We are all geniuses in retrospect. Still, we can confidently say predictions of a housing market slump in 2023 were very wrong. Interest rates rose to levels not seen since 2008, but the housing market remained surprisingly sturdy.

First, we should give the forecasters some credit. House price data is a fiendishly tricky thing, and not everyone is on about the same numbers. The Office for National Statistics (ONS) measures prices at completion; Halifax and Nationwide use data from their mortgage customers; Rightmove measures asking prices; and Savills measures house value, which ignores transactions entirely. Still, the consensus assumption from many experts was that over the 12 months to the end of 2023, house prices would sink between 5 and 10 per cent by some metric or another.

Admittedly, the 2023 calendar year is an arbitrary window for forecasting or recording data. Still, the slump did not happen. Not even close. Nationwide ultimately recorded a 1.8 per cent fall in prices in 2023, the ONS said 1.4 per cent, Rightmove 1.1 per cent, Savills said house values dropped a mere 0.3 per cent, and Halifax said prices rose by 1.8 per cent. For housing forecasters, 2023 was a predictive error equivalent to the Brexit vote, or Donald Trump’s presidential win. An anomaly they should have seen coming but did not.

In theory, rising interest rates hit buyers and owners alike. The former can no longer afford higher house prices because mortgages are more expensive. Meanwhile, many of the latter are forced into selling because they can no longer afford their mortgage.

Yet in 2023, owners held onto their homes because many more were on fixed-term mortgages than during the 2008 downturn, when variable-rate mortgages were much more popular. Rising wages and low unemployment, unlike in 2008, also helped them keep up with payments. So, even though buyers’ budgets shrank, sellers had less need to sell. The stand-off kept house prices as they were.

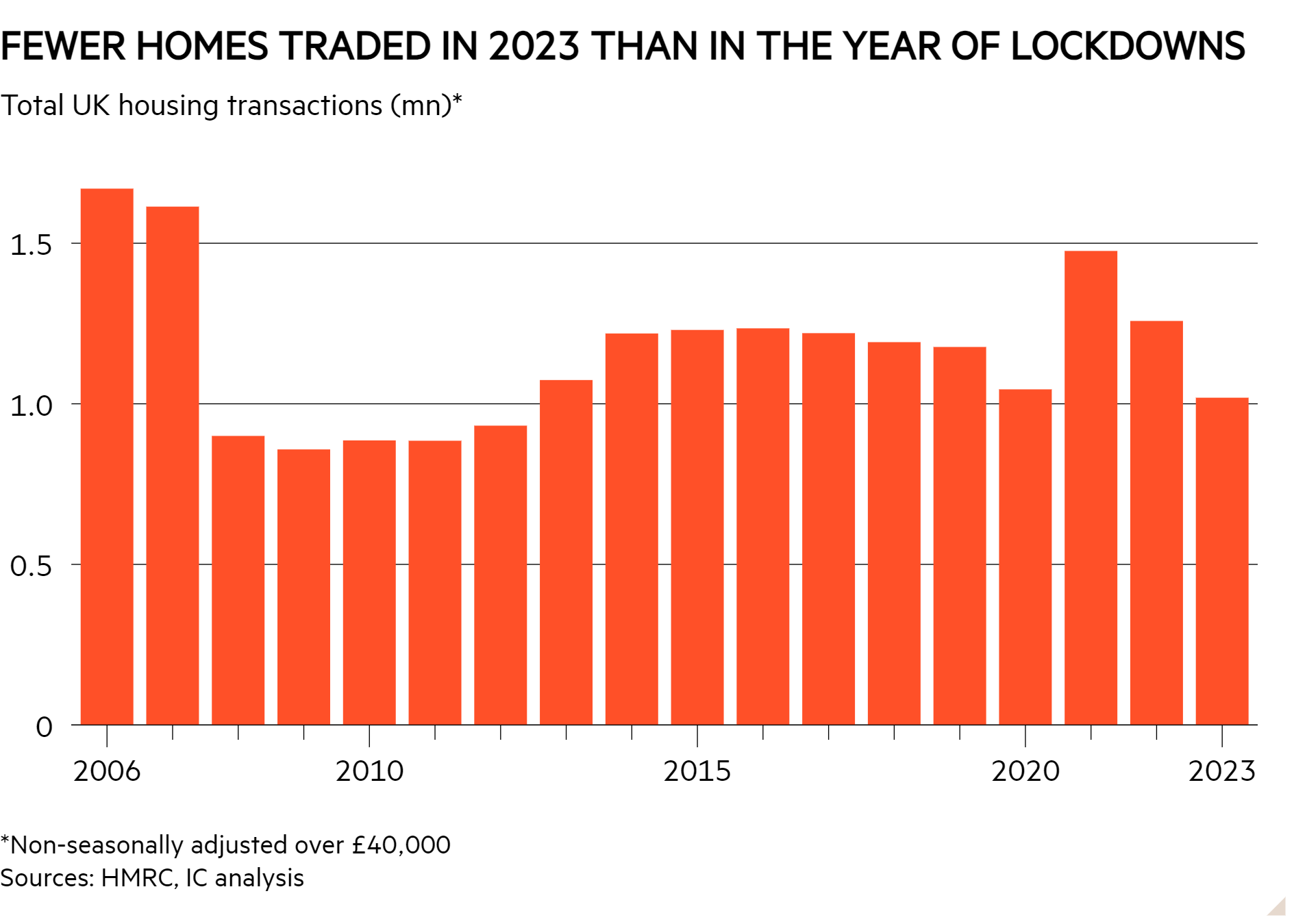

The numbers bear this out. IC analysis of HMRC data found that 2023 saw the lowest number of transactions in over a decade (see chart), and although mortgage arrears rose, they were nowhere near 2009 levels. In other words, most from the limited pool of sellers were not in dire straits.

The ‘I told you so’ award goes to the Joseph Rowntree Foundation (JRF), which outlined precisely how and why everything that happened would happen in a report from February 2023. In summary, its view was that all of the above combined with the persistent housing crisis keeping supply low would keep demand high even if budgets dropped.

But the JRF might turn out to be wrong, too. Bank of England data confirms that many homeowners will need to remortgage at higher rates between now and the end of 2026. As such, the central bank predicts monthly payments will rise to 9 per cent of post-tax income. It might not sound like a high figure to Londoners spending 35 per cent of their income on rent, but the figure is an average, meaning many homeowners will be in worse positions. It would also be the highest level since 2009.

Will this lead to a slump in house prices between now and 2026? Many of the same forecasters who were wrong about 2023 have revised their forecasts for 2024, anticipating anything from a 3 per cent drop to a 3 per cent rise. Your guess is as good as mine, but predictions of a significant fall have clearly tailed off.

House prices are the go-to metric for measuring the housing market. The logic is that if the average cost of a UK home at the point of sale is rising, so is demand. Over the year to December 2023, government data shows house prices fell 1.4 per cent, the impact of higher interest rates having broken a decade-long streak of rising prices.

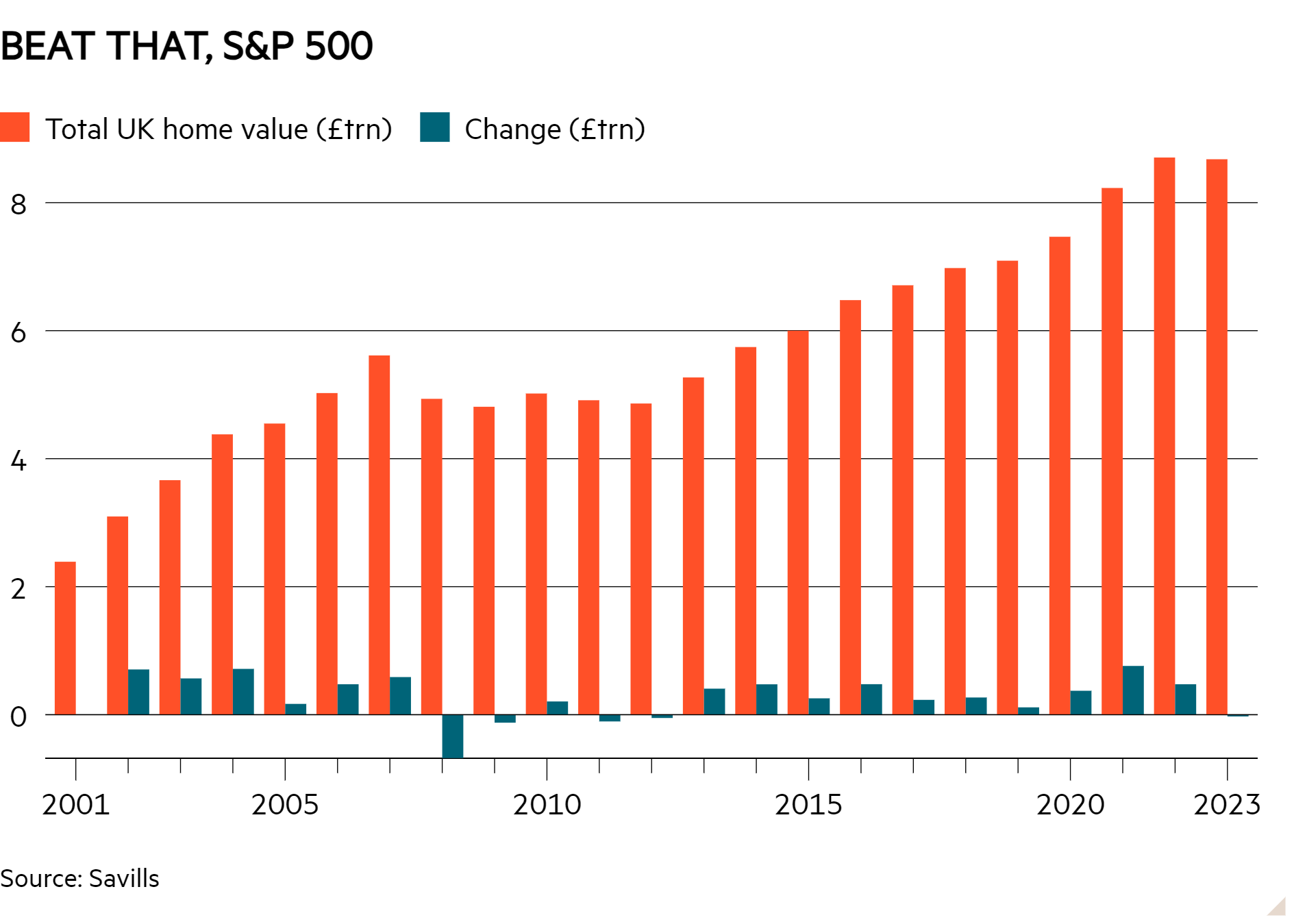

There is another way of looking at it. Rather than calculating an average house price based on data from some point in the sales process – at completion for the government numbers, at the mortgage approval stage for lenders Halifax and Nationwide, or from asking prices in the case of Rightmove and Zoopla indices – Savills has been measuring the market differently for over 20 years. According to its data, the total value of all UK homes as of the end of 2023, whether on the market or not, and whether owner-occupied, rented, or vacant, was £8.68tn, down 0.3 per cent from 2022 in the first fall since 2012.

This presents a slightly different view of the market. For those who consider a home an investment, whether because they are renting it or planning to sell it, home value makes more sense as a tracker of performance. After all, when real estate investment trusts (Reits) want to judge their portfolio value, they use holding value rather than the price at market sale. Likewise, homeowners are better off tracking the value of their investment instead of scrutinising the entire market for monthly changes in average price at the point of sale.

As expected, home value has fallen as transactions have dried up, but it is not by much. The 0.3 per cent drop looks more like stagnation than anything else. This is very different to 2008 and 2009, when over £800bn in home value was wiped out over the two years, a 14.3 per cent drop. Home values didn’t recover to their 2006 peak until 2013.

With some market data tentatively suggesting house prices are rising again as buyers take higher interest rates on the chin, Savills’ head of residential research, Lucian Cook, does not believe we will enter a 2008 or 2009-level downturn, for several reasons. The first is that the number of people on fixed-term mortgages has spread the pain of higher rates out across a longer period.

Cook says that’s partly because banks have “learned the lessons” from 2008-09 not to lend to those who can’t afford it. So far, this has meant fewer repossessions, which means there isn’t a sudden glut of stock. Indeed, as has been the case for years, housing supply is tight. Finally, there’s an economy which, though stagnant, hasn’t been accompanied by mass unemployment. This further bolsters people’s ability to pay their mortgages.

The data reveals other things. For example, in 2008 and 2009, the market downturn was seen across the country, whereas 2023’s drop was London-led. But the overall returns available remain the most telling statistics. If you bought a home in 2013, the data implies its value has jumped by about two-thirds. If you bought in 2001, you might be looking at a 263 per cent return on investment (ROI). And although home values have gone up and down over the years, the change over any given period has generally been less volatile than for equities. That has helped solidify the nation’s penchant for property investment.

- Housebuilders are responding to market slump

- Limited information about bulk deals

The past two years have shown just how cyclical the housebuilding business is. Higher interest rates have slashed private buyers’ budgets, so many of the UK’s biggest players have been bulk-selling homes to large buyers at discounts and eating the margin hit. Registered social housing providers (RPs), local councils and large institutional private rented sector (PRS) landlords buy these homes, sometimes before construction has completed or even started, and, in most cases, they then lease them out.

The model is an understandable response to a market downturn and can benefit investors, their buyers and the people ultimately living in the homes. However, many of these bulk deals are opaque, despite currently accounting for around a quarter of the largest listed housebuilders’ sales on average (see table). There is even less disclosure on RP deals, even though the limited information available suggests they can account for a significant proportion of these deals, and there is evidence of large housebuilder sales to at least one RP that is non-compliant with regulator standards.

We asked the UK’s largest listed housebuilders what proportion of their revenue in their most recent results came from sales to RPs, as well as for details on who those RPs are. Vistry (VTY) was the only FTSE 350 housebuilder who agreed to name some of its RP buyers. The rest of the FTSE 350 housebuilders declined to comment beyond the limited information available in their results. Only MJ Gleeson (GLE) and Springfield Properties (SPR), not in the large or mid-cap index, were fully transparent.

Investors should be wary of the opacity surrounding this proportion of housebuilder revenue. A source close to the Regulator for Social Housing (RSH) told us many of the units large housebuilders bulk sold to RPs during the 2008-09 downturn “needed additional work” and that RPs are “not sufficiently commercial when dealing with housebuilders”. As such, investors should scrutinise the current crop of bulk sales, especially when the fallout from the Grenfell fire tragedy shows how the high costs of poor dealmaking can come back to bite housebuilders years later.

| Housebuilder | Bulk/partnerships as a proportion of total* (%) | RPs as a proportion of total* (%) | Disclosure of RP names |

| Vistry (VTY) | 100 | 55 | Partial |

| Persimmon (PSN) | 22.7 | 22.7 | None |

| Springfield Properties (SPR) | 22.2 | 16 | Complete |

| MJ Gleeson (GLE) | 22 | 5.72 | Complete |

| Bellway (BWY) | 14 | 13.7 | None |

| Barratt Developments (BDEV) | 12.5 | 4.7 | None |

| Crest Nicholson (CRST) | 26 | Unknown | Partial in results |

| Taylor Wimpey (TW.) | 12.9 | Unknown | None |

| Redrow (RDW) | 2.8 | Unknown | None |

| Berkeley (BKG) | Unknown | Unknown | None |

| *Sales (or completions where sales were undisclosed) as per most recent results | |||

| Source: Company figures, IC analysis | |||

The amount of publicly available information is extremely limited. Some 4.7 per cent of Crest Nicholson’s (CRST) home sales were to RPs according to its latest results. Over the same period, the housebuilder entered into four joint ventures (JVs) with RPs through which it is to build homes for them. Two of those JVs, worth a combined £5.8mn, were with A2 Dominion Developments, an RP deemed non-compliant with the RSH’s standards. In its latest judgement on the RP from January, the RSH said: “This provider does not meet our governance requirements. There are issues of serious regulatory concern and in agreement with us the provider is working to improve its position.”

Asked about our findings, an RSH spokesperson said: “Social landlords must make sure that all their tenants’ homes meet our regulatory standards, as well as relevant building regulations and health and safety requirements. This applies to all homes, regardless of whether they were built by a social landlord, acquired from a third-party developer or delivered through a JV.

“When considering arrangements with private developers, social landlords should carry out appropriate due diligence, identify potential risks and carefully assess how they could impact on their financial plans.”

The good news

MJ Gleeson and Springfield Properties disclosed a complete list of the RPs to which they have sold houses. Castles and Coasts Housing Association and Livin Housing bought the small number of social homes MJ Gleeson bulk sold, according to its most recent results, and both are deemed compliant with RSH standards.

Meanwhile, Springfield bulk sold social homes to nine Scottish RPs, all deemed compliant with the Scottish social housing regulator’s requirements, and five local councils. According to the Scottish regulator, tenant satisfaction in most of the RPs and councils to which Springfield sold was below the average, but this could refer to sentiment before Springfield sold to them.

Investors may also consider the partial transparency of Vistry as a bull point. It told us it had sold to more than 90 RPs, albeit it only named the for-profit RPs Sanctuary, Clarion, Home Group, L&Q, Sovereign, Livewest, Midland Heart, Abri and Notting Hill, as well as non-profit RPs Sage and Legal & General. All the RPs it named are compliant with RSH standards.

Finally, there are the deals with large PRS landlords. Most of the bulk sales MJ Gleeson detailed in its most recent results were to private equity giant Carlyle Group. And, while Barratt declined to reveal the names of any of the RPs to which it had sold, it has been open about the 258 homes it sold to Citra Living, a PRS landlord owned by Lloyds Banking Group. Meanwhile, Vistry has been open about its 5,000-home deal with Sigma Capital Group.

The transparency matters for investors because while the sector is banking on a housing market recovery, analysts and commentators have suggested that this may not feed through to housebuilders themselves until around 2025. In the meantime, they will likely be engaging in more bulk sales.

And even after a recovery, companies selling en masse will continue. Vistry’s whole model depends on it, and others could copy that model even in good times. MJ Gleeson chief executive Graham Prothero said earlier this month that investors should distinguish between bulk sales, where housebuilders begrudgingly “bundle up and sell” homes initially planned for private sales in response to a weak market, and partnerships, where housebuilders such as Vistry intentionally partner with RPs, councils, or PRS landlords ahead of construction.

In other words, while bulk sales might fall away, partnership deals are likely to stay, certainly for Vistry and possibly for other housebuilders. Investors should want to know precisely how much revenue depends on those partnerships, and who those partners are.