A Gen-Z property investor who owns three properties has shut down claims landlords are at fault for Australia’s current rental crisis.

Harley Giddings, 24, has worked hard since adolescence and in every job ‘under the sun’ to own a house and is now the proud owner of multiple investment properties.

The young investor posted a TikTok to his thousands of followers saying he often gets comments ‘all the time’ that blame investors for the housing shortage.

The savvy landlord said he can understand Aussies’ frustrations but thinks this is ‘misguided’, firmly believing the sky-rocketing rents and housing shortage lie with high immigration and low building approvals.

‘In 2022 and 2023 the government let in over a million migrants into the country,’ he said.

Harley Giddings, 24, has a property portfolio consisting of three investment properties. He understands people are ‘hurting’ but believes Aussies are ‘misguided’ when blaming landlords for the rental crisis

‘Basic supply and demand’ is the reason for the Australian housing crisis, according to the 24-year-old

‘According the Australian Bureau of Statistics, this is the most amount of migrants Australia has ever let into the country since they started recording.

‘These one million migrants were let in at a time when Australia already had a housing crisis.’

Mr Giddings said that when people arrive in Australia they are looking at renting and not buying, which is why so many people are at inspections for rental opens.

‘Basic supply and demand,’ he said.

The second reason the young property investor gave for the housing shortage in Australia was the low amount of homes being built.

‘We are simply not building enough properties,’ he said.

‘In Victoria, my home state, we currently have the lowest amount of building approvals that we’ve had in the last decade.

‘This issue is Australia-wide.’

The 24-year-old quoted research from the Institute of Public Affairs that by 2028 Australia’s housing supply will be short by 252,800 homes.

Many Australians agreed with the young investor, also blaming the government.

‘Absolute master stroke by the government,’ one wrote.

‘Not to mention all of Victoria’s new tax laws on investments, landlords are getting rid of them,’ one said.

‘If you can’t keep up with supply reduce the demand,’ another wrote.

Mr Giddings said the the low number of houses being built in Australia is a major reason for rents increasing so high (pictured people at an auction)

However, other Aussies were quick to throw blame back at the investor.

‘You are also the problem. You cannot just blame building and immigration. You know why people can’t afford to build? Because they can’t afford the increased prices driven up by decades of investors,’ one wrote.

‘Investors and immigration: two problems [that] need to be stopped,’ another said.

Mr Giddings told Yahoo he understands it would be very hard at the moment to be a renter and there’s a lot of ‘hurt’ due to prices increasing not just in rent, but everything else as well.

‘I just think there’s a couple of factors that is like worsening the housing crisis that isn’t caused by renters or landlords,’ he said.

The investor, who became interested in property after reading multiple books and listening to podcasts about investing, made it clear to Yahoo that he did not blame the people moving to Australia, but government policy.

Mr Giddings dropped out of university half-way through his business degree because he didn’t think it would offer him much.

The 24-year-old instead worked two jobs, seven days a week, saving more than $100,000 by age 22.

Mr Giddings, who describes his family as middle class, went halves with his dad for his first property, as told by Yahoo.

The young investor believes high rents and a competitive market has been created by the government allowing one million migrants into the country in the middle of a housing crisis

‘My parents aren’t really the kind of investment-savvy people. Like, dad’s a firefighter, mum’s a hairdresser. So he had the borrowing power because he was working full time and I had the savings,’ he said.

The hard-worker, who has always been interested in investing, purchased away from his state of Victoria and instead invested in Western Australia.

‘There’s 15,000 suburbs in Australia, it’s highly unlikely that the area you live in is going to be one of the best performing,’ he said.

The first property cost the father and son $450,000 and then the 24-year-old used more savings to buy a second property.

Mr Giddings used the equity built up in the second property to purchase his third investment.

This impressive property portfolio was achieved by the time he was just 23.

According to the Australia Tax Office, most landlords are ‘mum and dad’ investors, with a massive 71 per cent of landlords in Australia owning just one investment property.

Only 19 per cent own two properties.

According to the Australian Bureau of Statistics work begun in 2023 on just 163,836 new houses, which is the lowest amount since 2012.

Compounding the issue is a 90,000 tradie shortage, who are needed in the next three months so the government’s housing plan can stay on deadline.

Nationwide has issued a warning to people under the age of 40 who don’t own a house. The UK’s largest building society has warned the house prices crisis means one in five can’t buy first home until age 40 in a Cost of Living crisis.

One in five in the UK faces buying their first home far later than previous generations have been able to.. 20 per cent will be left without their own first home into their forties, a rise on the current average first-time buyer age (33).

Nearly half of first-time buyers say their prospects of owning a home are further away than ever due to the ongoing cost-of-living crisis, research from Nationwide has found. The research came in a poll of 1,000 aspiring homeowners.

READ MORE UK set for snow within days with three English cities hammered by ‘2cm per hour’

It found that more than eight in ten (84 per cent) say that the Cost of Living crisis has impacted their plans, with 49 per cent having delayed them due to affordability concerns. Six in 10 are postponing their homeownership plans by up to three years.

Rachael Sinclair, Nationwide’s director of mortgages and financial wellbeing, said: “Getting that first home is as challenging as it ever has been. We need to solve the first-time buyer conundrum, which is why Nationwide has continually called for the government to set up an independent review of the first-time buyer market.

“It’s why we’ll also be jointly launching a Housing White Paper with the Building Societies Association next week, which will outline the essential policy changes that are needed to tackle the homeownership crisis and support people into their first home.”

According to the poll, the average amount people said they had to put towards the deposit was £9,533 – far short of the £22,400 needed for a 10 per cent deposit based on the £223,554 average first-time buyer house price, according to Nationwide’s House Price Index.

House prices fell for the first time in six months in March amid rising mortgage rates, according to a lender.

Property values declined by 1pc last month when compared to February, the Halifax house price index showed.

The survey found that the average house price in Britain dropped to £288,430, around £2,900 less than last month.

Compared to the same month last year, house prices have risen by 0.3pc.

Halifax Mortgages director Kim Kinnaird said: “Financial markets have also become less optimistic about the degree and timing of Base Rate cuts, as core inflation proves stickier than generally expected.

This has stalled the decline in mortgage rates that had helped to drive market activity around the turn of the year.”

Purplebricks chief executive Sam Mitchell added: “The blip in house prices was caused by a small increase in rates at the start of March, since then we have seen banks compete more aggressively, rates reduce further, inflation come down ahead of expectations, and both viewings and offers levels are ahead of expectations.”

A separate survey by rival lender Nationwide also showed a decline in monthly house prices by 0.2pc between February and March.

Ms Kinnaird added:

That a monthly fall should occur following five consecutive months of growth is not entirely unexpected particularly in view of the reset the market has been going through since interest rates

began to rise sharply in 2022.Despite this house prices have shown surprising resilience in the face of significantly higher borrowing costs.

Affordability constraints continue to be a challenge for prospective buyers, while existing homeowners on cheaper fixed-term deals are yet to feel the full effect of higher interest rates.

This means the housing market is still to fully adjust, with sellers likely to be pricing their properties accordingly.

Thanks for joining me. House prices unexpectedly fell last month, according to the Nationwide house price index.

Prices were down 0.2pc between February and March as mortgage approvals remained subdued.

5 things to start your day

1) Shop inflation falls below 2pc in boost for rate cut hopes | Bank of England’s target in sight as energy prices also drop

2) Prepare for chaotic rerun of Trump v Biden, City investors told | Low trust and a polarised electorate ring alarm bells

3) Why Elon Musk thinks Earth will have more robots than humans | AI boom revives hopes for Tesla billionaire’s vision

4) Energy Secretary considers axing £4bn of green levies from electricity bills | Policy costs could be holding back progress of net zero rollout

5) Social networks could quit Britain under online safety laws, Reddit claims | Burden of complying with new rules will hit smaller companies hardest

What happened overnight

Asian stocks rose while currencies stayed strong against the yen amid concerns about a possible intervention by the Bank of Japan.

Hong Kong’s Hang Seng was the standout, piling on more than 2pc on the first day of trading since Thursday as investors cheered data showing China’s manufacturing grew more than forecast last month.

Sydney, Seoul, Singapore, Taipei and Manila were in positive territory. Shanghai was slightly lower with Wellington and Jakarta.

Japan’s Nikkei was volatile. It reclaimed the 40,000 points mark in the morning session but was last flat, below the mark.

The yen was slightly weaker at 151.76 per dollar, not too far from the 34-year low of 151.975 it touched last week, with traders keenly watching for hints of intervention from Japanese authorities.

Meanwhile, expectations the Federal Reserve was close to cutting interest rates faded as data on Monday showed US manufacturing grew for the first time in one and a half years in March as production rebounded sharply and new orders increased, highlighting the strength of the economy.

The robust manufacturing data sent yields on US Treasuries higher, with two-year and 10-year yields climbing to two-week peaks, boosting the dollar.

Thanks for joining us. Retail sales came in better than expected last month in a sign Britain’s economy is moving out of recession.

Sales remained flat in February as food and fuel sellers saw a decline during the month, according to data from the Office for National Statistics (ONS).

However, economists had predicted sales to fall by 0.4pc, down from growth of 3.6pc the month before, the ONS said.

Online sales had grown during the month, especially for clothing, as last month’s wet weather pushed down the footfall of people heading out to the shops.

5 things to start your day

1) Sickness benefits bill to surge by a third as worklessness crisis deepens | Cost of health and disability payments to jump to £90bn within five years

2) Member vote on £2.9bn Virgin Money deal would breach takeover rules, Nationwide claims | Lender bypasses members to comply with legal reasons after blaming tight turnaround

3) US accuses Apple of illegal monopoly over smartphone market | Move is the latest in a wave of landmark US monopoly abuse cases against big tech

4) Mike Ashley sues Newcastle United amid row with Amanda Staveley | Former owner claims club breached competition law by refusing to supply kit to Sports Direct

5) Britain could be a world leader in nuclear power, but not with old technology | The Government must whole-heartedly commit if it is to make Big Fission a success

What happened overnight

The yuan fell sharply and Chinese shares skidded, dragging down markets broadly in Asia and dampening an equity rally spurred by a surprise rate cut in Switzerland that had investors wagering on who will ease policy next.

Traders also were on high alert as the yen crept back toward multi-decade lows despite jawboning efforts from Japanese government officials to shore it up and the central bank’s historic policy pivot earlier this week.

China’s yuan weakened sharply to a four-month low and breached the psychologically important 7.2 per dollar level. It was last nearly 0.4pc lower at 7.2243.

The fall prompted the country’s major state-owned banks to sell dollars for yuan in an attempt to slow its decline, sources told Reuters.

The yuan has been pressured by growing market expectations that Beijing needs to roll out more stimulus to stabilise the world’s second-largest economy, and by the weaker yen. The state bank buying did little to soothe investors’ nerves.

The mainland blue-chip CSI300 index and Shanghai Composite index each fell 1pc, while Hong Kong’s Hang Seng Index slid 2pc.

Elsewhere, Tokyo’s key Nikkei index ended at another record on Friday after Wall Street stocks also hit fresh highs on optimism about the US economy and Fed policy.

The benchmark Nikkei 225 index was up 0.2pc, or 72.77 points, to end at 40,888.43, while the broader Topix index added 0.6pc, or 17.01 points, to 2,813.22.

In America, US stocks extended their push to record highs yesterday, led by big gains for chipmakers.

The S&P 500 rose 0.3pc, to 5,241.53, and set an all-time high for a third straight day. Three out of every four stocks in the index gained ground.

The Dow Jones Industrial Average gained 0.7pc, to 39,781.37, and the Nasdaq Composite rose 0.2pc, to 16,401.84. Both indexes added to records set a day earlier.

The yield on benchmark US 10-year Treasury bonds was down 0.2 basis points to 4.269pc.

Thousands of wealthy retirees are ditching Florida and now choosing to spend their golden years in Appalachia instead – but not everyone is happy about it.

With its warm weather and low tax burden, the sunshine state has long been known as the retirement capital of the US.

Yet Southern Appalachia, known for its stunningly beautiful views, is increasingly giving Florida a run for its money, Wall Street Journal reported.

The population in counties in southern Appalachia designated as retirement or recreational areas grew by 3.8 percent between April 2020 and July 2022 – more than six times the national average, according to Hamilton Lombard, a demographer at the University of Virginia.

But while older populations are attracted by cheaper living and housing cost, lower crime levels and pleasant weather with fewer hurricanes, some locals are furious about the impact this influx is having on property prices, traffic and even restaurant bookings – with one resident saying ‘they should go back to where they came from’.

Southern Appalachia is becoming a thriving retirement community due to an aging and affluent population, but some local services are struggling to keep up

Helen (right), born and raised in Dawson, is not pleased with the influx of transplants moving to her rural neighborhood

Pictured: A map of Southern Appalachia in relation to the rest of the United States

Ed Helms, 75, and his wife moved from Panama City Beach, Florida to a gated community, half of it in Dawson and half in a neighboring county, to escape natural disasters, congestion, and the rising cost of living.

‘Our property insurance was going sky high,’ Helms, who worked in mergers and acquisitions, told the Wall Street Journal.

‘We got tired of being unable to find a place to sit in restaurants. Everything was getting out of reason. We wouldn’t go back for anything.’

People like the Helms are often referred to as ‘halfbacks’ – a nickname for those originally from the Northeast and Midwest who moved to Florida before eventually settling somewhere in the middle.

The trend back in the early 2000s and then slowed during the recession – but has now picked up again in earnest.

Gayle Manchin, the The Appalachian Regional Commission’s co-chair and wife of Democratic Senator Joe Manchin, told WSJ she believes the pandemic has fueled the retirees’ interest in moving back to more isolated, nature-filled areas.

According to Lombard of the University of Virginia, who has been tracking the pattern, an average of 328,000 individuals from other regions of the country have relocated to the five-state region of Georgia, Alabama, North Carolina, South Carolina, and Tennessee annually since 2020.

The Georgia county of Dawson has proven particularly popular, reporting a 12.5 percent population increase from 2020 to 2022, according to estimates by the U.S. Census Bureau.

But this huge influx has put enormous pressure on local services, leaving some lifelong residents like Helen Anderson unimpressed.

Anderson was born and raised in Dawsonville, Georgia, her family making ends meet by farming chicken and selling moonshine from the foothills of the Blue Ridge Mountains in Atlanta.

‘They ought to go back where they come from,’ she told the Wall Street Journal when discussing the newcomers.

Manchin told the WSJ that demand for affordable housing has skyrocketed as more workers are needed to serve the influx of halfbacks.

The migration of these wealthy retirees has spread governments thin as they trying to extend healthcare, housing, and other services to its citizens, she added.

But chairman of the Dawson County Board of Commissions Billy Thurmond noted that some of people who stop him to complain about the traffic and development are ironically the same people who moved to the county in recent years.

‘People who have moved here now want us to put up a gate and stop anybody else from moving here,’ he told WSJ. ‘It doesn’t work that way.’

County Manager Joey Leverette said medical calls to eldercare facilities in the county are also taking up resources. For that reason, county officials are considering splitting up staff to dedicate some to just emergency calls, freeing up teams to respond to fire calls.

‘It’s a game changer,’ Leverette told WSJ. ‘If we don’t get the funding, we’ll just have to keep plodding along as best we can.’

An average of 328,000 individuals from other regions of the country have relocated to the five-state region of Georgia, Alabama, North Carolina, South Carolina, and Tennessee annually since 2020

The population in counties in southern Appalachia designated as retirement or recreational areas grew by 3.8% -more than six times the national average -from April 2020 to July 2022

The demand for affordable housing has skyrocketed for the influx of new workers serving the halfbacks moving in

County Manager Joey Leverette said medical calls to eldercare facilities in the county are taking up resources

Retirees are leaving Florida in droves due to increased cost of living, natural disasters, and congestion

Southern Appalachia has been known for its rural and serene nature

The U.S. Census Bureau has projected further development for the county, according to a piece that the weekly Dawson County News recently shared on Facebook.

One person commented: ‘The entire south and southern living is being ruined.’

Linda Bennett, 81, has lived in Dawson County. Now that she is widowed, she resides in a home close to Georgia Route 400. She cherished being in the country, but she worries that North Georgia will never be the same with so many newcomers.

‘It has grown so much; it is just unreal,’ she told WSJ. ‘With all the houses and apartments they’re building, it’s not going to get any better. How could it?’

After her husband died, Delaware native Karen Rickards, 73, moved from Tallahassee, Florida to Dawson, Georgia.

A halfback herself, she is wondering how much more growth Dawson County can handle.

‘They are building house after house after house,’ she told WSJ. ‘Atlanta’s moving up here, no doubt.’

Thanks for joining me. We begin the day with the latest figures showing house prices increased for the first time in more than a year in February.

The average price of a home grew by 1.2pc in the year to February, rising for the first time since January 2023, making properties typically worth £260,420, according to the lender Nationwide.

5 things to start your day

1) Chinese EVs pose a threat to US national security, Biden warns | President’s comments come as the West braces for Beijing’s electric car shock

2) Public sector must temper pay demands or put frontline services at risk, says Treasury | Large wage increases remain unaffordable and are eating into departmental budgets

3) How the myth of the ‘state pension pot’ has warped Britain’s finances | National Insurance inconsistencies highlight the shaky position of retirement nest eggs

4) Sunak accused of ‘stealth amnesty’ on asylum seekers as immigration surges again | 1.4 million people granted UK visas in 2023 as arrivals hit 18-year high

5) Ben Marlow: Ocado has failed to deliver for M&S customers | The repeated dismissal of old-fashioned values has come back to bite the online apostles

What happened overnight

Facebook parent Meta announced it would no longer pay Australian media companies for news, prompting a government warning that the tech giant was in “dereliction” of past promises.

Extending a global retreat from news content, Meta said it would scrap the Facebook News tab in Australia and would not renew deals with news publishers worth hundreds of millions of dollars.

The decision had been on the cards, but will come as a hammer blow for Australian news outlets already struggling to stay afloat.

However, Australian shares hit fresh record highs – as did markets in Japan – as the key US PCE price index – the US Federal Reserve’s preferred measure of inflation – kept up hopes for a June rate cut.

Australia’s resources-heavy shares ASX 200 rose 0.6pd to a new record high of 7,745.6.

In Japan, the key Nikkei index almost touched 40,000 for the first time, rising 1.9pc, or 744.63 points, to close at 39,910.82, while the broader Topix index added 1.3pc, or 33.69 points, to 2,709.42.

China’s mainland markets were higher. The bluechips rose 0.4pc and Shanghai Composite index edged up 0.2pc, after rebounding nearly 10pc last month on the back of Beijing’s efforts to stop short-selling in the market.

Hong Kong’s Hang Seng index also reversed earlier losses to be up 0.6pc.

In America, the S&P 500 rose 0.5pc, to 5,096.27 to top its record set last week. The Nasdaq Composite index rose 0.9pc, to 38,996.39 and surpassed its all-time high that had stood since 2021. The Dow Jones Industrial Average of 30 leading US companies finished just below its record set last week after rising 0.1pc, to 38,996.39.

The yield on benchmark US 10-year Treasury bonds was little changed at 4.27pc.

Thanks for joining us. To kick off the week, we have figures showing that the asking prices for homes has increased for the first time in six months in a sign of confidence returning to the property market.

Rightmove said the average price of a property listed on its website has increased by 0.1pc compared to the same month last year, which was the first annual increase since July.

5 things to start your day

1) Currys draws takeover interest from Chinese giant | Prospect of bidding war emerges as JD.com enters talks with electricals retailer

2) Apple faces £430m EU fine in long-running row with Spotify | iPhone maker accused of using its App Store to drive up prices and block competition

3) Lockdown damage risks lasting for generations, warns World Bank | Children of those who missed out on school to be affected by ‘scars of pandemic’

4) John Lewis in fresh housing row over smoke vents in rental properties | Firefighters warn designs for Bromley scheme risk hampering potential rescue efforts

5) The economic cost of our crumbling mental health has finally become clear | As the country plunges into recession, Britain’s long-term sickness crisis demands serious action

What happened overnight

Shares were mostly higher in Asia after Chinese markets reopened Monday from a long Lunar New Year holiday.

Hong Kong’s Hang Seng fell 0.9pc to 16,192.24 on heavy selling of technology and property shares despite a flurry of announcements by Chinese state banks of plans for billions of dollars’ worth of loans for property projects.

Major developer Country Garden dropped 5.6pc and Sino-Ocean Group Holding plunged 6.5pc. China Vanke lost 4.6pc.

The Shanghai Composite index gained 0.8pc to 2,889.32.

Tokyo’s benchmark Nikkei index closed flat, as Nintendo shares tumbled after reports said its next console would be delayed.

The benchmark Nikkei 225 index edged down 16.86 points to end at 38,470.38, while the broader Topix index climbed 0.57 percent, or 14.96 points, to 2,639.69.

Nintendo’s shares sank 5.1pc following unconfirmed reports that the successor to the Switch console would not be delivered within this year.

Goldman Sachs said it expects the US stock market rally to surge even higher. In a note to clients, analysts forecast the S&P 500 would reach 5,200 by the end of 2024.

This would mean growth of 3.9pc on top of Friday’s close, after it dipped 0.5pc following a fresh record high on Thursday.

A rise in the US producer price index on Friday triggered a small rise in Treasury yields, which climbed by seven basis points to 4.65pc.

Think again if you believe every corner of Britain has seen house prices tumbling thanks to high inflation, soaring interest rates and the general cost of living crisis.

Despite the Office for National Statistics (ONS) announcing earlier this week that house prices in the UK have dropped £6,000 in 12 months (faster than they have in more than 12 years), there is a surprisingly large number of areas that have bucked the trend, giving hope that the 2024 housing market may be better than some of those gloomy predictions.

Kim Kinnaird, director of Halifax Mortgages, says national economic woes have been outweighed by local factors in many places. ‘House prices can be swayed by the number of homes for sale, the local jobs market and services like education and transport,’ she says.

And Nathan Emerson, chief executive of estate agents’ group Propertymark, says: ‘It’s inevitable the market becomes more fragmented than usual with some geographical areas performing better than others. Some parts of the UK have maintained stability with house prices, while some homeowners have actually seen their homes increase in value.’

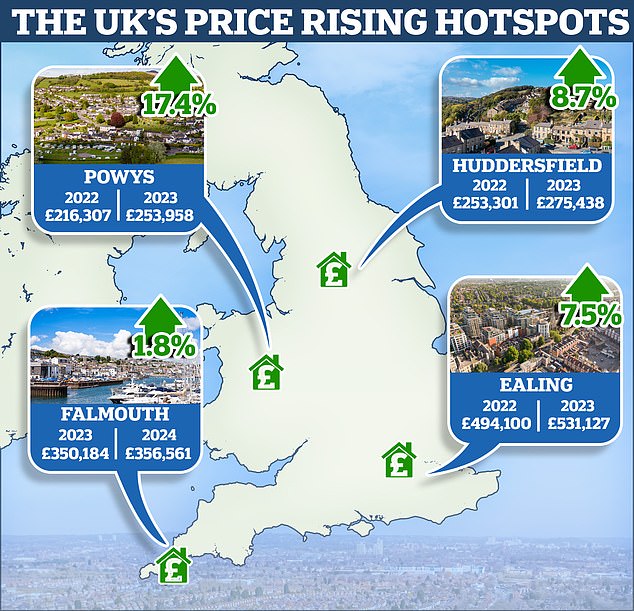

So, here are some of the big winners over the past year, despite economic headwinds.

Some of the property hotspots in the UK the past year include Powys in Wales, Huddersfield in West Yorkshire, Falmouth in Cornwall and Ealing in west London

FALMOUTH, CORNWALL

This port on the river Fal is the largest in Cornwall and has a rich history which began in 1613 when Falmouth was founded by Sir John Killigrew. Nearby is also Pendennis Castle which was built by Henry VIII in 1540 and is a major tourist attraction.

There’s been a marginal increase in house prices here, according to property consultancy Dataloft. At the end of 2022, a typical home in the town sold for £350,184, but a year later it was £356,561. This pretty, busy port hosts two university campuses so has a younger and more affluent population than most of Cornwall, producing a far wider range of restaurants, clubs and shops than usually found in the far South West.

The beautiful port on the river Fal in Cornwall has a rich history dating back to 1613

It hosts two university campuses so has a younger and more affluent population than most of Cornwall, producing a far wider range of restaurants, clubs and shops than usually found in the far South West

There is a farmers market every Tuesday, Thursday and Saturday as well as year-round live music and theatre in the Princess Pavilion, which is set in the middle of Gyllyngdune Gardens.

The actor Steve McFadden — who plays EastEnders hardman Phil Mitchell — has a second home in the town. It’s not far from the house formerly owned by Kaiser Chiefs frontman Ricky Wilson, who quit the Cornish port in 2020 when his career relaunched. He now hosts a daily show on Virgin Radio UK.

EALING, WEST LONDON

Halifax says the typical home here was valued at £494,100 a year ago, but now it’s up to £531,127 — a healthy 7.5 per cent rise. Much of the increase is down to the regeneration of the main shopping area and the arrival of Elizabeth Line, formerly known as Crossrail.

Now it takes a mere 12 minutes to get from Ealing Broadway to Paddington, and just 25 minutes to reach Tottenham Court Road in the heart of the capital.

A typical home in Ealing was valued at £494,100 a year ago, but now it’s up to £531,127

Ealing has its fair share of celebrity residents — Black Mirror creator Charlie Brooker lives there with his ex-Blue Peter presenter wife, Konnie Huq. It’s also home to more village-style living than most of the capital, courtesy of a Saturday Farmers’ Market and The Avenue Vintage and Antiques Market which draws crowds from across London.

Crowds flock to 28-acre Walpole Park which is home to the Pitzhanger Manor and Gallery, a children’s playground, a cafe, serpentine lake, fishponds and landscaped gardens. The park also hosts an annual Jazz Festival and a Beer Festival.

POWYS, WALES

Halifax says this has seen huge annual house price growth of 17.4 per cent. That’s taken the typical home from £216,307 to £253,958. Powys is the largest, but least densely populated county in Wales, much loved for its villages and market towns, and featuring a spectacular landscape of valleys and mountains including most of Brecon Beacons National Park.

The county covers a vast area and has the variety one might expect. In late spring each year, some of the industry’s biggest stars make the trip to Hay-on-Wye for the literary festival. The smallest town in Wales, Llanwrtyd Wells – with a population of just 850 people – is home to breweries, charming independent shops and hosts quirky events like bog snorkelling (exactly what it sounds like), all while being surrounded by the Cambrian Mountains.

A terraced row of quaint cottages sit alongside a canal near Brecon, in Powys

The Welsh county features a spectacular landscape of valleys and mountains

Welsh singer Charlotte Church spent 18 months renovating the Powys pile Rhydoldog House — the former home of designer Laura Ashley — into a health retreat called The Dreaming. ‘It’s for healing through beauty and wonder. It’s for everyone: affordable and inclusive, where anyone can learn to heal and even become the healer that their community needs,’ says the star.

Ex-Neighbours star Mark Little is another resident, in a farmhouse near Lake Vyrnwy and enjoys turning out for a local cricket team.

EXETER, DEVON

Prices in Exeter continued to rise in 2023, with a typical home costing £325,878, according to online agency Purplebricks. The city has garnered a higher profile reputation, thanks to its university joining the elite Russell Group and the premiership Exeter Chiefs rugby union club operating from a purpose-built ground with its own hotel.

There’s been a high volume of new housing built around the city, but the most popular suburb is one of its oldest. Topsham on the River Exe is an eclectic mix of 18th-century Dutch-gabled houses, renovated workers’ cottages and waterside villas.

Sitting on the River Exe, the picturesque city boasts a Russell Group university as well as the Exeter Chiefs rugby union club

The spectacular 15th-century Gothic cathedral is the centrepiece of this city and hosts events such as art exhibitions, talks and family-friendly workshops

Newly knighted Brexiteer pub king Sir Tim Martin lives here, while celebrity chef Michael Caines runs the nearby Michelin starred Lympstone Manor restaurant, hotel and vineyard.

The spectacular 15th century Gothic cathedral is the centrepiece of this city and hosts events beyond the usual services from art exhibitions, to talks and family friendly workshops. But there’s plenty more attractions on offer from the unique Underground Passages to the Roman Wall, beautiful quayside and the Royal Albert Memorial Museum dedicated to the city’s 2000-year history.

HUDDERSFIELD, YORKSHIRE

It’s famous as the birthplace of former Dr Who Jodie Whittaker and Labour ex-Prime Minister Harold Wilson, but now this Yorkshire market town — in the foothills of the Pennines — is in the news because typical house prices are up from £253,301 to £275,438, according to Halifax.

Home to approximately 162,000 people, the town has a strong sporting pedigree seen in its football club and the rugby league team the Huddersfield Giants. For those more culturally inclined, the Huddersfield central market is one of the largest in the UK, with over 100 stalls and there is a burgeoning food and drink scene.

The impressive Concert Hall sits in the heard of Huddersfield, where there is a burgeoning food and drink scene

The Lockwood railway viaduct, built in 1846, can be seen from nearby Beaumont Park

Local agents say the 8.7 per cent rise is down to the working-from-home trend, with many who would have moved to the likes of Manchester or Birmingham now wanting larger properties in the town with space for home offices. There are also plenty of green spaces including Greenhead and Beaumont Park.

They say the same goes for Bradford, another West Yorkshire town, where prices have gone up 8.5 per cent. Folk in Yorkshire like to buck the trend – and when it comes to property prices in some parts of the county they are doing just that.

Thanks for joining me. House prices declined at their lowest rate in a year in the 12-months to January amid hopes that the Bank of England will start cutting interest rates soon.

The Nationwide house price index showed that property values declined 0.2pc annually last month, having declined by 1.8pc across 2023.

5 things to start your day

1) Audit watchdog accuses HMRC of getting its sums wrong | Incorrect forecasting leaves the Treasury facing billion-pound shortfalls

2) Cruise giant forced to change itinerary after Red Sea attacks | Carnival reroutes 12 of its ships on around the world trips following months of disruption

3) How HSBC became the world’s most accident-prone bank | Battered lender scrambles to draw a line under a litany of recent regulatory run-ins

4) Jeremy Warner: Markets are fatally complacent about the risks of World War Three | The ‘great illusion’ that trade has made war less likely threatens to leave us perilously exposed

5) Ben Wright: Britain is in danger of throttling the university golden goose | Viewing third level admissions through the lens of immigration carries risks

What happened overnight

Asian stocks mostly declined as markets awaited a decision on interest rates by the Federal Reserve, while China reported manufacturing contracted in January for a fourth straight month.

Official data showed China’s manufacturing purchasing managers index, or PMI, rose to 49.2 in January, up from 49.0 in December, but still below the critical 50 mark that indicates expansion rather than contraction. Weak demand in the world’s second largest economy is dragging on growth.

South Korea’s Kospi shed 0.2pc to 2,494.30 after Samsung Electronics reported reported an annual 34pc decline in operating profit for the last quarter.

Hong Kong’s Hang Seng dipped 1.1pc to 15,536.00, while the Shanghai Composite shed 0.4pc to 2,819.91.

Tokyo stocks closed higher, with the benchmark Nikkei 225 index gaining 0.6pc, or 220.85 points, to 36,286.71, while the broader Topix index rose nearly 1pc, or 24.17 points, to 2,551.10.

Australia’s S&P/ASX 200 added 0.8pc to 7,657.20 after a survey showed Australia’s inflation rate fell to a two-year low in the December quarter, with the consumer price index at 4.1pc, leading to bets that the Reserve Bank may consider an interest rate cut in the next move.

American indexes saw little change on Tuesday, at least outside the technology heavy Nasdaq.

The S&P 500 dropped 0.1pc, from its record to 4,924.97. The Dow Jones Industrial Average of 30 leading US companies gained 0.3pc, reaching 38,467.31, while the Nasdaq Composite index fell 0.8pc to 15,509.90.

The yield on 10-year US Treasury bonds, the centerpiece of the bond market, fell to 4.04pc from 4.09pc late on Monday.