Alberta is changing the system for how publicly funded agencies — including school districts, universities and health-care providers — can own and sell property.

If passed, Bill 13, the Real Property Governance Act, would require provincial agencies, boards and commissions to give the province first right of refusal when they’re selling surplus land and buildings.

The proposed change affects Alberta’s post-secondary institutions, school jurisdictions and charter schools, Alberta Health Services and numerous government organizations including the Alberta Social Housing Corporation, among others.

Infrastructure Minister Pete Guthrie said Thursday the province will also no longer transfer ownership of new buildings, like schools and hospitals, to the organization running them. Instead, the plan is for the government to retain ownership and make long-term lease arrangements with operators.

However, institutions like school boards would continue to be responsible for maintenance.

After the bill was tabled Thursday, Public School Boards’ Association of Alberta president Dennis MacNeil said school boards have many questions about what it means for them.

Public agencies still get to make decisions about when land or buildings are no longer needed, although that process requires additional government approval when it comes to schools.

MacNeil said he has concerns about school boards’ autonomy to decide what happens to a school after it closes.

“If it’s in the hands of the government as opposed to the hands of the board, then it would be easier to turn it over to another entity that may be in competition with the public school board,” he said.

Legislation stems from MacKinnon panel recommendation

The government estimates that public agencies, boards and commissions hold $83 billion in assets, while the infrastructure ministry owns just $12 billion.

“That kind of gives you an idea of … the transferring away of assets that we do not hold as having availability to and access to as the government of Alberta,” Guthrie said.

The policy is a call back to the 2019 blue ribbon panel led by former Saskatchewan finance minister Janice MacKinnon that made recommendations for sweeping changes to Alberta government finances.

One of the MacKinnon panel recommendations was to “redefine” government land assets to include the broader public sector. The panel suggested that setting policy to deal with surplus land and buildings could offset other capital costs or provide more revenue for the province.

Guthrie said the province’s goal is to make it easier to understand the full inventory of government-owned property and more readily convert available real estate to “priority” uses — for example, affordable housing or addictions recovery centres.

Bill Werry is executive director of the Alberta Post-Secondary Network, a collective of 26 presidents of the province’s colleges and universities.

He said post-secondary institutions will be looking to work with the government on the regulations around provincial ownership and lease arrangements for public assets.

“Not all of our institutions are the same size and scope, nor do they all have the same history or land and assets,” he said.

“The majority of our members are part of the government’s consolidated financial reporting so they’ve already got obligations to the province relative to land and buildings as it stands.”

According to Guthrie, when it comes to post-secondary institutions, anything held within their land trusts would not be included in the new system.

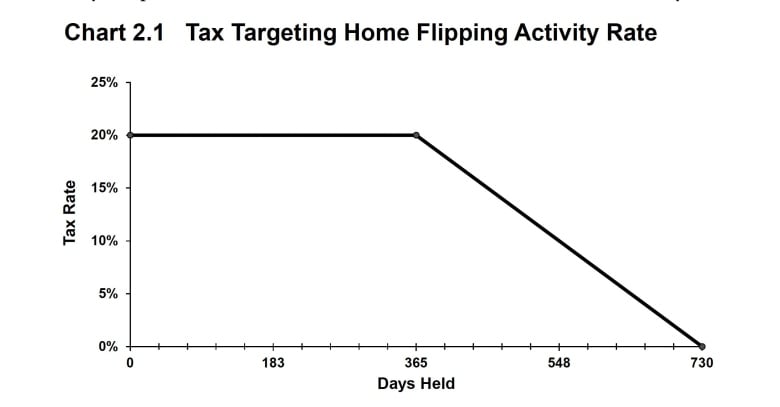

The B.C. government has announced plans to introduce a tax of up to 20 per cent on profits made when properties are sold within two years of their purchase.

The 20 per cent rate will be in place for a year after purchase and will slide to zero between 366 and 730 days after the acquisition.

B.C. Finance Minister Katrine Conroy announced the tax as one of the province’s latest tools to try to curb speculation over housing in a province where many struggle to afford appropriate shelter.

“Prices went up as governments stepped back and speculators moved in,” said Conroy during her speech presenting her latest budget in the legislature.

“That’s why we’re bringing in a home-flipping tax as our latest measure to crack down on bad actors.”

The tax is one of 20 pieces of legislation the government plans to introduce this session, meaning it will need to be passed at some point over the next three months before becoming law.

The plan is to implement it for properties sold on or after Jan. 1, 2025. It will also apply to properties purchased before then.

Conroy’s 2024-25 budget forecasts that the tax, once in place, would result in an additional $44 million in revenue in the 2025-26 fiscal year.

That revenue will go directly to building affordable housing throughout the province, she said.

Sellers would be taxed around 10 per cent after owning a home for a year and a half, with the tax lifted after ownership for two years.

The tax will apply to income from the sale of properties with a housing unit and properties zoned for residential use. It also applies to income made from condo assignments.

It does not apply to land or portions of land used for non-residential purposes, according to the government’s budget documents.

Other exemptions under the tax include life circumstances such as separation, divorce, death, disability or illness, relocation for work, involuntary job loss, change in household membership, personal safety or insolvency.

“The purpose of this tax is to support housing supply, not impede it,” reads the government’s budget documents.

“Exemptions will be provided for those who add to the housing supply or engage in construction and real estate development.”

The tax is to be paid in addition to any federal or other provincial income taxes incurred from the sale of property.

Alex Hemingway, a senior economist with the Canadian Centre for Policy Alternatives, said although the tax is another tool to try and address speculation, he’s not sure how successful it will be.

“I think a flipping tax can take a little bit of air out of the tires in terms of speculation, but it’s not really getting at the root of the housing crisis, which is a shortage of housing overall and a shortage of non-market housing in particular.”

He also said the tax could inadvertently drive down home sales and transactions, siphoning tax revenue away from property transfers.

First-time homebuyer credit

The budget also introduced expanded property transfer tax exemptions, increasing the First Time Homebuyers Program threshold up to $500,000 on the purchase of a home worth up to $835,000.

The province said the move would result in savings of up to $8,000 per purchase and would double the number of buyers that will benefit to approximately 14,500.

The province will also waive the property transfer tax for eligible purpose-built rental buildings that have four or more units until 2030.

A lavish Las Vegas property owned by alleged Ponzi schemer Greg Martel will be sold for $5.1 million US this week after a U.S. court authorized the deal and agreements settling opposing claims on the home.

But once the dust settles on the sale of the seven-bedroom, eight-bathroom, 9,221-square-foot house, it’s unlikely any of the money recovered will reach the many hundreds of people who lost money investing with Martel.

For one, the property has an outstanding mortgage of about $4 million US, according to receiver and trustee PricewaterhouseCoopers (PwC).

In addition, PwC needs to pay back an investor who funded its legal efforts in the United States to the tune of $400,000 Cdn. PwC also says it needs to pay itself after racking up a bill of over $1 million Cdn investigating Martel, according to documents posted on its website.

Martel is the disgraced Victoria, B.C., mortgage broker at the centre of an alleged financial fraud run through his company, Shop Your Own Mortgage (SYOM), also known as My Mortgage Auction Corp.

According to the latest estimate, he owes 1,300 investors $312 million Cdn, in what an expert intimate with the details of the case said has all the hallmarks of a Ponzi scheme.

SYOM collapsed last year amid a flurry of lawsuits filed by investors. The claims were consolidated by the court under a receivership order in May of 2023 and PwC was appointed receiver with the duty to recover money and assets of Martel and his company to pay back jilted investors.

The Las Vegas property is one such asset — and a contentious one at that — requiring many months of legal machinations on both sides of the border.

In order to seize and sell the Las Vegas property, an agreement had to be reached between PwC and a group of creditors led by American Daniel Castellini, who lost $2 million investing with Martel.

Tracked down in Thailand

A sworn declaration submitted in U.S. court by PwC senior vice-president Neil Bunker detailed how in September of last year, a private investigator hired by Castellini tracked Martel down in Thailand where he was hiding out.

The investigator arranged for Thai authorities to detain Martel on an expired tourist visa, before cutting a deal that saw Martel transfer title of the Las Vegas property to Castellini, along with two Teslas and a “substantial” amount of cash.

According to Bunker, the deed for the Las Vegas property was secured through audio-visual communication on Aug. 29, 2023. Martel was released from Thai custody the next day and ordered to leave the country.

After learning that Martel had transferred the Las Vegas property to Castellini, PwC successfully argued in U.S. court that the powers previously granted in Canadian court gave PwC primary authority to recover and sell the home.

PwC then struck a deal with Castellini that says once PwC completes the sale of the Las Vegas property, Castellini will be paid $28,000 from the proceeds. The reimbursement is for “certain expenses [Castellini] represents were incurred investigating Martel and his business dealing,” according to court documents.

Court documents also say Castellini has agreed to co-operate with PwC by sharing the name of the investigator who went to Thailand, as well as all reports and information the investigator provided.

After leaving Thailand, Martel went to Dubai, according to PwC. His whereabouts are unknown.

The Las Vegas property is being sold to Kirk and Janette Mendez, who had also filed a claim on the home.

The couple signed a lease agreement with Martel in February of last year, about the time SYOM was blowing up. They agreed to pay $27,500 per month, with an option to buy the home outright for $5.1 million in February of 2024.

The Mendezes paid Martel for the year upfront but court documents say it appears he absconded with all the money.

CBC has reached out to Castellini and the Mendezes for comment.

According to PwC, two other properties owned by Martel were sold late last year as part of the asset recovery effort.

A heavily mortgaged house in Victoria sold for $2.47 million in December, resulting in $109,606 in net equity for the creditor pot. And an Ontario property Martel co-owned with a former spouse sold for $310,000, resulting in $82,698 in net equity recovered.

Last September, Martel was found guilty of contempt of court and warrants for his arrest have been issued in Canada and the U.S.

Largest Ponzi fraud in Canadian history?

Martel and SYOM were supposedly in the business of pooling investor money to provide short-term bridge loans to real estate developers, but so far investigators have found no evidence that any bridge loans were ever extended.

Martel attracted investors by promising sky-high rates of return, sometimes as high as 100 per cent on an annualized basis.

Bunker said previously that the absence of company records point to the concept that SYOM was a Ponzi scheme orchestrated by Martel.

If true, it would put him in the running for perpetrating Canada’s largest Ponzi fraud ever.

In 2017, two Alberta men were found guilty of fraud and theft after bilking investors out of a combined total of between $100 million and $400 million. At the time the RCMP characterized the crime as the largest Ponzi scheme in Canadian history.

A Ponzi scheme is where people hand over money believing it will be used in legitimate investments, often with the promise of large returns. Behind the scenes, the money actually goes toward paying earlier investors who have also been promised profits.