TWO popular summer garden features could be knocking thousands of pounds off the value of your house without you realising.

With house sales still relatively slow, it’s more important than ever that sellers make their homes as desirable as possible for potential buyers.

House prices have remained relatively flat over the past year, but experts believe the property market will pick up following the general election and with rate cuts expected later this year.

With that in mind, homeowners keen to sell up should be wary of two popular summer garden features that could actually have a negative impact on the value of their property.

Garden ponds and swimming pools may be lovely during the warmer months, but they can actually wipe a combined £60k off the price of an average home, experts have warned.

A swimming pool could knock as much as 20% off your house price, equating to a hefty £55,000 penalty, according to Ruth Beeton, co-founder of Home Sale Pack.

Meanwhile, a pond is estimated to damage your home’s value by around 1.8%, which equates to around £5,000 off the average property price of £281,000, according to Office for National Statistics data.

“When it comes to the value of a property, it’s important to remember that potential buyers won’t necessarily view some features as positively as you might,” Ms Beeton said.

“Ponds and pools are a great example of this as both pose a potential safety risk, particularly for children.

“They also require a degree of maintenance, which requires time and money, and ponds can also attract rodents such as rats and mice.”

A pool typically costs £45 to £85 in labour per month to keep maintained, according to Checkatrade.

And these water features can be expensive to get rid of, too – which means either you’ll have to fork out or your buyer will be factoring the cost in – something to consider before taking the plunge and building one.

What if I have a pond or pool and want to sell?

If you do have one of these features, don’t panic.

First, remember that some people will actively be looking for these features – you might just appeal to a smaller market.

Ms Beeton said it’s important to ensure your home looks its “absolute best” when you market it online so potential buyers aren’t put off, or may even see the features as a positive.

For example, make sure you emphasise if they are not too deep or are easy to clean, and make the surrounding area look attractive on photos.

“The other option is to remove it altogether – although while this can be fairly straightforward when it comes to ponds, removing a pool can be an expensive endeavour,” Ms Beeton said.

To fill in your pond, a landscaper will typically charge between £110 and £180 per day, according to Checkatrade.

And you can expect to pay around £85 per tonne for topsoil.

However, the price of this can vary depending on the size of your pond and the local rates.

Meanwhile, removing a swimming pool can cost upwards of £10,000, although this will depend on the size of the pool.

It’s not just ponds and pools that can devalue your home.

We previously reported that conservatories could actually become unpopular with younger buyers and could be knocking £15k off a typical house price.

Meanwhile, brown, unpainted Pebbledash on your external walls could be reducing the value by £28,469 and poor parking options, or none at all, can also slash your asking price by £19,359.

You can read our full list of de-valuing features here.

BEFORE YOU MAKE THE PLUNGE….

SWIMMING pools and ponds, while offering luxury and leisure, can sometimes deter potential buyers and even decrease your home’s value.

Experts at Open Property Group told The Sun why you should think twice about adding the feature to your garden.

Upfront and Ongoing Costs:

- Installation: Pools and ponds require a significant initial investment. Depending on size, design, and materials, these costs can be substantial.

- Maintenance: Both pools and ponds require regular upkeep, including chemicals, cleaning equipment, and potential repairs. This translates to ongoing expenses for buyers.

- Heating (Pools): Especially in cooler climates, heating a pool adds to the monthly running cost, which might be a turnoff for some.

Limited Appeal:

- Niche Market: Not everyone enjoys swimming or having a water feature in their backyard. This limits the pool of potential buyers interested in your property.

- Safety Concerns: Families with young children might be wary of the safety hazards associated with pools.

- Time Commitment: Maintaining a pool or pond takes time and effort, which some buyers might not be willing to invest.

Reduced usable garden space:.

While swimming pools and ponds can enhance your enjoyment of a property, they might not be universally appealing to buyers.

How to boost the value of your home

If you are keen to sell your home, there are number of features which buyers are attracted to that could boost your value.

According to Open Property, the below features may help:

- An extension

- A home gym

- A home office, or other garden rooms – as long as there is space in your garden

- Open plan rooms with kitchen/living areas for socialising and being the heart of the home

However, sprucing up your home before selling doesn’t have to cost the earth.

“Think of quick wins that could make your home more attractive such as clearing your garden, giving your front door a fresh lick of paint, polishing your letterbox or power washing your entrance,” Daniel Copley, consumer expert at Zoopla told The Sun.

He added: “When it comes to the interior of your home, focus on clearing out any clutter from high-traffic areas like your kitchen or living room.”

Mr Copley also said that sellers should focus on the opportunities in your home to improve its value.

“For example, could you easily upgrade elements in your bathroom like taps and shower fixtures, or improve your home’s EPC rating by installing solar panels,” he explained.

What is going on with housing market?

The property market has seen a slow down over the past few years because mortgage rates have significantly increased, putting off first-time buyers and meaning homeowners are reluctant to move.

However, markets expect the Bank of England to cut its base rate in August this year after policymakers kept it at 5.25% in June.

This is important for buyers because high street banks and lenders use the BoE base rate to set their own interest rates on mortgages, loans and savings accounts.

So, if the base rate comes down, interest on mortgages rates and loans is likely to fall as well.

The number of people selling their home is now set to rise this year.

Zoopla expects 1.1m homes to be sold in 2024 – 10% more than in 202.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

By Mohamad Ali, SVP, IBM Consulting and Rahul Kalia, Managing Partner, United Kingdom and Ireland

July 09, 2024

IBM announced it has acquired SiXworks Limited (Ltd.), a UK-based consultancy serving the UK defence sector and specialising in digital transformation in highly secure environments. SiXworks is a trusted partner to the UK Ministry of Defence.

The acquisition deepens IBM Consulting’s ability to serve clients in the UK defence sector with additional highly specialist industry and technical domain skills across digital, cyber and defence cloud solutions.

Founded in 2017, and headquartered in Farnborough, England, SiXworks is a leading consulting provider of secure digital solutions, specialising in end-to-end digital transformation from defining requirements to agile solution delivery to post-deployment maintenance support.

This acquisition exemplifies IBM’s ongoing commitment to serving clients in the public sector. IBM’s acquisition of Octo established IBM as one of the top digital transformation partners to the U.S. federal government, including defence, health, and civilian agencies. Now SiXworks will add complementary capabilities to IBM’s existing cybersecurity, data and AI offerings in the United Kingdom – allowing IBM to enhance how we support end-to-end transformation for defence sector clients.

SiXworks will join IBM Consulting as part of the public sector industry team.

To learn more about SiXworks, visit: https://www.sixworks.net

Local estate agency, Lion Estates, have won The British Property Award for Milton Keynes for a second year due to their level of great customer service.

The Lion Estates team performed outstandingly throughout the extensive judging period, which focused on customer service levels. “This is testament to our ‘quality over quantity’ approach” said Dominic Marcel, Founding Partner.

Lion Estates are currently shortlisted for several national awards, which are due to be announced later this year. Thanks to The British Property Awards (BPA), agents across the UK have the essential chance to be assessed foe their service against that of their local, regional, and national competitors.

The property awards are given to agents that go above and beyond in providing exceptional customer service; these accolades serve as a spotlight to draw attention to these qualities in the local marketplace.

Since there is no admission fee, BPA is among the estate agency awards suppliers that is most inclusive. This has made it possible for their award to be structured in a way that ensures maximum participation, with over 90% of agents who meet their minimum criteria on a local level.

“When we launched in 2019 we didn’t want to simply offer a better version of the traditional estate agency set up, we wanted to revolutionise the home-moving experience by copying the models of countries where estate agents are seen as a valued asset, rather than a necessary evil. We are extremely proud that sticking to our ethos of offering a personalised approach to each of our clients by allocating one agent to look after both your sale and onward move has enabled us to grow a team of like-minded agents who are passionate about raising the standard of our industry.” Dominic said.

In order to get a fair and impartial assessment of each estate agent’s customer service, the BPA team personally mystery shops each agent in accordance with a set of 25 criteria. The judging criteria is extensive and intricate, examining various media, situations, and time periods to ensure that each agent has been evaluated equally and rigorously.

Robert McLean from BPA said, “Our awards have been specifically designed to be attainable to all agents, removing common barriers to entry, such as a cost, to ensure that we have the most inclusive awards. Our awards have also been designed to remove any opportunity for bias or manipulation. If agents have been attributed with one of our awards, it is simply down to the fantastic customer service levels that they have demonstrated across a prolonged period.”

Dominic added, “It’s amazing to think that in five short years we’re constantly being recognised as one of the top estate agencies in Milton Keynes and are the forefront of the ‘self-employed estate agent’ movement, not just in Milton Keynes, but across the whole of the UK. In order to continue providing the same high level of service to more home movers, we’re always looking for more agents who are as passionate about improving our industry to join our team. Those that believe that dealing with quality over quantity is in the best interest of the client.”

If you’re interested in joining the Lion Estates team, reach out to Dominic Marcel on dominic@lionestates.co.uk

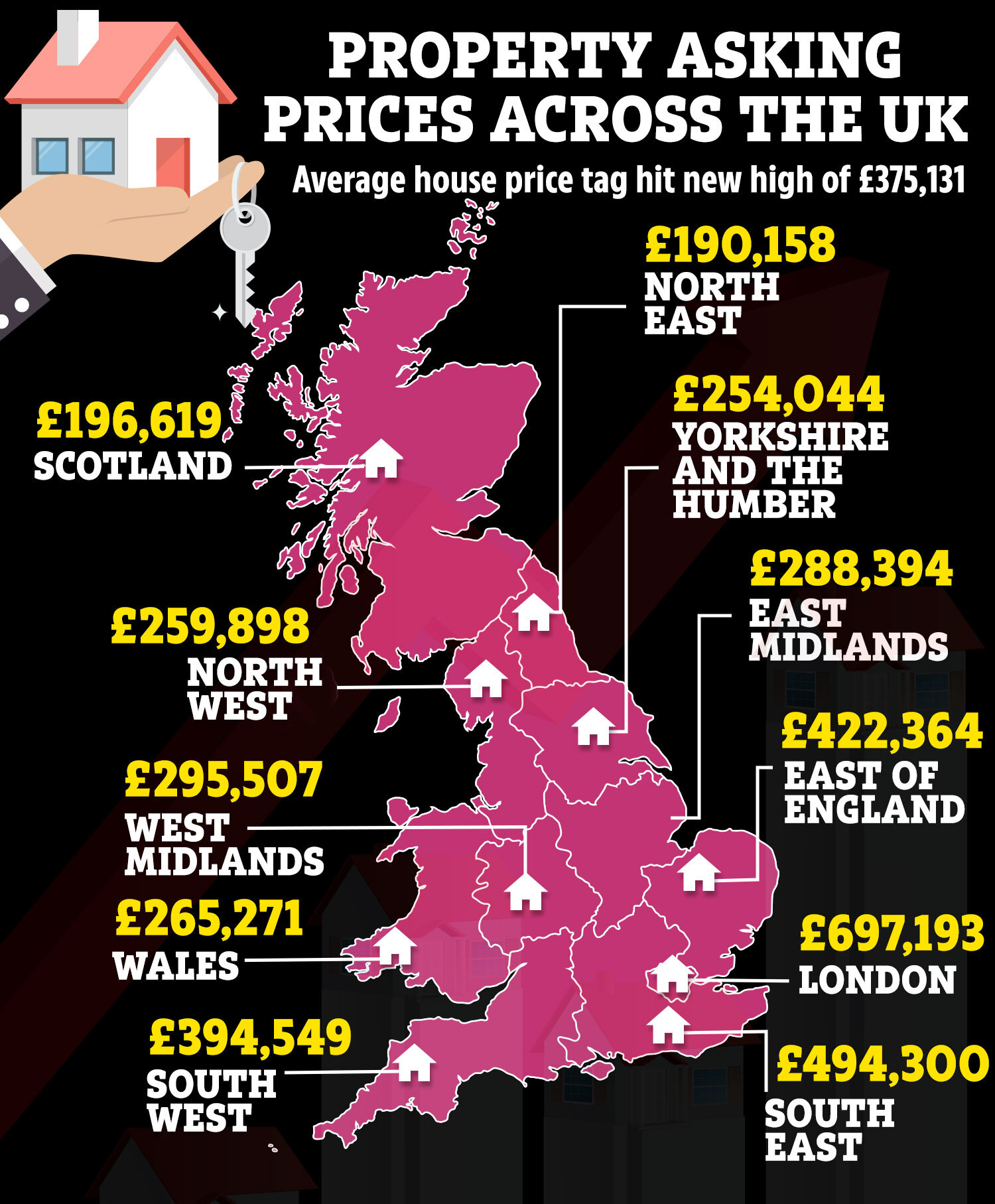

FIRST-TIME buyers will be keen to know the exact amount they need for a home deposit as house prices hit a record high.

The average price tag on a home reached £375,131 in May, according to Rightmove.

Across Britain, the price of a property coming to market rose 0.8%, or £2,807, month-on-month.

Typically, you need enough money in the bank for a 10% deposit – at the very least – to buy a property.

This means first-time buyers will need to put down an average of at least £37,513 in the current market to afford their first home.

Pent-up demand from would-be buyers who paused their plans last year is a key driver behind increased home mover activity.

This is despite mortgage rates remaining higher for longer than anticipated, Rightmove said.

The number of sales being agreed during the first four months of the year is 17% higher than last year.

The North East, with the cheapest average prices in Great Britain, has seen the strongest price growth in the last year, rising by an average of 5.8% to £190,158.

A first-time buyer in this region would need a 10% deposit of £19,015, based on this average

Scotland came in second, with the average house price now standing at £196,169 having risen by 2.7% in the last year.

At the other end of the spectrum, in the East of England, house prices fell by 0.6% in the last year.

The average house price in the region now stands at £422,264 and a 10% deposit would be £42,226.

The average house price in the South East also fell by 0.1% with the average house price now standing at £494,300.

In some positive signs for the mortgage market, HSBC UK, Barclays and TSB cut their mortgage rates last Friday.

Tim Bannister, Rightmove’s director of property science, said: “The momentum of the spring selling season has exerted enough upwards price pressure to reach a new record asking price.”

Rightmove anticipates the number of completed house sales this year to reach around 1.1 million.

How to get the best deal on your mortgage

IF you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

There are several ways to land the best deal.

Usually the larger the deposit you have the lower the rate you can get.

If you’re remortgaging and your loan-to-value ratio (LTV) has changed, you’ll get access to better rates than before.

Your LTV will go down if your outstanding mortgage is lower and/or your home’s value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you’re nearing the end of a fixed deal soon it’s worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

To find the best deal use a mortgage comparison tool to see what’s available.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You’ll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you’ll pay interest on it and so will cost more in the long term.

You can use a mortgage calculator to see how much you could borrow.

Remember you’ll have to pass the lender’s strict eligibility criteria too, which will include affordability checks and looking at your credit file.

You may also need to provide documents such as utility bills, proof of benefits, your last three month’s payslips, passports and bank statements.

But it said the lengthy time to complete a sale after finding a buyer remains a challenge for both agents and movers.

The average time between agreeing a sale and legal completion is five months.

In total, it is taking more than seven months on average from a seller coming to market to completing their move.

This means would-be sellers hoping to celebrate Christmas in a new home need to be coming to the market about now, the website said.

While the housing market may seem daunting, it is possible for first-time buyers to make their hard-earned cash go further and secure a mortgage they can afford to repay.

Below is a list of schemes that are available to help wanna homeowners get on the housing ladder.

The 100% mortgage

That’s why several of the big banks and building societies allow first-time buyers to borrow the full amount it costs to buy their home.

These deals are often referred to as 100% loan-to-value mortgages – because you don’t need any deposit to buy.

But in almost all cases, a family member will need to help out in some way.

Some deals need parents to agree to guarantee repayments, meaning the lender will need to check their income to make sure they can afford to.

The guarantee only kicks in if you can’t make a payment for any reason.

There are also a number of 100% family mortgages – some require a family member or close friend to deposit some savings with the lender for a fixed period.

Others will lend you 100% of the home’s purchase price but will want to take a “charge” on a family member’s home in place of a deposit.

This means that no cash changes hands, but should things go wrong, the lender will be able to get their money back from your relative.

Before that happens, your home would be sold and any money you still owed the lender would be taken from your family member’s home.

Either they would have to borrow money to pay back the lender, or they would, in the worst-case scenario, have to sell to cover any remaining debt.

There is a very serious warning that comes with taking a 100% mortgage.

If house prices fall, you could end up owing the bank more than your home is worth.

That only matters if you need to sell, or when you need to remortgage to a different lender.

But it can cause a major headache.

First Homes

If you’re a first-time buyer, you may be able buy a home for between 30% and 50% less than its market value through the government’s First Homes scheme.

You can buy a new build home from a developer or a property from someone who’s used the scheme before and is now selling.

The First Homes scheme is only available in England and to qualify you have to be 18 or older and a first-time buyer.

You’ll need to be able to get a mortgage for at least half the price of the home.

And you’ll only be able to use the scheme if your total household income is £80,000 or less.

If you’re in London, buyers’ joint income can be a maximum of £90,000.

Shared ownership

You can buy a home through the shared ownership scheme if you can’t afford all of the deposit and mortgage payments for a home that meets your needs.

You buy a share of the property and pay rent to a landlord on the rest.

England, Scotland, Northern Ireland and Wales all have slightly different rules, so check the details carefully.

You can buy a share between 10% and 75% of the home’s full market value and pay rent to the landlord on the rest.

There may also be ground rent and service charges to help maintain common areas shared between you and your neighbours, so factor these in.

You can take out a mortgage to buy your share or pay for it with savings.

You’ll also need to pay a deposit, usually between 5% and 10% of the share you’re buying.

You can buy more of the home later on, when you can afford to.

You’ll pay less rent to the landlord whose share will get smaller.

But watch out for the small print as sometimes you can only buy more of your home in £10,000 chunks.

You’re restricted to buying a new build or from a seller who also bought through shared ownership.

If you have a long-term disability, you may also be able to buy a home that suits your needs such as a ground floor flat.

Another thing you need to consider is that all shared ownership properties are leasehold.

You must check that your ground rents and service charges won’t be put up more than a fixed percentage plus or at the inflation rate.

Mortgage Guarantee Scheme

Available for first-time buyers and those who’ve owned a property before who have a minimum 5% deposit.

It can be used to buy any type of home so long as you don’t pay more than £600,000 for it.

By providing a guarantee that the government will cover some of a lender’s losses if a borrower can’t afford to repay their mortgage and the home is repossessed – more lenders are prepared to lend up to 95%.

There’s a clock ticking on this scheme – it’s due to end in June 2025.

Lifetime Isa

If you’re saving for a deposit to buy your first home then saving into a Lifetime Isa is a no brainer.

You can save up to £4,000 a year into it and the government will give you a free bonus worth 25% of whatever you save.

If you save the full allowance, that means you’ll get £1,000 a year, every year, for free from the government.

You have to be between 18 and 39 to open a Lisa and you can pay in and get the bonus until you’re 50.

You can have a cash or investment Lisa.

If you withdraw your money before you’re 60, it must be spent on buying your first home.

If you withdraw it for another reason, you will have to pay back 25% of your savings to the government.

Effectively you’re giving back the bonuses.

Help to Build

If you’ve decided to build a new home, you could be eligible to get a Help to Build equity loan from the government.

There are different rules in England, Wales and Scotland so check what’s available for you.

If you’re building a home in Northern Ireland you don’t have access to the scheme.

If you qualify, you can apply for the Help to Build equity loan to pay for land to build on or if you plan to build a new flat on top of an existing building.

If you buy a commercial property and convert it into a home you can also apply and when you knock a property down and build a new home in its place.

You can borrow between 5% and 20% of the land and building costs but you must be able to get a mortgage as well.

Buying the land and the estimated building costs must not be more than £600,000 with building costs capped at £400,000

You can only get an equity loan if you also have a mortgage offer for the home you want to build.

There’s a £1 monthly fee to Homes England to manage the loan and you’ll be charged yearly interest at 1.75% interest after five years.

After six years the amount of interest you pay will go up in line with the consumer price index, plus 2%.

Paying interest does not count towards paying back the equity loan.

Help to Buy – Wales

Help to Buy has ended in England but there is still a scheme in Wales.

You can apply for an equity loan from the government to buy a new build home from a registered builder.

You’ll have to put down at 5% deposit, can borrow up to 20% from the government and get a repayment mortgage for the rest of the purchase price.

Right to Buy

This scheme was famously brought in during the 1980s by then Prime Minister Maggie Thatcher.

It’s still running today and allows most council tenants the right to buy their council house at a discount.

There are different rules for Wales, Scotland and Northern Ireland.

You can make a joint application with up to three family members who’ve lived with you for the past 12 months.

If you rent from a Housing Association you may also have the right to buy it at a discount under the government’s Right to Acquire Scheme.

Deposit Unlock

This lets you buy a new build home from any developer registered with the scheme so long as you have a 5% deposit.

Newcastle Building Society, Nationwide and Accord Mortgages are the only lenders signed up to Deposit Unlock at the moment.

The scheme is only available if you apply through a mortgage broker.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

FIRST-TIME buyers will be keen to know the exact amount they need for a home deposit as house prices hit a record high.

The average price tag on a home reached £375,131 in May, according to Rightmove.

1

Across Britain, the price of a property coming to market rose 0.8%, or £2,807, month-on-month.

Typically, you need enough money in the bank for a 10% deposit – at the very least – to buy a property.

This means first-time buyers will need to put down an average of at least £37,513 in the current market to afford their first home.

Pent-up demand from would-be buyers who paused their plans last year is a key driver behind increased home mover activity.

This is despite mortgage rates remaining higher for longer than anticipated, Rightmove said.

The number of sales being agreed during the first four months of the year is 17% higher than last year.

The North East, with the cheapest average prices in Great Britain, has seen the strongest price growth in the last year, rising by an average of 5.8% to £190,158.

A first-time buyer in this region would need a 10% deposit of £19,015, based on this average

Scotland came in second, with the average house price now standing at £196,169 having risen by 2.7% in the last year.

At the other end of the spectrum, in the East of England, house prices fell by 0.6% in the last year.

The Sun’s James Flanders explains how to find the best deal on your mortgage

The average house price in the region now stands at £422,264 and a 10% deposit would be £42,226.

The average house price in the South East also fell by 0.1% with the average house price now standing at £494,300.

In some positive signs for the mortgage market, HSBC UK, Barclays and TSB cut their mortgage rates last Friday.

Tim Bannister, Rightmove’s director of property science, said: “The momentum of the spring selling season has exerted enough upwards price pressure to reach a new record asking price.”

Rightmove anticipates the number of completed house sales this year to reach around 1.1 million.

How to get the best deal on your mortgage

IF you’re looking for a traditional type of mortgage, getting the best rates depends entirely on what’s available at any given time.

There are several ways to land the best deal.

Usually the larger the deposit you have the lower the rate you can get.

If you’re remortgaging and your loan-to-value ratio (LTV) has changed, you’ll get access to better rates than before.

Your LTV will go down if your outstanding mortgage is lower and/or your home’s value is higher.

A change to your credit score or a better salary could also help you access better rates.

And if you’re nearing the end of a fixed deal soon it’s worth looking for new deals now.

You can lock in current deals sometimes up to six months before your current deal ends.

Leaving a fixed deal early will usually come with an early exit fee, so you want to avoid this extra cost.

But depending on the cost and how much you could save by switching versus sticking, it could be worth paying to leave the deal – but compare the costs first.

To find the best deal use a mortgage comparison tool to see what’s available.

You can also go to a mortgage broker who can compare a much larger range of deals for you.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You’ll also need to factor in fees for the mortgage, though some have no fees at all.

You can add the fee – sometimes more than £1,000 – to the cost of the mortgage, but be aware that means you’ll pay interest on it and so will cost more in the long term.

You can use a mortgage calculator to see how much you could borrow.

Remember you’ll have to pass the lender’s strict eligibility criteria too, which will include affordability checks and looking at your credit file.

You may also need to provide documents such as utility bills, proof of benefits, your last three month’s payslips, passports and bank statements.

But it said the lengthy time to complete a sale after finding a buyer remains a challenge for both agents and movers.

The average time between agreeing a sale and legal completion is five months.

In total, it is taking more than seven months on average from a seller coming to market to completing their move.

This means would-be sellers hoping to celebrate Christmas in a new home need to be coming to the market about now, the website said.

While the housing market may seem daunting, it is possible for first-time buyers to make their hard-earned cash go further and secure a mortgage they can afford to repay.

Below is a list of schemes that are available to help wanna homeowners get on the housing ladder.

The 100% mortgage

That’s why several of the big banks and building societies allow first-time buyers to borrow the full amount it costs to buy their home.

These deals are often referred to as 100% loan-to-value mortgages – because you don’t need any deposit to buy.

But in almost all cases, a family member will need to help out in some way.

Some deals need parents to agree to guarantee repayments, meaning the lender will need to check their income to make sure they can afford to.

The guarantee only kicks in if you can’t make a payment for any reason.

There are also a number of 100% family mortgages – some require a family member or close friend to deposit some savings with the lender for a fixed period.

Others will lend you 100% of the home’s purchase price but will want to take a “charge” on a family member’s home in place of a deposit.

This means that no cash changes hands, but should things go wrong, the lender will be able to get their money back from your relative.

Before that happens, your home would be sold and any money you still owed the lender would be taken from your family member’s home.

Either they would have to borrow money to pay back the lender, or they would, in the worst-case scenario, have to sell to cover any remaining debt.

There is a very serious warning that comes with taking a 100% mortgage.

If house prices fall, you could end up owing the bank more than your home is worth.

That only matters if you need to sell, or when you need to remortgage to a different lender.

But it can cause a major headache.

First Homes

If you’re a first-time buyer, you may be able buy a home for between 30% and 50% less than its market value through the government’s First Homes scheme.

You can buy a new build home from a developer or a property from someone who’s used the scheme before and is now selling.

The First Homes scheme is only available in England and to qualify you have to be 18 or older and a first-time buyer.

You’ll need to be able to get a mortgage for at least half the price of the home.

And you’ll only be able to use the scheme if your total household income is £80,000 or less.

If you’re in London, buyers’ joint income can be a maximum of £90,000.

Shared ownership

You can buy a home through the shared ownership scheme if you can’t afford all of the deposit and mortgage payments for a home that meets your needs.

You buy a share of the property and pay rent to a landlord on the rest.

England, Scotland, Northern Ireland and Wales all have slightly different rules, so check the details carefully.

You can buy a share between 10% and 75% of the home’s full market value and pay rent to the landlord on the rest.

There may also be ground rent and service charges to help maintain common areas shared between you and your neighbours, so factor these in.

You can take out a mortgage to buy your share or pay for it with savings.

You’ll also need to pay a deposit, usually between 5% and 10% of the share you’re buying.

You can buy more of the home later on, when you can afford to.

You’ll pay less rent to the landlord whose share will get smaller.

But watch out for the small print as sometimes you can only buy more of your home in £10,000 chunks.

You’re restricted to buying a new build or from a seller who also bought through shared ownership.

If you have a long-term disability, you may also be able to buy a home that suits your needs such as a ground floor flat.

Another thing you need to consider is that all shared ownership properties are leasehold.

You must check that your ground rents and service charges won’t be put up more than a fixed percentage plus or at the inflation rate.

Mortgage Guarantee Scheme

Available for first-time buyers and those who’ve owned a property before who have a minimum 5% deposit.

It can be used to buy any type of home so long as you don’t pay more than £600,000 for it.

By providing a guarantee that the government will cover some of a lender’s losses if a borrower can’t afford to repay their mortgage and the home is repossessed – more lenders are prepared to lend up to 95%.

There’s a clock ticking on this scheme – it’s due to end in June 2025.

Lifetime Isa

If you’re saving for a deposit to buy your first home then saving into a Lifetime Isa is a no brainer.

You can save up to £4,000 a year into it and the government will give you a free bonus worth 25% of whatever you save.

If you save the full allowance, that means you’ll get £1,000 a year, every year, for free from the government.

You have to be between 18 and 39 to open a Lisa and you can pay in and get the bonus until you’re 50.

You can have a cash or investment Lisa.

If you withdraw your money before you’re 60, it must be spent on buying your first home.

If you withdraw it for another reason, you will have to pay back 25% of your savings to the government.

Effectively you’re giving back the bonuses.

Help to Build

If you’ve decided to build a new home, you could be eligible to get a Help to Build equity loan from the government.

There are different rules in England, Wales and Scotland so check what’s available for you.

If you’re building a home in Northern Ireland you don’t have access to the scheme.

If you qualify, you can apply for the Help to Build equity loan to pay for land to build on or if you plan to build a new flat on top of an existing building.

If you buy a commercial property and convert it into a home you can also apply and when you knock a property down and build a new home in its place.

You can borrow between 5% and 20% of the land and building costs but you must be able to get a mortgage as well.

Buying the land and the estimated building costs must not be more than £600,000 with building costs capped at £400,000

You can only get an equity loan if you also have a mortgage offer for the home you want to build.

There’s a £1 monthly fee to Homes England to manage the loan and you’ll be charged yearly interest at 1.75% interest after five years.

After six years the amount of interest you pay will go up in line with the consumer price index, plus 2%.

Paying interest does not count towards paying back the equity loan.

Help to Buy – Wales

Help to Buy has ended in England but there is still a scheme in Wales.

You can apply for an equity loan from the government to buy a new build home from a registered builder.

You’ll have to put down at 5% deposit, can borrow up to 20% from the government and get a repayment mortgage for the rest of the purchase price.

Right to Buy

This scheme was famously brought in during the 1980s by then Prime Minister Maggie Thatcher.

It’s still running today and allows most council tenants the right to buy their council house at a discount.

There are different rules for Wales, Scotland and Northern Ireland.

You can make a joint application with up to three family members who’ve lived with you for the past 12 months.

If you rent from a Housing Association you may also have the right to buy it at a discount under the government’s Right to Acquire Scheme.

Deposit Unlock

This lets you buy a new build home from any developer registered with the scheme so long as you have a 5% deposit.

Newcastle Building Society, Nationwide and Accord Mortgages are the only lenders signed up to Deposit Unlock at the moment.

The scheme is only available if you apply through a mortgage broker.

Do you have a money problem that needs sorting? Get in touch by emailing money-sm@news.co.uk.

Plus, you can join our Sun Money Chats and Tips Facebook group to share your tips and stories

After falling for five months in a row, average house prices picked up in March by 1.4%, some £3,000, and a positive outcome compared to markets in England and Wales, according to the Walker Fraser Steele March House Price Index. Scotland’s average house price now stands a little above £223,500, that is within £300 of its peak level reached in June 2023. The seemingly marked turn-round speaks volumes about the narrow tramlines within which the market has moved over the past year.

In March, average property prices in Scotland increased by 1.4%, or almost £3,000, following a five-month decline. This was a far stronger performance than that witnessed in the English and Welsh markets. Scotland’s average house price is currently just over £223,500, which is about £300 less than its high price from June 2023.

This significant turnaround speaks volumes about the negligible movement we have seen in recent months. Four authorities—Midlothian, Argyll and Bute, Falkirk, and Inverclyde—achieved new heights in terms of their regional average values and the total number of local authorities reporting rising prices was twenty-one, the highest since May of last year – another clear and welcome sign that the market is beginning to stabilize.