Commenting on the figures, Robert Gardner, Nationwide’s chief economist, said: “Activity has picked up from the weak levels prevailing towards the end of 2023 but remain relatively subdued by historic standards.

“For example, the number of mortgages approved for house purchase in January was around 15% below pre-pandemic levels. This largely reflects the impact of higher interest rates on affordability. While mortgage rates are below the peaks seen in mid-2023, they remain well above the lows prevailing in the wake of the pandemic.

“With cost-of-living pressures easing as inflation moves back towards target, consumer sentiment is improving. Indeed, surveyors report a pickup in new buyer enquiries and new instructions to sell in recent months. Moreover, with income growth continuing to outpace house price growth by a healthy margin, housing affordability is improving, albeit gradually.

“If these trends are maintained, activity is likely to gain momentum, though the pace of the recovery is still likely to be heavily influenced by the trajectory of interest rates.

Karen Noye, mortgage expert at wealth manager Quilter said this annual increase should serve as a serious wake up call to Government, highlighting the real-world impact of repeatedly missing house-building targets.

She added: “Given the lack of demand due to the cost-of-living crisis, house prices should have decreased but because there is such little housing stock, prices continue on an upward course.

“As interest rates are set to decrease again and demand expected to pick up during spring, this small monthly dip in prices is likely to represent a blip rather than a trend.

“House price inflation has often been positioned as a good news story but younger generations are now facing such an uphill battle to get anything like enough money together for a deposit a further increase will be worrying. Wage growth simply fails to keep up with house price growth and there is a real worry that there will eventually be a generation that enters into retirement needing to have enough in their pension to pay for their living expenses but also for rental costs. This represents a tall order.”

Amy Reynolds, head of sales at Richmond estate agency Antony Roberts, said: “The persistent supply/demand imbalance, which is particularly evident across London, along with better mortgage rates since the turn of the year, are supporting overall market strength and stability.

“In line with what we are seeing on the ground, Nationwide’s latest house price index points to an upwards trajectory in property prices.

“The sales market continues to pick up some momentum with committed buyers and a strong pipeline of serious applicants boding well for the spring market.”

Nathan Emerson, chief executive of agency trade body Propertymark, added: “Sellers have every reason to start feeling positive about putting their home up for sale and being able to go on to buy their next perfect property. 2024 has shown a positive trend that house prices are growing once again following three years of economic turbulence.

“However the UK Government must look to make houses equally affordable for buyers and that can only be done by building more houses. Propertymark’s own Housing Insight Report found there has been an 80% increase in the number of new properties becoming available, ultimately making it easier for people to consider a move.”

House prices are just 3% below the all-time highs recorded in the summer of 2022 after they rose for first time in over a year during February, data from Nationwide has revealed.

UK house prices rose 0.7% month on month during February taking the annual rate of house price growth to 1.2% from -0.2% the previous month.

UPTICK

Robert Gardner, Nationwide‘s Chief Economist, says: “The decline in borrowing costs around the turn of the year appears to have prompted an uptick in the housing market.

Robert Gardner, Nationwide

“Indeed, industry data sources point to a noticeable increase in mortgage applications at the start of the year, while surveyors also reported a rise in new buyer enquiries.”

But he warns: “Near-term prospects remain highly uncertain, in part due to ongoing uncertainty about the future path of interest rates. After falling sharply in late December, swap rates, which underpin fixed rate mortgage pricing, have drifted back up.

“Borrowing costs remain well below the highs recorded last summer but, if the recent upward trend is sustained, it threatens to restrain the pace of any housing market recovery.”

WELCOMED

Nevertheless agents welcomed the news.

Iain McKenzie, The Guild of Property Professionals

Iain McKenzie, Chief Executive of The Guild of Property Professionals, says: “We’re expecting to see the house market back on the march this year, and a return to positive annual price growth is another good sign.

“Growth will be welcomed by sellers that have been cautious to stick out the ‘for sale’ signs since prices began to ease.”

And he adds: “This resurgence in activity is a promising sign that should bring more buyers out of hiding and encourage growth in the sector. We are already seeing this play out, with HMRC also recording an uptick in sales at the start of the year.”

CONFIDENT

Matt Thompson, Chestertons’ Head of Sales, says: “Buyers have become increasingly confident since the end of last year when interest rates were held at 5.25% and mortgage rates started to come down.

Matt Thompson, Chestertons

“This sentiment carried through to January and February 2024. Meanwhile, sellers have also been feeling more optimistic about attracting the right buyer for their home which has led to a slight increase in the number of properties being put up for sale.”

Tom Bill, Head of UK residential research at Knight Frank, adds: “Buyers feel confident that the only way for the base rate is down, which has seen demand and house prices pick up in recent months.

Tom Bill, Knight Frank

“The upwards pressure on mortgage rates in recent weeks shows sellers the importance of getting the asking price right.

“Banks are keen to lend and should eventually lower rates this year as inflation comes under control, which we believe will sustain positive annual growth in 2024 and see UK house prices increase by 3%.”

UPWARDS

Amy Reynolds, Head of Sales at Richmond-based Antony Roberts, adds: “In line with the bustling activity we are seeing on the ground, Nationwide’s latest house price index underscores the upwards trajectory in property prices.

“It is an opportune time for buyers and sellers to seize the moment. We’ve seen an uptick in applicants with sizeable budgets seeking to upsize to their forever homes, as well as first-time buyers and second steppers wanting flats with outside space.”

Jeremy Leaf

Jeremy Leaf, north London estate agent and a former RICS residential chairman, says: “In our offices, more valuations, listings and viewings combined with fewer fall-throughs than this time last year are feeding through to agreed sales, mortgage approvals and exchanges.”

But he cautions: “While Nationwide reports another rise in prices, the market does remain price sensitive. Only competitively-priced properties are attracting attention. Sellers must price realistically or offers won’t be forthcoming and market improvement may not be sustained.”

Nathan Emerson, Propertymark

And Nathan Emerson, Chief Executive of Propertymark, says: “The housing market always reacts to changing economic trends, so it is encouraging to witness many homeowners seeing both a month on month and year on year uplift on the price of their homes.

“This should help provide people with the confidence to potentially sell where they may have been holding back. The UK Government need to build on this as a chance to prove that the economy is heading in the right direction.”

MORTGAGE BROKERS

Mortgage brokers welcomed the news too.

Mark Harris, SPF Private Clients

Mark Harris, Chief Executive of SPF Private Clients, says: “With a growing feeling that base rate has peaked, and the next move in rates will be downwards, this is supporting buyer and seller confidence and boosting activity in the market.

“Mortgage rates are more attractively-priced than they were several months ago, even if the ‘best buy’ deals have been pulled recently.

“There will be ups and downs in mortgage pricing in the weeks and months ahead but there is a growing feeling of optimism that the situation is improving, which will be welcomed by hard-pressed borrowers.”

Riz Malik, R3 Mortgages

And Riz Malik, Founder & Director at Southend-on-Sea-based R3 Mortgages, told Newspage: “The UK housing market is poised in the starting blocks waiting for the starter pistol.

“This could either be an announcement in the upcoming Budget or the first cut in the base rate.

“That first cut in the base rate, when it comes, will see the property market spring out of the blocks.”

House prices are now around 3% below the all-time highs recorded in the summer of 2022 at £260,420, Nationwide said.

Commenting on the figures, Robert Gardner, Nationwide’s chief economist, said: “The decline in borrowing costs around the turn of the year appears to have prompted an uptick in the housing market.

“Indeed, industry data sources point to a noticeable increase in mortgage applications at the start of the year, while surveyors also reported a rise in new buyer enquiries.”

However, Gardner cautioned that near-term prospects remain highly uncertain, in part due to ongoing uncertainty about the future path of interest rates.

He added: “After falling sharply in late December, swap rates, which underpin fixed rate mortgage pricing, have drifted back up.

“Borrowing costs remain well below the highs recorded last summer but, if the recent upward trend is sustained, it threatens to restrain the pace of any housing market recovery.

“While the squeeze on household budgets is easing, with wage growth now outstripping inflation by a healthy margin, it will take time to make up for the ground lost over the past few years, especially given consumer confidence remains fragile.”

Nicky Stevenson, managing director at national estate agent group Fine & Country, suggested positive signs for the property market are turning from a trickle to a flood this year.

She said: “Demand is building as lower mortgage rates have encouraged buyers to restart their property search, and plunging inflation suggests better news is to come.

“Some buyers, assuming that we are at the peak of the rate rise cycle, are still waiting in the wings for the first downward nudge in interest rates before they return to the market. But this means there is a lot of pent-up demand that could soon be unleashed.

“We’re heading into one of the prime seasons for home sales, and sellers should look at this as a great time to get their home on the market.

“Properties tend to sell fastest at this time of year, and motivated buyers are still snapping up homes in desirable areas.”

Nathan Emerson, chief executive of Propertymark, added: “The housing market always reacts to changing economic trends, so it is encouraging to witness many homeowners seeing both a month on month and year on year uplift on the price of their homes.

“This should help provide people with the confidence to potentially sell where they may have been holding back. The UK Government need to build on this as a chance to prove that the economy is heading in the right direction.”

UK house prices returned to growth for the first time in more than a year as mortgage rates eased, according to Nationwide.

Property values increased by 0.7% between January and February, making the average home worth £260,420. Annually, house prices increased by 1.2% in February, following a 0.2% fall in January.

It marked the first month since January 2023 that Nationwide recorded positive annual growth in house prices.

Nationwide’s chief economist Robert Gardner said: “House prices are now around 3% below the all-time highs recorded in the summer of 2022, after taking account of seasonal effects. The decline in borrowing costs around the turn of the year appears to have prompted an uptick in the housing market.”

Read more: 7 homes with links to famous literary figures

Earlier this week, the Bank of England said that the number of mortgage approvals made to home buyers jumped to the highest level since October 2022 in January this year.

HM Revenue and Customs (HMRC) figures showed this week that 82,000 home sales took place in January, which was 12% lower than January 2023 and 2% higher than December 2023.

However, Quilter’s mortgage expert Karen Noye highlights, some lenders have recently been raising their mortgage costs. She also points out that some lenders, including Nationwide, have recently been raising their mortgage rates.

“Lower mortgage rates at the start of the year appear to have spurred some buyers back to the market which has buoyed prices, but more recently we have seen a further uptick in rates as swap rates have risen so this could be relatively short lived,” she said.

“Just last week, lenders including Nationwide, NatWest, Santander and HSBC all made the decision to increase their rates,” she added.

Gardner also warned that uncertainty about the future of interest rates could yet derail price rises. “Borrowing costs remain well below the highs recorded last summer but, if the recent upward trend is sustained, it threatens to restrain the pace of any housing market recovery,” he said.

Read more: Best UK mortgage deals of the week

Tom Bill, head of UK residential research at Knight Frank, predicts average house prices will rise by 3% this year, as interest rates are cut. “Banks are keen to lend and should eventually lower rates this year as inflation comes under control, which we believe will sustain positive annual growth in 2024 and see UK house prices increase by 3%,” he said.

Watch: Nationwide Becomes The Latest Mortgage Lender To Up Home Loan Costs

Download the Yahoo Finance app, available for Apple and Android.

(Bloomberg) — UK house prices rose more than forecast this month as cheaper borrowing costs extended the property-market recovery into 2024, according to one of the country’s biggest mortgage lenders.

Most Read from Bloomberg

Nationwide Building Society said the average price of a home rose 0.7% in January to £257,656 ($326,550), beating the 0.1% gain expected by economists. It left prices just 0.2% lower than a year earlier, the strongest reading in 12 months.

“There have been some encouraging signs for potential buyers recently with mortgage rates continuing to trend down,” said Robert Gardner, chief economist at Nationwide. “This follows a shift in view amongst investors around the future path of Bank Rate, with investors becoming more optimistic that the Bank of England will lower rates in the years ahead.”

“While a rapid rebound in activity or house prices in 2024 appears unlikely, the outlook is looking a little more positive.”

The findings add to evidence that the housing market will stabilize this year, after avoiding a widely-anticipated crash last year. Nationwide is predicting a modest decline in prices in 2024, though others see a small rise.

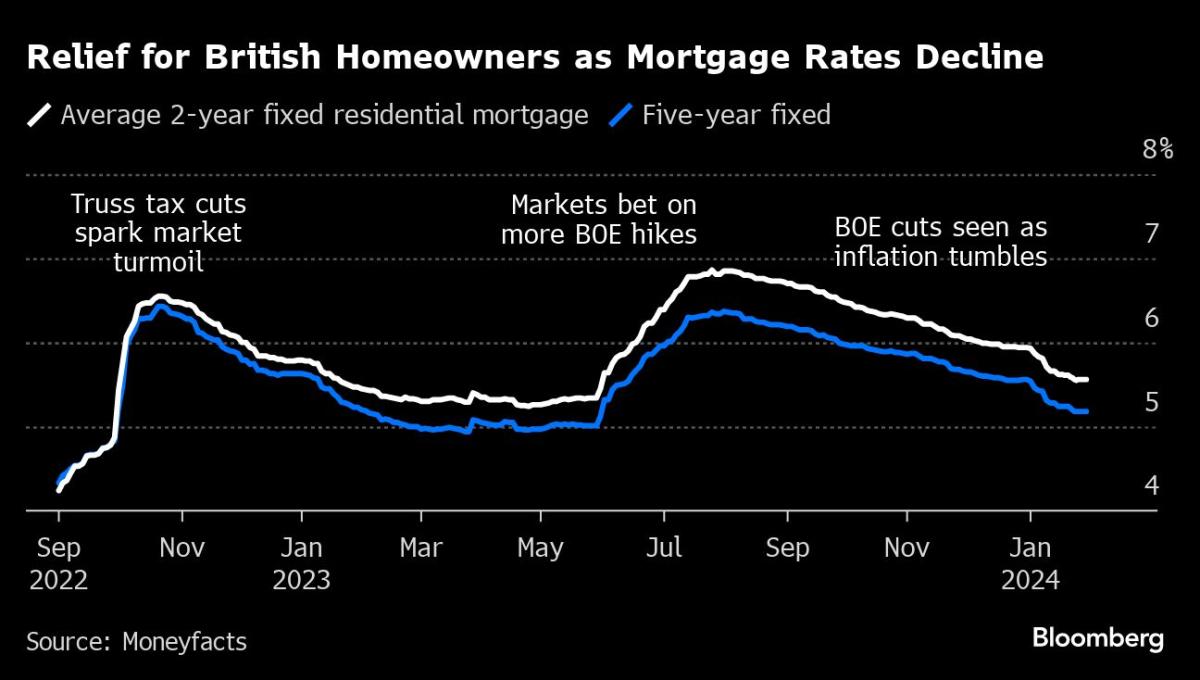

According to Moneyfacts, the average 2-year fixed mortgage rate has fallen to 5.18%, down from almost 7% last summer. The BOE is expected to begin cutting its key rate by the summer and may signal a pivot at its meeting on Thursday.

“The reported month-on-month increase in house prices will start to encourage homeowners to feel more confident that they can potentially make their next move,” said Nathan Emerson, CEO of Propertymark. “If the Bank of England decide to bring down interest rates too, this should give sellers even more confidence and ease the pressure on affordability. Hopefully this is the start of a period of economic recovery for the nation.”

However, Gardner noted that the interest-rate outlook remains “uncertain,” with traders scaling back bets in recent weeks on how far the BOE will cut rates after stronger-than-expected inflation data.

“How mortgage rates evolve will be crucial, as affordability pressures were the key factor holding back housing market activity in 2023,” he said. “Indeed, at the end of 2023, a borrower earning the average UK income and buying a typical first-time buyer property with a 20% deposit had a monthly mortgage payment equivalent to 38% of take-home pay – well above the long run average of 30%.”

Affordability pressures are greatest in London, where the average income of first-time buyers is 55% higher than the average income for adult full-time workers. In the South East and East of England, the next least affordable regions, first-time buyers typically earn 25% more than the average worker.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.