Lloyds Banking Group has offered a boost to homeowners and those trying to get on the property ladder as it predicted interest rates cuts on property prices.

They have predicted that the Bank of England will cut the base rate three times by the end of the year, starting in the summer; which is consistent with their earlier forecasts.

The Banking Group expects UK property prices to rise by 1.5 per cent this year.

However, their previous prediction was that house prices would fall 2.2 per cent.

William Chalmers, the banking group’s chief financial officer, said there’s a “more benign economic outlook” with the housing market proving more resilient than expected.

It also says unemployment will stay low, which is good news since Lloyds is seen as a proxy for the performance of the wider UK economy.

The Banking Group expects UK property prices to rise by 1.5 per cent this year

GETTY

They posted a 28 per cent drop in pre-tax profits to £1.6billion in the three months of the year, compared with £2.2billion a year ago.

There was an impairment charge of £57 million compared to loans of £448 billion.

Lloyds said its margins had been hit “mainly within UK mortgages” amid heightened competition between lenders to offer squeezed buyers better deals.

There were less mortgage lenders due to customers being squeezed amid the ongoing cost of living crisis.

Lloyds reassured the City by saying results this year would be in line with expectations, though profit margins will fall to 2.9 per cent from 3.22 per cent.

The fall was expected as more people moved their cash into savings accounts with higher returns and mortgage rates eased because of the competition stepping up among lenders.

Charlie Nunn, the group’s chief executive, said: “The Group is continuing to deliver in line with expectations in the first quarter of 2024, with solid net income, cost discipline and strong asset quality.

“Our performance provides us with further confidence around our strategic ambitions and 2024 and 2026 guidance.

“Guided by our purpose, we are continuing to support customers and successfully execute against our strategic outcomes, as highlighted in the third of our strategic seminars last month.

“This underpins our ambition of higher, more sustainable returns that will deliver for all of our stakeholders as we continue to Help Britain Prosper.”

Last month, Lloyds Banking Group said it planned to close 53 further branches in its network.

LATEST DEVELOPMENTS:

The group said it was closing 21 Lloyds branches, 22 Halifax branches and 10 Bank of Scotland sites.

In total, the banking group is closing 166 branches this year and 10 next year.

Jeremy Leaf, north London estate agent and a former chairman of the Royal Institution of Chartered Surveyors, said the housing market is still “playing catch-up” as the increase in new enquiries emboldens sellers to not only make their properties available, but chance their arm at higher asking figures.

He added: “The prospect of more stable or even falling mortgage rates is certainly helping to improve confidence generally.

“However, the uplift in supply has meant more choice, so the market remains price sensitive and buyers are negotiating hard – particularly those who require little or no finance.”

Rates peaked in July 2023, reaching 6.86pc, but have since fallen. The average two-year fix sits at around 5.83pc, while the average five-year fix is more like 5.40pc according to data firm Moneyfacts.

But in more recent times, mortgages have begun to edge up again as higher-than-expected inflation figures cast doubt over the likelihood the Bank of England will cut interest rates before the summer.

Tom Bill, head of UK residential research at Knight Frank, said changing economic predictions mean buyers and sellers “have faced mixed messages” this year, which may mean asking prices aren’t achieved.

He said: “While rising asking prices show seller expectations have improved, there is broader downwards pressure on prices as mortgage rates edge higher, supply increases and a wave of people roll off sub-2pc fixed-rate mortgages agreed in early 2022.

“The result is more friction around prices, particularly when a rate cut seems to move further into the distance with every release of economic data. That said, higher supply means there should be a recognisable spring bounce in the housing market.”

Nick Mendes, of mortgage brokerage John Charcol, said he had noticed a “slow down” of activity in recent weeks as mortgage rates stagnate and some buyers wait eagerly for a Bank Rate reduction.

He added: “We did see a lot of people entering the market earlier on in the year to beat the summer rush. Some house prices were reflecting the highs we saw just a few years ago.

“Some people will have stretched themselves, now unable to renew their rate in the current market and trying to downsize without losing on their property value.

“Always take asking prices with a pinch of salt; look at Land Registry prices for what [properties] were actually sold for.”

Outside London, Old Avenue in Weybridge, Surrey, had the highest average asking price for properties in 2024 so far, at £2.6m, Rightmove found.

Looking at homes to rent, the highest typical asking rents were found in Albion Street in Bayswater, central London, at £20,857 per month. This was followed by Pavilion Road in Knightsbridge, central London, where renters will need an average of £15,251 per month for a new let.

Outside London, Rightmove found the highest average asking rent was in London Road in Ascot, Berkshire, at £6,831 per month. Manor Road in Chigwell, Essex, had average asking rents of £4,311.

Meanwhile, renters looking for properties in Manchester’s vibrant city centre face average monthly rents of £3,766 in Deansgate, the research indicates.

Tim Bannister, a property expert at Rightmove, said: “London’s status as the hub of luxury property in the UK remains unchallenged, with Buckingham Gate in Westminster commanding the highest average asking price.

“Although the possibility of buying one of these homes is limited to a very lucky few, there’s clearly a fascination with these prestigious homes as we find they’re often among our most viewed properties on Rightmove.”

These days, chartered surveyor David Pardoe manages estates but, years ago, as an estate agent completing on the sale of a farm that was put on the market after the farmer had died, he was asked to tea by the widow and her son.

“They looked a little shifty and said that they’d kept something from me during the sale – the fact that the place was haunted.”

A sceptic by nature, Pardoe was told that the ghost of the farmer continued to turn on the milking parlour, even though it had been disconnected from the mains, at 3am each morning, just as he had done in life.

“Then his widow announced it wouldn’t be a problem as the ghost would follow them to the next home. I checked a year or so later, and it had.”

If that doesn’t happen, new owners can take matters into their own hands and organise for an exorcism or some alternative spirit cleansing ritual. Schneiderman says that there have been “numerous property sales” that he’s acted on where buyers have had their Feng Shui or Vastu consultant inspect the house in order to clean or purify the energy. It’s actually not that uncommon,” he adds.

Lindsay Cuthill, co-founder of Blue Book, an estate agency, believes buyers should take a sanguine approach to past goings-on.

“It’s important to remember that we are fleeting custodians of our homes, mere caretakers in the grand scheme of time.

“Our homes likely once belonged to others and are destined to shelter future generations. With each new owner comes new life and energy and our homes bear witness to all of the rich tapestry of life, from babies being born to people dying.”

Does a ghost put off a buyer? “Probably not,” says Cuthill. “Those buying a historic property normally know that a spirit is likely part of the package and, after all, not all spirits necessarily have to be bad.”

What about an untoward event? “It just depends on person to person,” says Wells. “I stopped at the gates to one house I was about to view with a client to say that there had been a fire some years before in which the owner had perished. He took the view that every house has had someone die in it and was quite matter of fact about it. Ultimately, it’s important to be upfront.”

Inflation is not only cramping Americans’ food and energy budgets, but it’s taking a bite out of the housing market. The combination of high interest rates and high prices continues to stifle the residential real estate market. The latest data shows mortgage applications have dropped for three straight weeks, while the average rate on a 30-year fixed mortgage has risen to 6.82%, up more than a half-percent from a year ago. At the same time, the average home price in the U.S. is at a record high. “Taking into account mortgage rates, incomes, and house prices, affordability right now is strained at the worst levels in about four decades,” says Lance Lambert, CEO of the real estate analytics firm ResiClub, in a recent interview with Fox Business.

With limited supply keeping prices elevated and the Federal Reserve keeping interest rates high to counter inflation, the market is caught in the perfect storm for buyers and sellers. “A lot of home buyers can’t get in, and a lot of home sellers can’t sell and buy something else because they can’t afford those new monthly payments,” says Lambert.

Faced with this latest economic challenge in an election year, the Biden administration is doing what it does best: blaming someone else. The same administration that tried to blame high gas prices on greedy gas station owners, and high food prices on ‘price-gouging’ corporations, is now blaming high home prices on…you guessed it…greedy real estate agents. “They’re scapegoating,” says Lambert. “They act like lowering commissions would improve housing affordability…you know, going after soccer moms making $60,000 a year, because that’s the only job that works around their kids’ schedule.”

Rather than attacking realtors, the administration should be implementing policies to increase housing supply and reduce inflation, according to Lambert. “Putting in tax policy that works for new construction and not against new construction, lower fees on homebuilding, all the boring stuff that would increase supply in the long-term…that is what would improve housing affordability,” he says.

The rise in banks using property surveyors who are working from home risks leaving homeowners trapped in homes they cannot sell, the industry has warned.

Remote or hybrid property surveyor jobs have jumped from 4pc pre-pandemic to 33pc today, according to exclusive data shared with The Telegraph by job search portal Indeed.

Valuations done from a desktop rely on pictures, making it hard for surveyors to see how properties are constructed. As a result, some bank surveyors are signing off on properties without realising they are unmortgageable.

Remote valuations help banks keep up with the volume of mortgage applications they receive – one surveyor told The Telegraph six valuations a day is standard practice.

But remote valuations can also “be detrimental” for a buyer when they come to sell the property.

Steve Savage, of Connells Survey and Valuation, said: “I had a case recently, a two-storey terrace house from 1900 with single skin brickwork spanning four inches. I carried out a Rics [Royal Institution of Chartered Surveyors] Level 2 homebuyer survey for the customer and found the property was unmortgageable.

“This was after a desktop valuation had been undertaken for the lender, giving the property the green light for a mortgage. Had the lender known the correct type of property construction, they would not have accepted the mortgage application.”

Mr Savage said the buyer may also have thought twice about buying the property, or tried to negotiate a better sale price earlier.

Mr Savage added: “Desktop and mortgage valuations are for the lenders’ benefit and will be limited in scope.

“The use of desktop valuations has increased since Covid… [They] can be detrimental to the customer when they come to sell the property.”

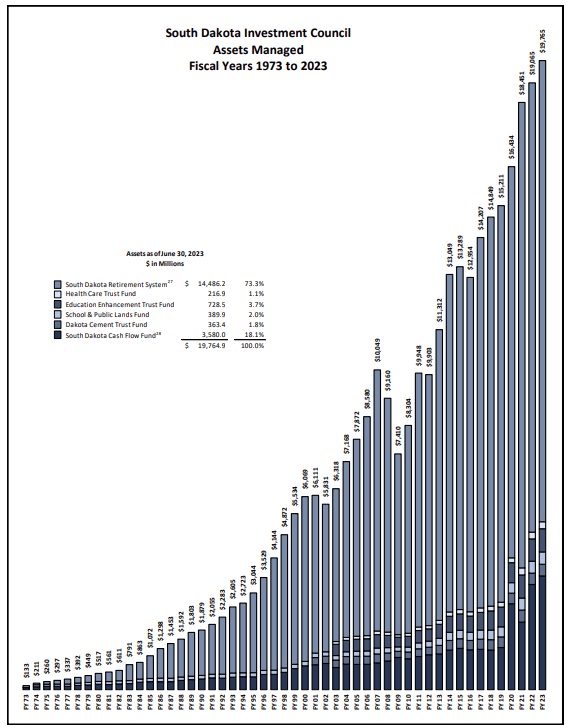

The overseers of South Dakota’s investments have put some money into companies that aim to cash in on artificial intelligence, but the explosion in public interest hasn’t changed the state’s money management strategy.

Leadership with the South Dakota Investment Council offered insights on the AI boom after prompting from its advisory board, which met in Sioux Falls on Thursday.

Matt Clark, the state’s chief investment officer, compared the current plenitude of cash-burning AI operations to companies wrapped up in the dot-com bust of 2000. That year’s crash of tech stocks left scores of companies that had hoped to find a toehold in the then-nascent world of online commerce in history’s dustbin.

As with the internet of 2000, Clark said, there’s little doubt that investments in AI will pay off for some companies. The question – one being asked and reevaluated constantly by the investment council during booms in one sector or the other, Clark said – is which ones.

“A lot of those companies that were around in 1999 did prosper, but over half of them disappeared, went bankrupt,” Clark told the council’s advisory board this week. “You can’t have 10 companies all get 30% market share. There’s going to be some disappointment.”

About the council

The council manages the assets of the South Dakota Retirement System, the Education Enhancement Trust, and the School and Public Lands Trust, among others.

The returns from investments and interest in the funds are used for a variety of purposes, such as boosting the state’s general fund and paying for scholarships. Unlike most states, the retirement system in South Dakota is fully funded for its participants, which include public employees ranging from teachers to correctional officers, state troopers and employees of the Department of Transportation.

On Thursday, council staff told board members that $13 million from the School and Public Lands Trust was transferred to schools in the month of February.

The South Dakota Retirement System returned 5.8% for the fourth quarter, underperforming compared to its benchmark. Staff told the board that quarterly underperformance was tied to a more conservative investment mix than its benchmark funds, which are more heavily influenced by the stock market.

Over the long-term, the state’s investments have grown considerably.

Today, at the 50-year mark in its history, the retirement fund is worth $14.5 billion and covers more than 33,000 recipients. When it began, there were 2,900 recipients and $50 million in the fund.

“The return over the full period has exceeded other state retirement systems across the nation,” according to the council’s 2023 annual report.

There’s a similar long-term growth trajectory for the managed assets as a whole. Day to day, week to week, and month to month, however, the funds may lose money or underperform.

Managing investments amid AI scramble

Board member questions on which sectors might be the best bets in the stock market followed a rundown of the state’s equity portfolio performance for the months of February and March. The council’s Jan Zeeck told the board that the equity portfolio moved into negative territory in February briefly before bouncing back to neutral last month, in line with a global rebound in durable goods orders.

Market volatility was an issue in the early months of 2024, Zeeck said, and the state has moved to a “defensive position” in response. The health care and pharmaceutical sectors have “taken a hit,” Zeeck said, as did consumer staples.

That comment prompted a board question on where the value might be in the market right now. Zeeck framed her response in part around the interest in AI. Pharmaceuticals and other staples, she said, are “just not exciting compared to all the talk of technology and AI.”

There are some significant differences between the 1999-2000 bubble and today, Zeeck said. The “Magnificent Seven” of the tech world – Microsoft, Alphabet (Google), Meta (Facebook), Apple, Tesla, Amazon and NVIDIA – are “bringing in a lot of cash flow, and it’s real.”

But that doesn’t mean investments in AI at companies like those will pay off in the long term, Zeeck said. NVIDIA stock has been on a roller coaster this year as the chip maker manages AI-related demand for its products.

“We don’t know what the returns will be on a lot of that,” she said. “Nobody really knows that yet.”

The state does have investments in tech firms, and Zeeck said they are “constantly evaluating” its position in those areas. In the full scope of the state’s managed assets, though, the technology sector and AI are minor factors.

“We really don’t have a big bet on tech stocks,” Clark told South Dakota Searchlight after the meeting.

GET THE MORNING HEADLINES DELIVERED TO YOUR INBOX

Anything that needs renovation or updating is especially tough to sell and price reductions are rife. A four-bedroom detached house with a swimming pool in St Mawgan has had its price cut from £1.5m to £1.25m between July and February.

Other sellers reacting to the market are the owners of a two-bedroom cottage – also in St Mawgan – reduced (twice) since December from £525,000 to £499,000; and a six-bedroom detached house on the Lizard Peninsula with a price reduction of £55,000 – from £750,000 to £695,000 between August and December.

Duncan Ley, of the estate agent Humberts, says: “We need more buyers. The market is improving but has some way to go – it will take two years to return to normality.”

Explaining the rise in properties coming on the market, he says that some vendors have been waiting out the frenetic post-Covid boom, loath to try and buy in such a competitive climate – and then were deterred by high interest rates last year.

Josephine Ashby, of John Bray & Partners, has just agreed an off-market sale on a holiday home in Polzeath for £3m for a family. “Part normal seasonal bounce, part pre-election urgency, it definitely feels like a buyer’s market,” she says.

Ireland says for families looking in the £500,000 to £1m bracket there’s still a shortage of suitable homes for sale. For those struggling to afford a family home for much less than that, the locations with the smallest affordability gap – where local wages are weighed against house prices – to buy a terraced house in Cornwall in 2022, were Camborne, Looe-Pelynt, St Austell Bat and Bodmin, according to research by the University of Exeter.

There is speculation that changes made in the Budget – a reduction in the higher rate of capital gains tax (CGT) on sales of residential property from 28pc to 24pc, and the abolition of extra tax reliefs for holiday lets that aren’t available to private rentals – might reverse the trend of people buying to profit from holiday lets.

Ashby says: “Perhaps the decrease in capital gains tax and the increased sting on furnished holiday rentals might push some wavering sellers into action, but it’s too early to tell.”

Dean Lonergan, of Jackson-Stops, adds that in some areas there is a glut of supply: “There are certainly more apartments coming on to the market in Newquay.”

There is a huge supply of holiday lets in Cornwall – but also huge demand. In February there were 16,295 available holiday let listings in the county, a rise of 18pc in a year, and 48pc more than in 2019, according to the analyst AirDNA. Demand for these properties has increased even more markedly, up 26pc in a year, and 185pc since February 2019. That suggests the staycation trend is not over – and owners may still balance their books.

Renting out holiday homes has become much more of a 12-month season in Cornwall, increasing the chances of making a profit even as reliefs are cut.

Buy-to-let investors are selling rather than buying, says Joanne Ireland of Relocate to Cornwall, a buying agent. “In Falmouth, for example, three-four-bedroom houses in their £300,000s used as student lets.”

“Landlords are getting out and we have zero enquiries from new ones,” says Jonathan Start, adding that the proposed end to section 21 notices is another factor, plus the prospect of a new Labour government. “We are not seeing any holiday let owners selling up yet.”

Buildings are responsible for more than a quarter of all greenhouse gas emissions — central heating in winter, air conditioning in summer, lighting all year round and power used by appliances from computers and phones to fridges and dishwashers, according to the experts.

With politicians in Britain and worldwide promising to bring down emissions, pressure is growing on property groups to make estates greener. Schroder Real Estate Investment Trust (SREIT) has seized the bull by the horns and its shares, now 42p, should respond. With 39 sites and more than 320 tenants, Schroder REIT has a diverse portfolio of commercial buildings, from industrial estates to office blocks and retail parks.

Property firms have not had an easy time but managers Nick Montgomery and Bradley Biggins have outperformed peers and delivered steady dividend growth. Now they are pledging to turn their portfolio from ‘brown to green’, using renewable energy, special boilers and a score of other initiatives.

The strategy is rooted in sound business sense. New rules are due by 2030, obliging property owners to cut buildings’ carbon footprint. By moving early, Schroder can show it is in the vanguard, winning friends among ecologically-minded shareholders and others.

Better still, the group can charge tenants more, many of whom are under pressure from investors, customers and employees to become ‘green and clean’.

Eco-friendly: With politicians in Britain and worldwide promising to bring down emissions, pressure is growing on property groups to make estates greener

While this may sound counter-intuitive when economic conditions are tough and businesses are strapped for cash, energy-efficient buildings are frequently cheaper to run so, even if rents are higher, overall costs should be on a par or lower than elsewhere.

Montgomery and Biggins choose their sites carefully, too, looking for areas where good stock is in short supply and demand is robust.

The company bought a business park just outside Cheadle, Manchester, surrounded by a couple of acres of land. After getting planning permission, they turned the space into the UK’s first net zero warehouse development, with solar panels, heat pump boilers and even a wildflower meadow.

Schroder paid £17 million for the property, spent £10 million upgrading it and has just had it valued at £40 million, with firms including German industrial giant Siemens happy to pay premium rates to secure space on this modern site.

Office blocks are turning greener under Schroder’s management too, such as The Tun in Edinburgh, where Montgomery and Biggins have introduced LED lighting, upgraded heating systems and signed premium rental agreements with blue-chip tenants.

Other properties include academic sites, such as the University of Law, Central London and well-located shopping sites, such as St John’s Retail Park, Bedford, where Lidl and B&M lure a steady stream of bargain hunters.

Industrial estates attract a range of tenants, too, from widget-makers to document storage firms, food delivery chains and even gyms.

Upgrades are a feature across the portfolio and Montgomery and Biggins make a point of engaging with tenants regularly. That facilitates rental growth and the duo anticipate growing income as economic conditions improve.

Schroder Reit is already in a robust financial position. The group’s year end runs to March 31 and a total dividend of 33.5p is expected, putting the stock on a yield of almost 8 per cent. Payouts should increase over time, especially as the firm took out long-term fixed-rate debt when interest rates were low.

Yet Schroder has been punished by the market, in line with other, less innovative property groups. Independent valuers suggest the company’s portfolio is worth £458 million. On the stock market, Schroder is valued at just £203 million, with shares more than 50 per cent below a 2018 peak.

Midas verdict: Schroder Reit has been hit hard by widespread antipathy towards the property sector but sentiment should change and Schroder shares should rally. At 42p, the stock is a buy, while generous dividends add to its appeal.

Traded on: Main market Ticker: SREI Contact: schroders.com or 020 7658 6000

House prices are set to bounce back in spring as lower mortgage rates lure buyers back into the market.

The number of property sales increased by 1pc to 82,940 between January and February, according to a report published by HMRC on Thursday.

The increase in transactions were due to improved buyer confidence as inflation and interest rates begin to steady, mortgage lenders said.

The Bank of England has held the base rate at 5.25pc since August, but this week accounting firm KPMG predicted the Bank would rates four times this year. Inflation, meanwhile, fell to a two-year low of 3.4pc in February.

Santander, HSBC and Barclays reduced mortgage rates this week, while others unveiled new deals to lure in homebuyers who “sat out” of the market in 2023.

Barclays cut fixed rates by up to 0.25 percentage points, with its two-year product now at 4.64% with a £999 fee.

HSBC’s equivalent deal is at 4.33% while Santander’s cuts include a five-year remortgage offer fixed at 4.34%.

Experts predict fixed mortgage rates could dip below 4pc within weeks as they react to an improving economic picture, easing affordability pressures on borrowers and fuelling optimism among homeowners.

The average two-year fixed-rate deal is now 5.8pc and the average five-year deal is 5.38pc, according to analyst Moneyfacts.