier, but it’s not as easy as simply transferring numbers from the front of the schedule to the back.

Lines 16 through 22 direct you to other lines and forms depending on whether your calculations result in an overall gain or loss. A couple of lines in Part 3 also deal with special rates for collectibles and depreciated real estate. Again, in these situations, expert tax advice might be warranted.

Use Schedule D to total up your gains and losses. If you total up a net capital loss, it’s not good investing news, but it is good tax news. Your loss can offset your regular income, reducing the taxes you owe – up to a net $3,000 loss limit.

If you reported a net loss greater than the annual limit, it can be carried forward to use against gains in future tax years until it’s exhausted.

As a bonus, your capital loss means you’re through with Schedule D. You simply transfer your loss amount to your 1040 and continue your filing work there.

Figure the tax on your gains

When you come up with a gain, the tax paperwork continues. And this is where the math really begins, especially if you’re doing your taxes by hand instead of using software.

Depending on your answers to the various Schedule D questions, you’re directed to the separate Qualified Dividends and Capital Gain Tax worksheet or the Schedule D Tax worksheet, which are found in the Form 1040 instructions booklet. These worksheets take you through calculations of your various types of income and figure the appropriate taxation level for each.

Before you begin either of these worksheets, be sure you’ve completed your Form 1040 through line 11 (that’s your taxable income amount), because that’s the starting point of both worksheets. From there you’ll have lots of addition, subtraction, multiplication and transferring of numbers from various forms.

But if you sold stock or other property, don’t be tempted to ignore Form 8949, Schedule D, the associated tax worksheets and all the extra calculations. Remember, the IRS received a copy of any tax statement your broker sent you, so the agency is expecting you to detail the sale, and gain or loss, with your tax filing.

Bottom line

The extra work needed in figuring your capital gains taxes is generally to your advantage. Regular income tax rates can be more than twice what’s levied on some long-term capital gains. So when you’re finally through with the calculations, your tax bill should be lower than it would have been if you had simply used the standard tax table to find your tax due.

Note: Kay Bell contributed to a previous version of this story.

Key takeaways

- Financing an overseas home purchase can be difficult if you aren’t a citizen or resident of that country.

- While some countries allow you to take out a local mortgage, you might find it easier to use a home equity line of credit (HELOC) from a U.S.-based lender.

- On the plus side, using a HELOC to buy international property lets you keep your property in the U.S. and provides quick access to funds.

- However, your home serves as collateral for the HELOC, putting you at risk of foreclosure if you can’t repay.

When Las Vegas-based real estate investor Alicia Cramer decided to buy property overseas, she took a novel approach. Using a home equity line of credit (HELOC) based on her stateside properties, she was able to invest abroad without spending months trying to get a local mortgage or unload her domestic real estate. “The HELOC was the best way to go if I didn’t want to sell everything,” she says. “Selling everything takes time anyway; a HELOC was faster.”

Cramer is just one of many property-owners in the U.S. looking beyond domestic borders to make their next investment. Thanks to their lower cost of living and affordable real estate, places like Mexico, Costa Rica, Panama and Indonesia are some of the most popular countries luring Americans to invest, according to a trend report by Coldwell Banker Global Luxury.

If you’re interested in buying a property overseas, a HELOC can be a good option to help finance your expenses. But before you go this route, it’s a good idea to consider the pros and cons as well as alternative options.

Financing foreign real estate

Local mortgages can be difficult to secure if you’re trying to purchase a property abroad – especially if you’re not a citizen or permanent resident of that country.

Even if the country has a mortgage industry, it can be tough to find a loan with terms as favorable as you’d get in the U.S. If you do secure one, it might come with a higher interest rate and a significant down payment requirement (often 30 percent – or more – of the property’s value). You’ll also want to consider the exchange rate between the country’s currency and the U.S. dollar. If the local currency strengthens against the dollar, your mortgage costs could go up. In addition, you may be forced to invest in a life insurance policy for the mortgage amount and name the bank as a beneficiary.

In Costa Rica, for example, obtaining a mortgage as a foreign citizen can be extremely challenging, local realty firms note. And the costs can add up quickly. Down payments can range from 30 to 50 percent, and interest rates are often between 8.5 and 10 percent for a 20-year loan, according to RE/MAX Ocean Surf & Sun in Tamarindo, Costa Rica.

Add in extensive paperwork, high fees and lengthy processing timelines, and it’s no wonder that Americans decide to finance a foreign property with a homegrown HELOC.

Using a HELOC to finance property overseas: Is it a good idea?

Compared to other financing options, using a HELOC to buy property abroad has its advantages. With a HELOC, you don’t have to sell any properties in the States to fund your overseas purchases. Plus, if you have a significant level of equity in your home, you can take out a sizable sum for your international investments – and get the money quicker than you would with many other types of funding.

But is it a good idea?

“Utilizing a HELOC for an international real estate investment can be a viable strategy, but it requires careful consideration,” says Mark Damsgaard, Founder & Head of Client Advisory at Global Residence Index, a firm that helps clients invest in international real estate. “The decision hinges on various factors, such as the current real estate market conditions, the investor’s risk appetite, and the specific terms of the HELOC.”

HELOCs typically have variable interest rates, so if rates go up, so will your monthly payments. “While it provides convenient access to funds based on home equity, I often advise my investor clients to be mindful of potential currency risks and interest rate fluctuations,” says Damsgaard.

While these concerns characterize any foreign investment, there’s an additional wrinkle with HELOCs: Your home serves as collateral for the line of credit. So if you can’t repay what you’ve borrowed, you could face foreclosure.

What are the pros of using a HELOC to purchase foreign property?

You keep your home in the U.S.

If you don’t want to sell your house to buy another house, a HELOC might be a good option.

There are many reasons why homeowners would want to hang on to their home, says Shreesh Deshpande, finance and real estate chair at the University of San Diego. In this instance, a HELOC could be a good alternative to selling.

“A lot of times the scenario is that somebody is planning to retire six years from now, but they still need to live in their existing property, so they keep their house while buying a house in a foreign country,” says Deshpande. “The other thing is that people want to have one foot in the U.S. and one foot abroad. A lot of the rationale has to do with staying close to their family. They have children and grandchildren in the U.S. so they don’t want to completely move.”

Better terms and lower down payments

With HELOCs, your credit line is determined based on the equity in your home. Banks normally lend around 80 to 85 percent of the home’s value. So, if you own your home outright and it’s appraised at $500,000, the bank might extend financing up to about $400,000.

Compare that to unsecured personal loans, most of which have a maximum of $50,000. There are lenders, such as SoFi and LightStream, who will do more — as much as $100,000, in some cases.

Be aware, though, that most lenders won’t let you use an unsecured personal loan to buy real estate or even make a down payment on a mortgage-financed purchase. Of course, you could get a collateralized personal loan; or if you can swing an all-cash deal, you could use the unsecured personal loan to get you over the hump.

HELOCs not only let you borrow more, they make you pay less. As of late January 2024, average HELOC rates range from 8.74 to 10.48 percent.

Personal loan rates vary quite a bit based on your credit score, but the average rate is currently 11.56 percent, and they can exceed 35 percent.

Plus, personal loans often have shorter terms, typically, one to seven years. HELOC borrowers can choose among various term limits, from 10 to 25-years. The loan is split into two periods: the draw period and the repayment period.

You become a cash buyer

A HELOC offers two things: capital and convenience. “The advantage is that the HELOC provides access to capital for the person who has a home in which he or she has significant home equity. And then they get this HELOC money to potentially invest in real estate,” says Deshpande.

Using the money from the HELOC essentially turns you into a cash buyer (as far as the seller is concerned). Being prepared to pay cash may get you a discount on the home’s sale price and or give you an advantage during negotiations.

It can also help speed up the transaction — another plus, as far as all parties are concerned. Borrowers can get a HELOC in as little as two weeks, depending on your lender and how quickly you can submit your paperwork.

More familiarity with your financing

As you may have experienced when buying a home in the U.S., applying for and taking out a mortgage can get complicated quickly. Now, imagine going through that process in a foreign country where you aren’t familiar with the real estate market, banking system, and, possibly, the language.

With a HELOC, you can feel more confident with your overseas investment, with a full understanding of your financing – including how much you have, how (and when) to repay it and where to find help if you have questions.

Cons of using a HELOC to purchase foreign property

Your home is used as collateral

HELOCs put your home on the line, literally. If you’re unable to make payments, the bank can take possession of the property.

“The bottom line is that if someone takes out a HELOC to buy an investment property abroad or wherever else, the person has increased their leverage or the amount of debt they have. So it’s definitely not reducing risk, it’s increasing risk,” says Deshpande.

Rates fluctuate

Traditionally, the interest on a HELOC accrues at a fluctuating, vs. a fixed, rate. As a result, your “monthly payments may fluctuate due to variable interest rates, akin to credit cards,” says Danny Margagliano, a Realtor with Team Margagliano in Destin, Florida. “This requires careful financial planning to mitigate potential risks.”

However, there are hybrid options that allow borrowers to pay a fixed rate on a portion of the credit line and an adjustable-rate on the remainder. Chase, for example, has a fixed-rate HELOC option which allows borrowers to switch from adjustable rates to a fixed rate during the draw period on loans of more than $1,000.

Unable to deduct the interest paid

One advantage of HELOCs is the tax break for homeowners. If using the money to buy, build or substantially improve their home, a taxpayer can deduct the paid interest on their returns each year.

But the improvements have to be on the collateralized home — the one backing the line of credit. If you use a HELOC to buy another property, the interest would not be tax-deductible.

Buying power may be limited

Of course, the amount of equity you have can dictate your buying power. Remember, most lenders are only going to let you borrow up to 80 percent of it, for starters. If you haven’t built up much equity in your home yet, it may be tricky to find a home that you can fully finance with a HELOC. In that case, you’ll need to explore other funding options.

How to use a home equity loan or HELOC to purchase foreign property

Before applying for a home equity loan or HELOC, you’ll want to make sure that you fulfill the eligibility requirements. Generally speaking, you’ll need a minimum of 20 percent equity in your home. Beyond that, most lenders expect a credit score in the mid-600s or higher, as well as steady income and a debt-to-income (DTI) ratio of 43 percent or less.

If you meet these criteria, you should be able to use a HELOC or a home equity loan (a HELOC’s fixed-rate, lump sum cousin) to buy property abroad. Generally speaking, the process will look like this:

- Shop around to compare lenders and find the most favorable loan terms and rates.

- Apply for the home equity loan or HELOC.

- Schedule an appraisal to determine the value of your home.

- Get approval from your lender.

- Close on the loan and receive the funds in a lump sum (with a home equity loan) or withdraw money as needed (with a HELOC).

Alternatives to using a HELOC or home equity loan to purchase property overseas

Overseas mortgage through your local lender

Although many lenders won’t fund a home purchase outside your home country, some will. For example, HSBC offers international banking services in select countries, and if you’re currently an account-holder, they may be able to help you secure a mortgage for international property.

If you go this route, hiring a local lawyer in the country where you’re buying might also be helpful. Before you agree to work with someone, ask about their experience with managing loans for international property and confirm that they’re permitted to practice in both the U. S. and their own land.

Retirement savings or self-directed IRA

You could tap into your retirement savings to purchase property overseas, but depending on how you do it, you may face tax consequences and other financial implications.

However, if you have a self-directed IRA, it can be a great resource to buy a house abroad and use it as a rental or investment property. In contrast to traditional IRAs, with this type of account, you’re free to invest in all kinds of assets, including domestic and international real estate. Be aware, though, that since the property is technically an investment, you can’t live in it until you reach the age when you start to receive distributions.

Developer financing or local mortgage

If you wish to buy a lot, home site or property under construction, developer financing may be an option. Fortunately, it usually comes with minimal paperwork and doesn’t require you to purchase life insurance. Depending on the country and developer, you may also lock in zero interest on this sort of loan.

Every type of developer financing is different, so read the fine print before you sign on the dotted line. Also, be sure you can repay the money you borrow with the repayment terms outlined in your contract.

You might also have the ability to take out a local mortgage to buy your new home. But as we’ve mentioned, this option often has major obstacles, depending on the country’s laws and policies. In some places, getting a local mortgage might not be possible at all.

Personal loans

Personal loans are another potential alternative to using HELOCs or home equity loans for overseas property. However, you can usually only borrow up to $50,000 (or, in some cases, $100,000) with this type of loan – and that might not be enough to buy a house abroad, even in a low-cost-of-living area.

Something else to keep in mind: You can’t use an unsecured personal loan for a down payment on a house, if you’re financing the purchase. If that’s your plan, you’d have to get a secured personal loan – and put down some type of collateral (such as a car) to get approved.

However, you could use an unsecured personal loan to augment your own funds to buy a home, foregoing financing entirely (see below).

Pay cash

If you can afford it, cash can be ideal if you’d like to buy a property overseas. It’s simple, it’s direct, and you can leverage it to negotiate the best possible price. It tends to expedite the closing process significantly, too.

Note that paying cash, however, makes the most sense if you’re buying a completed property, either pre-owned or new. You won’t want to risk your money on a project that may never materialize — especially if it’s located far away.

If you’re raising the cash by selling financial assets, like stocks or bonds, crunch some numbers first. Assess how much your investments are currently returning compared with the interest you’d pay on a HELOC. It’s also important to understand the costs involved with selling your investments. You might be on the hook for transaction fees or capital gains, which could cut into your earnings.

The bottom line on financing a property overseas

While all real estate transactions are complex, those that involve a property overseas come with an extra set of challenges. If you’re in the market for a house abroad, explore all your payment and financing options — and bear in mind that changes in currency rates can impact your overall costs significantly, both in purchasing and in maintaining your property.

Using a HELOC can be a strategic financing move. But reach out to a real estate attorney or experienced real estate professional — one specializing in overseas transactions — who can help you with the paperwork and guide you through the process. By doing so, you can protect your rights and avoid unnecessary roadblocks.

Key takeaways

- Let your mortgage lender or servicer know if you’re getting a divorce.

- Your divorce mortgage options include refinancing your mortgage, selling your home or paying your ex-partner for their share of equity.

- To help you decide, calculate the amount of home equity you have, as well as any tax implications and impact to your credit.

One of the biggest decisions divorcing couples face is who gets the house in a divorce. If you’re in this situation, your options might depend on how the home is financed and titled, among other factors. Another question people might ask during a divorce is, “What are my rights if my name is not on the mortgage?” Here’s everything you need to know about how divorce impacts your mortgage.

Mortgage options when dealing with divorce

1. Refinance your mortgage

Some divorcing couples with a joint mortgage decide to refinance to a new mortgage in only one of the spouse’s names. This releases a spouse from responsibility for that mortgage when their name is removed from the loan.

However, unless that partner’s name is also removed from the title, they can still benefit from the sale and equity in the home. It’s important to not only refinance but also update the house title to reflect one owner. When only one spouse is on the mortgage but both are on the title, you’ll need a quitclaim deed to remove one spouse’s name from the title.

Keep in mind: The spouse applying for the refinance can use only their own income and credit score to qualify, warns financial advisor Jeremy Runnels, CFP, of West Coast Financial in Santa Barbara, California. Depending on current rates, you could get a much higher rate when you refinance, as well.

“The lender is going to look at the individual and make sure they’re OK having them as the sole guarantor,” says Runnels. “The issue is can you afford it, and that goes for either spouse.”

If a partner will receive alimony or spousal support, they can use that income to qualify for a refinance, as long as the divorce settlement stipulates that they will receive alimony for at least three years, says Runnels.

If the couple has equity in the home, the spouse keeping the house could alternatively apply for a cash-out refinance to pay their ex-partner their share (more on that below).

Some refinancing options you have when dealing with a divorce include:

- Conventional refinance

- Streamline refinance (for FHA, VA and USDA loans)

- Cash-out refinance

2. Sell your home

The divorce agreement might call for the sale of the home and the splitting of profits. If you go this route — and many couples do — consider the costs. These might include the Realtor’s commission, the costs of sprucing up the property to make it more attractive to buyers, real property transfer taxes and capital gains taxes.

3. Pay your ex for their share of equity

Let’s say your home is worth $300,000, and you owe $200,000 on the joint mortgage. In this case, you’d have $100,000 in equity, so you’d need $50,000 to buy out the other spouse’s share (assuming a 50/50 split).

To get the cash, you could refinance into a $250,000 loan in your name only, and use the $50,000 cash payout to settle up with your ex.

You’ll need to qualify for the refinance, however.

“Their income needs to be high enough to handle the new mortgage on their own, and the home must have the equity in it to take the cash out,” says Michael Becker, loan originator and sales manager at the Baltimore retail branch of Sierra Pacific Mortgage. “FHA and conventional cash-out refinances are capped at 80 percent loan-to-value, while you can go to 100 percent on a VA loan.”

If you want to keep the house and don’t have enough equity to do a cash-out refinance or the money to pay your ex their share, a home equity line of credit (HELOC) or home equity loan could be the solution.

“You could look at doing either a home equity loan or a home equity line of credit, as some lenders will allow you to go to 95 to 100 percent of the value of your home,” says Becker.

Important financial considerations when getting divorced