Sandy Jamison, a broker with Tuscana Properties in Campbell, says she’s helped clients try to persuade sellers to lower their asking price or offer other concessions to offset high insurance costs.

Laure Andrillon/Special to the ChronicleWhen Cindi Koehn listed her Lake County home for sale last year, she didn’t expect any trouble selling the beautiful 1.7-acre property overlooking the lake. But three interested buyers walked away. The cost to insure it, they told her, would be too expensive.

Koehn was surprised and disappointed. In 2015, dozens of Lake County homes had burned to the ground in a series of wildfires. Four years later, Koehn was dropped by Farmers Insurance over concern about the risk of fire on her property. Still, she didn’t expect insurance problems to prevent her from selling her home.

“I feel like I’m at the mercy of the insurance industry,” Koehn said. “We thought that there wouldn’t be any issues when we went to sell.”

Article continues below this ad

Before insurance companies started retreating from the state, home insurance was divorced from the process of searching for a home. Only after getting their offer accepted would buyers begin to look for insurance, which is required for a mortgage. Now, with the insurance market in turmoil, some sellers like Koehn are finding buyers backing out due to the high cost or unavailability of insurance. Buyers, meanwhile, are scrambling preemptively to obtain insurance, making all-cash offers or choosing not to purchase homes at all.

Real estate brokers such as Sandy Jamison seek to accommodate buyers struggling with the high costs of homeowner’s insurance.

Laure Andrillon/Special to the Chronicle“Homeowner’s insurance used to be a rounding error, depending on where you lived. It’s not that way anymore,” said David Russell, a professor of insurance at CSU Northridge.

The problems are especially acute in areas of high wildfire risk, but they have rapidly spread across the state, including the Bay Area.

In Lake County, the availability and affordability of insurance has been an issue for several years, according to Marie Wotherspoon, a real estate agent in the area. But the effects of the crisis have begun manifesting elsewhere. In San Diego, where Wotherspoon was based until last year, Foremost Insurance’s decision to stop offering condo insurance caused a number of condo owners to lose coverage, she said. Even in some coastal cities, buyers have struggled to find insurance, she said.

Article continues below this ad

It’s not clear exactly what impact the insurance crisis will have on home prices. A report published in 2023 from research and technology nonprofit First Street Foundation found that a home worth $300,000 whose annual insurance premium rose from $1,400 to $3,200 — which the report says is the average cost of the FAIR Plan, the state-created wildfire insurer of last resort — could lose about 12% of its value.

Real estate broker Sandy Jamison says, “There’s this big black box where we cannot see how these (insurance) companies are rating properties.”

Laure Andrillon/Special to the Chronicle“I think we’re just beginning to understand that (insurance) might be an issue on almost every sale,” said Emma Morris, a Berkeley-based Realtor with Red Oak Realty.

Diane Britto, a Walnut Creek-based real estate broker, said she first noticed insurance becoming an issue for buyers near the end of 2023. Earlier that year, both State Farm and Farmers Insurance — the top two home insurers in the state — stopped writing new homeowner’s policies, even as they continue, for the most part, to renew existing policies.

Article continues below this ad

Even if a buyer finds a policy, they’re often blindsided by the high cost, Britto said. The average annual premium in California rose by about $400 from 2017 to 2021, double the national increase, according to the National Association of Insurance Commissioners.

“First-time buyers, they’re always shocked,” Britto said, noting that rental insurance typically costs hundreds annually, far less than home insurance.

Higher premiums can affect buyers’ ability to secure a loan. Some buyers are preapproved for a mortgage based on the average cost of insurance, only to discover that the cost of coverage could be double what they expected, according to Michael Koran, a Bay Area mortgage agent.

Buyers are running into insurance issues in San Francisco too, said Chris Lim and Michelle Balog, real estate agents with Christie’s International Real Estate. While the city doesn’t have the same wildfire risks as other parts of the Bay Area, they explained, its older buildings sometimes have outdated wiring that can present a fire risk, forcing sellers to replace their electrical systems or buyers to call multiple insurance brokers.

Article continues below this ad

Backing out of a deal can be costly, according to Daryl Fairweather, chief economist at online real estate brokerage Redfin. If a buyer retracts an offer that’s been accepted, they usually forfeit their earnest money, a deposit that’s usually between 1% and 3% of the sale price.

Some options, such as making an offer contingent on finding insurance, might make a seller more likely to choose a different offer — especially in high-demand areas like Walnut Creek, according to Britto.

Real estate broker Sandy Jamison prepares a listing for showing in San Jose. With the insurance market in turmoil, many potential homebuyers are scrambling to obtain coverage, making all-cash offers, or walking away from the market.

Laure Andrillon/Special to the ChronicleIn one situation, Britto recounted, a buyer made an offer only to learn later that the insurance company wouldn’t cover the property without expensive upgrades to the home’s plumbing system — a bill the seller wasn’t willing to foot.

Sandy Jamison, a broker with Tuscana Properties in Campbell, said she’s helped clients try to persuade sellers to lower their asking price or offer other concessions to offset high insurance prices, though sellers don’t always agree.

Article continues below this ad

Costly insurance payments increase a buyer’s debt-to-income ratio at a time when high interest rates have already done so, according to Koran. With too high a ratio, a buyer might be seen as a risky investment for a bank loan.

Koran hasn’t had anyone back out of a contract yet due to insurance, he said. If that possibility threatens, he encourages buyers to get help from their family or use their funds to pay off other debts and lower their debt-to-income ratio.

But he has seen some buyers walk away from a home purchase due to high insurance costs, citing the example of a roughly $2 million home in Marin County that would have cost $9,500 annually to insure under the FAIR Plan.

The FAIR Plan, whose clientele more than doubled in the last five years to 339,000 dwelling policyholders, is often the only option in fire-prone areas. Buyers throughout Lake County, for example, have struggled to find insurance, but it’s especially hard to find homes in forested areas, Wotherspoon said. FAIR Plan premiums, though, are generally higher than those in the normal market, and offer more limited coverage. Its rates are likely to rise even further, according to the plan’s president.

South Bay real estate broker Sandy Jamison said of insurance companies and how they designate high-risk properties, “We can’t really tell how they’re drawing the lines (or) where they’re drawing them until we go to apply for an insurance policy and they … give us a terrible rating.”

Laure Andrillon/Special to the ChronicleThe plan also caps coverage limits for homes at $3 million. Mortgage lenders will typically require an insurance policy that would completely cover the cost of replacing the home, according to Tom Banducci, a San Diego-based branch manager for Cornerstone First Mortgage.

In high-risk areas, some properties “might become ineligible for mortgages if insurance is not readily available and affordable,” Koran said.

As insurers pull out of the state and the availability of coverage dwindles, the impacts are also being felt in areas believed to have a lower risk for wildfires. In September, about 30% of FAIR Plan policies covered properties not located in wildfire-prone areas, according to recent testimony by FAIR Plan President Victoria Roach. As of March, that share is now 35%, according to a FAIR Plan spokesperson.

“There’s this big black box where we cannot see how these (insurance) companies are rating properties,” Jamison said. “We can’t really tell how they’re drawing the lines (or) where they’re drawing them until we go to apply for an insurance policy and they … give us a terrible rating.”

Still, mortgage rates are affecting the housing market more than insurance issues, said Fairweather, the economist. High mortgage rates are leading fewer homeowners to sell, restricting supply and raising prices. Though many real estate experts had predicted rates would fall this year, that has yet to happen.

In the short term, home values in competitive markets such as the Bay Area remain high. Megan Micco, a Berkeley real estate broker with Compass, said that while “the natural buyer instinct” is to offer less money to account for insurance or fireproofing costs, there are so few homes available that most sellers can find someone willing to pay full price.

That hasn’t been the case in some high wildfire-risk regions such as Lake and Mendocino counties, which are among the few counties in California where home values have declined over the past year, according to real estate brokerage site Zillow.

Koehn, a military veteran, finally got insurance for her Lake County home through USAA, but she has lost hope that her home will sell barring an end to the insurance crisis and high interest rates. For now, she’s renting a home in Santa Barbara County while paying the mortgage and utility bills for the empty house in Lake County, which has taken a deep cut out of her retirement savings.

“I’m 62,” she said. “The rest of my time is going to be spent with my grandchildren, but at the same time, I’m now worrying about a house which is seven hours away.”

Reach Megan Fan Munce: megan.munce@sfchronicle.com. Reach Christian Leonard: christian.leonard@sfchronicle.com

The median U.S. home pierce rose 5.2% year over year this week, and mortgage rates hit their highest level since November 2023

SEATTLE, April 25, 2024–(BUSINESS WIRE)–(NASDAQ: RDFN) —The median U.S. home-sale price hit a record $383,725 during the four weeks ending April 21, up 5.2% from a year earlier—one of the biggest jumps since October 2022. That’s according to a new report from Redfin (redfin.com), the technology-powered real estate brokerage.

The average weekly mortgage rate hit 7.1% this week, its highest level since November 2023, as it became clear the Fed would keep interest rates high longer than expected. High prices and mortgage rates drove the median monthly housing payment to a record $2,843, up 13% year over year.

Prices are soaring despite the fact that there’s more inventory than last year. New listings are up 10.2% year over year, though growth in listings may be losing momentum as stubbornly high rates solidify the lock-in effect. Prices are being buoyed by the fact that inventory remains low despite the recent improvement. Demand is holding up fairly well in the face of 7%-plus rates, though some indicators are starting to show a slowdown. Redfin’s Homebuyer Demand Index—a measure of requests for tours and other buying services from Redfin agents—is near its highest level in about eight months, but mortgage-purchase applications are down slightly (-1%) week over week.

“My advice to sellers is to price your home fairly. Even though sellers are getting top dollar at the moment, they should price competitively to attract buyers from the start and avoid having to drop their price as stubbornly high mortgage rates eat into buying budgets,” said Redfin Economic Research Lead Chen Zhao. “My advice for serious buyers who can afford today’s costs is to shop for your dream home and accept that this year is probably not the time to find a dream deal. Price growth may cool slightly in the coming months if mortgage rates stay high or rates might fall slightly—but overall housing costs are likely to remain elevated for the foreseeable future.”

For more of Redfin economists’ takes on the housing market, including how current financial events are impacting mortgage rates, please visit Redfin’s “From Our Economists” page.

Leading indicators

|

Indicators of homebuying demand and activity |

||||

|

|

Value (if applicable) |

Recent change |

Year-over-year change |

Source |

|

Daily average 30-year fixed mortgage rate |

7.39% (April 24) |

Up from roughly 7% one month earlier; near highest level since November 2023 |

Up from 6.59% |

Mortgage News Daily |

|

Weekly average 30-year fixed mortgage rate |

7.1% (week ending April 18) |

Up from 6.87% a month earlier; highest level since November 2023 |

Up from 6.39% |

Freddie Mac |

|

Mortgage-purchase applications (seasonally adjusted) |

|

Decreased 1% from a week earlier (as of week ending April 19) |

Down 15% |

Mortgage Bankers Association |

|

Redfin Homebuyer Demand Index (seasonally adjusted) |

|

Up 3% from a month earlier (as of week ending April 21) |

Down 9% |

Redfin Homebuyer Demand Index, a measure of requests for tours and other homebuying services from Redfin agents |

|

Touring activity |

|

Up 34% from the start of the year (as of April 23) |

At this time last year, it was up 29% from the start of 2023 |

ShowingTime, a home touring technology company |

|

Google searches for “home for sale” |

|

Unchanged from a month earlier (as of April 21) |

Down 17% |

Google Trends |

Key housing-market data

|

U.S. highlights: Four weeks ending April 21, 2024 Redfin’s national metrics include data from 400+ U.S. metro areas, and is based on homes listed and/or sold during the period. Weekly housing-market data goes back through 2015. Subject to revision. |

|||

|

|

Four weeks ending April 21, 2024 |

Year-over-year change |

Notes |

|

Median sale price |

$383,725 |

5.2% |

All-time high; biggest increase since Oct. 2022, with the exception of the 4 weeks ending Feb. 11, 2024 and the 4 weeks ending Feb. 18, 2024 (5.3% increases) |

|

Median asking price |

$415,925 |

6.7% |

All-time high; biggest increase since Sept. 2022 |

|

Median monthly mortgage payment |

$2,843 at a 7.1% mortgage rate |

12.6% |

All-time high |

|

Pending sales |

86,786 |

-3.8% |

Biggest decline in 6 weeks |

|

New listings |

95,580 |

10.2% |

|

|

Active listings |

840,411 |

10.1% |

|

|

Months of supply |

3.2 months |

+0.4 pts. |

4 to 5 months of supply is considered balanced, with a lower number indicating seller’s market conditions |

|

Share of homes off market in two weeks |

43.3% |

Down from 46% |

|

|

Median days on market |

35 |

Unchanged |

|

|

Share of homes sold above list price |

29.8% |

Essentially unchanged |

|

|

Share of homes with a price drop |

6% |

+1.7 pts. |

|

|

Average sale-to-list price ratio |

99.2% |

+0.1 pt. |

|

|

Metro-level highlights: Four weeks ending April 21, 2024 Redfin’s metro-level data includes the 50 most populous U.S. metros. Select metros may be excluded from time to time to ensure data accuracy. |

|||

|

|

Metros with biggest year-over-year increases |

Metros with biggest year-over-year decreases |

Notes |

|

Median sale price |

Anaheim, CA (25%) New Brunswick, NJ (14.9%) Detroit (14%) West Palm Beach, FL (13.4%) San Jose, CA (13%)

|

Austin, TX (-0.9%)

|

Declined in just 1 metro |

|

Pending sales |

San Jose, CA (14.2%) San Francisco (6.4%) Seattle (5.7%) Milwaukee (5.2%) Anaheim, CA (4.5%) |

Nassau County, NY (-13.9%) Phoenix (-13%) Fort Lauderdale, FL (-12.5%) Houston (-11.9%) Riverside, CA (-11.4%)

|

Increased in 9 metros |

|

New listings |

San Jose, CA (43.1%) Jacksonville, FL (29.1%) Phoenix (25.8%) Sacramento, CA (24%) Miami (21.9%)

|

Newark, NJ (-9.1%) Cleveland, OH (-5.9%) Chicago (-4.7%) Milwaukee (-4.7%) Providence, RI (-4.4%) Detroit (-4%) |

Declined in 6 metros |

To view the full report, including charts, please visit: https://www.redfin.com/news/housing-market-update-home-prices-costs-record-high

About Redfin

Redfin (www.redfin.com) is a technology-powered real estate company. We help people find a place to live with brokerage, rentals, lending, title insurance, and renovations services. We run the country’s #1 real estate brokerage site. Our customers can save thousands in fees while working with a top agent. Our home-buying customers see homes first with on-demand tours, and our lending and title services help them close quickly. Customers selling a home can have our renovations crew fix it up to sell for top dollar. Our rentals business empowers millions nationwide to find apartments and houses for rent. Since launching in 2006, we’ve saved customers more than $1.6 billion in commissions. We serve more than 100 markets across the U.S. and Canada and employ over 4,000 people.

Redfin’s subsidiaries and affiliated brands include: Bay Equity Home Loans®, Rent.™, Apartment Guide®, Title Forward® and WalkScore®.

For more information or to contact a local Redfin real estate agent, visit www.redfin.com. To learn about housing market trends and download data, visit the Redfin Data Center. To be added to Redfin’s press release distribution list, email press@redfin.com. To view Redfin’s press center, click here.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240425347655/en/

Contacts

Contact Redfin

Redfin Journalist Services:

Kenneth Applewhaite, 206-414-8880

press@redfin.com

Price growth is leveling off as elevated mortgage rates strain buyer budgets, but prices are still at historic highs because there aren’t enough homes for sale

SEATTLE, April 23, 2024–(BUSINESS WIRE)–(NASDAQ: RDFN) — U.S. home prices climbed 0.6% from a month earlier on a seasonally-adjusted basis in March, matching February’s 0.6% month-over-month gain, according to a new report from Redfin (redfin.com), the technology-powered real estate brokerage.

On a year-over-year basis, prices rose 7.3%, also little changed from the prior month’s 7% annual increase.

This is according to the Redfin Home Price Index (RHPI), which uses the repeat-sales pricing method to calculate seasonally adjusted changes in prices of single-family homes. The RHPI measures sale prices of homes that sold during a given period, and how those prices have changed since the last time those same homes sold. It’s similar to the S&P CoreLogic Case-Shiller Home Price Indices but publishes more than one month earlier. March data covers the three months ending March 31, 2024.

“Elevated mortgage rates are putting a cap on home price growth. Sellers can’t jack up prices like they did during the pandemic because buyer budgets are already constrained by 7% interest rates,” said Redfin Senior Economist Sheharyar Bokhari. “But while price growth is leveling off, prices remain at historic highs. That’s because a shortage of homes for sale—largely driven by the mortgage-rate lock-in effect—is buoying prices.”

Price growth may continue to stagnate in the coming months as mortgage rates stay high. The Federal Reserve recently warned that elevated inflation will probably delay the interest-rate cuts they had been planning this year.

Prices Fell in the Bay Area, Texas and Florida

Home prices fell from a month earlier in nine of the 50 most populous U.S. metropolitan areas: San Jose, CA (-1%), San Antonio (-0.8%), Fort Worth, TX (-0.6%), San Francisco (-0.5%), Fort Lauderdale, FL (-0.5%), Charlotte, NC (-0.5%), Orlando, FL (-0.3%), Indianapolis (-0.3%) and Minneapolis (-0.1%).

Prices rose most in Providence, RI (3.2%), Montgomery County, PA (2.5%), Nassau County, NY (2.4%), Milwaukee (1.7%) and Anaheim, CA (1.7%).

To view the full report, including charts and metro-level data, please visit:

https://www.redfin.com/news/redfin-home-price-index-march-2024

About Redfin

Redfin (www.redfin.com) is a technology-powered real estate company. We help people find a place to live with brokerage, rentals, lending, title insurance, and renovations services. We run the country’s #1 real estate brokerage site. Our customers can save thousands in fees while working with a top agent. Our home-buying customers see homes first with on-demand tours, and our lending and title services help them close quickly. Customers selling a home can have our renovations crew fix it up to sell for top dollar. Our rentals business empowers millions nationwide to find apartments and houses for rent. Since launching in 2006, we’ve saved customers more than $1.6 billion in commissions. We serve more than 100 markets across the U.S. and Canada and employ over 4,000 people.

Redfin’s subsidiaries and affiliated brands include: Bay Equity Home Loans®, Rent.™, Apartment Guide®, Title Forward® and WalkScore®.

For more information or to contact a local Redfin real estate agent, visit www.redfin.com. To learn about housing market trends and download data, visit the Redfin Data Center. To be added to Redfin’s press release distribution list, email press@redfin.com. To view Redfin’s press center, click here.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240423788774/en/

Contacts

Redfin Journalist Services:

Kenneth Applewhaite, 206-414-8880

press@redfin.com

The last month of 2020 should’ve been a happy time for real-estate agents. The catastrophe of the pandemic had turned into an improbable housing-market boom, as home sales reached 14-year highs. But instead of celebrating their unexpectedly prosperous year, a lot of agents were pissed.

In private chats and message boards, they complained about new rules that would publicly expose their commissions. For homebuyers, the amount an agent gets paid has historically been out of sight, out of mind. But as part of a November 2020 settlement between the Department of Justice and the industry’s top trade group, the National Association of Realtors, real-estate search sites like Zillow and Redfin would soon start publicizing exactly how much buyers’ agents stood to collect on nearly every home for sale in America.

Among real-estate agents, no topic is more sensitive than their commissions. In private comments at the time, screenshots of which were shared with Business Insider, agents revealed just how squeamish they were.

“It’s no one’s business,” one disgruntled agent commented in a private Facebook group. “Do we go around asking people how much they make?”

“Someone has it in for real estate,” another responded.

In the middle of the vitriol, a brave agent — whom I’ll call Julie — applauded the move, suggesting it could help rid the industry of one of its dirty secrets: a sly tactic called steering.

Because of America’s convoluted home-sales system, the seller typically pays out agents on both sides of a transaction. The commission is baked into the home’s final price — it’s usually between 5% and 6% of the total — and split evenly between the buyer’s and seller’s agents. Technically, the seller can promise as little as $0 to the buyer’s agent; after all, why pay for someone you didn’t hire? But there’s a catch: Offer less than the going rate, and you risk getting the cold shoulder from other brokers and fewer eyeballs on your listing. Agents might steer their clients toward the homes that offer the standard commission and away from ones that don’t. The practice screws over both sellers, who might miss out on offers, and buyers, who might unknowingly pass over their dream home.

“Whether or not people admit it, steering due to commission rate definitely happens and it is incredibly wrong,” Julie wrote in a Facebook comment.

“Wrong,” someone else replied, “or the real world?”

Steering is notoriously difficult to prove or quantify, but evidence of the practice can be found littered throughout the housing market. The extent of steering is a main point of contention in the multibillion-dollar class-action lawsuits over agent commissions; the plaintiffs say the threat of steering is a big reason commissions have barely budged over the years. Wendy Gilch, a consumer advocate who focuses on transparency in real estate with her company, Selling Later, likened this moment to “a reset button” for the industry.

“It’s a great opportunity to start over,” Gilch told me.

It’s hard to know how much steering actually happens, mostly because a buyer might never know they were a victim in the first place.

The first article in NAR’s code of ethics says Realtors must “protect and promote the interests of their client,” and the organization’s official position can be summed up simply: Steering doesn’t exist. It’s a myth, the argument goes, created by those who want to dismantle the system and force buyers and sellers to pay their agents separately. But multiple agents told me there are all kinds of ways shady practitioners try to skirt the rules.

For instance, some agents might filter out listings with subpar commissions before passing along options to their clients. Or if they do show their client a house, they could insinuate that a low commission is a warning sign that the seller is hard to deal with or invent reasons the house isn’t a good fit. They could also caution that if they’re not getting their desired commission from the seller, they’ll expect the buyer to make up the difference. Agents are within their rights to do that, but it can discourage a cash-strapped buyer from pursuing a home.

“All a Realtor has to do is make a face about a house and they put a question in the buyer’s mind as to whether or not it would be wise to put an offer in on a house,” Doug Miller, a real-estate attorney in Minnesota, said in an email.

Critics say the stickiness of the going commission rate is evidence of steering’s ubiquity. The cut that’s split between agents on both sides of the deal has basically fluctuated between 5% and 6% of the total sale price since at least 1992, despite the widespread adoption of home-search technology, an increase in the number of agents, and huge differences in agents’ experience and skill. In recent years, greater numbers of agents have been fighting for clients, while technology has streamlined their jobs and made it possible for anyone to look up homes online. In a competitive market, critics say, you’d expect the price of agents’ services to come down. But data from RealTrends indicates that in 2021, even as home prices were skyrocketing and agents were signing up en masse, the typical commission rate actually went up.

All a Realtor has to do is make a face about a house and they put a question in the buyer’s mind as to whether or not it would be wise to put an offer in.

A recent analysis of roughly 265,000 listings on Redfin in 34 large metropolitan areas found that, in a typical market, more than 85% of listings offered the two most common commission rates for buyers’ agents. In Austin, Houston, and Kansas City, Missouri, more than 95% of listings offered a commission to the buyer’s agent of 3% or 2.5%.

The authors of the study wondered whether buyers’ agents might forward fewer low-commission listings to their clients, which would mean fewer page views on sites like Zillow and Redfin. They found that, all else being equal, low-commission listings received significantly fewer page views on Redfin — even the homes that offered agent payments just slightly below the going rate got fewer eyeballs. Homes with lower buyer-agent commissions also took longer to sell and were less likely to sell at all than those offering the standard rate.

Agents I talked with stressed that there are plenty of honest, hardworking representatives who just want the best for their clients. I believe them. But there are also just lots of agents out there, and the bar for entry into the industry is shockingly low. In most states, getting a license to work as a real-estate agent requires paying a few hundred dollars, doing several weeks’ worth of coursework, and passing a multiple-choice test. It’s no surprise, then, that there are some 1.5 million NAR members, or more than two Realtors for every available home on the market. And that doesn’t even count all the agents who aren’t members of the organization — there are about 1.3 million licensees in the US who don’t belong to the group, meaning they can’t use the Realtor title and don’t subscribe to its code of ethics.

The low standards and lack of oversight can create hazardous conditions for buyers and sellers. A few years ago, the now defunct discount brokerage Rex Real Estate released recordings of roughly 600 calls in which other agents vowed to avoid properties listed by Rex that offered less-than-satisfactory commissions. In one call, court documents say, a Keller Williams agent told a Rex representative: “If you are not offering any buyer’s commission, then that’s fine. I’m not going to show that [property], and you’re probably going to run into the same issue with everybody here.” Another ReMax agent said, “I’m not going to show a listing where I’m not guaranteed a commission.”

Brendon Bowers, a former real-estate agent who spent a couple of years working as a branch manager for Rex in the Phoenix market, told me he encountered this sort of thing all the time. He said buyers’ agents might call and say, “‘Why is there no buyer’s commission?” or “Why do I have to negotiate this? Nevermind, we’re just going to go on to the next one.” Steering, he added, is “just flat-out a part of real estate.”

A spokesperson for the NAR told me that Rex was cherry-picking from thousands of calls and that these agents may have eventually shown their clients the homes, however begrudgingly. But even the mere threat of steering is enough to keep commissions from dropping, Stephen Brobeck, a senior fellow at the Consumer Federation of America, told me. The problem isn’t that steering is rampant, Brobeck said; if most listings in a market already offer uniform commission rates, there’s no need for an agent to steer their client in the first place. It’s the fear of steering that maintains the system. A seller might hear of examples of steering, or get a warning from their agent of the risks involved in offering substandard commissions, and decide it’s worth it just to promise the going rate. After all, everyone else is doing it.

Class-action plaintiffs, the Consumer Federation of America, and the Department of Justice have proposed something called decoupling, in which buyers and sellers just pay their agents separately, as a way to get rid of steering. The DOJ has argued that as long as sellers pay a commission to the buyer’s agents, they’ll be pressured to promise the going rate. In the proposed alternative, sellers would promise a commission only to their agent. For buyers, it would be more complicated; they’d have to figure out how to pay their agent directly, and how much. They could either pay the broker out of pocket or arrange to get a rebate from the seller once the deal closes.

Such changes could come sooner rather than later. With commissions under heightened scrutiny, more agents are getting buyers to sign buyer-broker representation contracts laying out the rate the agent expects to get paid, regardless of what the seller offers in the listing. If an agent wants 3% of the sale price and the house you buy provides only 2%, you might have to pick up the difference. If you’re working with a good agent, that will probably feel worth it. But if sellers stop offering commissions altogether, buyers might have to make some tough choices. Many more buyers might choose to go it alone rather than pay out of pocket for an agent’s services. Or they could pay their agents a flat fee or an hourly rate instead of a commission, though it’s unclear how many agents would take that deal. Buyers might also start writing offers on homes that are contingent on making sure their agent gets paid: “I’ll offer you $400,000 for your house, but you’ve got to give me back $12,000 so I can cut a check to my broker.” But there’s still no guarantee that sellers would agree to that, especially in a hot market like the one we’ve seen over the past few years.

Nobody expects agents to work for free, but the near uniformity of commission rates is strong evidence that buyers and sellers aren’t bargaining nearly as much as they should be.

The NAR says decoupling would only heighten the inequalities in the housing market. Rich people could afford to get an agent and enjoy all the benefits that come with one, while poorer buyers might be left on their own. Others in favor of decoupling say the industry would be forced to get creative to ensure that as many buyers as possible could still access agents. Meanwhile, buyers and sellers would negotiate harder and maybe save thousands of dollars on a sale.

Nobody expects agents to work for free, but the near uniformity of commission rates is strong evidence that buyers and sellers aren’t bargaining nearly as much as they should be. If you’re a buyer, there are steps you can take to avoid falling victim to steering. Be wary of relying too much on an agent to feed you listings; it’s worth doing your own research, too. On sites like Zillow and Redfin, you can often see the commission being offered to the buyer’s agent. If a listing is offering less than what’s typical in your area and your agent is acting weird about it, that might be a red flag. There are lots of willing brokers out there; if you suspect steering, agents told me, you’ve got plenty of options for a second opinion.

Again, there are good, honest agents out there who deserve every penny of their commission. But you don’t have to talk to many buyers to realize that not everyone meets that standard.

I recently called up Julie, the agent in the private Facebook group who spoke up about steering a few years ago. She asked that I not use her real name because she didn’t want to be drawn into the controversy over commissions and all the lawsuits the NAR is facing; if things were tense back in 2020, they’ve only gotten more heated since then. But her feelings about the issue hadn’t changed.

“I am responsible for taking care of my clients to the best of my ability,” she told me. “I tell my clients it’s not their job to provide for me. It’s my job to take care of them.”

James Rodriguez is a senior reporter on Business Insider’s Discourse team.

SEATTLE (KOMO) — If you’re waiting for a break in home prices, a new report from Seattle-based Redfin might convince you to get what you can.

According to their data, the U.S. housing market gained $2.4 trillion in value over the last year. The total value now is $47.5 trillion.

That’s based on more than 90 million residential properties nationwide. Mortgage rates may drop this year, but buyers still face limited supply.

RELATED | Here’s how much you need to make to ‘comfortably afford’ a Seattle home

“If you look at national listings across the U.S., we have 40% fewer listings today than we had in 2019. So if you’re trying to shop for a home, don’t think that you’re going to be flush with options,” said Ali Wolf, Chief Economist with Zonda.

Areas seeing the biggest price jump are cities in the Northeast and Midwest. Homes in urban areas are also more expensive than a year ago, but residential properties in the suburbs saw a bigger boost.

RELATED | Congress to take another swipe at tackling housing affordability crisis

“What we are seeing in the housing market is right now we are living through a record housing affordability shock,” said Zonda.

In Seattle, the entire housing market is now worth more than $911 Billion, up 4.6% from last year.

Tacoma saw an even bigger jump, gaining 5.6% in total value.

RELATED | High prices and interest rates leave 70% of Americans doubting home ownership in 2024

If you’re watching mortgage rates, hoping a break will help you compete, hold on.

Interest rates could be cut three times this year and economists said that could start as early as May.

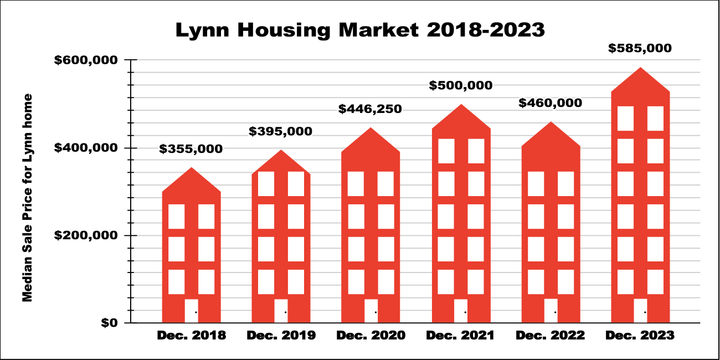

LYNN — The city’s housing market grew by roughly 22% in value in 2023, leaving the city’s residential real estate price at a six-year high.

Data collected from the online brokerage company Redfin reports that the median sale price of a home in Lynn has risen from $480,000 at the end of 2022 to $585,000 at the end of 2023. The 21.9% price bump follows the city’s first housing market dip since 2017, which occurred in 2022 when the median housing price decreased by 4% from the prior year.

North Shore Community College Economics Professor Moonsu Han said that while overall, property values throughout the country have been trending downwards since 2022, housing prices in the Northeast, particularly the Greater Boston area, have been steadily increasing.

“The gap (in housing prices) between Western area and Northeastern areas is still huge, near record high. The housing market in the Northeastern part of the United States is really hot, even though we have really high-interest rates, especially in Lynn and the Greater Boston area,” Han said.

According to Redfin, the number of home sales in Lynn also dropped by more than 11% between the end of 2023 and 2022. In 2023, listed homes remained on the market three days fewer than in 2022 before being sold.

Han said the growth of life sciences in the greater Boston area is growing the region’s population of young, well-paid professionals, contributing to a greater demand for quality housing in Lynn and, consequently, a more competitive market.

“The inflow of people into the area is big. That’s why a lot of people want to buy houses. However, COVID was a period of time when a lot of people refinanced their house with really, really, low-interest rates, leaving little incentive to sell their houses,” Han said. “There’s a much greater demand than there is a supply.”

Considering Mayor Jared Nicholson’s Administration and the city’s goals for inclusive growth, economic development, improved education, and reduced crime intervention, Han said he expects the city’s housing market to continue to grow in the future.

“The city’s leadership has a focus on inclusive growth, better infrastructure, education, and peace… that’s very important for housing prices and for the overall welfare of Lynn’s residents,” Han said.

With the revival of the Lynn ferry last summer and the temporary Lynn Commuter Rail platform on Ellis Street opening last December, Han said he expects faster transit between Lynn and Boston to correlate with the growth of Lynn-to-Boston commuters.

Han added that the development of condominiums and houses in Lynn and investments in education will likely fuel one another, increasing demand for Lynn homes.

“I think the City of Lynn has a really, really bright future,” Han said. “The housing market in Lynn is very, very hot, and it will continue to grow.”

“Nobody can afford a home right now.”

That’s how the vast majority of would-be buyers felt last year, according to a recent analysis by real estate group Redfin.

That was closer to being true for minority households.

The average Black household could afford just 7% of listings for sale last year on a median income, while white households could afford 22% of listings. The share was nearly as bad for Latino households, which could afford just 10% of homes for sale. Meanwhile, Asian households could afford 27% of homes for sale at the median income.

The affordability picture was bleak overall. Just 16% of homes for sale in 2023 were affordable to the typical US household, the lowest share on record since Redfin started tracking the metric a decade ago. Overall, the share of affordable listings in the US dropped to 352,500 last year, down 41% from 596,135 a year earlier and down from over 1 million during the prior decade. The costs of homeownership rose even in historically affordable areas due to limited inventory propping up prices.

Read more: How to buy a house: 13 steps to getting the keys to your new home

Despite these hurdles, there are signs 2024 could be better. Redfin economists noted that wages for non-white households grew faster last year, helping reduce the income gap. Rents have also shown signs of falling, which could help renters — often communities of color — save more toward their homebuying nest egg.

“The wage gap is a big part of it,” Daryl Fairweather, chief economist at Redfin, told Yahoo Finance. “Home prices have become so expensive in a lot of metro areas. It makes it really hard for Black and Latino households to be able to afford a home compared to their white counterparts.”

Fairweather added: “The higher the mortgage rate, the higher a mortgage payment will be. It creates another barrier for people with less income to put towards a down payment.”

Read more: Mortgage rates below 7% — is this a good time to buy a house?

‘The racial affordability gap exists nationwide’

Even the most affordable metropolitan areas in the US became less accessible to Black and Latino homebuyers last year as both prices and rates soared.

In Detroit, where mortgage payments are among the lowest in the country, just 31.8% of listings were affordable for the typical Black household in 2023, and 50.2% were affordable for the average Latino household. That’s much lower than the 66% affordable listings for the typical white household.

Homes listed in Detroit were priced at an average $85,000 in December, up 21.4% from 2022. According to the US Census Bureau, the typical single earner in Michigan made an annual income of $63,380.

And in more expensive markets, where nearly everyone had a hard time finding affordable housing, Black and Latino households had far less options to pick from.

For instance, in Anaheim, Calif., less than 0.5% of listings were affordable to the typical Black and Latino households in 2023, compared with nearly 2% that were affordable for the average white household, Redfin found.

As of December, the typical home listed in Anaheim cost $866,000, up 12% year over year. Meanwhile, the average Californian earned $75,235 annually as of May 2023.

“The racial housing affordability gap exists nationwide, from the least affordable metros to the most affordable metros,” the report said.

According to Redfin, a listing is considered affordable if a buyer would have to spend no more than 30% of their income on the payment. However, that goal has become harder to achieve as wages have failed to keep up with rising housing costs.

At a national level, an average homebuyer in 2023 had to earn an annual income of at least $109,868 if they were aiming to spend under 30% of their income on a monthly mortgage payment for a median-priced home. That was 8.5% more than 2022 and $31,226 more than the typical household earned in a year.

While wages for non-white households grew at a pace of 5.9% in December 2023 — compared to 5.6% for white households — minorities still lag behind. Per the latest US Census data, in 2022, the median household income varied by race.

The average Black household earned a median income of $52,860, compared to Latino households, which earned an average of $62,800. Meanwhile, white and Asian households made a median household income of $81,060 and $108,7000, respectively. On a national scale, the median household income was $74,580 in 2022.

“A perfect storm of inflation, high prices, soaring mortgage rate and low housing supply caused 2023 to go down as the least affordable year for housing in recent history,” Redfin senior economist Elijah de la Campa said in a separate report. “The good news is that affordability is already improving heading into the new year.”

Expect better homebuying conditions in 2024

Last year’s dramatic decline in affordability was in part due to a drop in listings, which fell 21% on a national scale year over year. Elevated mortgage rates also propped up housing costs as fewer homeowners decided to list their homes for sale — aggravating the inventory shortage.

But buyers could have better luck in 2024.

Rent prices are finally cooling down due to the building boom in recent years, Redfin noted, and should reduce further in 2024. Already, the median asking rent fell 2% year over year in November 2023 to $1,967, the largest annual drop since February 2020.

Renters, typically younger Americans in prime ages for homebuying, have long cited an inability to save for a down payment due to rising rent prices as a barrier to homeownership. The softening of rent prices could give them some wiggle room to save.

It’s not hard to imagine why down payments have been so hard to save up for.

According to a separate study by Realtor.com, down payments hit a new peak in the third quarter of 2023 with an average 15% down payment amount of $30,000. That’s up from 11.5% in 2020, when the typical down payment was just $17,000.

That uptick in down payments, a result of higher rates and home prices, was a major barrier for both Latino and Black homebuyers. Particularly those with below-average or no credit score.

“If you’re paying in cash or putting a large down payment, you can offset some of that increase in interest payments, but when you have a low down payment and if you have a lower credit score, the mortgage impact can be really high,” Fairweather said.

Further aiding affordability in 2024 would be softening mortgage rates, which Redfin predicts will land on 6.6% by the year-end. Other economists expect a bigger drop to around 6% or even under. The improved affordability could thaw some of the mortgage rate lock-in effect, convincing some homeowners to list now that rates are down over a full point from their near 8% peak in October.

According to Redfin, the increase in housing supply throughout 2024 and a burst of new construction could cause prices to drop by 1% on average by year-end.

“Small homes, like condos and townhomes, are in direct competition with apartment rentals. And since asking rents have been declining for three months in a row, that will put downward price pressure on more affordable, smaller homes,” Fairweather said. “This should improve affordability for first-time home buyers seeking starter homes.

“Also, the drop in mortgage rates we are forecasting should improve affordability.”

Gabriella is a personal finance and housing reporter at Yahoo Finance. Follow her on X @__gabriellacruz.

Real estate apps have been around for over 10 years now — and it seems like new ones come out as regularly as homes come to market. As their numbers grow, so does their variety: In addition to applications for buying, selling, and renting real estate, there are now platforms for obtaining mortgages, investing in real estate, and even designing a house.

Here are the nine of the best real estate applications on the market today.

What are real estate apps?

Real estate apps (short for applications) are a one-stop shop for prospective tenants, home buyers, home sellers, home owners and investors — not to mention the folks who like to just browse. They consist of databases with thousands — sometimes even millions — of properties, like a vast, location-spanning multiple listings service (MLS).

Most of these mobile apps make their money by charging a listing fee, selling ad space to Realtors or contractors, or taking a cut of the sale price or rent. Some are backed by real estate companies or brokerages, like Zillow and Redfin. Others are independent.

Types of real estate apps

The majority of real estate applications are focused on the house-hunting and renting experience. They’re a place for buyers to browse homes for sale or rent and a place for sellers and landlords to do market research, and list their properties for sale or rent.

There are real estate apps that focus on commercial properties to buy, sell or lease. Some provide directories of real estate agents and brokerages; others are oriented towards lenders and financial services. Rising in popularity of late have been apps geared real estate investments and home design.

Zillow

Best for initial research for home buying, renting, or selling

One of the most well-known and highly rated real estate search apps, the free Zillow app gives users access to a wide range of properties with detailed filter criteria. Through the app, you can coordinate your search for a home with someone else, meaning you or your roommate or partner can share your favorite finds easily.

The Zillow app does have a few flaws, however. Zillow’s “Zestimate,” its home evaluation tool, doesn’t always give an accurate picture of a home’s value, especially when details are missing from a listing. Real estate agents can also pay to have themselves featured as a contact for a property, even if they aren’t the actual listing agent, which can confuse things for homebuyers.

Pros:

- Most widely used application

- Can find homes for sale or for rent

- Can view sale price history for the whole neighborhood

Cons:

- Sometimes flawe price estimates and rental estimates

- Your information may be sold to lenders and Realtors

- Asking questions can lead to wave of unsolicited emails

Redfin

Best for saving on commissions

If you’re seriously home-hunting, the Redfin app can be a useful tool. Redfin is a real estate brokerage, so in addition to searching for properties through the app, you can go ahead and buy one with a Redfin agent and receive a portion of the agent’s commission back. If you sell your home and buy another one with a Redfin agent, you’ll only pay a 1% listing fee for your home, saving you from the standard 3% on both transactions.

The Redfin app also offers home value estimates, which might be more accurate than Zestimates, but still aren’t a substitute for an appraisal. Overall, the app is highly rated by users, and it’s free, making it a solid option for house hunters.

Pros:

- Save thousands in commission when buying or selling

- Accurate home value estimates

Cons:

- Limited neighborhood info

- Rental side is new with limited listings

Trulia

Best for getting a feel for a neighborhood

Trulia is actually owned by Zillow and uses information that comes from Zillow, but augments it a bit. Trulia includes features like drone film footage, quotes from people who live in the area, school ratings and walkability scores. Trulia’s home value estimates may be more accurate than Zillow’s because it uses more data points.

Pros:

- Extensive neighborhood data available in the app

- More accurate home estimates

- Easy to identify and contact the listing agent

Cons:

- Not great for home sellers: no agent directory, neighborhood price history isn’t as thorough

- Application can be difficult to navigate

Apartments.com

Best for renters

Are you looking for a rental? The Apartments.com app can help you easily unearth your next place. The app offers a streamlined search experience for apartments, condos, homes and townhomes, and you can sort through rentals based on unique filters such as wheelchair access, in-unit laundry, pet-friendliness or the addition of a dishwasher.

Although it’s free to browse rentals through the app, you’ll run into a fee if you want to apply for one directly through the platform. The in-app rental application costs $29.00 plus tax for up to 10 applications made within a 30-day period.

Pros:

- Apply to many apartments for the same fee

- View many types of rentals in one spot

Cons:

- Limited adoption outside of metropolitan areas

- No reviews from current or former tenants

Realtor.com

Best for landlords and for most accurate data

Homebuyers and renters alike can gain access to the most (and most up-to-date) listings by using the free Realtor.com app. With an extremely wide selection of properties available, you’re able to see all of the options out there. Realtor.com is also affiliated with the National Association of Realtors (NAR) and has access to a large portion of multiple listing services, so its listings are usually refreshed quicker compared to other sites.

Realtor is the only application on our list that lets landlords list rentals and take applications for free. So it might benefit you if you’re thinking about leasing that garage apartment or guest house or a second home.

In addition, listings on the Realtor.com app include handy information and filters, like the noise level of a neighborhood or commute time, which can be helpful when looking for a place to call home.

Pros:

- Updates the quickest: best spot to find brand new listings and see when something is sold

- Commute and noise level data in app

- Free rental listing and applications

Cons:

- Can’t filter results as thoroughly as other apps

- No easy way to see neighborhood home values

LoopNet

Best for commercial real estate

Residential real estate isn’t the only game in town. If you’re looking for a commercial property, the LoopNet app can help you find the perfect fit, and more information than what would be available on other apps geared toward residential homebuyers. You can easily search based on the type of commercial property you’re looking for, including office, retail, restaurant or multifamily dwelling.

One drawback that seems to be an issue among users, however, is the inability to save your search within the app. That means you’ll be forced to re-enter your search filters every time you want to explore listings.

Pros:

- Easy to find commercial properties for rent and for sale

- Thorough details in property listings

Cons:

- Only lists properties, not businesses that are for sale

- Limited tools like rent forecasts and loan calculators

Landa

Best for beginning real estate investors

The Landa app allows users to invest in real estate with as little as $5. Users can view rentals available to invest in and buy shares in properties. The application has an interface that allows you to see your real estate portfolio all in one place and updates you when you receive your share of the rental income.

Pros:

- Easy to find investment properties

- Low financial cost to get started

Cons:

- Limited real estate investment education within the application

- Newer company, limited track record

Rocket Mortgage

Best for financing

Rocket Mortgage is one of the top home loan lenders in the country. They have developed an industry-leading application that allows you to do most of the process on your phone. You can get pre-approval for a mortgage, submit documentation for underwriting, and e-sign your documents all in the secured application.

Pros:

- Streamlines the lending process: You can prequalify, submit documents and sign them all in the application

- Can submit mortgage payments on the app

- Includes affordability and payment calculators

Cons:

- Limited in-app financial education

Houzz

Best for people designing and building homes

Houzz is ideal for anyone designing their own home. The app allows you to decide layouts, color palettes and more. It can connect you with contractors, designers and builders all in one place. It even has a shopping cart where you can pick out furnishings and lighting fixtures, and have them shipped directly to your build site.

Pros:

- Connects you with local construction professionals

- Presents digital mock-ups of how things will look in your home

- Offers high-quality furnishings

Cons:

- High prices for most goods and services

- Potentially limited list of contractors

FAQs

-

One prized feature of home buying-oriented apps is the property evaluations they set on listings. They determine home value through proprietary algorithms. These algorithms incorporate data that includes things like recent home sales in the area, age of the home, square footage of the home, number of rooms and any previous sale price of the home — all factors that professional human appraisers often use, too.

-

Real estate applications have varying accuracies. The tools used by Trulia, Realtor and Redfin are generally viewed as the most accurate. Zillow’s estimate has become a bit of a joke in the industry.

Also, the apps don’t have a way to know everything that can significantly affect your home’s value — like its curb appeal or its condition. For example, they can’t know if you recently updated the kitchen, or that the carpeted floors are redolent of years of smoking and cats. All of these things can make the sum your home commands on the market quite different by than the estimate their computer came up with.