So long, 6% commission.

For decades, real estate commissions have been somewhat standardized, with most home sellers paying 5% to 6% commission to cover both the listing agent and the buyer’s agent.

On Friday, everything changed.

A landmark agreement from the National Assn. of Realtors paved the way for a new set of rules that will probably shake up the entire industry, affecting sellers, buyers and the agents tasked with pushing deals across the finish line.

The most pivotal rule change pertains to how buyers’ agents are paid. Traditionally, home sellers have paid for the commission of both their agent and the buyer’s agent, which critics argue stifled competition and drove up home prices.

The new rule prohibits most listings from saying how much buyers’ agents are paid, removing the assumption that sellers are on the hook for paying both agents.

The other new rule requires buyers’ agents to enter into written agreements with their clients, known as buyer brokerage agreements. These agreements outline exactly what services will be provided — and for how much.

The changes will take effect this July, pending court approval, and will have major implications on how real estate deals are done. Here’s how buyers, sellers and brokers will probably be affected.

Lower fees for sellers

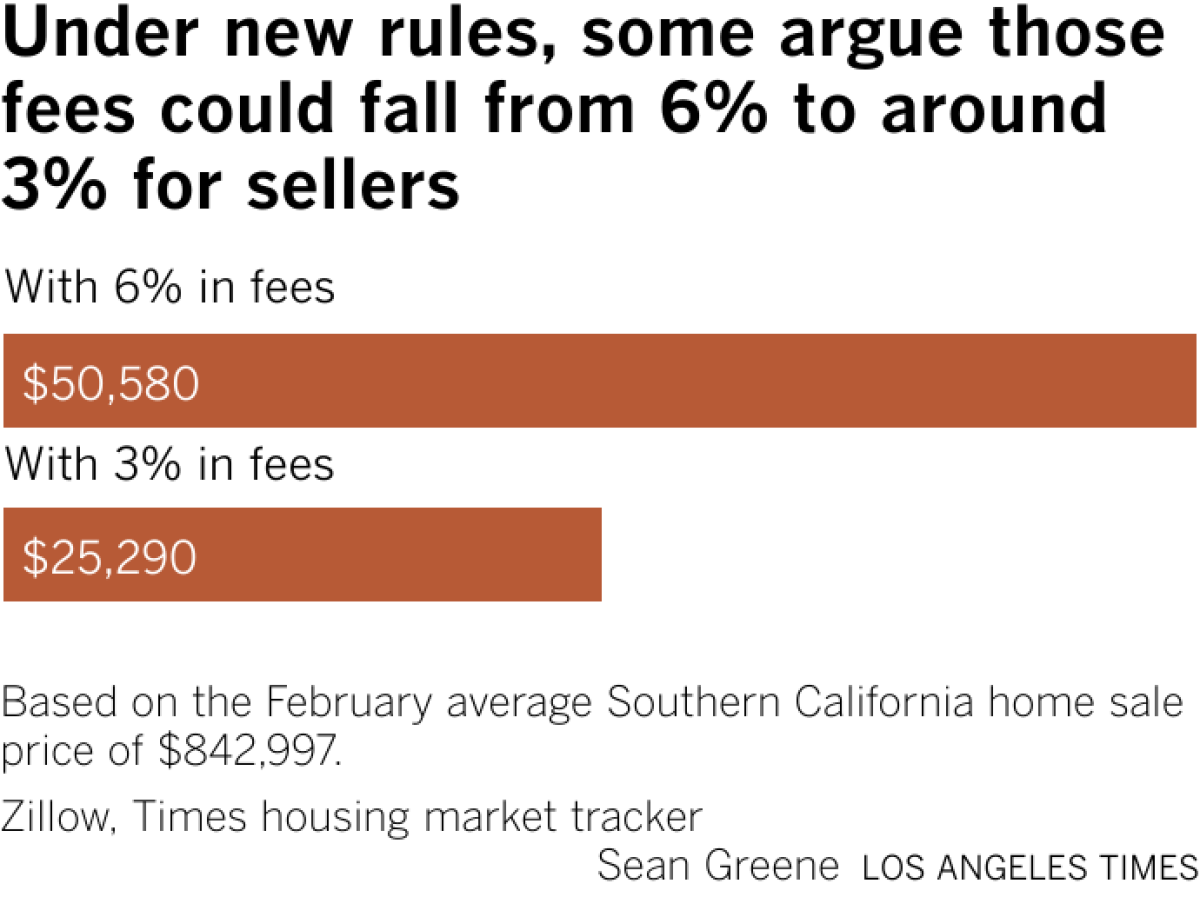

The most obvious takeaway is that if buyers end up paying for their real estate agents instead of sellers, sellers are set to save a lot of money.

In February, the average Southern California home sold for $842,997. Under the old system, where sellers pay both agents 3% commission, they’d shell out $50,580. But if they only have to pay one agent 3%, they’d save $25,290.

Buyers, then, would be the ones footing the bill for their agent. The added expense might seem pricey, but Michael Copeland, a real estate agent in Palm Springs, said the final numbers might ultimately shake out the same under the new rules.

“Buyers were often told by their agents that they didn’t have to pay anything and that services were free,” Copeland said. “But that’s not necessarily true.”

Copeland said when sellers pay 6% commission to split between both agents, they pad that number into the purchase price, so buyers actually end up paying more for the home, and thus, pay for their own agent.

So under the new system, buyers may end up paying their broker 3% commission, but the price of the home might be cheaper since the seller is only paying for their own agent.

More flexibility for buyers

One of the biggest complaints about the previous system was that it left buyers out of the negotiation process. Sellers paid each agent’s brokerage 3% or so, and that was that.

Lawsuits filed against the National Assn. of Realtors alleged that the practice kept commissions artificially high and incentivized buyers’ agents to “steer” them toward properties that offered them higher commission rates.

But under the new system, more buyers will be negotiating directly with their own agents — not just how much they’ll pay them, but what services they want the agent to provide. And those expectations will be specifically outlined in the buyer brokerage agreements, which are now required.

“Some buyers may just hire an attorney and pay a fee to handle the transaction,” Copeland said. “Or they’ll want to hire an agent as a consultant. Someone they can ask questions.”

In the age of the internet, access to real estate information is at an all-time high. Buyers can know virtually anything about a home on the market: not just bedrooms, bathrooms and square footage, but how much the home previously sold for, and how much similar homes in the area are selling for.

Buyers can also receive alerts to know exactly when a house in their price range hits the market, so some savvy shoppers might opt for an agent who leaves the touring process to them, but can help them look over an inspection report and file the right paperwork in the closing stages of the deal.

If a buyer wants a robust, hands-on agent that’s available 24/7, they can offer 3% or even more. If they want an agent who can just handle the more technical elements of the deal, they could offer 1% or 2%.

Some buyers might try to handle the process themselves and not pay an agent at all.

“Good agents will be able to show their value,” said Compass agent Michael Khorshidi. “Agents who aren’t able to show their value won’t benefit from this.”

New dynamics — and roles — for agents

For many agents, representing buyers can be rewarding since they get to help someone find their dream home, but the process is often more time-intensive. Agents might spend weeks or months setting up tours for clients, and there’s no guarantee that they’ll even buy a property in the end.

For that reason, many veteran agents prefer to represent sellers. The work is often more efficient — especially in a hot market, where deals can close in days.

So if the new rules leave less guaranteed money on the table for buyers’ agents, those agents might try to switch sides and only represent sellers. Or if they’re not able to make enough money representing buyers, they might exit the industry altogether — a trend that’s already taking place in Southern California’s cold post-pandemic real estate market.

Brent Chang, a luxury agent active in San Marino and Pasadena, said the new rules could lead to agents who specialize in specific types of sales.

“Just as there are agents like me who specialize in selling landmark properties, a new group of agents will emerge who specialize in helping buyers with highly competitive properties,” Chang said.

He said agents who have a proven track record of winning properties for their clients will be able to demand higher commissions.

Or their deals can be performance based. For example, an agent could represent you for 3%, and if they get the property for you, it’s another 3%.

“Ultimately, if the ruling leads to buyers receiving better service from their agents, then it has merit,” he said. “But I suspect it’ll be a while until we understand the consequences of these changes.”

Things are about to get weird for homebuyers and sellers.

I wrote late last year that 2024 would mark the beginning of a great experiment in real estate that would upend the way homebuyers and sellers pay their agents. Well, the experiment officially got underway Friday when the National Association of Realtors agreed to a $418 million settlement to bring to an end a series of class-action lawsuits over agent commissions.

The settlement came after a yearslong battle in which hundreds of thousands of sellers claimed that they were forced into paying unfairly high commissions to real-estate agents. In addition to the monetary penalties, the agreement could enable more buyers and sellers to start negotiating those commissions, which for decades have hovered between 5% and 6% of the sale price. The deal could also push more buyers to forgo hiring an agent or work out an alternate payment structure.

These changes, spread out over millions of transactions a year, have the chance to reshape the housing market. Some industry observers have predicted that the new commission rules could lead to a drop in both home prices and commissions. Buyers could even save as much as $30 billion every year, a recent working paper from the Federal Reserve Bank of Richmond estimated. But there’s also the possibility that the Department of Justice decides this settlement doesn’t go far enough, which could set up a showdown between the NAR and the DOJ. In other words, while the real-estate revolution is underway, this thing is far from over.

To grasp the scope of the settlement, it helps to understand how agents are paid. In most home sales, the seller uses a chunk of the final sale price to pay out the agents on both sides of the transaction. When a seller lists their home on the multiple-listings service — a database of local homes for sale where agents go to find homes to show clients — they advertise how much they’re willing to pay the buyer’s agent. For decades, sellers have generally offered buyers’ agents 2% to 3% of the final sale price, even though they can technically offer as little as $0. That’s because sellers fear that if they offer less than the industry standard, buyers’ agents will direct their clients away from their homes, a practice called “steering.” Don’t offer the standard rate; don’t get seen. To fix this issue, the plaintiffs in the lawsuits and the Department of Justice have pushed for a practice called “decoupling,” in which buyers and sellers just pay their agents separately. They argue that this would eliminate steering and push down commissions, saving people money and perhaps forcing many subpar agents out of the industry. A lot of agents are already barely scraping by — if their earnings fall, they might decide to exit the business altogether.

AP Photo/Rich Pedroncelli

The newly announced settlement doesn’t go quite that far. While sellers will no longer be required to say how much they’re offering a buyer’s agent when they list their homes on the MLS, they’re not expressly prohibited from offering that compensation somewhere else — it just can’t be anywhere on the MLS. There will likely be “a thousand work-arounds,” Bret Weinstein, the founder and CEO of the Denver brokerage Guide Real Estate, told me. A buyer’s agent could just call up the seller’s agent and ask what commission they’ll get, or the listing agent could advertise the commission tied to the home on their website. In theory, a seller might still offer compensation to a buyer’s agent because they want to get as many offers as possible on their home. If you’re a seller and you don’t offer anything, then any buyer who wants your home will have to pay their agent out of pocket, and a lot of cash-strapped buyers simply can’t do that. In some cases, sellers might still feel pressured to offer the going rate, so the agent’s commission could end up looking pretty much the same as it does today.

On the other hand, we’re likely to see both sellers and buyers negotiating on commissions in ways they simply haven’t before. If sellers are in a desirable market, they might start offering less commission to buyers’ agents, or none at all. On a $1 million home, a seller may save $30,000 if they don’t promise anything to the agent on the other side of the deal. This would force buyers’ agents to get more creative. They could work for a flat fee or cut their commission rate to attract price-sensitive clients. Some might offer varying levels of service for different prices — the white-glove treatment still goes for 3%, but just setting up a few showings is a cheaper rate. Other buyers might choose not to hire an agent at all or just get a lawyer to review contracts and make sure the transaction doesn’t go off the rails.

As for home prices, I’m not convinced they’ll actually drop as a result of this settlement. It’s hard to imagine a seller shaving 3% off their listing price just because they’re not offering a commission to the buyer’s agent, especially if a comparable house down the street is selling for a similar amount. Sales have slowed down with higher mortgage rates, but the seller still has the upper hand in most parts of the country.

The NAR will pay out a staggering amount of money to the class-action members (and their lawyers), but that $418 million pales in comparison to the billions of dollars in damages that the NAR and other major brokerages were facing as part of these lawsuits. In the first case to go to trial, in October, a jury slapped the NAR and its codefendants with $5.3 billion in damages. The settlement also doesn’t mean that the organization is off the hook just yet: One of the biggest remaining questions is what the Department of Justice will think of this proposed settlement, which still needs approval from a federal judge. Earlier this year, the department threw its support behind the idea of decoupling, or just having both sides pay their agents separately. It has made it clear that it doesn’t want sellers offering compensation to buyers’ agents. Instead, it proposed an alternative in which sellers don’t promise anything but buyers can still make offers that are contingent on getting some money back so they can pay their agent: “I’ll pay you $500,000, but you give me back $15,000 so I can cut a check to my broker.” The key difference is that the amount requested is negotiated between the buyer and their agent, not set by the seller.

So it seems like the newly announced settlement could fall short in the eyes of the department. But even if the DOJ isn’t able to push for more changes, this settlement could usher in a new era for the industry — one in which buyers and sellers no longer default to the standard commission rates that have prevailed for decades.

This settlement isn’t the end of this saga. The experiment is just beginning.

James Rodriguez is a senior reporter on Business Insider’s Discourse team.

The last month of 2020 should’ve been a happy time for real-estate agents. The catastrophe of the pandemic had turned into an improbable housing-market boom, as home sales reached 14-year highs. But instead of celebrating their unexpectedly prosperous year, a lot of agents were pissed.

In private chats and message boards, they complained about new rules that would publicly expose their commissions. For homebuyers, the amount an agent gets paid has historically been out of sight, out of mind. But as part of a November 2020 settlement between the Department of Justice and the industry’s top trade group, the National Association of Realtors, real-estate search sites like Zillow and Redfin would soon start publicizing exactly how much buyers’ agents stood to collect on nearly every home for sale in America.

Among real-estate agents, no topic is more sensitive than their commissions. In private comments at the time, screenshots of which were shared with Business Insider, agents revealed just how squeamish they were.

“It’s no one’s business,” one disgruntled agent commented in a private Facebook group. “Do we go around asking people how much they make?”

“Someone has it in for real estate,” another responded.

In the middle of the vitriol, a brave agent — whom I’ll call Julie — applauded the move, suggesting it could help rid the industry of one of its dirty secrets: a sly tactic called steering.

Because of America’s convoluted home-sales system, the seller typically pays out agents on both sides of a transaction. The commission is baked into the home’s final price — it’s usually between 5% and 6% of the total — and split evenly between the buyer’s and seller’s agents. Technically, the seller can promise as little as $0 to the buyer’s agent; after all, why pay for someone you didn’t hire? But there’s a catch: Offer less than the going rate, and you risk getting the cold shoulder from other brokers and fewer eyeballs on your listing. Agents might steer their clients toward the homes that offer the standard commission and away from ones that don’t. The practice screws over both sellers, who might miss out on offers, and buyers, who might unknowingly pass over their dream home.

“Whether or not people admit it, steering due to commission rate definitely happens and it is incredibly wrong,” Julie wrote in a Facebook comment.

“Wrong,” someone else replied, “or the real world?”

Steering is notoriously difficult to prove or quantify, but evidence of the practice can be found littered throughout the housing market. The extent of steering is a main point of contention in the multibillion-dollar class-action lawsuits over agent commissions; the plaintiffs say the threat of steering is a big reason commissions have barely budged over the years. Wendy Gilch, a consumer advocate who focuses on transparency in real estate with her company, Selling Later, likened this moment to “a reset button” for the industry.

“It’s a great opportunity to start over,” Gilch told me.

It’s hard to know how much steering actually happens, mostly because a buyer might never know they were a victim in the first place.

The first article in NAR’s code of ethics says Realtors must “protect and promote the interests of their client,” and the organization’s official position can be summed up simply: Steering doesn’t exist. It’s a myth, the argument goes, created by those who want to dismantle the system and force buyers and sellers to pay their agents separately. But multiple agents told me there are all kinds of ways shady practitioners try to skirt the rules.

For instance, some agents might filter out listings with subpar commissions before passing along options to their clients. Or if they do show their client a house, they could insinuate that a low commission is a warning sign that the seller is hard to deal with or invent reasons the house isn’t a good fit. They could also caution that if they’re not getting their desired commission from the seller, they’ll expect the buyer to make up the difference. Agents are within their rights to do that, but it can discourage a cash-strapped buyer from pursuing a home.

“All a Realtor has to do is make a face about a house and they put a question in the buyer’s mind as to whether or not it would be wise to put an offer in on a house,” Doug Miller, a real-estate attorney in Minnesota, said in an email.

Critics say the stickiness of the going commission rate is evidence of steering’s ubiquity. The cut that’s split between agents on both sides of the deal has basically fluctuated between 5% and 6% of the total sale price since at least 1992, despite the widespread adoption of home-search technology, an increase in the number of agents, and huge differences in agents’ experience and skill. In recent years, greater numbers of agents have been fighting for clients, while technology has streamlined their jobs and made it possible for anyone to look up homes online. In a competitive market, critics say, you’d expect the price of agents’ services to come down. But data from RealTrends indicates that in 2021, even as home prices were skyrocketing and agents were signing up en masse, the typical commission rate actually went up.

All a Realtor has to do is make a face about a house and they put a question in the buyer’s mind as to whether or not it would be wise to put an offer in.

A recent analysis of roughly 265,000 listings on Redfin in 34 large metropolitan areas found that, in a typical market, more than 85% of listings offered the two most common commission rates for buyers’ agents. In Austin, Houston, and Kansas City, Missouri, more than 95% of listings offered a commission to the buyer’s agent of 3% or 2.5%.

The authors of the study wondered whether buyers’ agents might forward fewer low-commission listings to their clients, which would mean fewer page views on sites like Zillow and Redfin. They found that, all else being equal, low-commission listings received significantly fewer page views on Redfin — even the homes that offered agent payments just slightly below the going rate got fewer eyeballs. Homes with lower buyer-agent commissions also took longer to sell and were less likely to sell at all than those offering the standard rate.

Agents I talked with stressed that there are plenty of honest, hardworking representatives who just want the best for their clients. I believe them. But there are also just lots of agents out there, and the bar for entry into the industry is shockingly low. In most states, getting a license to work as a real-estate agent requires paying a few hundred dollars, doing several weeks’ worth of coursework, and passing a multiple-choice test. It’s no surprise, then, that there are some 1.5 million NAR members, or more than two Realtors for every available home on the market. And that doesn’t even count all the agents who aren’t members of the organization — there are about 1.3 million licensees in the US who don’t belong to the group, meaning they can’t use the Realtor title and don’t subscribe to its code of ethics.

The low standards and lack of oversight can create hazardous conditions for buyers and sellers. A few years ago, the now defunct discount brokerage Rex Real Estate released recordings of roughly 600 calls in which other agents vowed to avoid properties listed by Rex that offered less-than-satisfactory commissions. In one call, court documents say, a Keller Williams agent told a Rex representative: “If you are not offering any buyer’s commission, then that’s fine. I’m not going to show that [property], and you’re probably going to run into the same issue with everybody here.” Another ReMax agent said, “I’m not going to show a listing where I’m not guaranteed a commission.”

Brendon Bowers, a former real-estate agent who spent a couple of years working as a branch manager for Rex in the Phoenix market, told me he encountered this sort of thing all the time. He said buyers’ agents might call and say, “‘Why is there no buyer’s commission?” or “Why do I have to negotiate this? Nevermind, we’re just going to go on to the next one.” Steering, he added, is “just flat-out a part of real estate.”

A spokesperson for the NAR told me that Rex was cherry-picking from thousands of calls and that these agents may have eventually shown their clients the homes, however begrudgingly. But even the mere threat of steering is enough to keep commissions from dropping, Stephen Brobeck, a senior fellow at the Consumer Federation of America, told me. The problem isn’t that steering is rampant, Brobeck said; if most listings in a market already offer uniform commission rates, there’s no need for an agent to steer their client in the first place. It’s the fear of steering that maintains the system. A seller might hear of examples of steering, or get a warning from their agent of the risks involved in offering substandard commissions, and decide it’s worth it just to promise the going rate. After all, everyone else is doing it.

Class-action plaintiffs, the Consumer Federation of America, and the Department of Justice have proposed something called decoupling, in which buyers and sellers just pay their agents separately, as a way to get rid of steering. The DOJ has argued that as long as sellers pay a commission to the buyer’s agents, they’ll be pressured to promise the going rate. In the proposed alternative, sellers would promise a commission only to their agent. For buyers, it would be more complicated; they’d have to figure out how to pay their agent directly, and how much. They could either pay the broker out of pocket or arrange to get a rebate from the seller once the deal closes.

Such changes could come sooner rather than later. With commissions under heightened scrutiny, more agents are getting buyers to sign buyer-broker representation contracts laying out the rate the agent expects to get paid, regardless of what the seller offers in the listing. If an agent wants 3% of the sale price and the house you buy provides only 2%, you might have to pick up the difference. If you’re working with a good agent, that will probably feel worth it. But if sellers stop offering commissions altogether, buyers might have to make some tough choices. Many more buyers might choose to go it alone rather than pay out of pocket for an agent’s services. Or they could pay their agents a flat fee or an hourly rate instead of a commission, though it’s unclear how many agents would take that deal. Buyers might also start writing offers on homes that are contingent on making sure their agent gets paid: “I’ll offer you $400,000 for your house, but you’ve got to give me back $12,000 so I can cut a check to my broker.” But there’s still no guarantee that sellers would agree to that, especially in a hot market like the one we’ve seen over the past few years.

Nobody expects agents to work for free, but the near uniformity of commission rates is strong evidence that buyers and sellers aren’t bargaining nearly as much as they should be.

The NAR says decoupling would only heighten the inequalities in the housing market. Rich people could afford to get an agent and enjoy all the benefits that come with one, while poorer buyers might be left on their own. Others in favor of decoupling say the industry would be forced to get creative to ensure that as many buyers as possible could still access agents. Meanwhile, buyers and sellers would negotiate harder and maybe save thousands of dollars on a sale.

Nobody expects agents to work for free, but the near uniformity of commission rates is strong evidence that buyers and sellers aren’t bargaining nearly as much as they should be. If you’re a buyer, there are steps you can take to avoid falling victim to steering. Be wary of relying too much on an agent to feed you listings; it’s worth doing your own research, too. On sites like Zillow and Redfin, you can often see the commission being offered to the buyer’s agent. If a listing is offering less than what’s typical in your area and your agent is acting weird about it, that might be a red flag. There are lots of willing brokers out there; if you suspect steering, agents told me, you’ve got plenty of options for a second opinion.

Again, there are good, honest agents out there who deserve every penny of their commission. But you don’t have to talk to many buyers to realize that not everyone meets that standard.

I recently called up Julie, the agent in the private Facebook group who spoke up about steering a few years ago. She asked that I not use her real name because she didn’t want to be drawn into the controversy over commissions and all the lawsuits the NAR is facing; if things were tense back in 2020, they’ve only gotten more heated since then. But her feelings about the issue hadn’t changed.

“I am responsible for taking care of my clients to the best of my ability,” she told me. “I tell my clients it’s not their job to provide for me. It’s my job to take care of them.”

James Rodriguez is a senior reporter on Business Insider’s Discourse team.

Home transaction volume tanked in 2023 as buyers and sellers became dissatisfied with the state of the real estate market. Would-be buyers became renters as mortgage rates surged to levels not seen since the turn of the century, hurting home demand and frustrating sellers.

But in the first month of 2024, those frustrations have started to fade into the background.

The real estate market may be in Goldilocks territory after an ugly year

Property prices rose by 1.4% year-over-year to $410,000 in January, according to a report from Realtor.com published on February 1. That steady growth threaded the needle in a departure from last year, as it seems to be neither unmanageable for buyers nor unacceptable for sellers.

To that point, the number of US homes listed jumped by 7.9%, Realtor.com found. New listings rose across the US, including 20% spikes in large cities like Denver, Seattle, and Miami.

An increase in housing supply is welcome news for buyers, considering the headaches that stemmed from the nation’s long-standing home shortage. That development seemed to spur more transactions, as the listings site noted that the time houses spent on the market was almost two weeks shorter than in January 2019, and four days shorter than last year.

“We are seeing increases in inventory and, importantly, gains in newly listed homes for sale indicating sellers are more ready to make moves,” Danielle Hale, the chief economist at Realtor.com, said in a statement for the report. She added, “time on market fell, signaling that buyers are ready to make offers on these new options.”

More properties to choose from and lower borrowing costs may lead to a modest resurgence in the housing market. Mortgage rates are down over one percentage point from their fall peak, though they’re still much higher than they were throughout the 2010s.

However, the picture isn’t all rosy for buyers. Home prices and mortgage rates are still above where they were last January, which means the monthly payment for a typical home with a 20% down payment is up 5.4%, or roughly $108, in the past 12 months — not counting tax and insurance costs. The silver lining is that growth is slowing, as costs in December were up 6.1%.

10 cities where prices are down

The outlook for buyers is finally improving, especially in cities where home prices are falling. Realtor.com tracks property statistics in the 50 largest real estate markets in the US and found that in January, 10 metropolitan areas saw their median listing price decline from 2023.

Below are those 10 cities with sliding property prices, along with the median home price, year-over-year growth for median home prices nominally and on a per-square-foot basis, the share of homes with reduced prices, and the growth of the share of homes with lower prices.

Things are not OK in Realtorland. The US housing market is still reeling from pandemic-era shocks, home sales are stuck in a rut, and mortgage rates, while inching downward, are still near two-decade highs. It’s a bad time to be a buyer, and maybe a worse time to be a seller.

Despite all this upheaval, there’s another story brewing in which the stakes for everyone in real estate, from agents to the average consumer, are even higher. It won’t have anything to do with the debate over whether you should put your hard-earned cash toward rent or a down payment. Instead, it’ll be about court cases.

The biggest threat facing the industry is a mounting wave of class-action lawsuits that accuse the National Association of Realtors, along with some of the country’s biggest real-estate brokerages, of conspiring to rip off consumers by keeping the commissions paid to agents unfairly high. These cases are expected to reach major milestones in the next year, and the ramifications could be staggering: Tens, if not hundreds, of billions of dollars hang in the balance. Hundreds of thousands of Realtors could see their commissions slashed, which might force many out of the business. The old way of buying and selling homes could go away forever.

2024 will mark the beginning of a great experiment in real estate. The status quo won’t change overnight — there will be more courtroom showdowns before that happens — but some forward-thinking brokerages and agents, as well as a handful of startups, are already trying to figure out what comes next. Things are about to get really weird — and for American homebuyers, that could be great news.

The old way in jeopardy

If you’ve bought a home, you probably never cut a check to the agent who held your hand through the ordeal. For decades, agent commissions have been mostly out of sight and out of mind for homebuyers. But in 2024, many buyers and sellers may have to start thinking hard about just how much they’re willing to pay their real-estate agents.

When a house trades hands, the money usually works its way down a circuitous path — the buyer pays the seller, who uses a slice of that sum (usually 5% to 6% of the final sale price) to pay their agent, who then splits that money with the buyer’s agent. I’ve previously written about why the system works this way and the arguments for and against the model, but as a recap: Consumer advocates say this setup discourages market competition between agents. If you’re a buyer, you want to pay as little as possible, but your agent stands to make more if the home price goes up. Plus, it’s the seller who decides what percentage each agent will make before even listing their house. As John Kwoka, an economist and antitrust researcher at Northeastern University, told me: The incentives aren’t aligned.

There are going to be real-estate agents who are not able to articulate, let alone demonstrate, their value. Those folks will probably be out of the business very quickly.

On the other hand, the NAR argues the system is designed to get a deal closed as efficiently as possible. When an offer comes in, there’s no bickering over commissions — everyone already knows who will get paid what. And the NAR, as well as the brokerages named in the lawsuits, has maintained that commissions are always negotiable. If you’re a seller and you want the agents to split only 1% of the sale price — or even 0% — you can do that.

The first major lawsuit to put this argument to the test, Sitzer/Burnett v. NAR, went to trial in 2023 — and it wasn’t pretty for the real-estate establishment. On Halloween, jurors deliberated for just a few hours before finding the defendants liable, siding with thousands of home sellers who claimed they’d been strong-armed into paying their agents the customary 5% to 6% of the sale price and dishing out $5.3 billion in damages.

And if the case has cracked open the door to major changes to the commission model, 2024 is shaping up to be the year it’ll be knocked down. The first thing to watch for will be an official ruling from the judge in the Sitzer/Burnett case, expected sometime in the spring. While the jury has already sided with the plaintiffs, the judge still needs to decide which kinds of actions the NAR and the brokerages will need to take to remedy the situation. In this case, it’s pretty clear what the plaintiffs and their lawyers want: They argue for “decoupling,” or changing the rules to make sure that buyers and sellers pay their agents separately. At the most extreme end, buyer’s and seller’s agents might be expressly prohibited from splitting commissions. The NAR has vowed to appeal the verdict, and said it expects arguments to take place later in 2024.

In addition to a ruling on the issue of decoupling, a larger case, Moehrl v. NAR, should reach trial in the last quarter of 2024. That suit involves sellers from a broad swath of the US, including Dallas, Phoenix, Philadelphia, and Miami, and damages could stack up to more than $40 billion.

Other class-action attorneys are bringing lawsuits as well. The two big cases so far have focused on home sellers, but a new case filed in November, known as Batton 2, takes aim at brokerages such as Douglas Elliman, Compass, and Redfin on behalf of a nationwide group of buyers. It’s not yet clear how big the damages could be in this case, but the sheer size of the plaintiff class points to a much-larger figure than that of the Moehrl case.

Meanwhile, the head plaintiff in the Sitzer case has filed another nationwide class-action suit against the NAR and brokerages that weren’t included in the original case, including Compass, eXp, and Redfin. While these cases won’t reach trial anytime soon, they put increasing pressure on the industry to find ways to settle, rather than risk years of time-consuming and costly litigation.

A new age of experimentation

Some real-estate agents may wait until a ruling from the judge in the Sitzer/Burnett case before changing their practices, or hold out hope until the last appeal has worked its way through the courts. Others have read the writing on the wall and are already starting to get creative with how they get paid.

“It’s a matter of allowing alternatives to be experimented with and see what sticks,” Kwoka, the Northeastern economist, told me. “We’re about to do that, ready or not.”

Even those who think the jury got it wrong are accepting that commissions are likely going to change. That group includes Brian Boero, the CEO of 1000watt, a brand and strategy agency that advises real-estate brokerages and mortgage companies. Boero said he’s busy prepping his clients for the reality of decoupling, a scenario that he expects to arrive “sooner rather than later.” According to Boero, the key for agents is to clearly explain to buyers what they do, how they get paid, and why they may need to start getting paid differently. In many instances, those conversations have been conveniently swept under the rug for decades.

“There are going to be real-estate agents who are not able to articulate, let alone demonstrate, their value,” Boero told me. “Those folks will probably be out of the business very quickly.”

Many buyer’s agents — at least the competent ones — will be fine. After all, despite all kinds of technological advances, more people are using agents today than they were before the pandemic.

“You would be foolish to buy a home without an expert helping you,” Boero said. “But I also think that a smaller, smarter, more professional real-estate industry is going to come out of this, and I think that’s a good thing.”

The Good Brigade/Getty Images

Decoupling also opens the door to further experimentation with agents’ fees. Joe Stockton, an attorney who previously worked at Zillow and has spent years thinking about creative fee arrangements, described to me one possibility: a tiered system in which buyers pay more for progressively broader offerings. At the top would be the “white-glove service,” or what you might expect of a sought-after agent today — the market insights, the pavement pounding in search of the best deals, all those hours spent advising and consoling and haggling with the sellers. Something like this could command $250 an hour, like a good lawyer, but be capped at some percentage of the sale price, like 3.5%. The tier below would offer good service but wouldn’t go above and beyond, and would notably exclude all that initial legwork; the agent could step in once you’d already found your options online and would command a smaller fee, like 1.5% of the sale price. At the most basic level, an agent could charge $2,000 for just making sure that nothing goes awry — you’d get none of the hand-holding and advisory services, but you wouldn’t have to pay for them, either.

“In either situation, a one-size-fits-all compensation model and fee structure doesn’t make sense,” Stockton told me. “In this new world order, the agent and the client will have the flexibility to negotiate something that makes sense for them both.”

It’s a matter of allowing alternatives to be experimented with and see what sticks. We’re about to do that, ready or not.

Right now, agents are mostly incentivized to close a transaction quickly — a $10,000 difference in the sale price would shift the amount an agent gets paid by only about $300 on the high end. But there’s a world in which a buyer’s agent’s cut goes up if they’re able to knock $50,000 off the list price, or if they find you a deal below a certain dollar amount that meets your criteria. Similar incentives could be baked into the commission for a seller’s agent as well. Nic Johnson, the CEO of ListWise, is working on such a solution: The company proposes a model in which agents bid for listings, which effectively sets the terms for how much they want to make if they’re able to boost the price of your home. So while an agent might be guaranteed only a 0.75% commission if the home sells for a predetermined baseline price, they may stand to increase that cut by several percentage points if the price goes up by $50,000 or $100,000.

“You need to make it so that the agent’s pay meaningfully varies based on different sale prices,” Johnson told me. “To me, that’s really the important thing: making sure the agent’s incentives are aligned with the homeowner’s.”

This all sounds pretty good for regular buyers and sellers — lower fees, a clearer picture of what you’re paying for, and a greater emphasis on negotiating rather than accepting the status quo. An analysis from a senior fellow at the Consumer Federation of America estimated that American consumers could save as much as $20 billion to $30 billion every year if commission rates fell in line with those of other developed markets, such as Australia, the Netherlands, and the UK. But there may be downsides, particularly for buyers who might not have enough cash on hand to pay their agents out of pocket. There are possible solutions — industry bigwigs could push for changes to mortgage rules so that commissions would be folded into a loan, or sellers could agree to give buyers rebates so they can pay their agents after a sale closes — but they’re far from guaranteed at this point. In the absence of those kinds of fixes, some homebuyers might be forced to accept less help on their purchase or even decide to brave the market alone.

These kinds of questions won’t all be resolved in 2024, but this coming year will mark the beginning of an experiment that could alter real estate beyond the typical boom-and-bust forces of mortgage rates and home prices. It’s time to prepare for a new world that’s rapidly approaching — one in which tinkering with agents’ fees will migrate from the periphery to the mainstream.

“It’s a matter of driving out excess costs,” Kwoka, the economist, said. “But more importantly, it’s just a matter of allowing for new arrangements to see if they work.”

James Rodriguez is a senior reporter on Business Insider’s Discourse team.