Investing in nature to address climate change, support biodiversity, and protect ocean health—and more—is expected to reach record levels this year in response to more regulation and market demand, according to Cambridge Associates, a global investment firm.

Still, the amount of private capital invested to support natural systems will fall far short of what’s needed, according to the annual “State of Finance for Nature” report published in December from the United Nations Environment Programme.

A big reason is that nearly US$7 trillion in public and private finance was directed to companies and economic activities in 2022 that caused direct harm to nature, while only US$200 billion was directed to so-called nature-based solutions, or NbS—investments that protect, conserve, restore, or engage in the sustainable management of land and water ecosystems, as defined by the United National Environment Assembly 5, or UNEA5, the report said.

“Without a big turnaround on nature-negative finance flows, increased finance for NbS will have limited impact,” it said.

But the report also said that the misalignment “represents a massive opportunity to turn around private and public finance flows” to meet targets set by the United Nations Rio Conventions on climate change, desertification, and biodiversity loss.

Advertisement – Scroll to Continue

The conventions aim to limit climate change to 1.5 degree Celsius above pre-industrial levels, protect 30% of the earth’s land and seas by 2030, and to reach “land degradation neutrality” by 2030. Reaching those goals will require more than double the amount of current levels of nature-based investing by 2025, to US$436 billion, and nearly triple today’s levels to US$542 billion by 2030, the report said.

Most of the US$200 billion invested in NbS today is by governments, but private investors contributed US$35 billion—including US$4.6 billion via impact investing funds and US$3.9 billion via philanthropy. The largest source of private finance was in the form of biodiversity offsets and credits. [An offset is designed to compensate for biodiversity loss, while a credit is the asset created to restore it].

Many wealthy individuals and families concerned about climate change and the environment so far have focused their investment dollars on climate solutions and innovations in technology and infrastructure, or in technologies supporting food and water efficiency, says Liqian Ma, head of sustainable investment at Cambridge Associates.

Advertisement – Scroll to Continue

But “increasingly there is growing awareness that nature provides a lot of gifts and solutions if we prudently and responsibly manage nature-based assets,” Ma says.

Investments can be made, for instance, in sustainable forestry and sustainable agriculture—which can help sequester carbon—in addition to wetland mitigation, conservation, and ecosystem services.

“Those areas are not in the mainstream, but they are additional tools for investors,” Ma says.

Advertisement – Scroll to Continue

Finance Earth, a London-based social enterprise, is among the organizations working to make these tools more mainstream by creating a wider array of nature-based solutions in addition to related investment vehicles.

Finance Earth groups nature-based solutions into six themes: agriculture, forestry, freshwater, marine/coastal, peatland, and species protection. Supporting many of these areas are an array of so-called ecosystem services, or benefits that nature provides such as absorbing carbon dioxide, boosting biodiversity, and providing nutrients, says Rich Fitton, director of Finance Earth.

Each of these ecosystem services are behind existing and emerging markets. Carbon-related disclosure requirements (at various stages of approval in the U.S. and elsewhere) have long spurred demand for carbon markets, the most mature of these markets.

Advertisement – Scroll to Continue

Cambridge Associates, for instance, works with dedicated asset managers who have been approved by the California Air Resources Board to buy carbon credits, Ma says.

In its annual investment outlook, the firm said California’s carbon credits should outperform global stocks this year as the board is expected to reduce the supply of available credits to meet the state’s emission reduction targets. The value of these credits is expected to rise as the supply drops.

In September, the G20 Task Force on Nature-Related Financial Disclosures released recommendations (similar to those put forward several years ago by the Task Force for Carbon-related Financial Disclosure) that provide guidance for how companies can look across their supply chains to assess their impact on nature, water, and biodiversity “and then start to understand what the nature-related risks are for their business,” Fitton says.

The recommendations will continue to spur already thriving biodiversity markets, which exist in more than 100 countries including the U.S. In the U.K., a new rule called “Biodiversity Net Gain” went into effect this month requiring developers to produce a 10% net gain in biodiversity for every project they create.

Though developers can plant trees on land they’ve developed for housing, for example, they also will likely need to buy biodiversity credits from an environmental nonprofit or wildlife trust to replace and add to the biodiversity that was lost, Fitton says.

Advertisement – Scroll to Continue

This new compliance market for biodiversity offsets could reach about £300 million (US$382 million) in size, he says.

Finance Earth and

are currently raising funds for a U.K. Nature Impact Fund that is likely to invest in those offsets in addition to other nature-based solutions, including voluntary offset markets for biodiverse woodlands and for peatlands restoration.

The fund was seeded with £30 million from the U.K. Department for Environment, Food and Rural Affairs—money that is designed to absorb first losses, should that be needed. The government investment gives mainstream investors more security to step into a relatively new sector, Fitton says.

“We need the public sector and philanthropy to take a bit more downside risk,” he says. That way Finance Earth can tell mainstream investors “look, I know you haven’t invested in nature directly before, but we are pretty confident we’ve got commercial-level returns we can generate, and we’ve got this public sector [entity] who’s endorsing the fund and taking more risk,” Fitton says.

Since December 2022, when 188 government representatives attending the UN Biodiversity Conference in Montreal agreed to address biodiversity loss, restore ecosystems, and protect indigenous rights, several asset managers began “creating new strategies or refining strategies to be more nature or biodiversity focused,” Ma says.

He cautioned, however, that some asset managers are more authentic about it than others.

“Some have taken it seriously to hire scientists to do this properly and make sure that it’s not just a greenwashing or impact-washing exercise,” Ma says. “We’re starting to see some of those strategies come to market and, in terms of actual decisions and deployments, that’s why we think this year we’ll see a boost.”

Fitton has noticed, too, that institutional investors are hiring experts in natural capital, recognizing that it’s a separate asset class that requires expertise.

“When that starts happening across the board then meaningful amounts of money will move,” he says. “There’s lots of projects there, there’s lots of things to invest in and there’ll be more and more projects to invest in as more of these markets become more and more mature.”

-

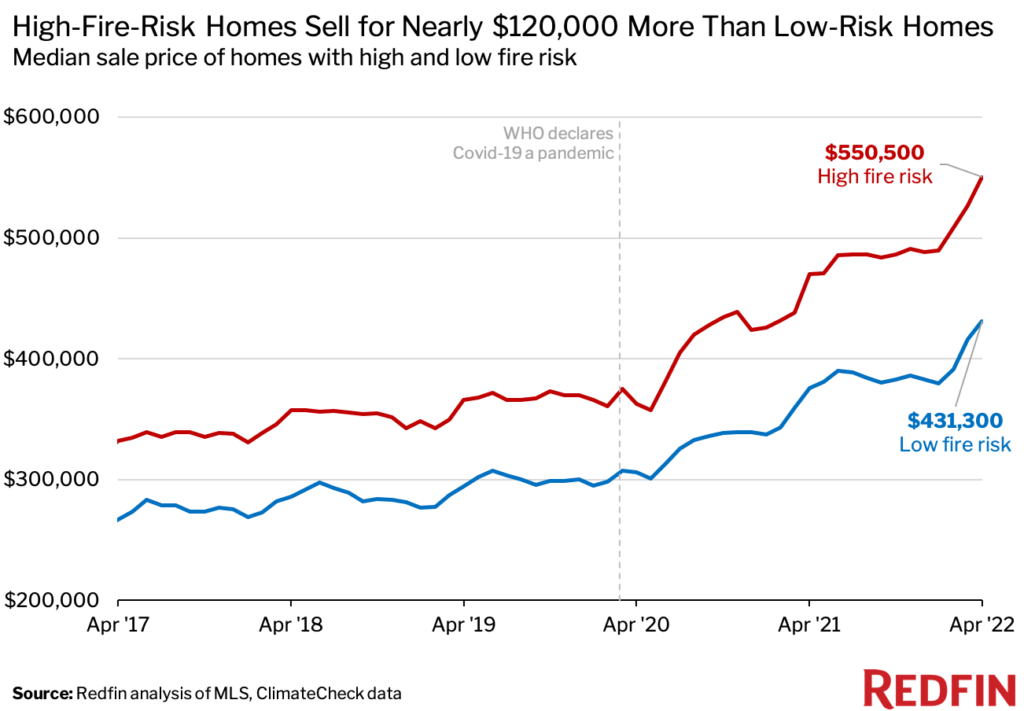

The typical high-fire-risk home sold for $550,500 in April, while the typical low-risk home sold for $431,300. That’s the biggest premium since at least 2017.

-

The median sale price of high-risk homes jumped 52% during the pandemic, while the median sale price of low-risk homes rose 41%.

-

High-risk homes sell for more in part because remote work has allowed many Americans to move to suburbs and rural areas, which are often more vulnerable.

-

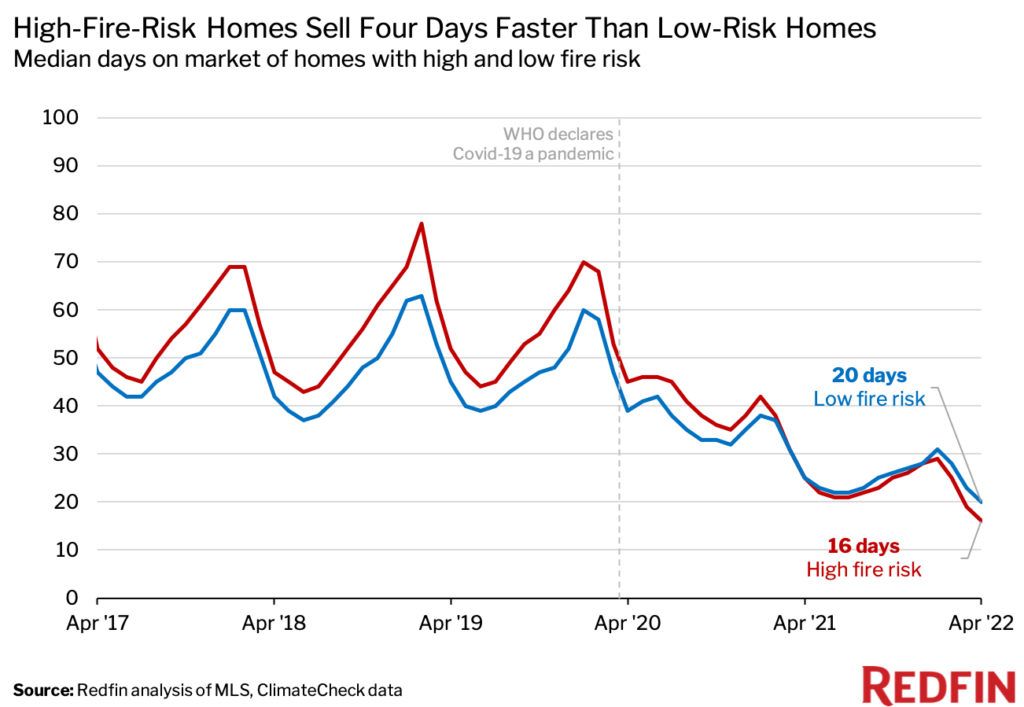

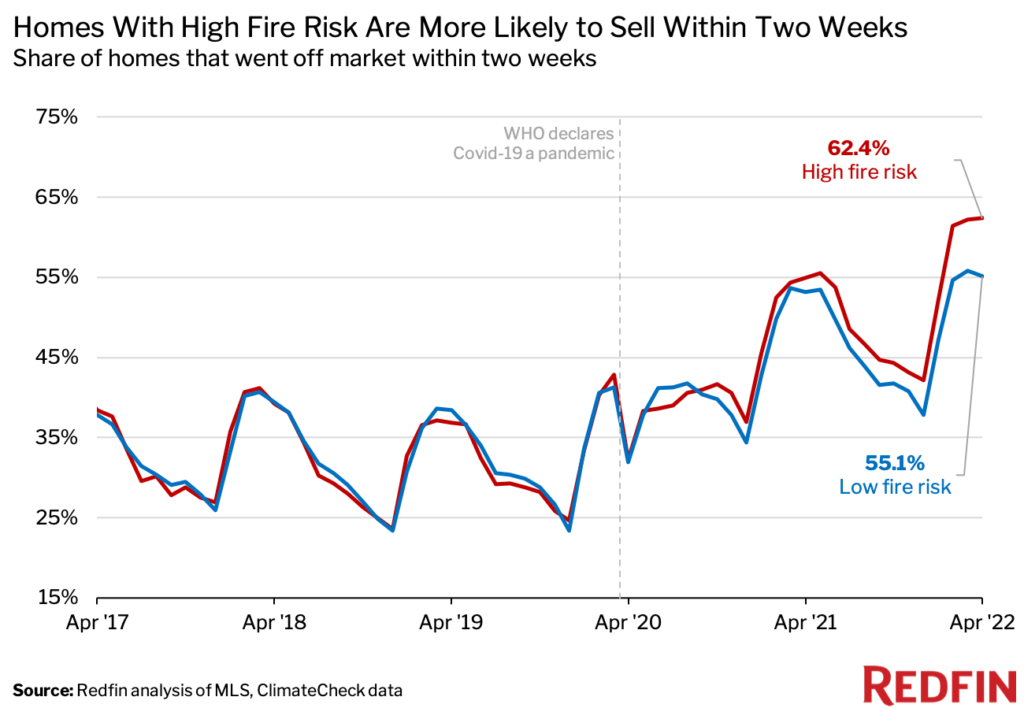

Homes with high fire risk are also selling faster than low-risk homes, but are more likely to experience price cuts once they’re on the market.

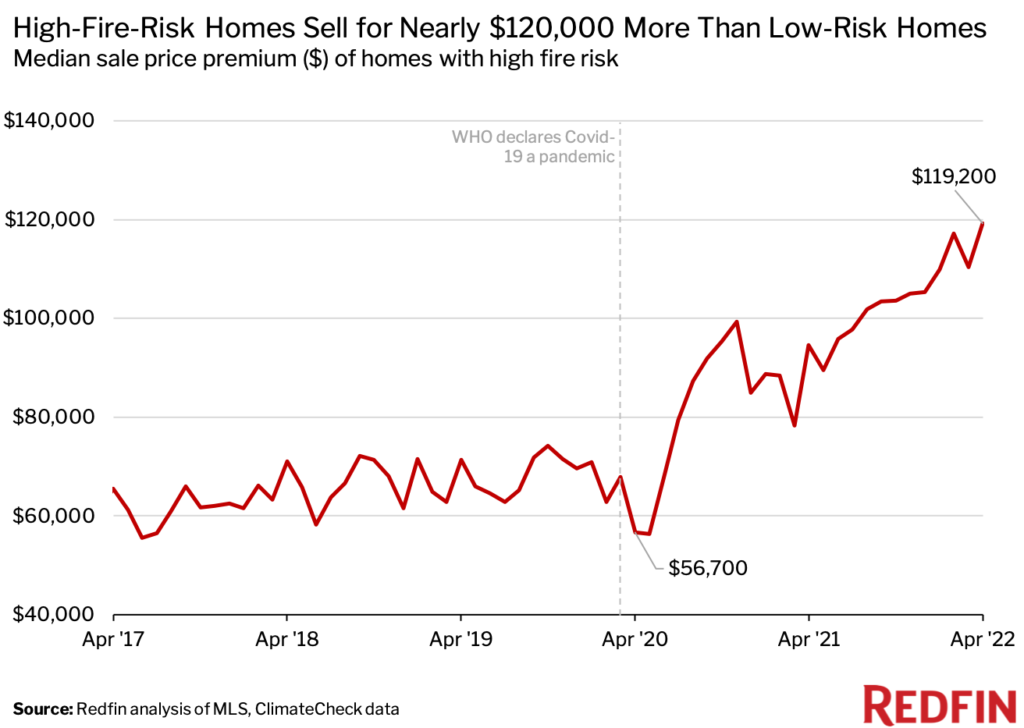

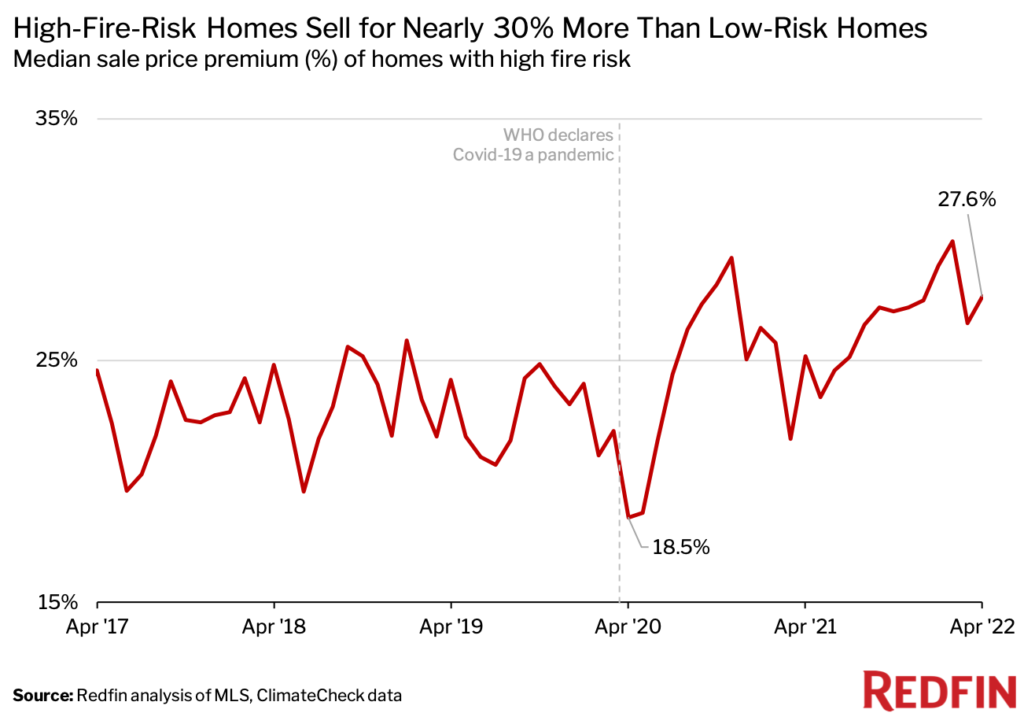

The median sale price of U.S. homes with high fire risk was $550,500 in April, compared with $431,300 for homes with low fire risk. In other words, the typical home with high fire risk sold for $119,200 (27.6%) more than the typical home with low fire risk—the largest premium in dollar terms since at least 2017. By comparison, homes with high fire risk sold for just $56,700 more (18.5%) two years earlier.

Fire-prone homes have historically fetched higher prices, likely because they tend to be larger and/or located in pricey West Coast metros. The typical high-fire-risk home purchased in April was 2,000 square feet, while the typical low-risk home was just 1,706 square feet. But the price premium for high-risk homes has surged during the pandemic. That’s in part because scores of Americans moved out of cities and into suburbs and rural areas, where homes are more likely to face fire risk due to the proximity to flammable vegetation. The median sale price of high-risk homes was up 51.7% in April from two years earlier, while the median sale price of low-risk homes was up 40.9%.

“Suburban homes tend to be more expensive because they’re large, and demand for large homes skyrocketed during the pandemic as Americans sought respite from crowded city life,” said Redfin Senior Economist Sheharyar Bokhari. “Pandemic buyers also hunted for deals due to surging home prices, and while fire-prone homes aren’t cheaper on average, buyers may feel they’re getting more bang for their buck because they’re getting more space. And for some pandemic buyers, the fire-prone home they bought in suburbia was actually cheaper than their last home because they were relocating from somewhere like San Francisco or Seattle.”

Wildfires in the U.S. have become increasingly catastrophic in recent years. The three most destructive wildfire years, in terms of acreage burned, have all occurred in the last decade, according to the National Interagency Fire Center.

While research has shown that many house hunters are concerned about climate risk when deciding where to live, oftentimes, it’s not a dealbreaker. For some, that’s because factors like relative affordability, home size and proximity to family take precedence. For others, it’s because they’re not aware of the climate risks in the area they’re moving to. Redfin.com now publishes climate-risk data for nearly every U.S. home, with the exception of rentals, to help house hunters make more informed decisions.

“For a lot of pandemic-era homebuyers, what has felt much more urgent than avoiding fire danger is finding a home they can afford at a time when inventory is so low and prices are so high,” said Corey Keach, a Redfin real estate agent in the Boulder, CO area, where the Marshall Fire—the most destructive in the state’s history—destroyed more than 1,000 homes at the end of 2021. “I worked with a young family whose Louisville home burned down in the Marshall Fire. Afterwards, they moved to nearby Superior, where a lot of homes also burned down. They just wanted to get into their next home fast because they had already gone through the painstaking buying process in 2020 and were worried prices were going to skyrocket another 20%.”

Keach continued: “As the market cools and shifts more in buyers’ favor, buyers may start thinking more about climate risk. My advice for house hunters in fire-prone areas is to look at newly built homes, which are more likely to have sprinkler systems and concrete-board siding instead of wood siding.”

Homes With High Fire Risk Also Sell Faster Than Low-Risk Homes

Fire-prone homes not only sell for more; they also get snatched up faster—another indication that evolving homebuyer preferences during the pandemic made high-risk areas seem more attractive to many house hunters. The typical high-risk home sold in 16 days in April, compared with 20 days for the typical low-risk home. That marks a shift from before the pandemic, when low-risk homes typically sold faster.

Another gauge of housing-market speed shows a similar trend: Nearly two-thirds (62.4%) of high-fire-risk homes sold within two weeks in April, compared with just 55.1% of low-risk homes. Prior to the pandemic, high- and low-risk homes had about the same likelihood of selling within two weeks.

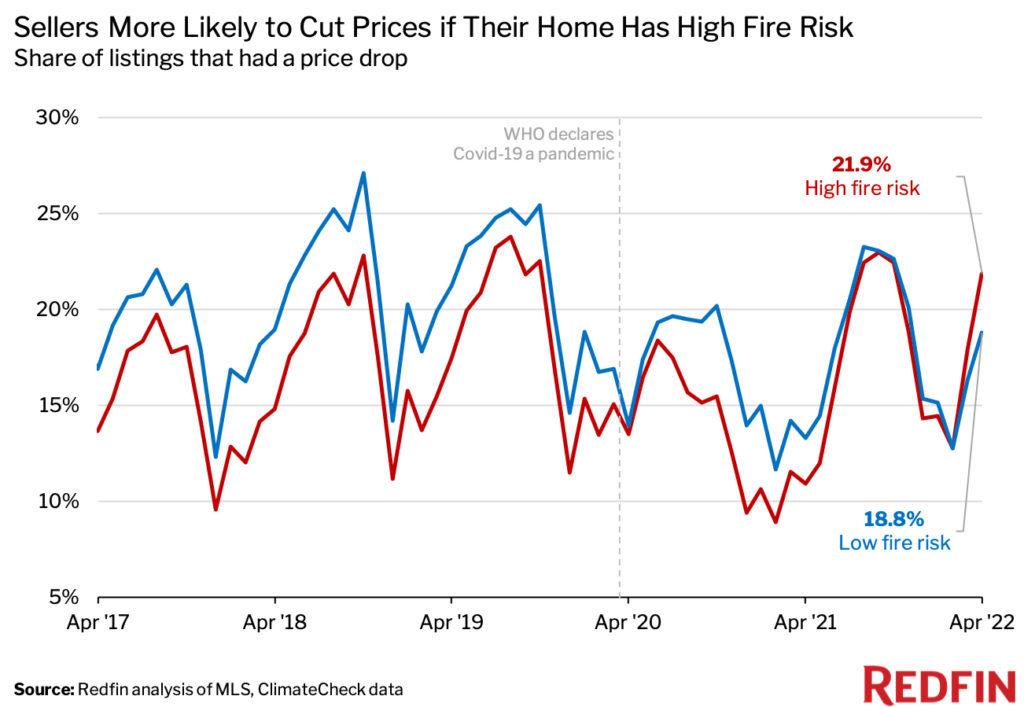

Price Cuts Are More Common For Homes With High Fire Risk

Another interesting shift we’ve observed in recent weeks is that sellers of high-fire-risk homes have become more likely than sellers of low-risk homes to slash their listing prices after putting their homes on the market. In April, 21.9% of high-risk listings had price drops, compared with 18.8% of low-risk listings. That’s only the second month on record (the first was March) during which fire-prone homes were more likely to have price drops.

“As the housing market cools, sellers are more likely to lower their pricing expectations in places where surging homebuyer demand has caused prices to significantly overinflate—places like the fire-prone suburbs Americans flocked to during the pandemic,” Bokhari said.

Price drops have been on the rise in the country as a whole lately as surging mortgage rates have triggered a slowdown in homebuyer demand. Boise, ID and Sacramento, CA, two hotspots for homebuyers relocating from pricey major cities, were among the top five metros where sellers cut their asking prices in April. Both face substantial risk from wildfires.

Methodology

Fire-risk data came from ClimateCheck, which assigns six different fire-risk categories to properties across the U.S.: very low risk, low risk, moderate risk, high risk, very high risk and extreme risk. For the purposes of this report, a high-risk property is one that falls into the high, very high or extreme category, while a low-risk property is one that falls into the very low, low or moderate category. We matched fire-risk data with MLS data in roughly 700 U.S. metro areas, allowing us to report on metrics including home sales and prices by fire risk. The climate-risk data in this report is from March 31, 2021.

Considering all that’s happening with climate change and the potential risk it brings to homeowners, you may be wondering if your house is in a flood zone. Whether you are a first-time homebuyer, looking to sell a vacation home, or simply a homeowner looking for some answers, you have the right and responsibility to find out.

Flooding is one of the most expensive natural disasters, causing damage to not only your home’s structure but your belongings. In fact, if your home floods just one inch, the damage can cost you upwards of $25,000. Flood damage can result from many environmental factors, such as hurricanes, a breached dam, severe storms, over-saturated ground from overflowing rivers, lakes, oceans, and more.

Whether you’re living in Vancouver, BC, or Miami, FL, floods can happen anywhere, and the number of homes at risk of flooding increases every year. However, many people across the nation aren’t sure what flood zone their home, or prospective home, is in and if they’re truly at risk. We’ll walk through how to check your home’s flood zone, what the different flood zones mean, and what you need to know if you’re buying or selling a house in a flood zone.

Check FEMA’s flood map to find out if your house is in a flood zone

To start, visit the Federal Emergency Management Agency (FEMA) Flood Map Service Center, a tool that displays information such as flood zones, floodways, and your home’s risk level. Type in a property’s address, and a map showing its flood zone will appear. As you’re analyzing the map, it’s important to remember that just part of the home’s lot could be in the flood zone. FEMA’s flood zone classifications range from low-risk to high-risk areas. Zones B, X, and C are low-risk flood zones, while A or V are high-risk flood zones. Let’s dive into what the different flood zones mean.

What do the different flood zones mean?

Zones with a letter grade of A or V are considered high-risk areas, while areas with letter grades of B, C, or X are considered low to moderate risk zones. FEMA has numerous flood zone classifications. Here are the most common flood zones and what they mean:

| Zone | Description |

|---|---|

| A99 | An area protected upon completion of an under-construction federal flood protection system like a dam or levee. This zone still has a 1% chance of flooding each year and is a required flood insurance zone. |

| AH | An area with a 1% chance of flooding each year, with the probability of 1 to 3 feet of water that pools in areas. Over the course of a 30-year mortgage, the likelihood of a flood is 26%. This is a zone where flood insurance is mandatory with BFEs at selected intervals. |

| AR | An area with increased flood risk where temporary flood insurance is required. This area will be protected from the 1% annual chance flood by a federal flood protection system actively building or restoring a flood control system such as a levee or dam. |

| VE, V1-V30 | Coastal areas are subject to a 1% chance of flooding per year, with additional hazards due to storm-induced velocity wave action. BFEs are determined in this zone. Mandatory flood insurance purchase requirements and floodplain management standards apply. |

| V | Coastal areas inundated by 1% chance of flooding. This zone doesn’t have BFEs, but is considered high-risk with mandatory flood insurance requirements. Over the course of a 30-year mortgage, the likelihood of a flood is 26%. |

| X (shaded), B | This is a moderate risk flood zone with a chance of a flood somewhere between the 100-year and 500-year mark. These areas are typically protected by levees or have shallow flooding areas. Zone B is being replaced with shaded zone X on new flood insurance rate maps (FIRMs). |

| D | This zone is designed to catch all other risk areas that are not defined by other flood zones. Zone D indicates a possible risk of flooding, but the hazard level is undetermined. |

| AO | This zone is specific to properties located near a river or stream. Areas in this zone still have a 1% chance of flooding each year with a 26% chance of flooding over the course of a 30-year mortgage. Flood depths range from 1 to 3 feet, resulting in Zone AO requiring flood insurance. |

| AE, A1-A30 | Zone AE is a newer version of what used to be zones A1-A30. These zones represent areas with a 1% chance of flooding each year, for which BFEs have been determined. Flood insurance is mandatory in these zones. |

| X (unshaded, C | Zone C and Zone X are low-risk areas with a .2% chance of an annual flood. These zones usually have minimal flooding, though there may be some ponding or local drainage problems. Zone X in particular is considered to be outside of the 500-year flood area and is protected from the 100-year flood by a levee. Zone C is being replaced with unshaded zone X on new FIRMs. |

*Base Flood Elevation (BFE): The elevation of surface water resulting from a flood has a 1% chance of equaling or exceeding that level in any given year.

It’s important to note that just because your home is not in a designated flood zone doesn’t mean flooding won’t happen. In fact, 20% of flood claims each year come from areas that are low risk. This is partly because flooding is so unpredictable and can be the result of several factors, such as thawing snow, burst pipes, hurricanes, tornadoes, flash floods, construction issues, and more.

What to know about buying a home in a flood zone

For almost everyone, finding out a home you’ve fallen in love with is in a high-risk flood zone can be a little heartbreaking. Sure, buying a home in a flood zone comes with additional risks, but it’s not a total deal-breaker. However, there are some things to consider that make the process a little different than buying a house in a low-risk flood zone, including:

Flood disclosure requirements

In the United States, there is no federal law that says home sellers are required to disclose information about a property’s flood risk or previous flood damage to prospective home buyers. However, 29 states do have flood disclosure requirements. This means, depending on where the property is located, it may be in your hands to research the flood risk of a property by visiting the Federal Emergency Management Agency (FEMA) Flood Map Service Center.

The general rule of thumb is that a home seller should never hide material facts about a home from prospective buyers regardless of state laws. Some states do have a specific form sellers use to disclose any known issues that could impact the safety or value of the home.

Flood insurance requirements

Even if your home is not in a high-risk flood zone, you should consider getting flood insurance. For example, should your home flood just one inch, the damage can cost you upwards of $25,000. Your mortgage lender may require you to have flood insurance coverage even if your home is located in a moderate-to-low-risk area. While you can purchase flood insurance at any time, note that it won’t take effect until 30 days after you’ve paid your premium.

Homeowners with property in a high-risk flood zone can obtain coverage through a private flood insurance plan or through the National Flood Insurance Program (NFIP), a program that covers nearly 5 million policyholders nationwide. NFIP is funded and backed by the federal government, which FEMA oversees. However, NFIP coverage isn’t available everywhere. Find out if your insurance provider participates in NFIP, or simply call your provider to inquire about adding flood insurance to your homeowner’s policy. Let’s look at the differences between the two options:

| NFIP | Private Flood Insurance | |

|---|---|---|

| Max rebuild cost | $250,000 | Typically up to $500,000 or higher |

| Availability | All 50 states | May only offer coverage in higher-risk areas |

| Elevation certificate required | Yes | No |

| Waiting period | 30 days | 15 days |

| Lender accepted | Yes | Yes |

| Building coverage | Replacement cost | Replacement cost |

| Contents coverage | Actual cash value | Contents coverage |

| Loss-of-use coverage | No | Yes |

| Loss avoidance coverage | No | Yes |

| Debris removal | Yes | Yes |

Home values impacted by flood zones

Now, you may be wondering if property value can be negatively impacted if it’s in a high-risk flood zone. The short answer is yes. However, homeowners can offset this and protect the home from flooding by implementing a few strategies, such as purchasing flood insurance, installing a sump pump, investing in flood sensors, and adding barriers around your home.

What to know about selling a home in a flood zone

Real estate disclosures and flood zones

Real estate disclosures, or a seller disclosure, is a set of documents answered by the seller of a home, listing any known issues with the property and any remodel projects completed during the time they owned the home. All states have laws regarding real estate disclosures and documents that provide details about a property’s condition that might negatively impact its value. However, as mentioned above, the specific laws regarding previous flooding information and flood zone status vary state by state.

Strategies for selling a house in a flood zone

It’s true that some buyers may not be willing to take on the risk of living in a flood zone. However, there are some strategies to make your home more attractive to those on the fence:

- Adjust sale price based on flood zone and the local housing market. Work with your real estate agent on a pricing strategy to determine a competitive sale price and get buyers through the door.

- Be sure to mention if your home has never flooded. Request a copy of a free report showing your past seven years of insurance claims history through the Comprehensive Loss Underwriting Exchange (CLUE). This may help put potential buyers at ease and give them peace of mind if they’re hesitant about making an offer.

- Offer to cover the insurance bill. Another option is to offer to cover the flood insurance costs for a year as an incentive to buy the home. This can be done through an adjustment to the purchase price or as a credit at closing.

- Ask about the Community Rating System. The Community Rating System is an optional incentive program that encourages community-wide initiatives to reduce flooding. Communities enrolled in the program may be eligible for discounted flood insurance.

- Order a certificate of elevation. A potential buyer may be required to present the elevation certificate to their insurance agency as well as their lender. The certificate describes the risk a property would be at if a major flood were to occur and if the property is above the height of estimated floodwaters.

Reduce flood risk with home improvements

There are many ways to reduce the risk of flood damage, and not all of them are difficult or expensive. Michael Stahl, the CMO of SERVPRO, a trusted leader in the restoration industry, advises homeowners on several proactive ways to reduce water damage. “Regular maintenance work such as cleaning gutters, roof repair, checking rain spouts to ensure the water drains away from your home, and repairing sidewalks and driveways near your home can help mitigate damage,” suggests Stahl. “Additionally, proper landscaping can greatly help mitigate flood risks. By sloping your yard away from your home and adding drainage to your driveway, you help prevent opportunities for flood water to gather and cause damage.”

Michael Stahl further explains, “If flooding has occurred, you must ensure safety – is it safe to stay in your house? Are there concerns about electricity or hazards that can cause slips, falls, and injuries? Once you assess these, removing wet furniture and other items and putting them in a safe, dry place can help start the process. It’s important to know that wet materials are heavy, so you want to ensure you can safely do this without injury. We always recommend reaching out to an expert in water restoration to help with this process and provide the professional services ultimately needed to mitigate the damage.”

To appeal to more buyers, here are additional home improvements and renovations to consider:

- Elevate your home. Raise the first floor of your house by just one foot above base flood elevation, and you could see a 30% reduction in annual flood insurance premiums, according to FEMA. It’s important to note that a project like this, on average, costs about $47,500.

- Elevate major appliances. Save yourself and future buyers from an additional flood insurance surcharge by relocating your appliances, water heater, HVAC system, and furnace to an elevated platform.

- Reduce the risk of sitting water by adding vents in the crawl space. Water and moisture can cause costly structural damage to your foundation. If your home is ever to flood, vents in the crawl space will allow any water that enters the crawl space to exit back out. Sitting water can damage your foundation so it’s important to properly maintain a crawlspace to prevent costly repairs in the future. Vents in the crawl space allow water to flow freely in and out of the enclosure, reducing the risk of structural issues in the event of flooding.

- Add barriers or sandbags around your home. Beams, levees, and flood walls can reduce the risk of flood water entering your home. Be sure to research whether your local building codes permit barriers around your home. If permanent barriers aren’t an option, you can always add sandbags around your home to create a protective wall for added protection.

- Install an automatic shutoff valve and check valve. An automatic shutoff valve installed near the primary water inlet in your house can help reduce the risk of major flood damage to your home. When a battery-powered flood sensor is activated, it turns off the main water supply. You can also install a check valve in plumbing to prevent flood water from backing up into your drains.

- Be proactive and invest in flood sensors. Flood sensors are placed in several locations throughout your home and will notify you the moment water is detected where it shouldn’t be. It will also alert you of other events that can cause water damage, like a burst pipe or overflowing sink.

- Install a battery-powered sump pump. A sump pump is designed to remove water that has accumulated in your basement and out of your home to a dry well or storm drain. It can cost about $1,200 to install a sump pump but it’s a solid investment to minimize flood damage.

Learn more about FEMA’s new pricing methodology for insurance premiums, Risk Rating 2.0.