Gov. Eric Holcomb announced Thursday that state economic development leaders have secured nearly $20.7 billion in committed capital investment this year.

The governor told the Indiana Economic Development Corp. board of directors that dollar volume represents the highest quarter on record for capital investment in the agency’s nearly 20-year history.

“This is a significant time in Indiana’s history,” Holcomb said in a statement. “Decades from now, we’ll look back on these years as a critical turning point that transformed Indiana’s future, cultivating the growth of future industries and creating high-paying, in-demand career opportunities for Hoosiers for generations to come.”

During the first quarter, 45 companies committed to locate or expand in Indiana, investing $20.68 billion in their operations and creating 5,158 new jobs with an average wage of $33.79 an hour or more than $70,000 annually, Holcomb told the IEDC board. He was joined for the announcement by Secretary of Commerce David Rosenberg and IEDC Chief Strategy Officer Ann Lathrop.

The committed capital investment totals 72% of the capital investment committed in all of 2023 – $28.7 billion, an all-time high for the IEDC, a news release said.

On many individual announcements involving economic development projects, the state typically declines to disclose how much companies plan to pay workers when jobs are being added.

IEDC board approval is often a necessary step in a company’s decision to announce a project. The state often approves tax incentives for various investments.

The news release said several companies are expected to make announcements in the coming weeks.

Sponsored by

Since 2020, North Carolina has announced more than 67,000 new jobs and $42.3 billion of capital investment, according to the N.C. Department of Commerce. During that same period, ElectriCities has tracked significant growth in North Carolina public power communities, including more than 8,500 new jobs and investment of more than $3.4 billion. We sat down with three North Carolina-based industrial site consultants to get their take on what’s driving the state’s recent investment boom and what they’re hearing from clients about continued economic expansion.

Our experts may not agree on the best barbecue style (more on that later), but there’s consensus about what makes North Carolina a top state for business. Factors like the state’s central location, educated and ready workforce, favorable tax climate, and low cost of doing business top the list.

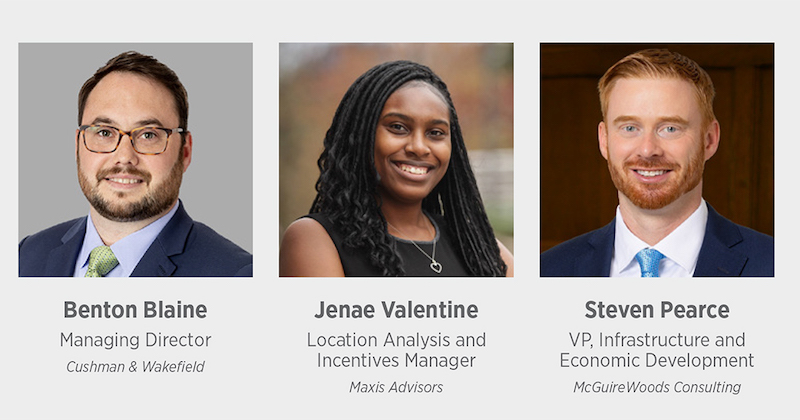

“I don’t think you can overstate being centrally located on the East Coast and how important that is to an industrial user who’s thinking about how they maximize their reach to their customer base,” said Steven Pearce, Vice President of Infrastructure and Economic Development at McGuireWoods Consulting.

Jenae Valentine, Location Analysis and Incentives Manager with Maxis Advisors, said population migration and quality of life are important drivers for many of her clients, as these factors are positive indicators of growth.

“North Carolina has so many assets and resources that have been developed over decades — all the ingredients are here.”

— Benton Blaine, Managing Director,

Cushman & Wakefield

Benton Blaine, Managing Director at Cushman & Wakefield, touted the state’s great interstate system and robust electrical infrastructure. “North Carolina has so many assets and resources that have been developed over decades—all the ingredients are here,” he said.

While projects related to EVs and batteries, including manufacturing, material processing, and recycling, are ongoing and still being sited, all three experts expressed concern about what may happen once the influx of federal funding stops.

“I don’t have a crystal ball, but I think we’ll see fewer and smaller EV and battery projects when federal dollars aren’t there to support them,” Pearce said.

Blaine said he expects to see a more diversified market, including lower-tier suppliers in EV, as well as manufacturing projects in solar, transformers, food, and life science.

When it comes to electric service, top considerations are reliability and cost, our experts said. Clients also want to know the source of their electricity and how much of the mix is renewable.

Valentine said, “My clients want to understand an electric provider’s ability to meet their ramp-up schedule so that when they’re ready to become fully operational, they’ll have the power needed to support their manufacturing operations.”

Knowing power is available is trickier these days.

“Up until 2019, my largest project was 11 megawatts, and that was a big project. Now I have a 150, a 100, an 80, two 60s, and a 40,” Blaine said. “We’re talking about projects that need to use a measurable portion of an entire power plant.”

Part of the fun of site selection in North Carolina is watching trend lines to forecast continued industrial growth.

Along with watching what he calls the natural progression of the EV supply chain, Blaine hopes we’ll see incentives for workforce training that supports current and future technology.

Pearce is watching the impact of the uncertainty that often comes with election years and current geopolitical movement. Since higher interest rates impact investment, he’s hopeful they’ll drop this year. He’s also watching population growth—or lack of it, based on recent data.

Along with all that, Valentine said she’s keeping an eye on construction costs, industrial lease rates, industrial vacancy, and job reports.

Whatever the future brings, it’s clear that each of these industrial site selection consultants appreciates what our state has to offer and that each enjoys calling North Carolina home.

They do not, however, enjoy the same style of North Carolina barbecue. Blaine and Valentine share an affinity for Lexington-style, while Pearce prefers Eastern-style. When it comes to the ’cue, let’s just agree to disagree.