When Chloé Daniels was 28 years old in 2019, she made the biggest financial mistake of her life. She gave her then-boyfriend roughly $30,000 in just over a year as “an investment” in his business of flipping houses in the Chicago area.

“It was my entire life savings at the time,” says Daniels, now 32. “I didn’t even have an emergency fund. And every time I had money, I would re-invest. I just kept funneling more money into it.”

When the pandemic hit, the house flipping operation fell apart. Labor costs ballooned. Lumber prices skyrocketed. It wasn’t long before the relationship fell apart, too.

Daniels soon realized she was never going to get her initial $30,000 investment back. To this day, she says she’s never recouped the money.

“I didn’t know anything about investing then,” says Daniels.

The experience spurred Daniels to learn the best practices of investing and personal finance, knowledge she parlayed into her current role as a full-time financial educator at her company Clo Bare Money Coach.

“After picking the riskiest investment I could have ever made, I don’t want to risk my money like that,” says Daniels.

Since 2021, Daniels has attracted a legion of mostly Gen Z and millennial followers on social media by teaching people “how to invest the lazy way.” Her content, courses and webinars focus on learning how to automate savings and create simple portfolios with low-cost funds.

Instead of betting on hot stocks, buying gold or yes even investing in super risky private money lending deals, Daniels emphasizes a set-it-and-forget-it approach to building wealth. She’s created dozens of videos explaining the perks of Roth IRAs and the historically positive long-term returns of buying index funds.

“My approach is still aggressive – most of my portfolio is all in stocks — but it’s a more tried-and-true approach to investing,” she says.

Her current philosophy that index funds are best for most investors— an idea touted by investing legend Warren Buffet as well as a growing number of financial influencers — is a stark departure from the dicey gamble with her ex’s real estate venture.

As Daniels notes in an April 2023 video: “The lazy way I’m investing is way simpler, way less risky and incredibly easy.”

Daniels’ ‘lazy’ investing strategy explained

Daniels is a strong believer in using tax-advantaged retirement accounts like 401(k)s and individual retirement accounts (IRAs) to build simple portfolios with a handful of inexpensive index funds.

An index fund serves as a collection of stocks, offering investors instant diversification with the purchase of a single share. Take the S&P 500, for example, which tracks the 500 best performing companies in the U.S. By purchasing an S&P 500 index fund, you acquire fractional ownership in all the companies the index tracks, from Apple and Microsoft to Coca-Cola and Disney.

You can buy low-cost index funds as either an exchange-traded fund (ETF) or a mutual fund. Both function very similarly, though some 401(k) plan platforms only allow you to purchase mutual funds, while ETFs are generally available at all brokers that allow stock trading.

Index funds are considered less risky than picking individual stocks, since your money is spread over hundreds of companies instead of just one or two. Most are also cheap, with the best index funds featuring expense ratios of less than 0.03 percent, or $3 for every $10,000 invested.

Daniels began her investing journey in earnest by maxing out her 401(k) retirement plan in 2020 while working full-time as a communications specialist at an engineering firm. She contributed about 25 percent of her six-figure salary to the account and earned a company match, which is essentially free money.

She’s expanded her investment accounts since then, adding a Roth IRA, traditional IRA, solo 401(k), a taxable brokerage and even investing the funds within her health savings account. In March 2024, her net worth was $296,000, according to documents reviewed by Bankrate.

But she’s used the same low-cost passively managed funds to build wealth across all her accounts.

Here are the main funds Daniels uses in her investment accounts:

- QQQ: Invesco QQQ Trust (Nasdaq)

- VTSAX: Vanguard Total Stock Market Index Fund

- VOO: Vanguard S&P 500 ETF

- VOOG: Vanguard S&P 500 Growth Index Fund ETF

- VOOV: Vanguard S&P 500 Value Index Fund ETF

- VIMAX: Vanguard Mid-Cap Index Fund

- VIOG: Vanguard S&P Small-Cap 600 Growth Index Fund ETF

Putting investing on auto-pilot

Daniels not only keeps her portfolio simple, she also puts her contributions on auto-pilot.

By transferring a percentage of her earnings directly to her investment accounts each month, she’s practicing dollar-cost averaging, a strategy where you invest a fixed amount of money at regular intervals. This helps buy more shares when prices are low and fewer when prices are high, smoothing out the impact of market turbulence without trying to time the market — a notoriously difficult task.

“If the guys on Wall Street – who not only have more education but also more access to information — can’t consistently time the market correctly, then I’m not going to,” Daniels says.

If consistently buying index funds sounds super boring, that’s the whole point.

“We have movies like ‘Wolf of Wall Street’ or ‘Dumb Money’ that make us think investing is like gambling, it’s day trading, it’s super risky,” says Daniels. “There’s not a single movie out there about index funds because it’s not exciting. It’s very boring.

“‘Oh, index funds are doing fine again’ doesn’t exactly make for exciting headlines,” adds Daniels.

Investing over paying off low-interest student loan debt

While the idea of consistently buying cheap index funds isn’t new, Daniels holds a somewhat unconventional attitude toward investing and paying off debt.

Unlike some voices in the world of personal finance, Daniels says there are more important things than being entirely debt-free as quickly as possible.

It’s a stance in stark contrast to influencers like radio host Dave Ramsey, who built a multi-million dollar financial education empire on the premise that people should eliminate all debt before ever putting money in the stock market.

“That’s an insane idea,” Daniels says. “There’s so much in between ‘be debt-free’ and ‘only invest.’ I think you should be doing both.”

Daniels believes paying off high-interest credit card debt is essential, but as she points out, most millennials and Gen Zers are saddled with tens of thousands of dollars in low-interest student loan debt.

She thinks it often makes more sense to make a small or minimum payment on student loan debt — so long as the interest rate is below about 5 to 8 percent — while investing at the same time.

Putting extra cash in the market instead — especially in your 20s and 30s when the power of compounding interest is really on your side— can yield better returns over time, Daniels says, even when accounting for interest charges.

That’s because the stock market has historically earned average returns of 8 percent or more, while low-interest student loan debt may only charge an interest rate of 4 percent or less. It’s not costing you much to hold that debt, but you miss out on the potential growth of investing at least a portion of your money.

“When you run different scenarios, you can see if it makes sense to decide if you want to pay off your debt early, do I want to do a combination of both or do I just want to (make the minimum payments) and be investing,” Daniels says.

Daniels acknowledges she didn’t follow this approach in her late 20s, when she paid off almost $40,000 in student loans in two years. She refers to it as her “debt-free mistake” and her other biggest financial regret.

“I’ve done the calculations, and that’s cost me about $1 million long term,” says Daniels. “Yes, I saved about $18,000 in interest by paying off that much debt when I did. But I don’t think anyone would really choose to save $18,000 in interest over making $1 million over time.”

Daniels still carries about $10,000 in student loan debt at a 3.5 percent interest rate. She plans on making the minimum payment until the debt is eventually paid off.

Quitting her 9-5 to to run Clo-Bare full time

In October 2021, Daniels left her job as a communications specialist to pursue Clo Bare Money Coach full time.

In addition to posting daily content about saving and investing on Instagram and Tik-Tok (where she now has over 120,000 followers on each), Daniels offered 1-on-1 financial coaching. She earned about $5,000 a month in the six months leading up to quitting her 9-5 job.

But after devoting all her time to her growing business, Daniels says the profits really started rolling in.

By December, Daniels debuted her Lazy Investor’s Course where 91 people signed up to get access for $379 each — a nearly $35,000 launch. Just over two years later, the self-paced Lazy Investor’s Course retails for $997.

What began as blogging part-time about her personal experiences saving and budgeting money back in 2018 has transformed into a six-figure full-time career managing an education platform built around her personal brand.

“I knew I would regret it if I didn’t try it,” she says.

Daniels is always quick to point out that she’s not a certified financial planner, or licensed to provide specific investment advice. She’s offering educational resources and sharing both the wins and failures she’s experienced along her journey.

Different aspects of that journey really resonate with people, especially other women in their late 20s and 30s. Whether it’s struggling to decide whether to pay off student loans or invest, or escaping a financially abusive relationship, her videos are filled with comments like “Oh man, I can relate” and “Definitely been there, and then some.”

Instead of downplaying her mistakes, Daniels has made a small fortune embracing them and using them as examples to teach others about how to be smarter with their money. Her nobody’s-perfect approach works, and it’s helping thousands of people learn about investing.

“Over and over again, my students say they chose me because they saw themselves in me,” she says. “And the fact I tell people they can get rewarded for being lazy with investing — I think that really resonates too.”

A home equity line of credit (HELOC) on an investment property is a loan taken out against a piece of real estate that you use to earn income or a financial return. So, instead of taking out a HELOC on the property where you actually reside, a HELOC on an investment property leverages a place where you do not live as collateral to borrow money.

While many borrowers have been interested in HELOCs over the past two years, HELOCs on investment properties aren’t nearly as common — or as easy to get. The vast majority of HELOCs are taken out against primary residences; lenders are more comfortable with a loan against the actual roof over your head because they know you’ll prioritize repaying that loan.

However, some lenders do offer HELOCs on investment properties. Here’s how they work, and how to decide if they’re a good strategy for your financing needs.

How do you get a HELOC on an investment property?

Getting a HELOC is similar to getting a mortgage (in fact, HELOCs are a type of second mortgage). Here’s how the application process works.

1. Know your finances.

Before you apply for a home equity line of credit, you’re going to want to estimate how much equity you have. Property values have continued rising this year – albeit more slowly than they had been during the peak of the pandemic – so you’ll want to get a sense of what your property is worth versus how much, if any, you have left to pay on the first mortgage. The difference between how much you owe and the investment property’s fair market value equals, roughly, the amount of your equity stake. In ascertaining the value, you might want to consult a real estate professional who specializes in similar properties to issue a broker price opinion on yours.

2. Shop around to find the best deal.

Shopping around for a HELOC on an investment property is going to be more limited than for the regular, residence-based variety: There simply aren’t as many lenders that offer these lines of credit. Still, there are always choices, and it’s always important to compare. Try to find at least three lenders, and try to suss out how practiced they are in this sort of HELOC. Look at the APR that each lender offers, and be sure to scrutinize the fine print to understand whether there are additional fees such as a penalty for closing the line of credit early.

3. Apply.

When you’re ready to officially apply for a HELOC, be prepared for the kind of complete under-the-hood type of financial scrutiny you would receive with any type of request to borrow a sizable chunk of money. A lender will look at your credit score, your debt load, your cash flow, your cash reserves and every other detail about your finances to determine a) whether they will loan you the cash and b) how much they’re going to charge you to borrow it. The lender will also probably do an appraisal of your property, which sets the official value on it. In determining its worth, they’ll look at its condition and also the amount and sort of income it generates.

4. Close.

Closing on a HELOC is typically a much faster process than closing on a traditional mortgage. Some lenders will close in as little as three days, and you can access the cash within a week.

What are the pros and cons of getting a HELOC on an investment property?

Pros

- Cheaper than many other forms of borrowing: The interest rates on HELOCs are often lower compared to other forms of financing like credit cards and personal loans. (You’ll likely pay a bit more because it’s tied to an investment property, however — more on that below.) A HELOC might also be simpler and cheaper to obtain than a business or commercial property loan.

- Less risk for you: Taking out a HELOC on an investment property might feel a bit safer than a HELOC on your primary residence. If you default on the line of credit, at least the home you live in won’t be subject to foreclosure.

- A flexible way to access cash: You can continually draw from the HELOC during the initial draw period, so it’s often a good fit for fluctuating or longer-term expenses like renovation projects.

- Cheap initial payments: With most HELOCs, you only need to pay interest during the draw period. Paying back the principal starts during the repayment period.

Cons

- Limited availability: Not many lenders offer HELOCs on investment properties.

- Higher rates: An investment property is inherently riskier than a primary residence: You don’t live in it, which means you aren’t as impacted if you lose it. That means that lenders charge higher rates for any type of financing attached to one, including a HELOC. For example, at this writing,TD Bank’s lowest available APR on HELOCs for investment properties is more than 1 percentage point higher than a HELOC on a primary or secondary home.

- Extra fees: Most HELOCs come with an annual fee and an early cancellation or termination fee if you close the line within the first two or three years.

- Negative equity concerns: Real estate doesn’t always appreciate, and if your property loses value, you could wind up underwater (owing more on a property than it’s worth).

HELOC requirements for investment properties vs. primary residences

| Investment properties | Primary residences | |

|---|---|---|

| Credit score minimum | Generally 700 | 650-680 |

| Debt-to-income (DTI) maximum | 43% (can depend on anticipated rental income) | 43% to 50% |

| Loan-to-value (LTV) maximum | 80% | 85% |

When is it a good idea to use a HELOC on an investment property?

Using a HELOC on an investment property can be an easy way to access cash that will generate a return. For example, you might use the funds from the HELOC to buy another property that can act as an additional investment, without depleting your savings. Or you might use the funds to upgrade or expand your property, making it more attractive to prospective tenants and enhancing its revenue stream. HELOCs are an especially good idea when you want to use the funds on the real estate itself — especially because there are tax benefits (see below).

Are you able to deduct a HELOC on your taxes?

Tax advantages are one of the pluses of HELOCs. You might be able to deduct the interest paid on a HELOC, including a HELOC on an investment property, so long as the funds were used to build, improve or repair the real estate backing the loan in some way. Remodeling the premises, upgrading the HVAC system, constructing a new wing, or even buying an adjacent lot could all count as tax-deductible improvements.

You can’t deduct all of the interest, however. With HELOCs, you can only deduct the interest actually accrued on withdrawn funds (not on your total line of credit). Depending on your filing status, overall you can deduct up to $750,000 (if married filing jointly) or $375,000 (single or filing separately) of interest on combined debt, including any mortgages on your primary residence. You must also itemize deductions on your tax return.

What are the alternatives to using a HELOC on an investment property?

- Cash-out refinance: With a cash-out refinance, you’ll refinance the loan on your investment property to a higher amount — provided you have enough equity — and take the difference in cash. Some savvy real estate investors use this method to continuously add new properties to their portfolio mix. However, this strategy might not work as well today, with mortgage interest rates having gone up.

- HELOC on your home: If you can’t find a lender willing to extend a line of credit on your investment property, you might want to consider taking out a HELOC on your primary residence. This means your home is on the line, however, if you can’t repay what you borrow. You might not be able to get as sizable a loan, however, and you won’t be able to deduct any interest (because the loan’s backed by your home, not the investment property).

- Personal loan: Depending on your debt load, you might be able to take out an unsecured personal loan as a lump sum. The interest rates on these can be much higher if your credit isn’t the best, however, and you’ll need to start repaying what you borrowed right away.

- Small business loan: If you have set up a company to own/operate your investment property, consider comparing small business loans or line of credit to access the funds you need. The interest rates on these loans will likely be higher than that of a personal HELOC, and you’ll have to start full repayments right away or make more frequent payments (in the case of the line of credit). But if you have a solid business plan you can show to a lender that documents your strategy for expanding your real estate investment portfolio, this can be another viable option.

The bottom line on using a HELOC on an investment property

Opening a HELOC on an investment property can be a savvy financial move, particularly if your need for funds is real estate–related. You can leverage the property to improve the property — and its income-generating or appreciation potential. Plus, you may be able to score some tax benefits.

However, a HELOC on an investment property isn’t all upside: Rates are higher than some other types of financing — including residential-property HELOCs — and you need to have pretty solid financials. Also, the availability is limited to a small number of lenders.

So you’ve realized a profit on your investments? Buckle up and get ready to report your transactions to the Internal Revenue Service (IRS) on Schedule D and see how much tax you owe.

But it’s not all bad news. If you lost money, this form helps you use those losses to offset any gains or a portion of your ordinary income, reducing the taxes you owe. And if you profited from your transactions, Schedule D helps ensure you don’t overpay Uncle Sam for your gains.

What is a Schedule D?

Schedule D is an IRS tax form that reports your realized gains and losses from capital assets, that is, investments and other business interests. It includes relevant information such as the total purchase price of assets, the total price those assets were sold for and whether those assets were held for the long term (more than a year) or short term (less than a year).

Who has to file a Schedule D?

You’ll have to file a Schedule D form if you realized any capital gains or losses from your investments in taxable accounts. That is, if you sold an asset in a taxable account, you’ll need to file. Investments include stocks, ETFs, mutual funds, bonds, options, real estate, futures, cryptocurrency and more. Those who have capital losses that they’re carrying over from previous tax years will want to file Schedule D so that they can take advantage of the tax benefit.

Others will need to file Schedule D as well. Those who have realized capital gains or losses from a partnership, estate, trust or S corporation will need to report those to the IRS on this form. Those with gains or losses not reported on another form can report them on Schedule D, as can filers with nonbusiness bad debts. Those with like-kind exchanges and installment sales may need to answer questions about their transactions on Schedule D.

How you report a gain or loss and how you’re taxed

The two-page Schedule D, with all its sections, columns and special computations, looks daunting and it certainly can be.

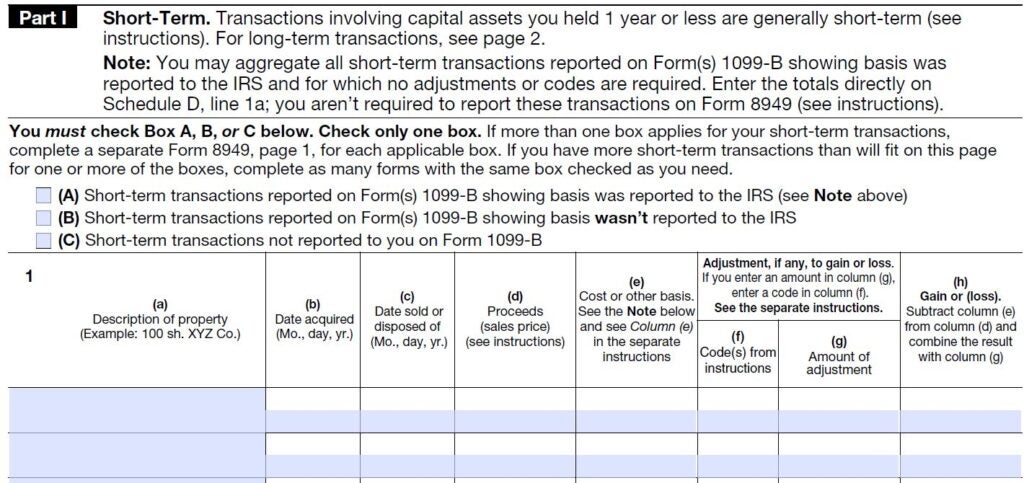

To start you must report any transactions first on Form 8949 and then transfer the info to Schedule D. On Form 8949 you’ll note when you bought the asset and when you sold it, as well as what it cost and what you sold it for. Your purchase and sales dates are critical because how long you hold the property determines its tax rate.

If you owned the asset for a year or less, any gain would typically cost you more in taxes. These short-term sales are taxed at the same rate as your regular income, which could be as high as 37 percent on your 2023 tax return. Short-term sales are reported in Part 1 of the form.

However, if you held the property for more than a year, it’s considered a long-term asset and is eligible for a lower capital gains tax rate — 0 percent, 15 percent or 20 percent, depending upon your income level. Sales of long-term assets are reported in Part 2 of the form, which looks nearly identical to Part 1 above.

Detail your transactions

Once you determine whether your gain or loss is short-term or long-term, it’s time to enter the transaction specifics in the appropriate section of Form 8949. All transactions require the same information, entered in either Part 1 (short term) or Part 2 (long term), in the appropriate alphabetically designated column. For most transactions, you’ll complete:

(a) The name or description of the asset you sold

(b) When you acquired it

(c) When you sold it

(d) What price you sold it for

(e) The asset’s cost or other basis

(h) The gain or loss

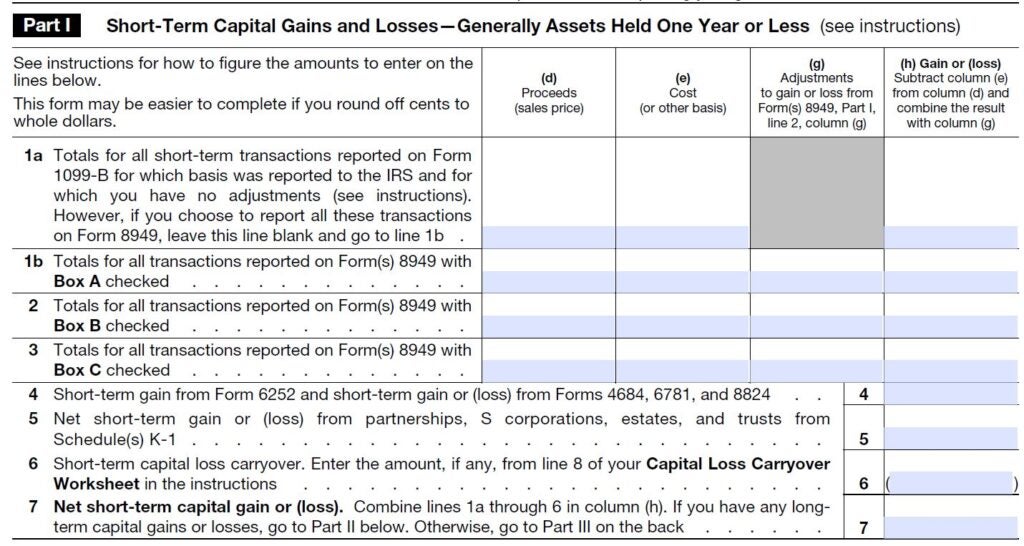

Total your entries on Form 8949 and then transfer the information to the appropriate short-term or long-term sections of Schedule D. On that tax schedule you’ll subtract your basis from the sales price to arrive at your total capital gain or loss, as in the sample below.

Schedule D also asks for information on some specific transactions that do not apply to all taxpayers, such as installment sales, like-kind exchanges, commodity straddles, sales of business property and gains or losses reported to you on Schedule K-1.

Check out the complete list and if any of these apply to your tax situation, it probably would be wise to turn Schedule D and the rest of your tax paperwork over to a professional. These are complicated matters, and it can be easy to make a mistake even with the best intentions.

Schedule D also requires information on any capital loss carry-over you have from earlier tax years on line 14, as well as the amount of capital gains distributions you earned on your investments.

You may be able to avoid filing Schedule D, if one of the two situations below applies to your return:

- If distributions, line 13, are your only investment items to report, you don’t have to fill out Schedule D; they go directly on your 1040 or 1040A return.

- You also can escape Schedule D if your only capital gain is from the sale of your residence. As long as you meet some basic residency requirements and your home-sale profit is $250,000 or less ($500,000 for married-filing-jointly home sellers), it’s not taxable and you don’t have to tell the IRS about it here or on any other form.

Total your transactions

Once you’ve filled in all the short-term and long-term transaction information in Parts 1 and 2, it’s time to turn over Schedule D and combine your asset-sale details in Part 3. This section essentially consolidates the work you did earlier, but it’s not as easy as simply transferring numbers from the front of the schedule to the back.

Lines 16 through 22 direct you to other lines and forms depending on whether your calculations result in an overall gain or loss. A couple of lines in Part 3 also deal with special rates for collectibles and depreciated real estate. Again, in these situations, expert tax advice might be warranted.

Use Schedule D to total up your gains and losses. If you total up a net capital loss, it’s not good investing news, but it is good tax news. Your loss can offset your regular income, reducing the taxes you owe – up to a net $3,000 loss limit.

If you reported a net loss greater than the annual limit, it can be carried forward to use against gains in future tax years until it’s exhausted.

As a bonus, your capital loss means you’re through with Schedule D. You simply transfer your loss amount to your 1040 and continue your filing work there.

Figure the tax on your gains

When you come up with a gain, the tax paperwork continues. And this is where the math really begins, especially if you’re doing your taxes by hand instead of using software.

Depending on your answers to the various Schedule D questions, you’re directed to the separate Qualified Dividends and Capital Gain Tax worksheet or the Schedule D Tax worksheet, which are found in the Form 1040 instructions booklet. These worksheets take you through calculations of your various types of income and figure the appropriate taxation level for each.

Before you begin either of these worksheets, be sure you’ve completed your Form 1040 through line 11 (that’s your taxable income amount), because that’s the starting point of both worksheets. From there you’ll have lots of addition, subtraction, multiplication and transferring of numbers from various forms.

But if you sold stock or other property, don’t be tempted to ignore Form 8949, Schedule D, the associated tax worksheets and all the extra calculations. Remember, the IRS received a copy of any tax statement your broker sent you, so the agency is expecting you to detail the sale, and gain or loss, with your tax filing.

Bottom line

The extra work needed in figuring your capital gains taxes is generally to your advantage. Regular income tax rates can be more than twice what’s levied on some long-term capital gains. So when you’re finally through with the calculations, your tax bill should be lower than it would have been if you had simply used the standard tax table to find your tax due.

Note: Kay Bell contributed to a previous version of this story.