When Patrick Smitheman, of Harwood Estate Agents, heard that the group of nine artists were staging a unique exhibition at the Footprint Gallery in Jackfield he offered to sponsor the fliers and a reception on the opening evening on May 22.

Broseley-based artist Sam Waters approached Patrick whose offices are nearby.

“There’s a synergy between estate agents and artists, when a new home is found there is an exciting new beginning and space created for artwork,” she said.

“Nine different artists, from print making, paint, mixed media and ceramics to abstract landscapes, florals and statement portraits have come together to hire the Footprint Gallery for two weeks to showcase their work in the Beyond Boundaries Exhibition.

“Each day two artists will be in attendance to welcome visitors, have a chat about art or help visitors to select a piece that they love. Original artwork brings joy and a unique style to people’s homes,” said Sam.

“We are sharing the cost of hiring the gallery and Beyond Boundaries is our first exhibition together at The Footprint gallery which we hope will attract people from a wide area.

“The artists are grateful to Patrick for sponsoring our first event and we are looking forward to our collaboration,” she added.

Patrick said: “Harwood are really pleased to have been asked to play a little part in supporting the exhibition co-ordinated by Sam.”

The exhibition runs from May 22 to June 2, and is open daily from 10am-4pm with free entry. The Footprint Gallery is at Jackfield Tile Museum, Jackfield.

CADILLAC — Surrounded by supporters in front of the foundation of his future home on Huston Street, Robb Vancil was overwhelmed.

“I’m at a loss for words,” said Vancil, who was one of three Cadillac Area Habitat for Humanity partner families who on Monday celebrated the start of construction of their homes.

The other two groundbreaking celebrations were held on South 39 Road, at the future home of Candice Tripp and her family, and on Washington Street, at the future home of Beth Miller and her family.

Cadillac Area Habitat for Humanity Executive Director Amy Gibbs said they’re hoping to have all three homes finished by next spring.

The three partner families will be engaged in a number of Habitat-related activities as a requirement of their partnership.

“The families are ready to engage in our program that consists of classes, sweat equity hours and construction activities leading to acquiring a mortgage and becoming a Habitat homeowner,” Gibbs said.

At the beginning of the year, the organization announced a goal of building more than 30 homes in the Wexford, Missaukee and Osceola region by 2028.

“CAHFH is working hard to eliminate the housing crisis we are in by tripling our production and we could not do what we do without the many partners we have in our community,” reads a press release about this year’s home builds. “Safe and affordable housing is key to every person’s success.”

Barclays’ investment bank stuttered in the first quarter, failing to follow rivals’ sharp dealmaking gains as revenue from fixed income trading tumbled by 21%.

The UK lender, which has been looking to reduce reliance on its investment bank under a strategic shift unveiled in February, brought in revenue of £3.3bn for the unit, which was slightly under market expectations.

Its fixed income trading unit accounted for £1.4bn of that revenue, sliding by 21% for the period. Despite a 25% uptick in equity trading fees, overall global markets revenue at Barclays was down 8%.

Its investment banking fees were up 2% to £617m, a much smaller gain than double digit jumps at rivals. Barclays’ M&A unit was down by 30% for the period, and its leading debt underwriting business gained 18% to £401m, again a smaller rise than many peers.

Wall Street banks saw a rebound in investment banking fees during the first quarter, with equity and debt underwriting pushing large percentage gains at Bank of America, Citigroup, Goldman Sachs, JPMorgan and Morgan Stanley.

European investment banks are likely to see sharper gains as their investment banking businesses are more dominated by debt capital markets work. Deutsche Bank’s origination and advisory business posted a 54% gain during the first quarter, driven by debt underwriting.

While M&A volumes jumped 30% during the first three months of the year, according to data provider Dealogic, fees have yet to return, with most US banks posting declines.

Barclays’ overall revenue of £7bn was slightly ahead of analyst expectations, however, and down by 4% compared with the same period last year. Profit of £1.6bn was also ahead of market consensus.

“We are focused on disciplined execution of the plan that we presented at our investor update on 20 February,” said Barclays chief executive C. S. Venkatakrishnan.

Barclays has been hiring senior dealmakers in Europe and the US as it looks to rebuild after a series of exits. Most recently, it brought in Stephen Pick from UBS as head of its Emea M&A division and Rafael Abati as head of its energy transition dealmaking team in the region.

However, the bank is also cutting costs, with plans to cut £2bn worth of expenses unveiled in a February strategy update. It will cut hundreds of jobs across its investment banking, markets and research division as part of the plans.

Barclays ranks sixth by investment banking fees so far this year, according to Dealogic, with a 3.4% market share.

In its full-year 2023 results in February, Barclays named new leaders of its investment bank. Stephen Dainton was promoted to head of investment bank management, while Adeel Khan was named sole head of its markets unit. Cathal Deasy and Taylor Wright remain in charge of its dealmaking division.

Write to Paul Clarke at paul.clarke@dowjones.com

Angela Rayner purchased a four-bedroom property after she and her husband made almost £200,000 selling their former council houses.

The couple appear to have made around £182,500 after selling two homes they owned in the Stockport area of Greater Manchester in the mid 2010s.

Ms Rayner is facing scrutiny over whether she or Mark Rayner, her husband at the time, paid the right amount of capital gains tax when the two properties were sold.

Despite the couple both selling their homes, Ms Rayner was the sole owner of their new four-bedroom house, bought in 2016.

Ms Rayner sold her council house on Vicarage Road for a gain of £48,500 in March 2015 while Mr Rayner made £134,000, when he sold his in April 2016.

That same month, almost a year after Ms Rayner was elected MP, she purchased a £375,000 property in her new constituency of Ashton-under-Lyne.

The four-bedroom red brick house has three reception rooms, a large secluded garden and two detached garages, according to the Rightmove listing from the time.

The deputy Labour leader sold her house in Vicarage Road for £127,500 in 2015 and, according to official Land Registry documents, bought the property in Ashton-under-Lyme.

On the same day Ms Rayner bought the house, her husband sold his Lowndes Lane home for £145,250, according to Rightmove.

However, despite Mr Rayner being listed on the electoral roll for the property from 2017 along with Ms Rayner and her son Ryan Batty, she is the only proprietor named on official documents. The couple are understood to have separated in 2020.

In 2022, Mr Rayner applied for home rights under the Family Law Act, which prevents one person from being able to sell a house and leave the other homeless.

Greater Manchester Police is investigating whether any offences were committed, and is understood to have spoken to neighbours about Ms Rayner’s living arrangements.

Ms Rayner has repeatedly insisted she has done nothing wrong, but has declined to publish details of her tax affairs. She has said she will “do the right thing and step down” if she is found to have committed a criminal offence.

The Labour Party and Greater Manchester Police have been contacted for comment.

First home buyers have a record market share with close to 26 percent of property purchases. File photo.

Photo: 123RF

Property market conditions are set to favour first home buyers for the forseeable future, according to the latest report from CoreLogic.

The research firm’s regular report into market conditions says first home buyers have held their record market share, with close to 26 percent of property purchases in March, equal to owner-occupiers looking to move on.

Chief property economist Kelvin Davidson said their relative dominance was helped by several factors.

“The most important are access to KiwiSaver for at least part of the deposit, making full use of the low deposit lending allowances at the banks… and of course relatively reduced activity from other buyer groups.”

First home buyers were particularly strong in major city markets, taking 36 percent of Wellington sales, 34 percent in Hamilton and 28 percent in both Auckland and Christchurch.

Davidson said owner-occupiers looking to trade up were being held back by higher costs, including legal and removal fees, as well as a lack of choice in the type of properties they were wanting.

Investors were also being stymied by difficulties in getting bank finance, low rent yields, and – until recently – restrictive tax rules.

Davidson said factors to watch included an expected loosening of loan to value ratios (LVRs) likely to be around the middle of the year when debt to income ratios might come into force, reduced brightline tax rule, and mooted changes to bank lending rules in the Credit Contracts and Consumer Finance Act.

“I think they’re probably a story more for next year, there’s a cocktail of factors… that’s adding up to a view that there will be a boost to the market, but high mortgage rates will still be the key.”

One question would be whether the large number of redundancies looming in the public service might lead to a rise in distressed or mortgagee sales, but Davidson said banks had shown they were flexible in helping borrowers through tough times.

Dallas officials will vote on a 15-year proposal Wednesday in an effort to relocate the WNBA’s Dallas Wings from Arlington to the Dallas Memorial Auditorium, part of Kay Bailey Hutchison Convention Center downtown.

The recently awarded a three-year, nearly $7.7 million contract to a national architecture, engineering and construction management firm for the arena renovation and reconstruction, and city officials anticipate the project could be done as early as 2026.

If the Wings were to relocate to the site, they would have to use the arena at least 70 days a year between April 15 and Nov. 1, according to the proposal before council members on Wednesday. The proposal includes year-round use of the building for training and office space, with the team obtaining a final certificate of occupancy no later than March 1, 2026.

Here’s what to know about the Memorial Auditorium arena:

The oldest structure in the convention center complex downtown

The convention center is a mosaic of structures. Every new building has been part of a city-led effort to expand the complex that stretches from the City Hall to the Cedars neighborhood.

Memorial Auditorium, built in 1957, is the complex’s first and oldest structure. It is near The Black Academy of Arts and Letters, which also is undergoing renovations as part of the larger redevelopment plan.

George Dahl, the Dallas architect responsible for the construction and design of the 26 Art Deco-style buildings in Fair Park, designed the arena.

How many people can the arena host?

The arena has the capacity to hold nearly 10,000 attendees. It was always imagined as a multipurpose space capable of hosting concerts and arena sports matches, among other entertainment events.

In 1973, the auditorium was renamed the convention center arena after the complex had a million square-feet added to it.

The arena has hosted big ticket names such as the Beatles and Led Zeppelin

At its peak, the arena was the stage for acts like Elvis Presley, the Jackson Five, the Beatles and Led Zeppelin.

Between 1967 and 1977, artists like the Doors, Jimi Hendrix, Janis Joplin, Miles Davis, the Rolling Stones, the Who, the Grateful Dead, Black Sabbath, Bruce Springsteen, David Bowie, Billy Joel, Prince, and Fleetwood Mac also performed at the memorial.

The Dallas Chaparrals, a basketball team affiliated to the American Basketball Association were also based in the arena until 1973, and the arena also hosted an appearance by John F. Kennedy during his 1960 presidential campaign.

How will the arena change with the renovations?

Rosa Fleming, director of the city’s convention and event service department, told The Dallas Morning News in February that the arena’s renovation and upgrades will include efforts to make the space compliant with the requirements of the American with Disabilities Act. The renovations could also add more seats to the arena.

Right now, its antiquated design and the lack of accessibility limits the arena’s use to 26 events per year. But the upgrades will allow the space to be used as many as 100 times per year.

How does the arena fit with the larger redevelopment plan

In the last decade, the city has approved projects that could make the area around the convention center more walkable and public-transit friendly.

The city estimated in January 2023 that it would need $2.8 billion to build the new convention center, with a new deck park over Interstate 30 nearby. The city also said it estimated needing more than $386 million to renovate and reconstruct the arena and The Black Academy of Arts and Letters, both of which which are attached to the current convention center.

The convention center’s expansion and the deck park will open the Cedars neighborhood and Old City Park to Farmers Market, and city officials see it as a way of amping up the revitalization efforts in neighborhoods split by I-30.

- Strong start to 2024

- But margins expected to dip this year

Elixirr International (ELIX) has reported double-digit growth, and momentum is set to continue into 2024. Revenue at the Aim-traded consultancy increased by a fifth in 2023 to £85.9mn, and adjusted Ebitda jumped by 24 per cent to £25.4mn.

Organic revenue growth was strong at 15 per cent, and this was evenly spread between existing clients and new ones. Acquisitions were responsible for the remaining progress, with Elixirr branching out from strategy consulting into areas such as artificial intelligence and data analytics.

Revenue per partner has increased by 7 per cent to £3.9mn and Elixirr managed to poach three new partners last year, suggesting its reputation in the industry is strong – despite plenty of competition.

Market conditions remain “challenging”, with UK banking clients proving particularly troublesome, according to chief executive and founder Stephen Newton. However, the group has diversified in recent years, meaning it is less exposed to the fortunes of the financial services sector.

This seems to be paying off. The group achieved record sales in the first quarter of 2024, and revenue for the full year is expected to reach £104mn-£110mn. Adjusted Ebitda margins are due to dip from 30 per cent to 27-29 per cent as a result of a recent acquisition, but this still implies profit growth of at least 11 per cent.

Much will depend on how Elixirr’s acquisition strategy plays out, and investors don’t have much to go on in terms of track record. For now, however, this ‘challenger’ consultancy is thriving in a difficult market for the biggest players. Buy.

Last IC View: Buy, 590p, 18 Sep 2023

| ELIXIRR INTERNATIONAL (ELIX) | ||||

| ORD PRICE: | 585p | MARKET VALUE: | £277mn | |

| TOUCH: | 580-590p | 12-MONTH HIGH: | 665p | LOW: 402p |

| DIVIDEND YIELD: | 2.5% | PE RATIO: | 16 | |

| NET ASSET VALUE: | 253p* | NET CASH: | £12.8mn | |

| Year to 31 Dec | Turnover (£mn) | Pre-tax profit (£mn) | Earnings per share (p) | Dividend per share (p) |

| 2019 | 24.5 | 1.73 | 3.18 | nil |

| 2020 | 30.3 | 5.82 | 11.7 | 2.20 |

| 2021 | 50.6 | 12.2 | 22.0 | 4.10 |

| 2022 (restated) | 71.7 | 15.7 | 27.9 | 10.8 |

| 2023 | 85.9 | 22.1 | 37.5 | 14.8 |

| % change | +20 | +40 | +35 | +37 |

| Ex-div: | tbc | |||

| Payment: | Aug 2024 | |||

| *includes intangible assets of £101mn, or 213p a share | ||||

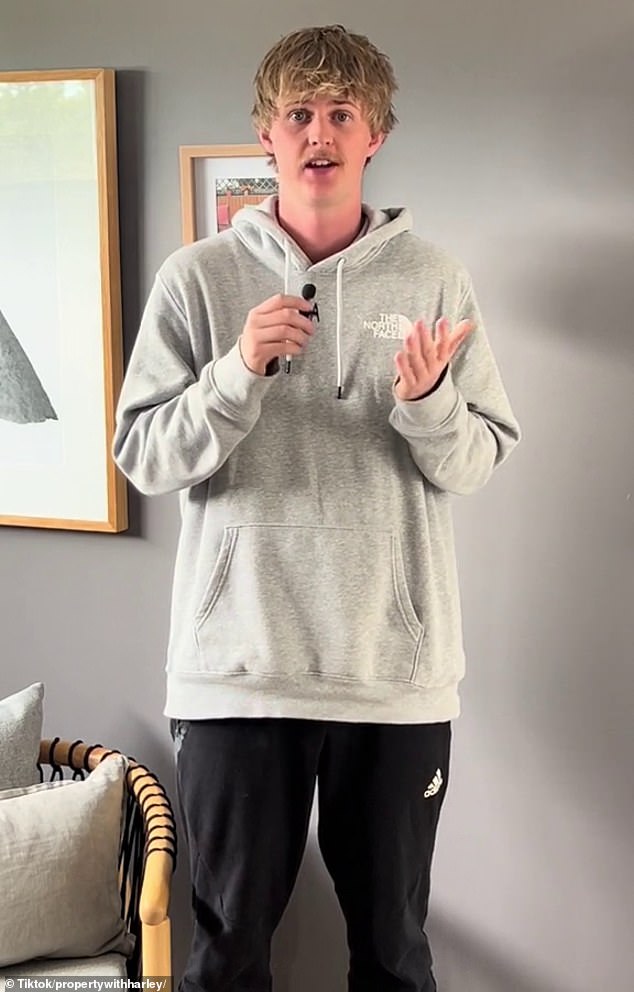

A Gen-Z property investor who owns three properties has shut down claims landlords are at fault for Australia’s current rental crisis.

Harley Giddings, 24, has worked hard since adolescence and in every job ‘under the sun’ to own a house and is now the proud owner of multiple investment properties.

The young investor posted a TikTok to his thousands of followers saying he often gets comments ‘all the time’ that blame investors for the housing shortage.

The savvy landlord said he can understand Aussies’ frustrations but thinks this is ‘misguided’, firmly believing the sky-rocketing rents and housing shortage lie with high immigration and low building approvals.

‘In 2022 and 2023 the government let in over a million migrants into the country,’ he said.

Harley Giddings, 24, has a property portfolio consisting of three investment properties. He understands people are ‘hurting’ but believes Aussies are ‘misguided’ when blaming landlords for the rental crisis

‘Basic supply and demand’ is the reason for the Australian housing crisis, according to the 24-year-old

‘According the Australian Bureau of Statistics, this is the most amount of migrants Australia has ever let into the country since they started recording.

‘These one million migrants were let in at a time when Australia already had a housing crisis.’

Mr Giddings said that when people arrive in Australia they are looking at renting and not buying, which is why so many people are at inspections for rental opens.

‘Basic supply and demand,’ he said.

The second reason the young property investor gave for the housing shortage in Australia was the low amount of homes being built.

‘We are simply not building enough properties,’ he said.

‘In Victoria, my home state, we currently have the lowest amount of building approvals that we’ve had in the last decade.

‘This issue is Australia-wide.’

The 24-year-old quoted research from the Institute of Public Affairs that by 2028 Australia’s housing supply will be short by 252,800 homes.

Many Australians agreed with the young investor, also blaming the government.

‘Absolute master stroke by the government,’ one wrote.

‘Not to mention all of Victoria’s new tax laws on investments, landlords are getting rid of them,’ one said.

‘If you can’t keep up with supply reduce the demand,’ another wrote.

Mr Giddings said the the low number of houses being built in Australia is a major reason for rents increasing so high (pictured people at an auction)

However, other Aussies were quick to throw blame back at the investor.

‘You are also the problem. You cannot just blame building and immigration. You know why people can’t afford to build? Because they can’t afford the increased prices driven up by decades of investors,’ one wrote.

‘Investors and immigration: two problems [that] need to be stopped,’ another said.

Mr Giddings told Yahoo he understands it would be very hard at the moment to be a renter and there’s a lot of ‘hurt’ due to prices increasing not just in rent, but everything else as well.

‘I just think there’s a couple of factors that is like worsening the housing crisis that isn’t caused by renters or landlords,’ he said.

The investor, who became interested in property after reading multiple books and listening to podcasts about investing, made it clear to Yahoo that he did not blame the people moving to Australia, but government policy.

Mr Giddings dropped out of university half-way through his business degree because he didn’t think it would offer him much.

The 24-year-old instead worked two jobs, seven days a week, saving more than $100,000 by age 22.

Mr Giddings, who describes his family as middle class, went halves with his dad for his first property, as told by Yahoo.

The young investor believes high rents and a competitive market has been created by the government allowing one million migrants into the country in the middle of a housing crisis

‘My parents aren’t really the kind of investment-savvy people. Like, dad’s a firefighter, mum’s a hairdresser. So he had the borrowing power because he was working full time and I had the savings,’ he said.

The hard-worker, who has always been interested in investing, purchased away from his state of Victoria and instead invested in Western Australia.

‘There’s 15,000 suburbs in Australia, it’s highly unlikely that the area you live in is going to be one of the best performing,’ he said.

The first property cost the father and son $450,000 and then the 24-year-old used more savings to buy a second property.

Mr Giddings used the equity built up in the second property to purchase his third investment.

This impressive property portfolio was achieved by the time he was just 23.

According to the Australia Tax Office, most landlords are ‘mum and dad’ investors, with a massive 71 per cent of landlords in Australia owning just one investment property.

Only 19 per cent own two properties.

According to the Australian Bureau of Statistics work begun in 2023 on just 163,836 new houses, which is the lowest amount since 2012.

Compounding the issue is a 90,000 tradie shortage, who are needed in the next three months so the government’s housing plan can stay on deadline.

Arrests in property fraud scheme

Orenthanal James Bennett and Victoria Strickler are accused of targeting the homes of people who had died or were suffering from health issues, transferring the deeds for three Bay Area homes out of the legal owners’ names.

TAMPA, Fla. – The FDLE busted a multi-year property fraud scheme across Hillsborough and Pasco Counties.

Investigators arrested Orenthanal James Bennett and Victoria Strickler, charging them both with organized scheme to defraud over $50,000.

Investigators say the fraudsters targeted the homes of people who had died or were suffering from health issues.

The FDLE accuses Bennett of transferring the deeds for two homes in Pasco County and one home in Hillsborough County out of the legal owners’ names.

According to investigators, the owners of two of the homes had died several years prior, and the owners of the third home were suffering from dementia-related health issues.

READ: Florida Legislature considering crackdown on title fraud

“When this does happen, you don’t really know about it until, maybe there’s a knock on your door and someone says, ‘This is my property. What are you doing here?’” Pasco County Clerk Nikki Alvarez-Sowles said.

Pasco County officials say vulnerable people and properties are some of the most common targets of property fraud.

READ: Property deed fraud growing problem in Florida; state offers assistance in detection

“And you wouldn’t even know it because people are recording things in the official record on a property, and it would change the title ownership from the owner into usually a company name,” Alvarez-Sowles said. “It could be also an individual name. Could be fictitious. And they do it, maybe a couple of times. And then, at the point in time, they sell the property to an unknowing buyer.”

In this case, investigators say once Bennett transferred the deeds out of the legal owners’ names, he allegedly transferred the deeds through multiple different entities that he was associated with, before selling them.

According to an affidavit, the properties were sold for a total of nearly $250,000.

After the homes were sold, the investigators say Bennett signed the deeds, and Strickler, who’s a title agent, notarized them.

Orenthanal James Bennett and Victoria Strickler mugshots.

“The only deeds that I believe my client was involved in were transactions between the other individual, the other gentleman, or entities that he was involved with and her,” Bjorn Brunvand, Strickler’s attorney said. “So, the deeds leading up to that, my client had no involvement in.”

Strickler’s attorney says she has had professional transactions with Bennett in the past, but there was no conspiracy in this case.

READ: Gov. DeSantis signs bill that cracks down on squatters in Florida: ‘The squatter scam ends today’

“That is a person that she has had business transactions with and in the past, in her professional capacity,” Brunvand said. “So, yes, there’s been transactions with that person, but there has been no conspiracy. There has been no agreement to violate the law. And, if there was any criminal conduct in any way connected to my client, she was unaware of it.”

Brunvand says she’s cooperated with law enforcement throughout years of investigation.

Attorney General Ashley Moody’s office is investigating the case.

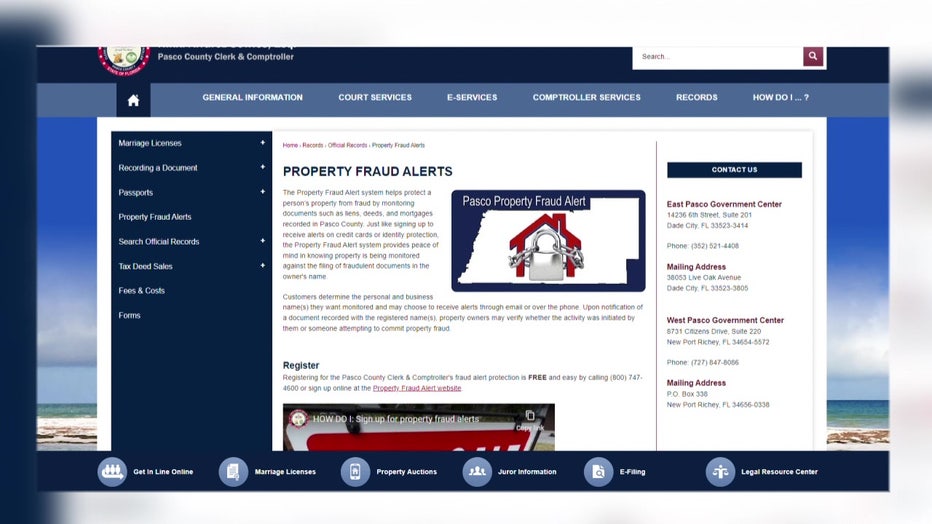

Pasco County officials say property fraud is an issue around the state.

Nearly every county in Florida has a fraud alert system, where property owners can sign up to get alerts any time some documents are filed with their information.

“So, when a document gets recorded in our official record, it will hit off of the name that you put into the search term,” Alvarez-Sowles said.

She says this alert system is designed to help people get the information as soon as people and keep property fraud from happening.

“I would get a notification emailed to me with a link to the document,” Alvarez-Sowles said. “I can go look at the document. I can tell right then if I initiated that or if it’s fraudulent.”

Click here for more information about how to sign up for property fraud alerts in Pasco County.

Click here for information about signing up for property fraud in your county.

Margaret Josephs has a new renovation project in the works.

Earlier in April, The Real Housewives of New Jersey cast member revealed via her Instagram that she’s restoring her giant “Tudor front door” in a project that will take three weeks.

Margaret Josephs reveals her latest renovation project

“I didn’t think she looked bad for 118 years young but you guys obviously did!” Margaret captioned a video post where she revealed the project timeline for the incredible historical piece.

“Thankfully [ZK Painting] is going to give her a full makeover!” she said of the professional painter and refinished she hired to do the job.

Here’s What You May Have Missed on Bravo:

Melissa Gorga Reveals if Her Fallout with Jackie Goldschneider Has to Do with Teresa Giudice

Teresa Giudice Addresses Rumors She and Luis Ruelas Are Getting a Divorce: “Are You Serious?”

Where Do Dolores Catania and Margaret Josephs Stand Today? Here’s What They Just Revealed

“It is finally time for the Tudor club door to be refinished and be restored to the love and the original state it was once in,” Margaret said in the video as professionals took the door of its hinges to be taken away for restoration.

The New Jersey resident also noted she’s had the door “repainted a few times,” but “it cracks” from exposure to the sun and elements. She also shared that Kenney’s company is doing a “high gloss” on the door to give it that extra special sheen.

In a more recent Instagram Story, Margaret shared a reel of the door getting stripped and refinished via ZK Painting, “If [you’re] wondering the progress of the front door!!” Margaret wrote over the reel, highlighting the intricacy of the process. “Rome was not built in [a] day!”

The reel in question, shared by ZK Painting’s Instagram page, showed the process of stripping the stains and paint detailed what went into the project.

“Looks like this massive door for [Margaret] was originally stained and clear coated,” the account captioned the video. “After we chemically stripped all the old layers of paint we used 60 grit sand paper and a hard pad to sand off the remaining stain and clearcoat. This reveals a fresh layer of wood and to makes everything flat in preparation for the piano black high gloss treatment this door will receive!

They concluded the caption by noting what comes next: “This was the easy part. Next we hand sand all the moldings!”

Press play on the video above to tour Margaret’s New Jersey home and watch The Real Housewives of New Jersey on Peacock and the Bravo app.