The National Assn. of Realtors on Friday said it will make changes to its commission rules to settle national allegations the requirements stifled competition, a move that may reduce costs for at least some consumers.

The settlement, which still must receive court approval, could mark a major change in the housing market.

Today, sellers typically pay a 5% to 6% commission when they sell their homes, with half of that going to the listing agent’s brokerage and half to the buyer agent’s brokerage, and critics of that model say the settlement could upend that practice.

“This settlement over time will benefit home sellers and buyers greatly, eventually lowering agent commissions by tens of billions of dollars a year and helping align agent compensation and services rendered,” Stephen Brobeck, a senior fellow with the Consumer Federation of America, said in a statement.

Under an existing Realtor rule, listing agents must make an offer of compensation to the buyer’s broker in order to list homes on NAR-affiliated multiple listing services, or the MLS.

Though NAR says this offer can be zero dollars, the requirement to post an offer — known in the industry as “cooperative compensation” — has reduced competition and kept commission rates artificially high, according to lawsuits filed against the Realtors. The rule has also caused buyers’ agents to “steer” their clients to homes that offer higher commission rates, the lawsuits allege.

In a news release, the national trade group said it continues to deny any wrongdoing as it relates to its current commission rule, but to settle the allegations, it will pay $418 million and prohibit offers of compensation to buyers’ brokers on affiliated multiple listing services, which also populate listings on sites such as Zillow and Redfin.

“NAR has worked hard for years to resolve this litigation in a manner that benefits our members and American consumers,” Nykia Wright, interim chief executive of NAR, said in a statement. “It has always been our goal to preserve consumer choice and protect our members to the greatest extent possible. This settlement achieves both of those goals.”

Home sellers could still offer to pay buyers’ broker commissions under the settlement if they communicated it outside the MLS, according to the National Assn. of Realtors.

But not setting the rules of the game at the outset will inject more competition into the process and open up new ways of payment that should lower costs, according to Robert A. Braun, a partner with Cohen Milstein Sellers & Toll, which is representing home sellers in two of the settling cases.

Braun said sellers may still choose to pay buyers’ agents something, or buyers may pay their agents directly after negotiating a fee. They may also choose to go without an agent altogether.

Another option? A buyer agrees to pay a certain price — say $800,000 — only on the condition that the seller then pays the buyer’s agent $24,000, or 3%. “You got a free market,” Braun said.

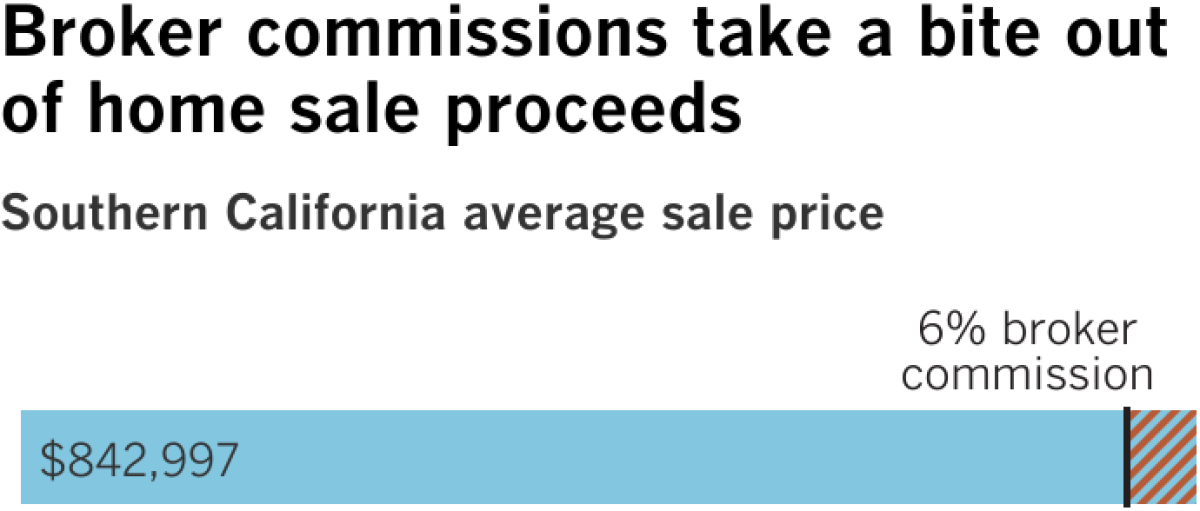

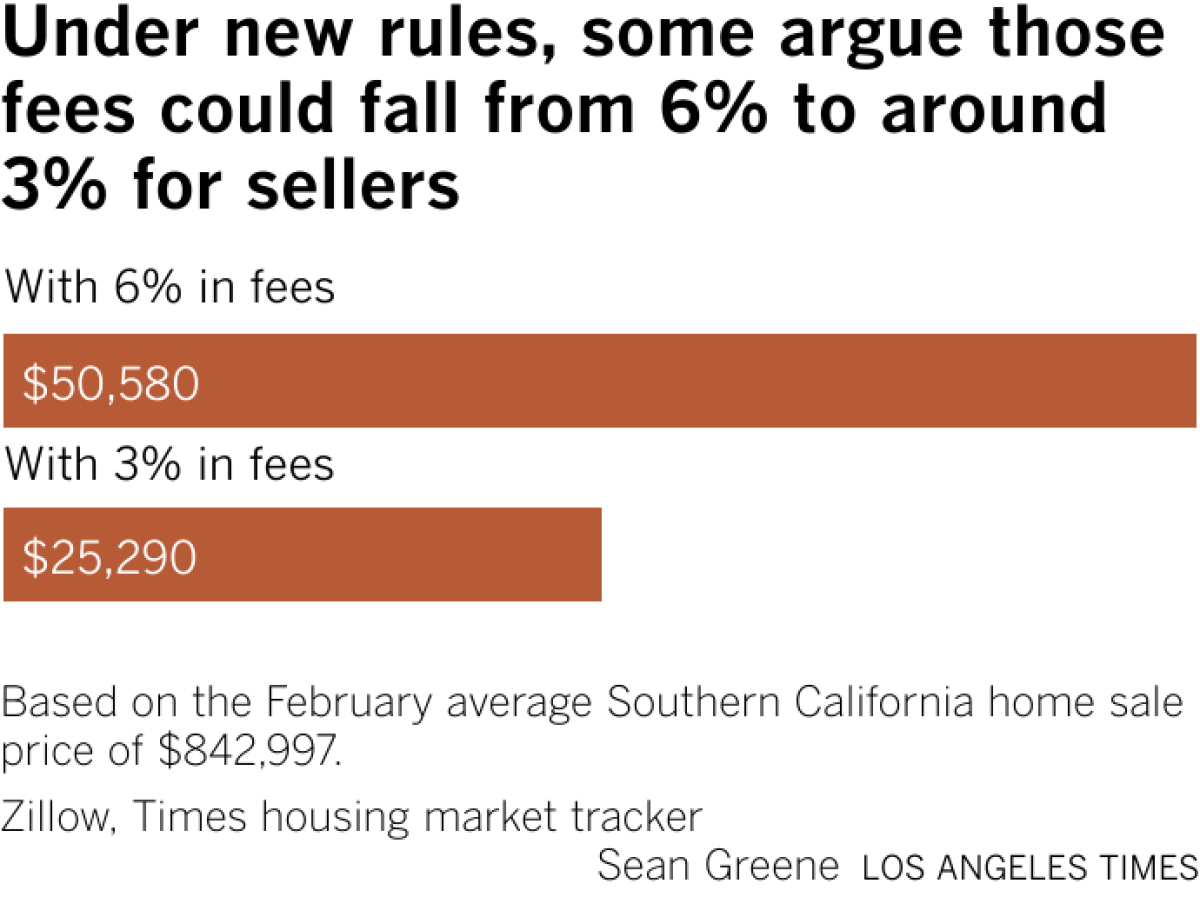

Commission rates are a small proportion of a sales price, but they add up. For a home sold at the average Southern California price of $842,997, 6% is $50,580.

If such changes drive down commissions overall, it could have a big effect on real estate agents who are paid a proportion of the commission sent to their brokerage.

Higher mortgage rates sent home sales tumbling, reducing pay for agents who are compensated based on the number and price of the deals they transact.

In California alone, NAR lost 9,723 members from December 2023 to January 2024 — a 4.75% decline.

Not all agents are worried.

Michael Khorshidi works mostly with buyers, but sees the new requirements as an opportunity to show the value he brings to clients. Agents who aren’t able to demonstrate their worth will be the ones who lose work, he said.

“We’re always transitioning,” Khorshidi said. “This is just the latest transition.”

If the settlement ends up creating a system in which buyers pay their agents directly, it could saddle them with new costs.

However, Braun argued that buyers would ultimately see reduced costs as well because under the current system, buyer agent commissions get passed along to buyers in the form of higher home prices.

That doesn’t mean sellers make a conscious decision to set their home prices higher because they need to pay a buyer’s agent. Rather, Braun said it means fewer homes make financial sense to sell because some homeowners don’t have enough equity to pay two commissions.

If buyers paid their own agent, more homeowners could afford to sell, increasing supply and helping put downward pressure on price, Braun said.

“Going forward, there is a significant likelihood home prices will be lower than they otherwise would be,” he said.

Michael Copeland, a real estate agent in Palm Springs, doesn’t think the agreement will alter the market too dramatically.

To bring in buyers, sellers may still be incentivized to cover both commissions — just as they do today.

Excitement is in the air as the fabulous 12,000-square-foot Clubhouse is taking shape at RiverCreek in Estero. Nestled on a more than 4-acre recreational complex, the Clubhouse at RiverCreek will be the hub of the communitys vibrant lifestyle and activities.

Residents will revel in year-round fun at the elegant Event Room for happy hours and social events organized by a dedicated lifestyle director. The Sports Lounge and Card Salon will offer spaces for poker, Texas Hold Em, Mahjong, and more. Homeowners can stay fit at the fully equipped fitness center or enjoy the Indoor Sports Complex for basketball. Outdoors and sports enthusiasts can play tennis, pickleball, or bocce on shaded courts. The resort-style pool, shaded cabanas, and cozy fire pit provide relaxation, while younger residents will love the interactive splash park and shaded playground for fun in the Florida sun.

The contemporary-style new homes priced from the $600s to $800s at RiverCreek perfectly complement the fabulous lifestyle found within. At RiverCreek, youll discover Esteros best new home value and enjoy in-style living with amazing one- and two-story home designs featuring a gorgeous selection of luxury standard features. RiverCreek offers a variety of floorplan designs ranging in size from approximately 1,900 to over 4,300 square feet and includes up to five bedrooms, master suites upstairs or downstairs, 2-3 car garages, and plenty of flexible living spaces.

This incredible new community has it all, offering a resort lifestyle that is second to none and incredible new home designs in a beautiful Estero location. RiverCreek, which is off the Corkscrew Road corridor and just east of I-75, is one of Southwest Floridas most well-liked communities. Residents here can access a wide range of dining, shopping, top-notch schools, and entertainment options.

Models are open daily for tours at RiverCreek. For more information, call (239) 308-4600 or visit GLHomes.com/RiverCreek.

About GL Homes

Founded in 1976, GL Homes is a uniquely American success story. Built by Itchko Ezratti, who believed that hard work, integrity, and quality craftsmanship would thrive in the marketplace, GL Homes has since grown into one of Floridas largest homebuilders.

Misha Ezratti, son of company founder Itchko Ezratti, is President of GL Homes and leads the charge in overseeing operations across the state of Florida today. Misha Ezratti continues to reinforce the culture started by his father, namely, that every employee and customer is part of the GL Homes family. Those enduring values are reflected in every home built by GL Homes today.

With a more than 45-year track record, countless industry awards and accolades, and, most notably, more than 100,000 happy GL homeowners, its easy to see how Itchko Ezrattis GL Homes has grown into a top luxury home builder across both Florida and the nation.

This news content may be integrated into any legitimate news gathering and publishing effort. Linking is permitted.

News Release Distribution and Press Release Distribution Services Provided by WebWire.

A house for sale sign is shown in front of a house in Oakville, Ont., in February, 2023.Richard Buchan/The Canadian Press

A decade ago, Joe Bladek’s clients typically put down deposits of between $1,000 and $5,000 when making an offer on a new home. Today, the Barrie, Ont.-based mortgage broker said, those deposits are more commonly in the range of $5,000 to $10,000 – and recently, he worked on an offer where the buyer put down a $50,000 deposit and had to ask family for help to scrounge up the funds.

“A lot of clients don’t realize that deposits are quite large these days,” Mr. Bladek said. It’s partly owing to the higher cost of homes themselves, since deposits are typically between 1 to 10 per cent of the sale price. But it’s also a holdover from the pandemic bidding wars, when buyers sought to compete with firm offers. And while deposits come from the down payment, buyers need to have the money on hand.

It’s just one example of how the costs linked to buying and selling a home have crept up over the years, largely because of higher housing prices.

Experts say buyers should typically expect to spend between 1 and 5 per cent of a home’s purchase price on moving and closing costs.

Twenty years ago, if someone were to buy a house at the national average price of $245,149, they would have likely spent between $2,450 and $12,250 to close on their house and to move. At the end of 2023, someone who bought at the national average price of $657,145 would have needed to pay between $6,571 and $32,857 for moving and closing costs.

A statistic used often by the real estate industry, though hardly ever with a citation, says that Canadians move every seven years on average. If true, a hypothetical buyer who moved three times in the past 20 years could have spent a total of between $15,000 and $62,000, roughly, depending on the value of their homes.

In Toronto, where the average house price was $1.126-million at the end of 2023, moving and closing costs would range from $11,260 to $56,300. Now imagine today’s first-time buyers moving multiple times over a lifetime.

Rona Birenbaum, certified financial planner and the founder of Caring for Clients in Toronto, said moving costs can hurt someone’s financial plan in the short term. While she said they’re often not enough to derail someone’s financial picture, “they don’t give you any kind of return on investment; they are absolute expenses,” she said.

“That money that comes out of the client’s financial picture – if it was in the financial picture, it would be compounding. So you lose the compounding on that money, on that wealth.”

Ms. Birenbaum added that in particular for older Canadians, multiple moves later in life can eat into funds that should be earmarked for necessary living expenses and end-of-life care.

For some buyers at the margin, the costs associated with closing on a home and moving house can change the economics of buying.

“They can be very prohibitive,” said Mr. Bladek. “Some clients of mine who’ve come to me wanted to move into a new home and can qualify for that new home, but with all the fees involved and the market the way that it is … can’t make it at the end of the day.”

There are plenty of costs linked to buying or selling a home in Canada, including land transfer tax (in most provinces), lawyer and realtor fees, title transfer and insurance, deposit money, property appraisal fee, home inspection, a status certificate for condo owners, and of course, movers, among others.

The biggest cost for many buyers is the land transfer tax, said Daniel La Gamba, a real estate lawyer and founding partner of LD Law LLP in Toronto. Ontario, Quebec, British Columbia, Manitoba, Nova Scotia, New Brunswick and Prince Edward Island have such taxes, and Toronto homeowners pay double the tax of buyers elsewhere in Ontario. Montreal also has its own land transfer tax.

Land transfer taxes are based on property value and often run in the thousands of dollars, though each province takes a slightly different approach. New Brunswick and Prince Edward Island charge a flat rate of 1 per cent of the purchase price or assessment value; Nova Scotia’s is 5 per cent; the other provinces have marginal tax brackets. While the taxes themselves have remained consistent for years, steadily climbing home prices mean that someone buying today is likely facing a heftier upfront tax bill than they would have in years past.

Mr. La Gamba said that someone buying a million-dollar home in Ontario would pay $16,475, and that amount would increase to $32,950 for someone buying in Toronto.

Sellers also pay the commission for both their agents and the buyer’s, which come to a combined 5 per cent plus sales tax, though Mr. La Gamba noted there is the potential to negotiate.

The cost of moving services themselves also spiked during the pandemic as fuel and labour shortage costs hit local and long-haul movers. According to Statistics Canada, moving company rates increased a whopping 18.9 per cent in the third quarter of 2021, and have continued to post small increases in the years since.

Are you a young Canadian with money on your mind? To set yourself up for success and steer clear of costly mistakes, listen to our award-winning Stress Test podcast.