A financial analyst nicknamed the ‘Oracle of Wall Street’ has said a ‘growing crisis of the young American male’ will cause house prices to fall as much as 30 percent.

Meredith Whitney, who earned the title after predicting the financial crisis of 2007 – 2008, suggested young men increasingly living with their parents and disinterested in starting families will drastically reduce housing demand.

The trend of men refusing to settle in turn means more women are remaining single into later life, leaving them without the income or need for big family homes.

But it comes as baby boomers start to downsize, meaning there will be a surplus of available family homes. Much of the last decade’s gains in property values have been driven by high demand and low supply – a phenomenon, Whitney says, is reversing.

To explain the rise in men living at home, she pointed to the increasing prevalence of video games, starting in the mid-2000s.

Meredith Whitney, also known as the ‘Oracle of Wall Street,’ has predicted house prices are set to fall because men are increasingly disinterested in starting families

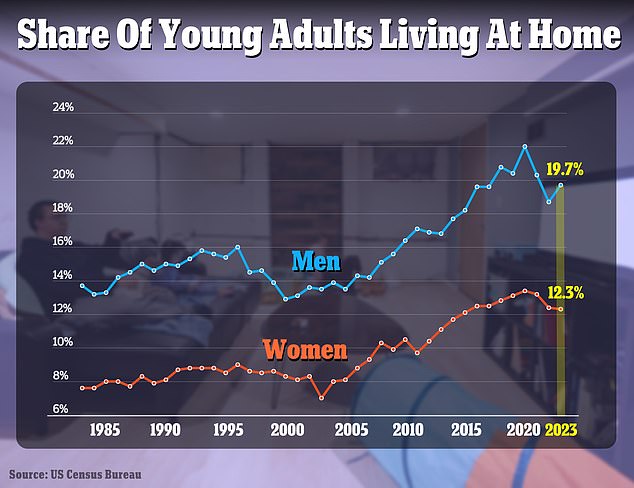

Over the last decades, the number of young men living in their family home has been on the rise. (Young adults are defined as those aged between 25 and 34)

‘You feel like you’re with other people but you’re actually at home alone, and that created a big chasm in young male sociability,’ she told DailyMail.com.

Whitney cited US Census Bureau data showing that before the financial crisis around 13 percent of men aged between 25 and 34 lived at home.

That rose to as high as 22 percent during the pandemic but even after falling back down was still almost 20 percent in 2023. It was only in the last decade that rate had risen above 16 percent.

The data also shows that young women have consistently been around twice as likely to leave their parents’ homes. Last year, just 12.3 percent were still at home.

The figures coincide with a decline in romantic relationships among young men. A 2023 Pew Research study found 63 percent of males under 30 describe themselves as single.

Experts have attributed the figures to a confluence of factors such as increased porn consumption, the rise in hook-up apps and the legacy of lockdown during the pandemic.

‘The pace at which young men live at home versus young women live at home is around 2x, I correlated all of this with in the early, mid-2000s launch of the Xbox, Wii and PlayStation,’ she said.

‘The biggest driver of home prices has historically been household formation,’ Whitney told DailyMail.com. ‘Household formation today is the lowest it’s been in 160 years.’

And household formation, she said, is driven by the ‘five Ds’ – ‘diamonds, diapers, divorce, debt, and death.’

‘Without at least the first two Ds, there’s no reason to buy a home,’ she said.

Whitney previously told Fortune the drop could be as much as 30 percent.

Whitney attributed the increasing rate of men living at home to the rise of video gaming, starting in the mid-2000s

Single women have increasingly been purchasing homes of their own. Female buyers alone make up 19 percent of American homebuyers – almost double that of single men – according to recent data from the National Association of Realtors.

That is a stark contrast from 40 years ago when the portion of single women and men buying homes was roughly the same – 11 percent and 10 percent respectively.

As of 2023, the proportion of single men purchasing property has stayed steady at 10 percent. According to the NAR, the share of recent buyers who are married couples has also dropped to 59 percent.

In 1981, when the organization began analyzing the profiles of buyers and sellers, married couples made up 73 percent of homeowners.

However, according to Whitney, single women alone will be unable to absorb the entire supply of large, family homes.

‘I don’t see single women buying a four bedroom, three bath home,’ she said.

And spurring the downsizing of the elderly into smaller homes are rising costs, Whitney said.

Despite the inconvenience of moving in old age, burdensome costs like household expenses, property taxes, insurance, utilities, homeowners association fees and mortgages may leave them with little choice.

Single women are purchasing an increasing share of homes but Whitney doubts they will be able to absorb all the demand, so prices will fall. Pictured is a ‘for sale’ sign outside a home in Phoenix, Arizona

Whether or not aging baby boomers will vacate their homes and flood the market in the coming years is uncertain

While the youth aspiring to buy homes may be eagerly waiting for baby boomers and older homeowners to start vacating theirs, whether or not that will happen is up for debate.

A Redfin survey in February found that out of more than 800 Americans aged 60 and older, some 71 percent said they would stay in place in their current homes.

A separate study by government-backed lender Freddie Mac downplayed the significance of the ‘silver tsunami’ – a metaphor sometimes used to describe population aging.

‘Some have warned of a ‘silver tsunami’ as aging boomers look to sell their homes, flooding the market with inventory,’ it read.

‘But as this analysis demonstrates, the tsunami is more like a tide, bringing a gradual exit that will mostly be offset by new entrants.’

Home prices have doubled in less than ten years in 68 of the 100 largest cities in the US, a sobering new study shows.

And in some major American cities, the cost of the average property has doubled in as little as five years.

In Detroit, home prices were half of what they are now as recently as 2019, data from real estate marketplace Point2 reveals.

Home prices in Miami and Tampa, Florida, have doubled since 2018, as they have in Baltimore, Maryland, and Spokane, Washington.

Buyers in Irvine, California – the most expensive housing market in the study – have seen average home prices double from an already steep $750,000 to $1.5 million in just seven years.

A storm of high inflation and interest rates, tight supply and surging demand has meant that the national median home price has yo-yoed toward around twice what it was a decade ago.

The cost of the average home in the US has gone up from around $200,000 to around $400,000.

According to Point2, a common home appreciation theory is that residential properties tend to double in value in about 10 years.

In the so-called ‘Motor City’ Detroit, one of the reasons that house prices have risen twofold in half this amount of time is because they have been historically low compared to the national average.

House prices in the city have been among the fastest-growing in the US in recent years, as the city bounces back from the mortgage crisis which left some homes virtually worthless.

Less than two decades ago, one in five houses stood empty in the city with foreclosures mounting and properties on deserted streets being sold for $1.

The crisis and the demise of the big carmakers – which had previously made Detroit an industrial powerhouse – drove millions from their homes.

But as the car industry – this time with a focus on electric vehicles – begins to pick up speed again, house prices have risen rapidly.

House prices in Detroit have been among the fastest-growing in the US in recent years, as the city bounces back from the mortgage crisis which left some homes virtually worthless

At the start of 2019 you could buy a home in Detroit for $40,000, according to Point2.

Now, according to listings website Realtor.com, the median home listing price in the city is $89,900.

Despite the short-term price surge, Detroit still remains among the more affordable of the major cities in the US.

Detroit was lagging behind other cities in terms of house price growth, according to CoreLogic chief economist Selma Hepp, so some of this growth is catch-up.

Similarly, data shows that prices also doubled quickly in Spokane, where not that long ago, in March 2018, a home cost just $184,500 – compared to $371,000 today.

Spokane has seen house prices surge as Americans have moved to the city amid investor interest and urban revitalization efforts.

And some people who fled to so-called pandemic ‘boomtowns’ such as Boise, Portland and Austin, later moved to Spokane in search of cheaper housing – which has driven up prices further.

Prices also doubled quickly in Spokane, where not that long ago, in March 2018, a home cost just $184,500 as compared to $371,000 today

According to Point2, home prices have accelerated just as dramatically in Miami, as well as in Tampa, amid a surge of new residents.

The past six years were enough for homes to double in cost to about half a million dollars in both cities.

Prices in all five of the largest markets in Florida – including Jacksonville, Orlando, and St. Petersburg – have doubled in just six to eight years.

Arizona is in a similar position – with seven large cities doubling in price between six and seven years.

Prices increased twofold in booming Scottsdale, where the average home costs a huge $837,500 compared to $416,000 at the end of 2017.

Phoenix has also seen a surge in home prices – which local incomes can barely keep up with.

Home prices have surged dramatically in Miami amid a surge of new residents

House prices in Tampa, Florida, have doubled in the last six years according to Point2

It comes as separate data shows the US housing market gained a huge $2 trillion in value in the last year alone, amid a historic shortage of homes for sale.

Soaring mortgage rates mean many Americans locked into lower deals have stayed put, leading to a significant inventory shortage.

This, in turn, has meant home values have continued to rise, pricing many Americans out of the market entirely.

While mortgage rates had been slowly declining in the first months of this year, the average 30-year fixed rate deal is beginning to creep up again.

Following data released earlier this week which showed inflation remains stubborn, the average 30-year mortgage deal rose to 6.88 percent, according government-backed lender Freddie Mac.

America has a record number of ‘million-dollar cities’ – where the average house price now exceeds six figures, new data shows.

In total 550 US cities have an average property price of $1 million or above, up by 59 from this time last year.

The data from property portal Zillow lays bare how red-hot America’s real estate landscape remains after years of consistent growth.

California alone counts 210 ‘million-dollar cities’ – the highest of any US state and an increase of 12 from last year.

It was followed by New York, New Jersey and Florida which count 66, 49 and 32 respectively.

California alone counts 210 ‘million-dollar cities’ – the highest of any US state and an increase of 12 from last year. Pictured: a San Francisco home on the market for $1.49 million

In total 550 US cities have an average property price of $1 million or above. Pictured: a San Francisco home on the market for $1.49 million

The growth of luxury real estate has largely outstripped the general housing market, Zillow’s research shows.

While typical US home values have grown 4.2 percent compared to last year, those in ‘million-dollar cities’ had seen an average year-on-year increase of 4.6 percent.

New Jersey has experienced the biggest increase in cities where home values are over $1 million. It added 14 to its state in the last year.

Meanwhile New York, San Francisco, Los Angeles and Boston were the four metro areas with the highest amount of ‘million-dollar cities.’

It comes as America’s so-called ‘frozen’ property market shows signs of thawing as the number of new listings advertised on Zillow increased 20 percent between January and February.

Soaring mortgages have created a ‘lock-in effect’ as homeowners are reluctant to trade in the cheap 30-year fixed deals they secured before rates started rising.

Data from Government-backed lender Freddie Mac shows the average rate on a 30-year fixed mortgage is now 6.79 percent.

This is more than double where they were three years ago when they were hovering at 3.17 percent.

New York, San Francisco, Los Angeles and Boston were the four metro areas with the highest amount of ‘million-dollar cities.’ Pictured: a $1 million home currently for sale on Zillow in Boston, MA

An LA home for sale for $1.49 million on Zillow

The New York metro area had the largest amount of ‘million-dollar cities.’ Pictured: a $1.5 million apartment for sale in Manhattan’s Lenox Hill

It means a buyer purchasing a $400,000 property today faces monthly payments of $2,474. This analysis assumes a 5 percent downpayment.

However, had they bought in March 2021, this figure would be just $1,637 – a difference of $800 per month.

Yet a recent report by Zillow suggested housing activity was starting to uptick again.

Homes that sold in February spent an average of 17 days on the market – slower than during the homebuying frenzy of 2021 and 2022 but still much faster than pre-pandemic.

Experts are divided over where the housing market is now headed after they have remained surprisingly resilient.

Last week Shark Tank star Barbara Corcoran predicted even the smallest drop in mortgage rates would cause property values to shoot up.

She told Fox Business: ”If rates go down, just another percentage point, prices are going to go through the roof.

‘Everyone will come out and buy. There are probably 10 buyers on the sidelines [for each home on the market] waiting for interest rates to come down,’ she continued. ‘So everybody’s going to charge the market.’

Contrastingly, analyst Meredith Whitney recently told DailyMail.com that prices would soon fall as more and more Baby Boomers start to downsize -and free up inventory.

Whitney – who earned the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crash – said: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

Shark Tank star Barbara Corcoran has revealed when housing prices will go ‘through the roof’.

The self-made real estate millionaire said a fall in interest rates is key – to lower the cost of borrowing and attract buyers who will bid up prices.

The ‘magic number’ is a fall of 1 percent to take mortgage rates under 6 percent.

‘If rates go down, just another percentage point, prices are going to go through the roof,’ Corcoran said in a Fox Business interview Wednesday.

‘Everyone will come out and buy. There are probably 10 buyers on the sidelines [for each home on the market] waiting for interest rates to come down,’ she continued. ‘So everybody’s going to charge the market.’

As of latest data from government-backed lender Freddie Mac from March 21, the average 30-year fixed rate mortgage is 6.87 percent.

That is down from the 8 percent rates seen in October last year, but still double the historically low rates of around 3 percent seen during the pandemic.

What is needed to get the mortgage rate to fall below the 6 percent that Corcoran sees as ‘the magic number that people get juicy about’?

While the Federal Reserve does not directly set mortgage rates, the benchmark borrowing rate it sets does indirectly influence the amount Americans pay on a loan to purchase a home.

Mortgage rates track the pattern of 10-year Treasury Yields, which are determined by a range of factors including inflation, economic growth and the Fed’s benchmark funds rate.

The Federal Reserve left interest rates unchanged for the fifth consecutive meeting earlier this month, keeping benchmark borrowing costs at a 23-year high between 5.25 and 5.5 percent.

The Fed‘s series of aggressive rate hikes were intended to pour cold water on rampant inflation, which peaked at 9.1 percent in June 2022.

At its latest meeting, Fed policymakers penciled in three quarter-percentage point cuts by the end of the year – but did not commit to a date when it might start decreasing rates.

If interest rates fall, this will then have an impact on mortgage rates.

But Corcoran warned Americans that instead of getting a cheaper deal when rates come down, the housing market may actually heat up.

Corcoran warned Americans that if interest rates come down, it will mean house prices will go up even further as demand to buy suddenly soars

As of latest data from government-backed lender Freddie Mac from March 21, the average 30-year fixed rate mortgage is 6.87 percent

‘If you wait for interest rates to come down by another point, I don’t think you’ll gain, I think you’ll wind up paying more because I wouldn’t be surprised if real estate went up by another 8 or 10 percent if interest rates come down another point,’ she said.

Elevated mortgage rates and a historic shortage of homes for sale has meant that house prices are already high – pricing many Americans out of the market.

In 2023 alone, the US housing market gained $2 trillion in value.

Corcoran’s comments come after a survey from real estate listings company Realtor.com revealed that the majority of homebuyers would need mortgage rates to dip to 5 percent before they followed through on a purchase.

Some 72 percent of potential home buyers said pulling the trigger would be feasible if mortgage rates dropped below 5 percent

According to the survey of 5,000 US consumers, conducted during the first week of November when rates were at their highest, about 18 percent of Americans said they were waiting for rates to fall below 7 percent.

If they dropped below 6 percent, an additional 22 percent of respondents said they would buy a home.

But the vast majority – some 72 percent – said rates would need to go below the ‘magic’ mortgage rate of 5 percent before they would sign on the dotted line for a home.

- Research shows homes listed in the first fortnight of June attract price premium

- Sellers stand to make an extra $7,700 on a typical property, Zillow claims

- Experts say America’s property market is finally showing signs of thawing

- Sellers could also see a big drop in costs after the trade body for realtors last week agreed to eliminate a notorious commission scheme

Homeowners looking to sell up may wish to wait until the summer if they want to maximize their profits.

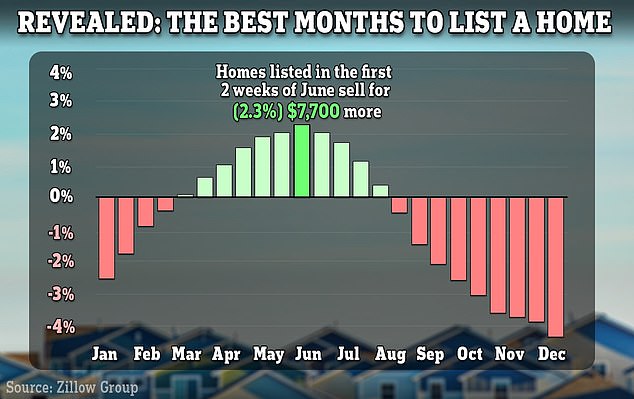

New analysis by property portal Zillow shows home listed in the first two weeks of June typically sell for $7,700 more than they would do otherwise.

By comparison, sellers risk shaving more than 4 percent off their asking price if they wait until December.

The findings of the report are another reason to hold off selling for now – it emerged last week that commission fees charged by real estage agents are set to drop in the summer.

The housing market historically always heats up in the spring and summer months as parents want to relocate ahead of the next schoolyear.

New analysis by property portal Zillow shows home listed in the first two weeks of June typically sell for $7,700 more than they would do otherwise

Sellers’ homes also benefit from fresh flowers and greenery after the winter.

Amanda Pendleton, a home trends expert at Zillow, told CNBC: ‘It’s sort of an ideal time for both buyers and for sellers, and that’s why we just see a lot more activity that time of year.’

Experts claim Americans frozen property market is finally showing signs of thawing. A report by Redfin found the number of new listings jumped 14.8 percent compared to a year ago – the largest annual increase since May 2021.

Prior to the pandemic, May was the hottest month to list a property. However, a volatile mortgage market saw this pushed back to June last year.

According to Zillow’s data, homes listed in the first fortnight of June 2023 sold for 2.3 percent more than average. It equates to a $7,700 boost on an average home.

Prime selling months vary slightly by city though, researchers noted.

For example, in New York, homes listed in the first half of July tended to attract a 2.4 percent premium – or $15,500 in real terms.

Meanwhile sellers in Los Angeles should strike in the first half of May to benefit from a 4.1 percent premium on their home listing. It works out at $39,300 extra.

Prior to the pandemic, May was the hottest month to list a property. However, a volatile mortgage market saw this pushed back to June last year

America’s property market has all but frozen in response to soaring mortgage rates deterring owners from moving.

The average rate on a 30-year fixed-rate home loan is now 6.74 percent, according to Government-backed lender Freddie Mac.

This is almost double where they were in March 2022 when they were hovering at 3.76 percent.

It means a buyer today purchasing a $400,000 home faces paying around $700 per month on their mortgage than had they bought two years ago. This analysis assumes a 5 percent downpayment.

Rising rates have created a ‘lock-in effect’ whereby buyers do not want to give up their cheap deals.

America’s property market has been all but frozen as a result. In the first week of March, applications to purchase a home were 11 percent lower than the same period a year ago, according to the Mortgage Bankers’ Association.

Research out in February revealed the ‘magic’ mortgage rate that will kickstart the housing market.

A majority of prospective home buyers say they would finally follow through with the purchase of a home if rates dipped below 5 percent, according to a new survey by Realtor.com.

There was more good news for sellers last week. They could see a BIG drop in selling costs after realtors agreed to eliminate notorious commission scheme and pay $418 million damages in landmark legal settlement.

Meanwhile, millions of homebuyers could soon be in line for a $10,000 tax credit under sweeping reforms of the housing market proposed by President Biden during his State of the Union address.

America’s real estate market is steeped in uncertainty as soaring mortgage rates effectively freeze buyer activity.

It has left many questioning: is property still a good investment?

But a new study by GoBankingRates claims to shed light on the areas that are most likely to help owners get the best returns.

Researchers analyzed the average house price – as recorded by Zillow – in major US metros as of January 2024 and established where prices have risen quickest in the past five years.

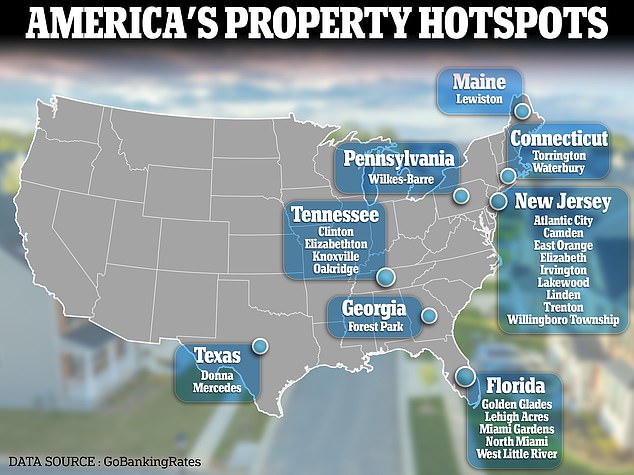

Their findings show that Atlantic City, New Jersey, is the best place to gain value on a property. The average home in the area costs $218,761, having shot up 102 percent in price since 2019 and 16 percent in the last year alone.

A new study by GoBankingRates claims to shed light on the areas that are most likely to help owners get the best returns

It was followed by Waterbury, Connecticut, where the typical home costs $249,073, up 15 percent from last year and 100 percent from five years ago.

The top five was rounded out by Lewiston, Maine, Mercedes, Texas, and Torrington, Connecticut.

By comparison, the national average home value in the US in January 2024 was $343,951, up 50 percent from 2019 and 3 percent from last year.

New Jersey was the state to appear most prominently on the list, with nine of the 25 places ranked located in the Garden state.

It was followed by Florida and Tennessee which had four cities each on the list.

Notably no cities in New York or California made the top 25. The rankings were compiled by combining the percentage changes in each city in one year and in the last five years.

The findings come after a separate report by property portal Redfin found the US housing market had gained $2 trillion in value over the last year.

Redfin’s analysis of more than 90 million homes across the country found the total value of residential real estate had increased 5.3 percent to $47.5 trillion in December.

However, experts have repeatedly sounded the alarm over a real estate ‘correction’ which will see house values fall somewhat after ballooning during the pandemic.

Former Oppenheimer analyst Meredith Whitney – who has been dubbed the ‘Oracle of Wall Street’ after predicting the 2008 financial crash – told DailyMail.com that house prices would start to fall as Baby Boomers begin downsizing.

She said: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’, said house prices in some states will fall this year

Mortgage rates are hovering close to 7 percent – almost double where they were two years ago

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

The average rate on a 30-year fixed-rate home loan is now 6.94 percent, according to Government-backed lender Freddie Mac. It is almost double what they were two years ago.

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Data from Redfin shows that the typical US homeowner now spends twice as long in their properties as they did in 2005.

Today an owner can expect to spend 11.9 years in the same property, compared to 6.5 years two decades ago.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

| City | Average house price | % change in 1 year | % change in 5 years |

|---|---|---|---|

| Atlantic City, New Jersey | $218,761 | 16% | 102% |

| Waterbury, Connecticut | $249,073 | 15% | 100% |

| Lewiston, Maine | $274,687 | 14% | 91% |

| Mercedes, Texas | $123,572 | 13% | 92% |

| Torrington, Connecticut | $255,834 | 14% | 81% |

| Irvington, New Jersey | $359,441 | 10% | 101% |

| Elizabeth, New Jersey | $498,548 | 15% | 75% |

| Knoxville, Tennessee | $341,351 | 12% | 88% |

| Camden, New Jersey | $115,800 | 12% | 85% |

| Trenton, New Jersey | $307,421 | 12% | 84% |

| Oakridge, Tennessee | $285,447 | 11% | 92% |

| East Orange, New Jersey | $425,011 | 11% | 90% |

| Golden Glades, Florida | $490,839 | 11% | 86% |

| Willingboro Township, New Jersey | $303,989 | 10% | 92% |

| West Little River, Florida | $401,228 | 12% | 84% |

| Lakewood, New Jersey | $402,932 | 13% | 75% |

| Donna, Texas | $131,471 | 11% | 84% |

| Wilkes-Barre, Pennsylvania | $137,986 | 10% | 87% |

| Forest Park, Georgia | $177,414 | 5% | 114% |

| Clinton, Tennessee | $287,509 | 11% | 82% |

| Miami Gardens, Florida | $449,676 | 11% | 81% |

| North Miami, Florida | $473,109 | 10% | 84% |

| Linden, New Jersey | $497,627 | 13% | 71% |

| Lehigh Acres, Florida | $312,991 | 9% | 90% |

| Elizabethton, Tennessee | $203,565 | 12% | 74% |

The US housing market gained a huge $2 trillion over the last year, amid a historic shortage of homes for sale.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023, up from $474,740 a year earlier.

According to Redfin analysis of more than 90 million homes across the country, the total value of US residential real estate increased 5.3 percent from a year earlier to $47.5 trillion in December.

While soaring mortgage rates mean housing demand is sluggish, home values continue to rise, pricing many Americans out of the market.

In the last two years, the housing market has gained $5.6 trillion, Redfin found.

However a disparity remains across the US. While affordable East Coast and Midwest metros saw the biggest rise in home values in the last year, so-called pandemic ‘boomtowns’ have seen the largest decline.

The average home rose more than $20,000 and is now valued at $495,183 as of December 2023. The biggest rises were on the east coast of America

Scroll down for the full list of metros with the biggest price rises.

According to Redfin, there are three major reasons why home values are continuing to rise.

Many homeowners are locked into ultra-low mortgage rates from previous years, meaning they are hesitant to put their houses on the market.

With supply tighter than demand, buyers are competing for a limited pool of homes. That is propping up values for both properties that are already for sale, and those that could hit the market in the future.

The total value of US homes was nearing a trough at the end of 2022, which is part of the reason year-over-year growth at the end of 2023 was so large, it added.

It is typical for home values to cool in the winter, but they experienced an abnormally large slowdown in 2022 as the shock of surging mortgage rates sent a freeze through the housing market.

While America grapples with a housing shortage, it is also continuing to build homes, which contributed to the gain in total home values last year, Redfin said.

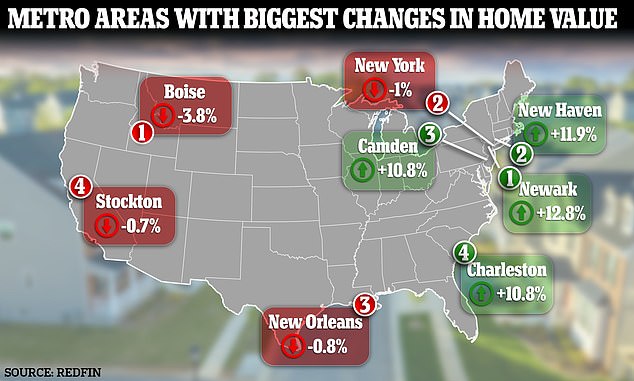

Home values in Newark, New Jersey, saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion.

Next come two other East Coast metros, New Haven, Connecticut, and Camden, New Jersey. Homes in New Haven gained 11.9 percent in value to $86.5 billion, while properties in Camden went up by 10.8 percent to $153 billion.

Home values in Newark, New Jersey , saw the biggest gain in value in the year to December 2023 – increasing by 12.8 percent to $359.6 billion

Fixed 30-year mortgage rates are now hovering around 6.9 percent, according to Government-backed lender Freddie Mac

Charleston, South Carolina, ranked fourth – with values increasing by 10.8 percent to $188.5 billion.

Next are three Midwestern metros, Elgin, Illinois, Grand Rapids, Michigan and Milwaukee, Wisconsin.

Places like Newark and Camden are likely seeing home values jump in part because they are attracting demand from people who are priced out of New York and can now work remotely, Redfin said.

Midwestern metros like Milwaukee and Grand Rapids are experiencing home value gains for a similar reason.

They are affordable, and when mortgage rates and home prices are elevated, demand for affordable homes goes up.

‘America’s homeowners are sitting pretty. They’re holding a massive amount of housing wealth, despite lackluster demand from buyers, because home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao.

‘Prospective buyers aren’t as lucky. The combination of elevated mortgage rates, high home prices and a limited pool of homes for sale means homeownership is about as unaffordable as ever.’

But not every homeowner has seen their property increase in value.

‘Home values skyrocketed during the pandemic and now a supply shortage is preventing those values from falling,’ said Redfin economics research lead Chen Zhao

Four metros saw declines in overall home value, according to Redfin.

Pandemic ‘boomtown’ Boise, in Idaho, saw prices decline 3.8 percent to a total of $123.9 billion and New York saw prices fall 1 percent to $2.4 trillion.

New Orleans prices went down 0.8 percent to $124 billion and homes in Stockton, California, lost 0.7 percent in value – falling to a total of $109.2 billion in value.

The metros with the smallest increases were Philadelphia, at 0.3 percent, Honolulu, at 0.8 percent, Austin, Texas, at 1 percent, Denver at 1.3 percent and Riverside, California at 1.6 percent.

Most of these metros have something in common, said Redfin, which is that they have become unaffordable for many homebuyers. This means that there is a cap on demand, so home values no longer have much, if any, room to rise.

New York, Honolulu, Riverside and Denver all have median home sale prices of at least $550,000 – well above the national median.

And in Boise and Austin, which also have median sale prices above the national level, many people are priced out because an influx of out-of-towners caused home values to skyrocket during the pandemic.

But some experts predict that there will be a shift in the housing market in some parts of the US in 2024, driven by a surge in Baby Boomers downsizing into smaller properties.

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’ after she correctly predicted the 2008 financial crash, said house prices in some states will fall this year.

So-called pandemic ‘boomtown’ Boise, Idaho, saw prices decline 3.8 percent to a total of $123.9 billion in December 2023 – the most of any metro

Analyst Meredith Whitney, who is known as the ‘Oracle of Wall Street’, said house prices in some states will fall this year

This, in turn, will free up inventory and bring costs down for first-time buyers.

Whitney said homes in New York, New Jersey and Ohio will see a fall in prices. By comparison, homes in Texas, Tennessee and Utah will remain strong, she said.

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

Americans are staying in their homes before selling up for twice as long as they did in 2005 – and baby boomers are to blame.

The typical homeowner spends 11.5 years in their house today, up from 6.5 years two decades ago, according to a new report by Redfin.

Researchers said the trend is being driven by older homeowners who are not ‘financially incentivized’ to move. A lack of homes on the market pushes up prices.

It comes after former Oppenheimer analyst Meredith Whitney told DailyMail.com that the house prices will finally start to decline as more seniors start downsizing – thereby freeing up homes.

According to Redfin’s analysis of US Census Bureau data, homeowner tenure peaked at 13.4 years in 2020.

The typical homeowner spends 11.5 years in their house today, up from 6.5 years two decades ago, according to a new report by Redfin

It comes after former Oppenheimer analyst Meredith Whitney, pictured, told DailyMail.com that the house prices will finally start to decline as more seniors start downsizing – thereby freeing up homes

The analysis also found that millennials were more likely to stay in their homes for shorter periods, in part because they change jobs more frequently than older generations.

Two in five baby boomers – those born between 1946 and 1964 – have lived in their home for 20 or more years.

By comparison, less than 7 percent of millennials – born between 1981 and 1996 – have lived in their home for ten years or longer.

The report notes: ‘Most – 54 percent – of baby boomers who own homes own them free and clear with no outstanding mortgage.

‘For that group, the median monthly cost of owning a home – which includes insurance and property taxes among other things – is just over $600.

‘Nearly all boomers who do have a mortgage have a much lower rate than they would if they sold and bought a new home with today’s 7 percent-ish rates.’

But researchers noted that older homeowners ‘hanging onto their homes’ is ‘an obstacle for young first-time buyers trying to break into the market.’

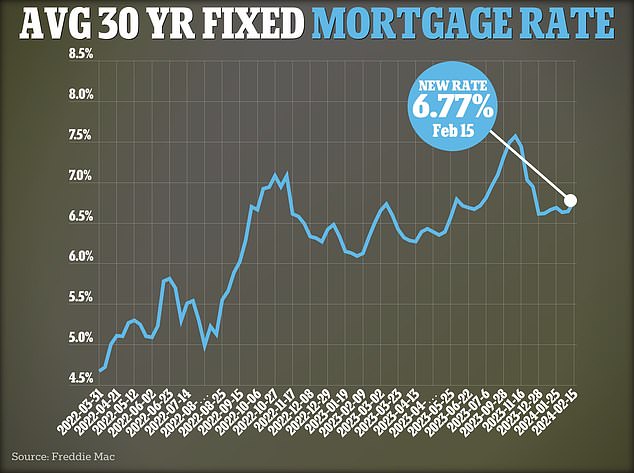

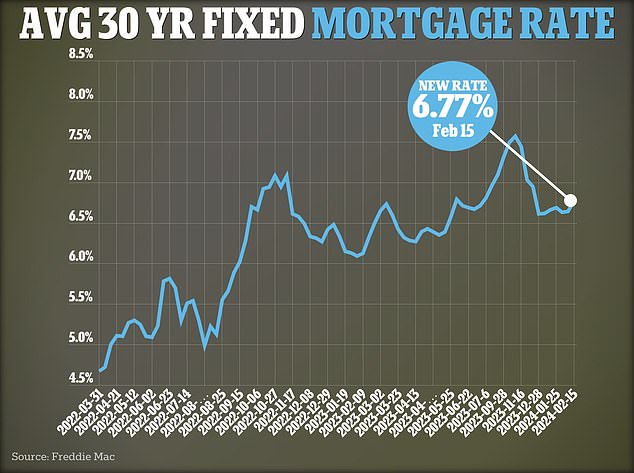

The average rate on a 30-year fixed home loan reached 6.77 percent, up from 6.64 percent last week, according to figures from Government-backed lender Freddie Mac

The findings echo comments made by Whitney, an analyst who was dubbed the ‘Oracle of Wall Street’ after she accurately predicted the 2008 financial crisis.

Her research shows that around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

However she claims a significant upheaval is in-store as more of these older owners start to sell up – freeing inventory and bringing prices down.

Whitney told DailyMail.com: ‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

During the pandemic the median US house price ballooned from $303,465 in March 2020 to $402,045 by December 2023, Redfin figures show.

Many families were embroiled in a so-called ‘race for space’ as they looked for bigger homes and gardens to spend lockdown. A widespread shift to working-from-home also unchained workers from their city center properties.

But house prices have remained elevated ever since – despite mortgage rates soaring in response to the Federal Reserve‘s funds rate reaching a 22-year high.

The average rate on a 30-year mortgage is currently hovering at 6.77 – around double what they were two years ago, figures from Government-backed lender Freddie Mac show.

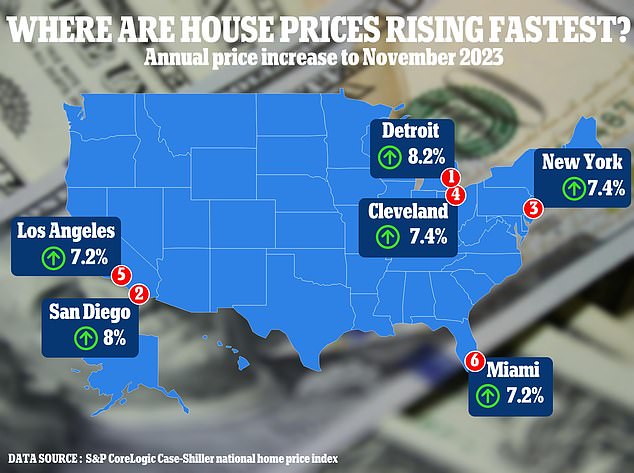

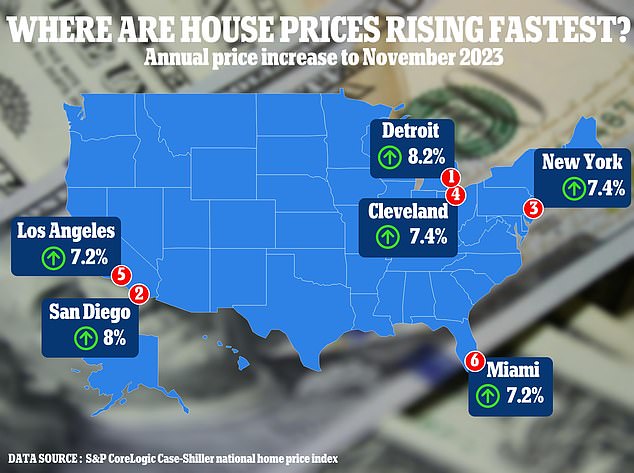

In the year to November 2023, property prices in Detroit increased 8.2 percent, according to latest data from the leading measure of US house prices

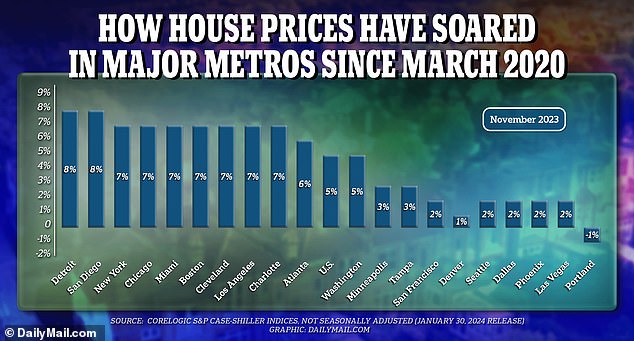

A recent report by CoreLogic shows how property prices have shot up in certain US metros

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

She notes that in the last decade homeowners have built up $21 trillion in equity in their homes – so any price falls is unlikely to seriously harm them.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

Over the last few years, it has become increasingly difficult for Americans to buy property.

Mortgage rates and house prices have skyrocketed, making becoming a homeowner a pipe dream for many.

But Elizabeth and Ethan Finkelstein have a solution: cheap old houses.

That is the name of the couple’s Instagram page, which connects Americans with historic, characterful fixer-uppers – all on sale for under $100,000.

The account boomed during the pandemic, and now has a huge 2.7 million followers, stemming a book and a spin-off show on HGTV with a new series coming in spring.

They started the account in 2016, but Elizabeth and Ethan believe there is an ever greater need for a creative approach to homeownership in today’s unaffordable market.

Elizabeth and Ethan Finkelstein set up their Instagram page Cheap Old Houses in 2016

‘It’s just gotten exponentially harder every single year for people to buy a home, Elizabeth told DailyMail.com.

‘It’s undeniable that millennials and younger people, especially, feel priced out of the housing market and pursuing all of the “American Dream” hallmarks we’ve always been taught to aspire to. Cheap old houses offer another pathway.’

‘Even before the pandemic, Cheap Old Houses took off pretty quickly. Now it just feels like a feeling of desperation among so many people,’ Ethan added.

Housing inventory across the US is at a historic low and mortgage rates closed in on 8 percent last year, pushing up the cost of homes and pricing many Americans out of the market.

Cheap Old Houses, which has 2.7 million followers, connects Americans with historic, characterful fixer-uppers – all on sale for under $100,000

Elizabeth and Ethan, who live in Albany, New York, and have an old house of their own, believe a solution is looking to saving these houses, and with them, America’s built history.

‘One of the biggest hindrances to people buying old houses is the way that they’re often portrayed as money pits. They’re more than that,’ said Elizabeth.

‘New houses are money pits now if they’re built poorly, which many of them are, and in 10 years they will be leaking.’

Their aim is to demystify the process of buying an old house. And since they set up the account, they have had one or two people a month say they have purchased a property featured on their feed. Over the years this has added up to hundreds of people.

‘It made financial sense’: An $86,000 stately home

Jessica, Steven and their two children live in Danascara Place in upstate New York

Jessica Rhodes, 36, and her husband Steven, 37, bought the stately Danascara Place in Fonda, New York, in 2019.

The couple both grew up in the area and knew about the house – which is surrounded by farmland and a creek on one side.

The Federal-style mansion, which was built around 1795, had been abandoned for eight years, suffered foreclosures, and been damaged by fire.

But when it went on the market for just $86,000, it made financial sense to take on the project, Jessica said.

The Federal-style mansion, which was built around 1795, had been abandoned for eight years, suffered foreclosures, and been damaged by fire

The family are now working on restoring the Federal-style mansion room by room

The couple had bought and done small restoration work on old homes before – and recognized the foundations of the property were surprisingly solid.

‘We asked our contractor friend to look around and he said it would cost around the same amount to make the house livable as it would be to buy it,’ Jessica told DailyMail.com.

‘Financially it made sense. It would cost less than the mortgage we were paying on the other house we were living in.’

Jessica, Steven, and their two young sons moved into the house in November 2019 – once the bare bones of a heating system and working bathrooms had been installed.

Their children are now 7 and 9 years old, and the family are slowly working on restoring the house room by room.

Not only are they preserving the history of the place, but they are discovering features which Jessica tracks on her Instagram account.

‘I’d love for our kids to know that they can do anything if they commit to figure it out and working hard. I think that’s a good lesson to learn in life and I would love it if they could learn that through seeing what we do,’ she said.

A $25,000 muraled mansion

The Cook House had been abandoned for decades and was in ‘dire condition’ before Lucas bought and restored it

Lucas Neuffer, 30, had to do some digging to find the owner of the Cook House in Evansville, Indiana.

He had driven past the 10,000 square-foot mansion, which had sat vacant for decades on an acre of land, many times on his commute to the office where he worked as a realtor.

So when he found out that there were plans to tear the house down, he set about trying to find the owner.

‘No one knew where she was and I did every bit of research I could to find her,’ he said. ‘I ended up finding her through the guy who was moving the lawn outside the house. I stopped him one day.’

Lucas and his wife Kindel now live in the 10,000 square-foot house, which has 10 hand-painted murals which Lucas has learnt how to restore

Eventually he persuaded the owner, who had not been to the house in 15 years, to sell it to him for $25,000 – all the savings he had at the time.

It was 2017, and Lucas was 23 years old. In the seven years since, he has completely transformed the house from the ‘dire condition’ he bought it in.

‘Two significant sections of the house were actually missing. You could see right through the house from the yard,’ he said.

Now, he estimates that it could be worth somewhere around $1 million.

Significant parts of the house were missing, said Lucas, including a bay window at the back of the house which was restored

During the years of restoration Lucas has made sure to bring back the forgotten history of the mansion.

‘I reached out to local people as much as I could to learn how to restore parts of it that I didn’t previously know how to do. I’ve learned how to plaster walls, and it’s got 10 hand painted murals which I’ve started restoring.’

He even found an album of photographs of the house from when it was listed for sale in 1981, and has tried to match the interiors as much as he can – including light fixtures, furniture and even stained glass.

‘My wife Kindel always says it’s like walking through a museum,’ he said.

Inspired by the immense project of restoring his first old house, Lucas now owns six historically significant properties in the area.

‘I was struck by the amount of properties in Evansville that are not maintained and are falling down,’ he said. ‘I thought if I can fix up and save the Cook House then I can save anything.’

A modern take on a Midwest farmhouse

James and Jacob bought farmhouse Farrand Hall, in Colon, Michigan, in 2017

‘When we first got the keys and headed to the house, I posted a photo online and the caption was: “either this is the best or the worst decision we’ve ever made”,’ said James Gray.

Now, 7 years later, James jokes that ‘it depends on the day’ which of these decisions he thinks it was.

James and his partner Jacob Hagan bought an elegant 4,000 square-feet 1854 Greek Revival farmhouse, called Farrand Hall, in 2017.

Located in Colon, Michigan, it was nearby to where they were living in Chicago at the time.

They fell in love with the property and its grounds, despite the work that needed to be done to it.

They paid $214,000 for the house – more on the expensive side for a cheap old house – but now estimate it is worth around $1 million today.

‘We spent the first couple of years doing a lot of interior renovations ourselves. We would drive out on Friday and stay up late fixing plaster walls and sanding. Then we’d wake up on Saturday and Sunday and work all day before driving back to Chicago,’ James told DailyMail.com.

Although the project is still ‘ongoing’, James says, it got to a point a few years ago when they felt they could stop worrying about renovations and just enjoy the property.

James and Jacob took a hands on approach to restoring much of the interiors of the home – and now host events at the property

James warns others to carefully consider their financial position before buying an old house which needs a lot of work

For the couple, it is important to maintain the historical integrity of the house – but also make it feel modern and livable. Much of their furniture and interiors are from thrift stores and online auctions.

‘We’re not trying to take it back to 1854,’ said James. ‘This is a modern era and the way that we use the house with guests and now doing events on the property, it needed to be more functional. So we really wanted to balance that old and new.’

Farrand Hall has now become a business, complete with a new dining building, and hosts dining experiences with chefs from all around the US.

Are there any tips they would give to anyone looking to buy an old house? James warns that with a project of this size, people should assess their financial position before entering into it.

‘Getting a mortgage can be very difficult depending on the condition of the house, and often it is just cash offers,’ he said. ‘We were lucky we were in a position where it worked out for us, but make sure you think carefully and research.’

Looking local and asking around for can be really beneficial, said James. ‘We found somebody local who gave us a really great deal and we paid about $3,000 in total to turn one room into a bathroom,’ he said.

The couple recommend asking local contractors and workers for deals. They build this bathroom from scratch for just $3,000

Ethan and Elizabeth are keen to stress, however, that not all cheap old houses are hundred-year old crumbling mansions.

‘What we are interested in fixing up is the everyday average American bungalow. It will have the kitchen which every American had in the 1940s. But those are the ones which are most vulnerable to being destroyed or ripped apart,’ said Ethan.

‘The focus has been micro houses and new buildings, and we are over here advocating for these small towns and small houses that just need a little bit of restoration and some elbow grease and someone to care for them again.’

It may also be more difficult to get a mortgage on more extreme homes that need a lot of work or are shells inside, Elizabeth added.

Namely, the mortgage company just wants to know that there’s heating, and a working kitchen and bathroom, she said.

As a result, some people use non-traditional financing, like a special program in their city, a renovation loan or buying in cash.

‘But there are cheap old houses that you can get a mortgage for, or buy, and move in right away,’ she said.

‘There are the giant mansions and then there are the people who buy a small move-in ready bungalow that might not have the latest kitchen and bathrooms, but it is livable as it is.’

- Meredith Whitney accurately predicted the 2008 financial crisis

- Now she claims US housing market is in the midst of a major shift

- It marks a reversal of the pandemic-inspired housing boom

America’s real estate landscape is in the midst of a major upheaval that will make homes more affordable to first-time buyers, claims a former Oppenheimer analyst.

Meredith Whitney earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis.

Now she claims house prices are on the brink of decline after the pandemic inspired a real estate boom that saw the average property shoot up over $100,000 in value in less than four years.

However, she said the trend will be geo-specific with the likes of New York, New Jersey and Ohio worst-affected. By comparison, homes in Texas, Tennessee and Utah are among the states set to remain strong.

The shift will be driven by a surge in Baby Boomers downsizing into smaller properties – freeing up inventory and bringing costs down for first-time buyers, Whitney said.

Meredith Whitney, pictured, earnt the nickname the ‘Oracle of Wall Street’ after accurately predicting the 2008 financial crisis

In the year to November 2023, property prices in Detroit increased 8.2 percent, according to latest data from the leading measure of US house prices

A recent report by CoreLogic shows how property prices have shot up in certain US metros

She told DailyMail.com: ‘Around 90 percent of housing stock is owned by over 40s while 74 percent is by those over 50.

‘It makes logical sense that lots of these owners will start to downsize in the next decade. That’s almost 35 million homes – it’s a huge number to go through the system.

‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later.’

During the pandemic the median US house price ballooned from $303,465 in March 2020 to $402,045 by December 2023, Redfin figures show.

Many families were embroiled in a so-called ‘race for space’ as they looked for bigger homes and gardens to spend lockdown. A widespread shift to working-from-home also unchained workers from their city center properties.

But house prices have remained elevated ever since – despite mortgage rates soaring in response to the Federal Reserve’s funds rate reaching a 22-year high.

The average rate on a 30-year mortgage is currently hovering at 6.77 – around double what they were two years ago, figures from Government-backed lender Freddie Mac show.

In a normal market this would be enough to dampen demand for homes and thus quash prices. However, several experts have noted that a widespread property shortage in the US has kept home values artificially high.

Whitney told DailyMail.com: ‘My advice to homeowners is: if you want to sell, you’re better off doing it sooner than later’

The average rate on a 30-year fixed home loan reached 6.77 percent, up from 6.64 percent last week, according to figures from Government-backed lender Freddie Mac

Data from Redfin shows that the typical US homeowner now spends twice as long in their properties as they did in 2005.

Today an owner can expect to spend 11.9 years in the same property, compared to 6.5 years two decades ago.

Whitney insists that there will be no house price ‘crash’ but rather an overdue correction.

She notes that in the last decade homeowners have built up $21 trillion in equity in their homes – so any price falls is unlikely to seriously harm them.

And some markets will fare much better than others.

She said: ‘Every 60 years we see a similar kind of seismic shift in the US economy from an economic standpoint.

‘Today we’re seeing businesses shift into those tax-friendly states across the Sunbelt and in Texas, Tennessee and North Carolina. These are the housing markets where growth will persist.

‘But New York, New Jersey, Ohio and Illinois will see an outmigration of population meaning there will be no growth in their housing markets.’