House prices continued to fall in February, but private rents hit their highest level on record, the latest readings from the ONS have found.

UK house prices fell by the least in eight months when the figure edged down by 0.2 per cent on an annual basis in February, against a 1.3 per cent decline in the previous month.

The average price of a property during the month cost £281k, the UK Statistics Authority said on Wednesday.

London was the English region with the lowest annual inflation, where prices decreased by 4.8 per cent in the 12 months to February 2024.

Between January and February, UK transactions increased by 1.2 per cent on a seasonally adjusted basis.

Iain McKenzie, chief of The Guild of Property Professionals, said: “Sellers will be delighted by another month of modest house price growth and this trend could continue as we move through the busy spring and summer months.

“A return to annual growth is now within reach after a difficult year for homeowners in 2023, many of whom may have felt that they had missed a window of opportunity to sell their property.”

He added: “Buyers may not be as excited about the prospect of house prices increasing, but it should be reassuring to know that any purchases made now are unlikely to lose value immediately after they exchange.”

Other groups which measure house prices have also shown a recovery, despite mortgage rates ticking back up.

A recent report by lender Nationwide said house prices grew in March at their fastest rate since December 2022.

Anthony Codling, managing director at RBC Capital Markets, said: “When we consider all the other economic moving parts and political machinations house prices continue to display a high level of stability and seem to be able to weather any storm thrown at them.

“This stability should encourage more people to move home and with wages currently rising faster than inflation, homebuyers may find they have a bigger budget than they thought.”

Rents remain a headache (and London is the worst)

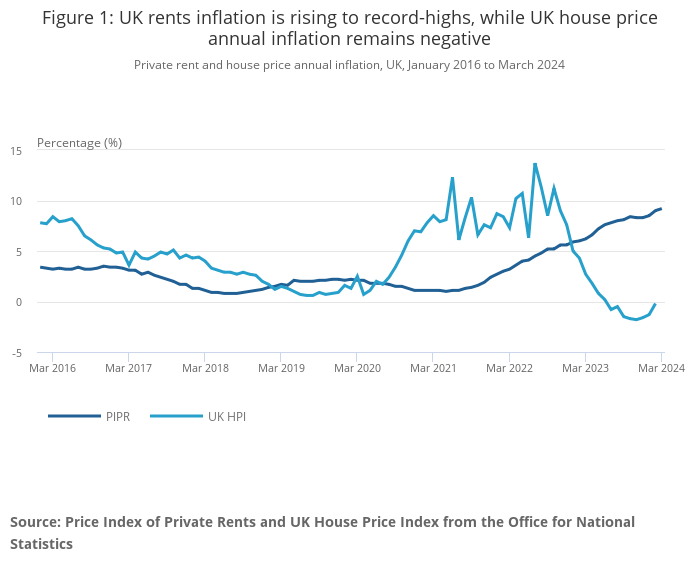

Meanwhile, rental costs in the UK continued to grow with average rents rising 9.2 per cent in March – the highest level since data collection began in 2015.

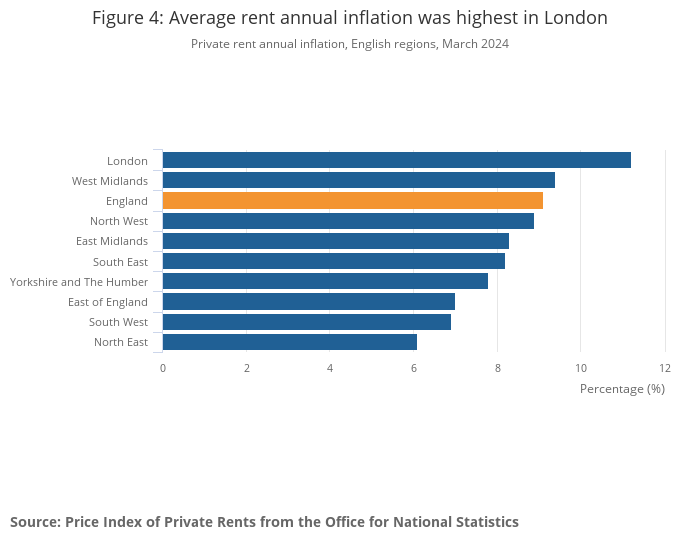

London was the English region with the highest annual rents inflation in the 12 months to March 2024, at 11.2 per cent, which was up from 10.6% in February 2024.

Rebecca Florisson, principal analyst at the Work Foundation at Lancaster University, said: “Inflation might be falling, but those in the private rented sector are in the midst of a cost of renting crisis.”

“The record 9.2 per cent rise on the year is bad news for all renters, who are seeing rents outpace average wage rises of six per cent.”

She added: However, it is particularly challenging for the 1.4 million private renters in severely insecure employment – such as those on zero-hour contracts or in temporary work – who face insecurity at work and at home. This particularly affects severely insecure workers from Black and Asian backgrounds and workers aged 25 to 34.”

“Private renters already spend a higher percentage of their monthly earnings on housing than those in all other forms of accommodation. And insecure workers are particularly vulnerable to the rising cost of rents as they earn on average £3,276 less than those in secure jobs.”

UK house prices slipped for the first time in six months in March, lender Halifax said in data that confirmed a setback in the property market’s recovery.

Halifax said that the average house price dropped 1% to £288,430 last month. That followed a 0.3% gain in the month of February and small increases in each of the previous four months.

Unlock exclusive access to the story of India’s general elections, only on the HT App. Download Now!

It chimes with an unexpected slide in prices in Nationwide Building Society’s measure earlier this week, which economists interpreted as an interruption in the overall trend toward little change or mild gains in the market this year until the Bank of England cuts interest rates. From a year ago, Halifax said prices have risen 0.3%.

“The direction of travel for the property market is currently sideways,” said Tom Bill, head of UK residential research at Knight Frank. “Once a rate cut appears firmly on the horizon and more mortgage rates start with a 3, we expect stronger demand to push UK prices 3% higher this year.”

Other indicators have pointed to continued growth for property prices, with demand improving from buyers and sellers also putting more places up for sale. The market is responding to a dip in mortgage costs and the expectation that interest rates will fall later this year. Mortgage approvals surged to the highest level in 17 months in February.

“That a monthly fall should occur following five consecutive months of growth is not entirely unexpected particularly in view of the reset the market has been going through since interest rates began to rise sharply in 2022,” Kim Kinnaird, director of Halifax Mortgages, said in a report Friday. “Despite this house prices have shown surprising resilience in the face of significantly higher borrowing costs.”

Earlier on Friday, the property website Rightmove said that last Thursday was its biggest day for new sellers coming onto the market this year.

While mortgage rates have cooled from the 15-year high hit last summer, borrowing costs have crept up again in recent weeks.

The average two-year fixed mortgage rate has climbed to 5.81%, up from 5.55% in late January, according to Moneyfacts. However, it is still well below the highs of almost 6.9% seen last summer as the BOE edges toward cutting interest rates.

Prices were largely stagnant in London, up 0.4% compared to a year ago, while Northern Ireland was the strongest performing region with 4.3% growth. Halifax said there was a “north/south divide” in English house prices with the North West enjoying a 3.7% jump year-on-year.

Markets expect the central bank to begin loosening policy in August, with three cuts almost fully priced in by the end of the year.

“Affordability constraints continue to be a challenge for prospective buyers, while existing homeowners on cheaper fixed-term deals are yet to feel the full effect of higher interest rates,” Kinnaird said. “This means the housing market is still to fully adjust, with sellers likely to be pricing their properties accordingly.”

She also said that financial markets have become less optimistic about the scale and timing of BOE rate cuts, which has halted a drop in mortgage rates that benefited the property market in the past few months.

This article was generated from an automated news agency feed without modifications to text.

Discover the complete story of India’s general elections on our exclusive Elections Product! Access all the content absolutely free on the HT App. Download now! Get Latest World News along with Latest News from India at Hindustan Times.

FTSE 100 seen 1.2% lower after US markets slide, crude oil above $90

07:19 , Graeme Evans

London’s FTSE 100 index is set to fall by about 1.2% after Wall Street shares last night slumped on fears that US interest rates will stay elevated for longer.

The sight of Brent Crude above $90 a barrel contributed to the worries that persistent inflation pressures will delay the hoped-for summer cut in rates.

The Dow Jones Industrial Average fell 1.4% and the S&P 500 index by 1.2%, leaving US markets on course for their worst week since October. The VIX index of volatility also jumped to a five-month high.

IG Index is reporting that futures markets expect the FTSE 100 index to decline by almost 100 points to 7878. The top flight yesterday finished within sight of a record high, having risen 0.5%.

The selling comes ahead of today’s release of US non-farm payrolls, which will offer fresh clues about the interest rate outlook.

Deutsche Bank economists are forecasting growth in payrolls of 200,000, which compares with the previous month’s reading of 275,000. The unemployment rate is seen ticking down a tenth to 3.8%.

Halifax: UK house prices slip in March, but up from last year

07:09 , Daniel O’Boyle

UK house prices declined y 1% during March, but are still slightly up year-on-year, according to Halifax.

The latest Halifax House Price Index showed the average price was £288,430. That’s down 1% from February but up 0.3% from last March.

In London, prices grew slightly faster year-on-year, by 0.4% to £539,917.

Kim Kinnaird, Director, Halifax Mortgages, said: ““That a monthly fall should occur following five consecutive months of growth is not entirely unexpected, particularly in view of the reset the market has been going through since interest rates began to rise sharply in 2022. Despite this house prices have shown surprising resilience in the face of significantly higher borrowing costs.”

Recap: Yesterday’s top stories

06:36 , Simon Hunt

Good morning from the Standard City desk.

For the unfashionable over-50 crowd who like Superdry clobber the idea that it might disappear altogether seems more than a shame.

No one is mistaking me for a clothes horse, but it does nice fitting chinos and jackets that are smart enough to work anywhere.

When Superdry floated on the stock market in 2010 at 500p it was valued at £395 million, it had no debt, and co-founder Julian Dunkerton banked £80 million and had stock then worth another £130 million.

Since the stock is now about 10p and the company is worth £10 million that valuation now looks absurd.This never was Dunkerton’s fault – he hired bankers to get him a price, that’s the one they got. Then he handed over to other management, who vastly exaggerated the possibilities Superdry had of becoming some sort of global lifestyle brand. (The price point is different, but see also: Aston Martin.)

The pity about brands like Superdry is that they are stuck in the squeezed middle.

At the cheap end, Primark soars. At the top end, Burberry does well.

In the middle, Superdry, Ted Baker and the rest have a really rough game to play.

Their best bet is to be bought out by (shudders) Sports Direct, now Frasers Group, with the kit downgraded and sold for cheap.

~

Here’s a summary of our top headlines from yesterday:

-

Co-op shows faith in mutual model with target for 8 million members by 2030 as the total passes 5 million, amid a doubling in the number of sign-ups.

-

Bet365 fined £582,000 – less than a day’s pay for CEO Denise Coates – after gambling watchdog found insufficient player protection and money laundering checks

-

Country Life publisher Future says its revenue is growing again, driven by Go Compare, which offset effects of “challenging” digital advertising market

-

Markets: Gold at record $2300 an ounce as Fed boss sticks to line that rates likely to fall this year. FTSE 100 up 9.7 points at 7947.

-

CAB payments gets a payments license to operate in the EU, raising hopes it can turn around its fortunes after a catastrophic IPO last year

-

And…why it’s too early to judge the success of the Future Fund

UK house prices fell for the first time in three months as high mortgage rates continued to hit the market, according to Nationwide.

Property values fell by 0.2% between February and March, the Nationwide house price index showed, although they were up 1.6% compared to the same month last year.

The average home was worth £261,142 as buyers were hit with the impact of interest rates which have stood at 5.25% since August last year.

Robert Gardner, Nationwide’s chief economist, said: “Activity has picked up from the weak levels prevailing towards the end of 2023 but remain relatively subdued by historic standards.

Read more: Best UK mortgage deals of the week

“For example, the number of mortgages approved for house purchase in January was around 15% below pre-pandemic levels. This largely reflects the impact of higher interest rates on affordability.”

Northern Ireland remained the best performing area of the UK in the first three months of the year, with prices up 4.6% compared with the first quarter of 2023.

England overall saw a modest year-on-year increase of 0.4%, while Wales reported a 1.2% increase. Scotland’s annual price growth accelerated to 3.7%.

London remained the most expensive city in the country, with an average house price of £519,505. This was an annual increase of 1.6%, but a monthly fall of 2.4%.

Kate Steere, housing expert at personal finance comparison site finder.com, said: “Today’s figures show that we’re not out of the woods yet. Lenders have cut mortgage rates and wage growth has outstripped inflation, but buyers are still concerned about affordability issues and demand has been dampened as a result.

“The Bank of England’s decision to hold rates has tempered house price recovery. Meanwhile, half of experts believe that the Bank will wait until June 2024 before cutting rates, meaning we’re likely to see only a subdued recovery in house prices in the next couple of months,” she added.

Read more: UK house prices average discount drops to £10,000

Mortgage advisers have called for the Bank of England to cut interest rates after the dip in house prices.

Emma Jones, managing director of Whenthebanksaysno.co.uk, said: “Yes, activity levels remain subdued by historic standards, but sentiment is starting to improve. A base rate reduction by the Monetary Policy Committee would be welcomed and could encourage many more buyers to make their move.”

Hannah Bashford, director at Model Financial Solutions, said: “If the Bank of England cut rates in the next few months, this will definitely help to stimulate the market and we’ll see more people moving again, which will help to boost house prices.”

Watch: How much money do I need to buy a house?

Download the Yahoo Finance app, available for Apple and Android.

According to new government figures, average price house prices were £2,000 cheaper in January compared to the same period the year before.

The latest report from the Land Registry on the state of the property market showed that during the month, property prices decreased by 0.6 per cent to £282k, with London experiencing a 3.9 per cent fall, the biggest out of any region.

At the start of the year, houses in the capital cost £517k, remaining the most expensive area in Britain.

Separately, the Office for National Statistics said on Wednesday that average UK private rents jumped 9 per cent in the 12 months to February, up from 8.5 per cent in January. That was the highest rate of growth since the agency began collecting data in January 2015.

Figures from the Land Registry are generally considered a more reliable indicator of house price performance as they record the exact price paid for properties across the country. Other house price indices, such as Rightmove’s index, use asking prices.

The figures come as house prices are expected to fall by around three per cent this year, before recovering the following year and rising by around 3.5 per cent.

But properties across the UK still remain around £40k more expensive than before the pandemic.

Tom Bill, head of UK residential research at Knight Frank, said: “Although UK house prices are heading back into positive territory, the recovery is slower and more inconsistent than expected two months ago.

“Mixed signals on inflation mean rate cut expectations have cooled, mortgage costs have crept up and downwards pressure on house prices has increased.”

He added: “Based on current evidence, buyers can expect a rate cut in the summer rather than the spring although mortgage rates may fall slightly in coming months if core inflation comes under control.”

Prospective buyers in the UK have had a torrid time over the past three years,

First facing the fallout from Liz Truss’s mini-budget and then lenders raising mortgage deals in response to interest rate hikes from the central bank.

Sentiment in the housing market has improved, helped largely by cooling inflation, which has now fallen to its lowest level in nearly two and a half years.

Anthony Codling, managing director at RBC Capital Markets, said: “We view house prices as stable rather than rising or falling and stable is just what the housing market needs when there are so many other moving parts.

“Housebuilders, estate agents and homebuyers and sellers alike can all work and plan ahead with stable pricing.”

He added:“The crash in house prices so many were predicting seems ever further behind us and there is a sense that the housing market is just getting on with life, it doesn’t need any help, but it probably wouldn’t turn down any help if offered.”

Average private rents rose at their fastest annual pace last month since comparable records began in 2015, according to official UK figures.

The data from the Office for National Statistics (ONS) showed no let up in the surging costs faced by renters since 2022.

It reported a leap of 9% over the 12 months to February in a provisional estimate, up from the 8.5% annual rate seen in January.

The ONS said average UK house prices decreased 0.6% in the 12 months to January, to £282,000, noting an easing in the pace of decline.

Money latest: Reaction as UK inflation eases by more than expected

More recent industry data has suggested a return to price growth as mortgage rates have come down in anticipation of Bank of England interest rate cuts.

The upwards pressure on rents has come from demand hugely outstripping supply and landlords passing on to tenants the higher interest rates they are facing.

ONS deputy director for prices, Matt Corder, said: “Brent saw the highest annual rental growth of all local areas and Melton saw the lowest, while rental prices were highest in Kensington & Chelsea and lowest in Dumfries & Galloway.

“Average UK house prices continued to fall, albeit at a slower annual rate than seen recently.

“Indeed, Scotland’s average house prices rose at their fastest annual rate for more than a year.”

At a rate of 9%, the pace of rent increases is hugely outstripping inflation.

Read more:

The seaside town where the rental market is broken

Separate ONS data on Wednesday showed a slowing in the annual headline measure from 4% in January to 3.4% last month.

However, the prospects for Bank of England interest rate cuts still seem to be months away, as the figures will not have erased concerns among rate-setters about inflationary pressures ahead.

Hannah Bashford, director of model financial solutions, said of the ONS figures: “As shocking as this data is, it’s not a surprise as we have seen many landlords having to raise their rents to cover the increased interest costs and satisfy lenders’ affordability criteria.

“The rental market is broken and those that do not have mortgages are reaping the benefits of these hikes, while others are just about clinging onto their investments.

“These rents make it almost impossible to save for a deposit and so the circle continues.”

19 March 2024

68 Views

Happy birthday to us….and all members of the The ValPal Network!

We are celebrating a decade in business and in those 10 years we have helped agents generate a staggering 8.7million sales leads.

TVPN was launched in 2014 as the original online valuation tool – a groundbreaking development for estate agency. And the lead-generation revolution continues with the introduction of new features that keep us at the cutting edge of PropTech innovation.

In the last 10 years the average house price in the UK has risen from just under £190,000 to just over £285,000 – an increase of around 50%.

In the very early days, people had to be persuaded that technology had a worthwhile place in estate agency – some of them thought it was just a gimmick.

Innovating and refining

But they soon discovered that, as well as providing a service for potential clients visiting their website, the ValPal tool was generating precious leads every time it was used.

Today the branch office network has flourished and now stands at 4330 because since we started, we’ve been determined to keep on innovating and refining to make absolutely sure that ValPal grows in its effectiveness as a lead generator and provides agents with as much vital sales intelligence as possible.

Our latest new feature enables agents to discover whether their leads are already on the market with another firm and it’s been created through our partnership with data provider TwentyCi.

Success rates

TVPN director, Craig Vile, says: “Since partnering with them, our eyes have been opened to some fascinating insights including how many leads come to market, how long leads take to instruct an agent and the success rates of marketing campaigns.

“The data shows us that a percentage of ValPal leads are already on the market when they first fill in the ValPal tool. The reasons vary for example the seller may decide to get an instant online valuation with another agent after their listing agent advises them to reduce the asking price, or perhaps a lack of viewings.

“Obviously your call to the lead will need to be very different if they are already on the market with another agent, but there’s no way you can know this information before you speak to them, until now.”

The ValPal tool now has an optional add-on to ask the prospect if their property is already on the market. This information is then fed to the agent in the lead details so that agents can tailor their calls accordingly.

To find out more about how The ValPal Network can help your agency, click here to get in touch or call us on 0208 663 4930.

UK house prices rose for the fifth month straight in February, as buyers bet that mortgage rates will drop.

The typical price of a home is now £291,699, Halifax said, only £1,800 off the all-time high seen in June 2022.

The Halifax House Price Index showed a 1.7% year-on-year rise in UK house prices in February, slowing from 2.3% in January.

Month on month, the index added 0.4% compared to 1.2% the previous month.

Prospective buyers are being encouraged by easing mortgage costs and a rosier economic outlook but the lender warned that there is uncertainty on the horizon.

Read more: What the budget means for you

Kim Kinnaird, director at Halifax Mortgages, said: “Although lower mortgage rates, alongside expectations of Bank of England interest rate cuts this year, should help buyer confidence in the short term, the downward trend on rates is showing signs of fading.

“Raising a deposit and affording a mortgage remains challenging, especially for first-time buyers, so there could be a slowdown in the housing market this year.”

Regionally, Northern Ireland showed the strongest growth, with house prices rising by 5% annually to an average of £195,956.

The North West, North East, and Wales also saw significant increases.

London’s average house price remains the highest at £536,996, marking a 1.5% annual increase, the first positive growth since January 2023.

Eastern England experienced the most considerable decline last month with an average price drop of 0.8%.

Read more: What a 2p national insurance cut means for your finances

The increase in prices last month was nonetheless the weakest reading since September, underlining the headwinds continuing to face the housing market.

Nathan Emerson, chief executive of property professionals’ body Propertymark, said: “In order to persuade more people this is the year to sell their home, the Bank of England should start considering reducing interest rates to ease borrowing costs for aspiring homeowners.”

Tom Bill, head of UK residential research at estate agent Knight Frank, said: “Financial markets are expecting fewer rate cuts than the start of this year due to stubborn wage growth.

“This mixed picture means transactions should increase versus last year and we expect prices to rise by 3%, but the last two months of weaker inflation signals have been a useful reminder that asking prices need to remain realistic.

“The regional breakdown shows how affordability remains a big constraint on the market, with better-value areas seeing stronger price growth over the last year.”

Watch: UK house prices creep up as experts predict ‘smoother year’ for buyers and sellers

Download the Yahoo Finance app, available for Apple and Android.

UK house prices returned to growth for the first time in more than a year as mortgage rates eased, according to Nationwide.

Property values increased by 0.7% between January and February, making the average home worth £260,420. Annually, house prices increased by 1.2% in February, following a 0.2% fall in January.

It marked the first month since January 2023 that Nationwide recorded positive annual growth in house prices.

Nationwide’s chief economist Robert Gardner said: “House prices are now around 3% below the all-time highs recorded in the summer of 2022, after taking account of seasonal effects. The decline in borrowing costs around the turn of the year appears to have prompted an uptick in the housing market.”

Read more: 7 homes with links to famous literary figures

Earlier this week, the Bank of England said that the number of mortgage approvals made to home buyers jumped to the highest level since October 2022 in January this year.

HM Revenue and Customs (HMRC) figures showed this week that 82,000 home sales took place in January, which was 12% lower than January 2023 and 2% higher than December 2023.

However, Quilter’s mortgage expert Karen Noye highlights, some lenders have recently been raising their mortgage costs. She also points out that some lenders, including Nationwide, have recently been raising their mortgage rates.

“Lower mortgage rates at the start of the year appear to have spurred some buyers back to the market which has buoyed prices, but more recently we have seen a further uptick in rates as swap rates have risen so this could be relatively short lived,” she said.

“Just last week, lenders including Nationwide, NatWest, Santander and HSBC all made the decision to increase their rates,” she added.

Gardner also warned that uncertainty about the future of interest rates could yet derail price rises. “Borrowing costs remain well below the highs recorded last summer but, if the recent upward trend is sustained, it threatens to restrain the pace of any housing market recovery,” he said.

Read more: Best UK mortgage deals of the week

Tom Bill, head of UK residential research at Knight Frank, predicts average house prices will rise by 3% this year, as interest rates are cut. “Banks are keen to lend and should eventually lower rates this year as inflation comes under control, which we believe will sustain positive annual growth in 2024 and see UK house prices increase by 3%,” he said.

Watch: Nationwide Becomes The Latest Mortgage Lender To Up Home Loan Costs

Download the Yahoo Finance app, available for Apple and Android.

UK house prices rose for the fourth consecutive month in January to the highest level since October 2022 as falling mortgage rates boosted the market.

Average house prices increased to £291,029 in January, which was £3,900 more than last month, according to the Halifax house price index.

The survey showed that property values increased by 1.3% in January compared to the previous month.

Compared to the same month last year, property prices grew by 2.5%, which was the highest annual growth since January 2023.

It was the fourth monthly gain in a row after six consecutive falls before that.

Read more: What is the First Homes scheme and who is eligible?

Halifax mortgage director, Kim Kinnaird, said: ““The recent reduction of mortgage rates from lenders as competition picks up, alongside fading inflationary pressures and a still-resilient labour market has contributed to increased confidence among buyers and sellers. This has resulted in a positive start to 2024’s housing market.

“However, while housing activity has increased over recent months, interest rates remain elevated compared to the historic lows seen in recent years and demand continues to exceed supply. For those looking to buy a first home, the average deposit raised is now £53,414, around 19% of the purchase price. It’s not surprising that almost two thirds (63%) of new buyers getting a foot on the ladder are now buying in joint names.”

In London, the average price was down 0.4% year-on-year at £529,528, bucking the wider trend of growth.

Northern Ireland recorded the strongest growth across all the nations or regions within the UK – house prices here increased by 5.3% on an annual basis.

Properties in Northern Ireland now cost on average £195,760, which is £9,761 higher than the same time in January 2023.

Read more: State pension age needs to jump to 71, says think tank

Scotland and Wales both saw growth, 4% on an annual basis to £206,087 and £219,609 respectively. North West (3.2%), Yorkshire and Humber (2.8%), North East (2.0%) and East Midlands (0.5%) also recorded house price increases over the last year.

The South East fell the most last month when compared to other UK regions, with homes selling for an average £379,220 (-2.3%), a drop of £8,866.

Alice Haine, personal finance analyst at Bestinvest by Evelyn Partners, the wealth manager, said: “Interest rates have remained on pause at a 16-year high of 5.25% since August 2023 and, with inflation expected to retreat rapidly in the coming months, cuts are expected as soon as the summer.

“The improving outlook has resulted in better mortgage rates and affordability levels for first-time buyers and those looking to refinance.”

The increase in house prices for a fourth month in a row puts Britain about halfway towards a 3% increase in house prices this year already, according to economists.

Andrew Wishart, senior property economist at Capital Economics, said: “The Halifax index has a track record of being quick to respond to changes in mortgage rates, so the large increases of 1.1% in December and 1.3% in January reflect the swift drop in the average quoted mortgage rate from 5% in November to about 4.5% in January.

“Fixed mortgage rates are unlikely to fall any further in the near term, which will restrain future monthly gains in the Halifax index.”

The average rate on a two-year fixed deal this week stood at 5.55% while for a five-year deal, rates came down to 5.09%, according to figures from Uswitch.

Sarah Coles, Yahoo Finance UK columnist and head of personal finance at Hargreaves Lansdown, said: “We’re still a long way from a sellers’ market, but if you have been trying in vain to persuade buyers to see your home for months, it’s a really positive development. However, sellers shouldn’t get carried away with pricing, because this bounce may not last.”

Watch: How much money do I need to buy a house?

Download the Yahoo Finance app, available for Apple and Android.