The National Association of Realtors (NAR) has reached a $418 million settlement after a federal jury ruled that the organization and major brokerages had conspired to inflate broker commissions. The Corcoran Group founder Barbara Corcoran joins Yahoo Finance Live to discuss the impact of this settlement on prices in the housing market.

Corcoran believes that the ruling will not alleviate high housing prices. She highlights that the low housing inventory and increased demand have led to even more price increases. Despite this, Corcoran explains why people looking to buy homes should do so “right now. “It’s always my mantra,” she adds, “Not because I’m an ex-real estate broker by any means…but it always is true that the minute you go out into the marketplace when everyone else is out, you’ll always pay more. Why would you way for that?”

For more expert insight and the latest market action, click here to watch this full episode of Yahoo Finance Live.

Editor’s note: This article was written by Angel Smith

Video Transcript

– So Barbara, you mentioned confusion, and I think a lot of people are confused, me included, about what this is going to do to the price of homes, right? Because you have the argument out there that if you’re not paying for a fee here, an agent fee, then it makes more sense for the home seller, maybe they could list their house, their home a little bit more– maybe they’ll list it less because they’re not having to deal with those fees.

Then you also have the other side of the argument where this could actually attract more people into potentially buying a home, and get them off the sidelines here if we do see a drop in fees. What’s the ultimate impact on home prices?

BARBARA CORCORAN: I don’t really believe either of those things are going to happen. It’s a neutral. Think of yourself. If you’re selling your home, and if you, let’s say you save 3% with a new ruling and say, I don’t want to pay the buyer’s broker the extra 3%, do you think you’re going to pass that along to the buyer, which a lot of people are saying is the case?

No. Sellers are greedy. It’s a one-time chance to get the most for your house and you’re not going to give that money away. So if you think prices are going to come down, definitely not the case. There is such a shortage of houses right now, that prices have gone up despite everybody singing the blues. 9% this year, pardon me, 6% this year, how did that happen? It happened simply because of supply and demand. There’s a lot of buyers and not enough houses to be available. And that’s what rules the market.

– Do you see prices continuing that move to the upside?

BARBARA CORCORAN: I think the prices are going to go through the roof, especially if interest rates come down another point by year end. I think everybody and their mother and their in-laws is going to come out looking for a new house. And the competition is going to be so fierce that house prices will have to go up.

– So when should people be buying?

BARBARA CORCORAN: Right now, but that’s always my mantra. Always the best time to buy [COUGHS] not because I’m an ex real estate broker, by any means, but I’m sure I’m biased in my attitude toward it. But it always is true that the minute you go out in the marketplace when everybody else is out, you always pay more. Why would you wait for that?

Are home prices about to fall?

That’s the question many of us are asking after the National Association of Realtors, the trade group representing the industry, agreed to cough up $418 million as part of an antitrust lawsuit alleging that the group had artificially inflated realtor commissions that home sellers pay — which, in turn, helped inflate home prices.

Until now, home sellers paid about 6 percent of the sale price toward a fee that would be split between their own agent and the buyer’s agent. Experts are divided on exactly how much impact this will have on home buyers, who will now likely have to start paying their agents themselves. The median sale price of homes as of late 2023 was about $417,700 — 6 percent of that amounts to a little over $25,000.

As Business Insider’s James Rodriguez noted, lower fees don’t automatically mean homes will be cheaper. In certain cases, it’s possible that sellers might list their home for the same price they would have before the settlement, and pocket more of the sale. But lower commission fees can also encourage more homeowners to list their property on the market, which could lower house prices overall.

The fact is, this real estate settlement is still too new for anyone to know for sure what the ripple effects will be. But one potential winner is tech companies in the real estate space, such as Zillow and Redfin, which have made it more feasible for people to start the home-buying process on their own instead of with a real estate agent. Vox spoke to Sonia Gilbukh, a real estate professor at City University of New York, Baruch College, to explore some of the possible outcomes.

The following conversation has been edited for length and clarity.

What was the problem with the old way realtor commissions worked? And how does this settlement change that?

It used to be that when a seller hired their agent to list a property for sale, they were paying the full commission for the transaction, which was approximately 6 percent — sometimes 5 and a half. The selling agent would then offer about half of that commission to the buyer’s side. Then the buyer’s agent will bring their clients to show all the properties, and if they end up buying the house, [the buyer’s agent] would be entitled to that commission that the seller agent was advertising for the property.

There were several rules that were part of the NAR settlement. Can you explain the new rule that sellers can’t advertise buyer agents’ commissions on the multiple listing service, or MLS, the portal that many realtors subscribe to in order to share and receive information about for-sale homes?

Yes, so the settlement is that they can no longer say, “I’m going to offer the buyer agent 3 percent,” for example, or 2.5 percent. So now, what happens is that the buyer’s agent basically would have no way to know whether they’re going to be paid for the work that they do. So something will have to change. Most likely, the buyer agents will have to directly negotiate with the buyer on the commission that they’re going to receive on a transaction.

Is it still possible that the seller’s agent would pay the buyer agent’s fee?

I think if they really wanted to, they could still post it on their website — there are ways to communicate that. But I think it would be harder to sell that as an industry standard, to the seller. Because the way it worked before is that the selling agent would say, “If you want to sell your house, we have to offer the buyer agent 3 percent, the industry standard. If we don’t, then the buyer agents are not going to show your house to their clients and you’re not going to be able to sell.” Now I feel like it would be harder to make that argument.

I’m guessing that new ways of compensating buyer agents will emerge — maybe some flat fee services, or they’ll negotiate to get paid a percentage of the deal but out of the buyer’s pocket. I don’t think they’re going to be able to keep the status quo.

I’ve been seeing in various reports that the old system, of the seller paying both agents, incentivized a practice called “steering.” Can you explain what that is, and is it really common?

Steering is a practice where the buying agent will not show, or discourage their buyers from properties that offer lower commissions.

Maisy Wong, Panle Jia Barwick, and Parag Pathak have a paper called Conflicts of Interest and Steering in Residential Brokerage, and they show that when buyer agents are offered less than the industry standard, the homes have more trouble selling. That’s basically their conclusion, that the buyer agents are steering their clients away from homes that offer lower commissions to them. I think there’s some potentially alternative explanations — if you offer less commission than the standard, maybe you’re particularly hard to deal with, difficult to negotiate with. But we certainly do see that in the data, that if you’re offering less than the standard, you were potentially jeopardizing your sale outcomes.

The plaintiffs for this lawsuit were home sellers. Beyond lower fees, what does this mean for sellers? Are there other benefits for them?

Well, we don’t know what’s going to happen, but let’s say that they’re no longer responsible for the buyer commission, then the sellers are going to be paying a 3 percent transaction cost. Now, of course, most people who sell their house also then buy a different house — so they’re still going to be paying the buyer commission on the new house that they buy.

I think what’s going to come out of this decoupling of the commission — that the buyer is going to pay for their agent, the seller’s going to pay for their agent — is that the commissions are going to become more negotiable.

And what will happen for buyers? Will some of them forgo hiring a realtor at all? Will the process of searching for a home look different?

I was talking to my mother-in-law, who is a real estate agent, and she actually owned a brokerage before. She was telling me that she views buyers to be in one of two categories: Either you’re a first-time buyer, or you’re somebody who’s selling their house and also buying something else. Those who are selling and then buying, they probably have a relationship with their agents, they probably want their agents to help them buy. So it could be a similar scenario of the status quo for them, with the possibility of maybe shaving a little bit more off the commission.

For new buyers, I think the option of paying a flat fee is going to be more attractive, because it’s going to be cheaper for them to pay a flat fee of, say, $2,000 for you to help me navigate the paperwork or something like that.

Will this mean that home prices fall?

I think eventually, if the transaction costs are going to fall, because the commissions are going to become cheaper and more negotiable. That will put a downward pressure on houses — I also think that will bring more people to sell their homes, because the transaction fee falls, people are going to be more likely to move.

I see. But you said “eventually,” so it’s not necessarily something we might see right away.

Yeah, I think it’s hard to know what’s going to happen — how buyer agents are going to be compensated, and [if] we still have buyer agents at all. We’re in this period of murky transition. For now, it’s pretty easy to sell because there’s just not a lot of inventory. But there’s not a lot of transactions actually happening.

I’m curious why we used this structure in the first place. Why have sellers typically paid both selling and buying agents?

It became the industry standard [in a period when] we had no information out there. We didn’t have Zillow. So buyer agents had a monopoly on information; if I’m not compensated as a buyer agent, or if my compensation is uncertain, then I’m going to only show [clients] the listings where I’m also the seller agent. When the commission structure changed, it improved the cooperation between agents, so they ended up showing their clients listings from other agencies. So that was actually really good.

But of course, now we have Zillow. And the potential for [buyer agents] to steer their clients only to their listings is very limited right now. There’s sort of no need for this system anymore.

Since commissions have historically been paid as a percentage of the sale, did that incentivize agents to show more expensive listings?

For the selling side, they have the incentive to sell at the highest price, essentially. But when you talk to agents, their main objective is to have the transaction happen in the first place. If they put the price too high, they risk the transaction not happening at all, then it’s not really a good trade-off. There’s also this thinking that the big houses sort of subsidize the salaries of the agents, who then also work with cheaper homes.

Some experts seem to think that this settlement will mean some real estate agents exit the industry. Do you think that’s likely? And if there are fewer realtors, is that good or bad for home buyers?

I think that’s very likely. I think most new people who come into the profession start out as buying agents, so if their compensation is going to fall, it’s not going to be worth it for them to enter anymore.

I do think it’s a good thing overall. I actually have a paper, with my co-author Paul Goldsmith-Pinkham, about the experience of real estate agents, and we find that over a quarter of all agents in the market have no experience at all. I think those are the people most likely to exit. As a result, we’re going to have more experienced real estate intermediaries, and more competitive pricing. So I do think it’s overall a good thing for consumers.

What’s the housing market like right now? Is it a seller’s market or a buyer’s market?

I think it’s still a seller’s market, but it’s sort of artificial, because we still have pretty low inventory. So yes, houses are selling quickly, but mostly because there aren’t a lot of homes for sale. Once we’re past this lock-in period — right now, most of the homes have been sold on really low mortgage rates, so it’s hard for sellers to sell and buy something new, because mortgage rates are so much higher. But eventually people will start moving, and eventually they’ll be paying off their loans. So maybe eventually the [mortgage] rates will also drop.

What else is possible in terms of reform and change in the real estate industry?

They could just straight-up outlaw sellers paying buyer commissions — but the current settlement essentially all but does that.

Are there reasons other than the long-term possibility of lower home prices for sellers and buyers to get excited about this settlement? Just how important is it?

I think it’s important. I think there’s going to be more experienced agents out there to represent buyers and sellers. I think the prices are going to drop — a little or a lot, we don’t know yet — but I think they’ll have to adjust. I think there’s going to be more people willing to move homes because the transaction cost of doing that is going to be lower.

The point you make about more homes just being on the market — that seems huge, because as you said before, one of the biggest roadblocks we’re facing is low inventory.

Yes, yeah.

I do want to say that, even though I’ve done extensive research on inexperienced agents, I do think that experienced professionals are really valuable. People should seek help, because [buying a property] is the most important transaction in their lives, probably.

Things are about to get weird for homebuyers and sellers.

I wrote late last year that 2024 would mark the beginning of a great experiment in real estate that would upend the way homebuyers and sellers pay their agents. Well, the experiment officially got underway Friday when the National Association of Realtors agreed to a $418 million settlement to bring to an end a series of class-action lawsuits over agent commissions.

The settlement came after a yearslong battle in which hundreds of thousands of sellers claimed that they were forced into paying unfairly high commissions to real-estate agents. In addition to the monetary penalties, the agreement could enable more buyers and sellers to start negotiating those commissions, which for decades have hovered between 5% and 6% of the sale price. The deal could also push more buyers to forgo hiring an agent or work out an alternate payment structure.

These changes, spread out over millions of transactions a year, have the chance to reshape the housing market. Some industry observers have predicted that the new commission rules could lead to a drop in both home prices and commissions. Buyers could even save as much as $30 billion every year, a recent working paper from the Federal Reserve Bank of Richmond estimated. But there’s also the possibility that the Department of Justice decides this settlement doesn’t go far enough, which could set up a showdown between the NAR and the DOJ. In other words, while the real-estate revolution is underway, this thing is far from over.

To grasp the scope of the settlement, it helps to understand how agents are paid. In most home sales, the seller uses a chunk of the final sale price to pay out the agents on both sides of the transaction. When a seller lists their home on the multiple-listings service — a database of local homes for sale where agents go to find homes to show clients — they advertise how much they’re willing to pay the buyer’s agent. For decades, sellers have generally offered buyers’ agents 2% to 3% of the final sale price, even though they can technically offer as little as $0. That’s because sellers fear that if they offer less than the industry standard, buyers’ agents will direct their clients away from their homes, a practice called “steering.” Don’t offer the standard rate; don’t get seen. To fix this issue, the plaintiffs in the lawsuits and the Department of Justice have pushed for a practice called “decoupling,” in which buyers and sellers just pay their agents separately. They argue that this would eliminate steering and push down commissions, saving people money and perhaps forcing many subpar agents out of the industry. A lot of agents are already barely scraping by — if their earnings fall, they might decide to exit the business altogether.

AP Photo/Rich Pedroncelli

The newly announced settlement doesn’t go quite that far. While sellers will no longer be required to say how much they’re offering a buyer’s agent when they list their homes on the MLS, they’re not expressly prohibited from offering that compensation somewhere else — it just can’t be anywhere on the MLS. There will likely be “a thousand work-arounds,” Bret Weinstein, the founder and CEO of the Denver brokerage Guide Real Estate, told me. A buyer’s agent could just call up the seller’s agent and ask what commission they’ll get, or the listing agent could advertise the commission tied to the home on their website. In theory, a seller might still offer compensation to a buyer’s agent because they want to get as many offers as possible on their home. If you’re a seller and you don’t offer anything, then any buyer who wants your home will have to pay their agent out of pocket, and a lot of cash-strapped buyers simply can’t do that. In some cases, sellers might still feel pressured to offer the going rate, so the agent’s commission could end up looking pretty much the same as it does today.

On the other hand, we’re likely to see both sellers and buyers negotiating on commissions in ways they simply haven’t before. If sellers are in a desirable market, they might start offering less commission to buyers’ agents, or none at all. On a $1 million home, a seller may save $30,000 if they don’t promise anything to the agent on the other side of the deal. This would force buyers’ agents to get more creative. They could work for a flat fee or cut their commission rate to attract price-sensitive clients. Some might offer varying levels of service for different prices — the white-glove treatment still goes for 3%, but just setting up a few showings is a cheaper rate. Other buyers might choose not to hire an agent at all or just get a lawyer to review contracts and make sure the transaction doesn’t go off the rails.

As for home prices, I’m not convinced they’ll actually drop as a result of this settlement. It’s hard to imagine a seller shaving 3% off their listing price just because they’re not offering a commission to the buyer’s agent, especially if a comparable house down the street is selling for a similar amount. Sales have slowed down with higher mortgage rates, but the seller still has the upper hand in most parts of the country.

The NAR will pay out a staggering amount of money to the class-action members (and their lawyers), but that $418 million pales in comparison to the billions of dollars in damages that the NAR and other major brokerages were facing as part of these lawsuits. In the first case to go to trial, in October, a jury slapped the NAR and its codefendants with $5.3 billion in damages. The settlement also doesn’t mean that the organization is off the hook just yet: One of the biggest remaining questions is what the Department of Justice will think of this proposed settlement, which still needs approval from a federal judge. Earlier this year, the department threw its support behind the idea of decoupling, or just having both sides pay their agents separately. It has made it clear that it doesn’t want sellers offering compensation to buyers’ agents. Instead, it proposed an alternative in which sellers don’t promise anything but buyers can still make offers that are contingent on getting some money back so they can pay their agent: “I’ll pay you $500,000, but you give me back $15,000 so I can cut a check to my broker.” The key difference is that the amount requested is negotiated between the buyer and their agent, not set by the seller.

So it seems like the newly announced settlement could fall short in the eyes of the department. But even if the DOJ isn’t able to push for more changes, this settlement could usher in a new era for the industry — one in which buyers and sellers no longer default to the standard commission rates that have prevailed for decades.

This settlement isn’t the end of this saga. The experiment is just beginning.

James Rodriguez is a senior reporter on Business Insider’s Discourse team.

The National Assn. of Realtors on Friday said it will make changes to its commission rules to settle national allegations the requirements stifled competition, a move that may reduce costs for at least some consumers.

The settlement, which still must receive court approval, could mark a major change in the housing market.

Today, sellers typically pay a 5% to 6% commission when they sell their homes, with half of that going to the listing agent’s brokerage and half to the buyer agent’s brokerage, and critics of that model say the settlement could upend that practice.

“This settlement over time will benefit home sellers and buyers greatly, eventually lowering agent commissions by tens of billions of dollars a year and helping align agent compensation and services rendered,” Stephen Brobeck, a senior fellow with the Consumer Federation of America, said in a statement.

Under an existing Realtor rule, listing agents must make an offer of compensation to the buyer’s broker in order to list homes on NAR-affiliated multiple listing services, or the MLS.

Though NAR says this offer can be zero dollars, the requirement to post an offer — known in the industry as “cooperative compensation” — has reduced competition and kept commission rates artificially high, according to lawsuits filed against the Realtors. The rule has also caused buyers’ agents to “steer” their clients to homes that offer higher commission rates, the lawsuits allege.

In a news release, the national trade group said it continues to deny any wrongdoing as it relates to its current commission rule, but to settle the allegations, it will pay $418 million and prohibit offers of compensation to buyers’ brokers on affiliated multiple listing services, which also populate listings on sites such as Zillow and Redfin.

“NAR has worked hard for years to resolve this litigation in a manner that benefits our members and American consumers,” Nykia Wright, interim chief executive of NAR, said in a statement. “It has always been our goal to preserve consumer choice and protect our members to the greatest extent possible. This settlement achieves both of those goals.”

Home sellers could still offer to pay buyers’ broker commissions under the settlement if they communicated it outside the MLS, according to the National Assn. of Realtors.

But not setting the rules of the game at the outset will inject more competition into the process and open up new ways of payment that should lower costs, according to Robert A. Braun, a partner with Cohen Milstein Sellers & Toll, which is representing home sellers in two of the settling cases.

Braun said sellers may still choose to pay buyers’ agents something, or buyers may pay their agents directly after negotiating a fee. They may also choose to go without an agent altogether.

Another option? A buyer agrees to pay a certain price — say $800,000 — only on the condition that the seller then pays the buyer’s agent $24,000, or 3%. “You got a free market,” Braun said.

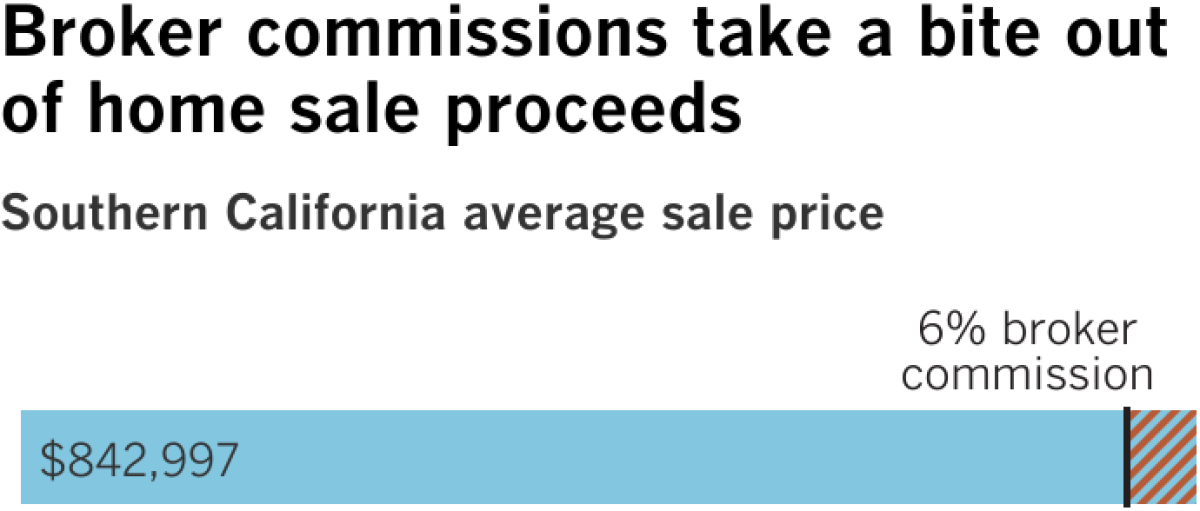

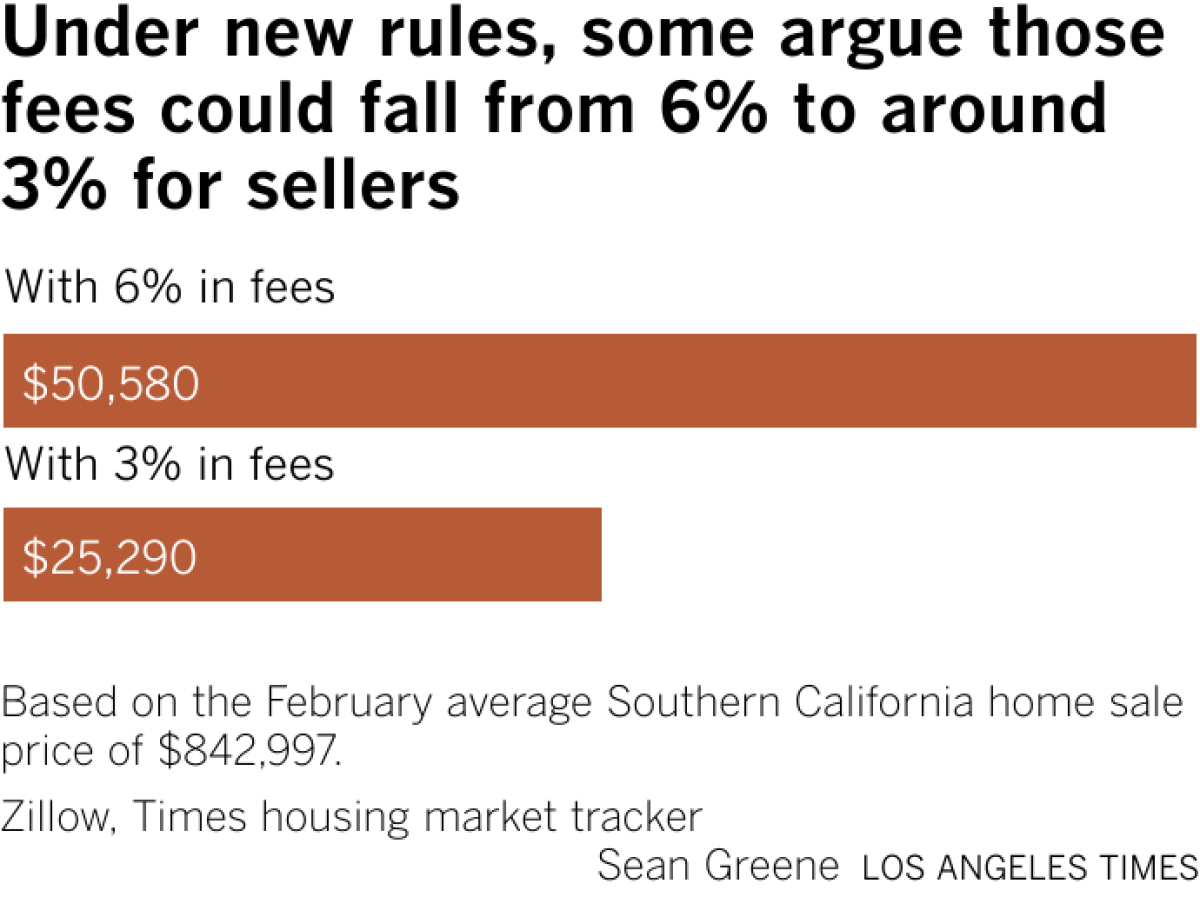

Commission rates are a small proportion of a sales price, but they add up. For a home sold at the average Southern California price of $842,997, 6% is $50,580.

If such changes drive down commissions overall, it could have a big effect on real estate agents who are paid a proportion of the commission sent to their brokerage.

Higher mortgage rates sent home sales tumbling, reducing pay for agents who are compensated based on the number and price of the deals they transact.

In California alone, NAR lost 9,723 members from December 2023 to January 2024 — a 4.75% decline.

Not all agents are worried.

Michael Khorshidi works mostly with buyers, but sees the new requirements as an opportunity to show the value he brings to clients. Agents who aren’t able to demonstrate their worth will be the ones who lose work, he said.

“We’re always transitioning,” Khorshidi said. “This is just the latest transition.”

If the settlement ends up creating a system in which buyers pay their agents directly, it could saddle them with new costs.

However, Braun argued that buyers would ultimately see reduced costs as well because under the current system, buyer agent commissions get passed along to buyers in the form of higher home prices.

That doesn’t mean sellers make a conscious decision to set their home prices higher because they need to pay a buyer’s agent. Rather, Braun said it means fewer homes make financial sense to sell because some homeowners don’t have enough equity to pay two commissions.

If buyers paid their own agent, more homeowners could afford to sell, increasing supply and helping put downward pressure on price, Braun said.

“Going forward, there is a significant likelihood home prices will be lower than they otherwise would be,” he said.

Michael Copeland, a real estate agent in Palm Springs, doesn’t think the agreement will alter the market too dramatically.

To bring in buyers, sellers may still be incentivized to cover both commissions — just as they do today.

(AP) – A powerful real estate trade association has agreed to pay $418 million and change its rules to settle lawsuits claiming homeowners have been unfairly forced to pay artificially inflated agent commissions when they sold their home.

The National Association of Realtors said Friday that its agents who list a home for sale on a Multiple Listing Service, or MLS, will no longer be allowed to use the service to offer to pay a commission to agents that represent potential homebuyers. The rule change leaves it open for individual home sellers to negotiate such offers with a buyer’s agent outside of the MLS platforms, however.

NAR also agreed to create a rule that would require MLS agents or other participants working with a homebuyer to enter into written agreement with them. The move is meant to ensure that homebuyers know going in what their agent’s service will charge them for their services.

The rule changes, which are set to go into effect in mid-July, represent a major change in the way real estate agents operate.

The NAR faced multiple lawsuits over the way agent commissions are set. In October, a federal jury in Missouri found that the NAR and several large real estate brokerages conspired to require that home sellers pay homebuyers’ agent commission in violation of federal antitrust law.

The jury ordered the defendants to pay almost $1.8 billion in damages — and potentially more than $5 billion if the court ended up awarding the plaintiffs treble damages.

The NAR said the settlement covers over one million of its members, its affiliated Multiple Listing Services and all brokerages with a NAR member as a principal that had a residential transaction volume in 2022 of $2 billion or less.

The settlement, which is subject to court approval, does not include real estate agents affiliated with HomeServices of America and its related companies, the NAR said.

Copyright 2024 The Associated Press. All rights reserved.