Takeaways:

- Prospective homebuyers in Kansas City face stiff competition in the housing market. Home sales are down because supply is tight.

- Existing homeowners buoyed by historically low mortgage rates are reluctant to sell.

- The Kansas City metro is seeing a surge of new home construction. But construction is struggling to keep up with demand due to high building costs.

If you’re looking to buy a home in Kansas City in today’s market, brace for scarcity and tough competition.

Real estate experts say that people who already own their homes, locked in with historically low mortgage rates, appear reluctant to sell and take on higher interest rates that would come with the purchase of a house in today’s mortgage market.

Seattle-based real estate brokerage Redfin found that 433 homes were sold in the Kansas City limits in February, a 13% drop from the same period last year.

Meanwhile, home construction is surging. The Heartland Multiple Listing Service shows that 638 residential building permits were issued across the Kansas City area in the first two months of 2024, nearly double the start of last year.

But homebuilders say rising labor and materials cost make it hard to keep up with demand due to heightened building costs, ultimately pushing affordability out of reach for many first-time homebuyers.

“New housing supply is increasingly difficult to deliver,” said Will Ruder, executive vice president of the Home Builders Association of Greater Kansas City.”

What’s contributing to Kansas City’s housing shortage?

In February, Redfin reported, the median sale price of a home in Kansas City reached $250,000, marking an 11% increase from last year.

Data show, predictably, that a shortage of existing houses (as opposed to newly built homes) on the market is driving up prices. According to U.S. Bank, 2023 saw the slowest year for existing home sales nationwide since 1995.

The trend of large corporate investors purchasing swaths of single-family residences to convert into rentals intensifies competition among buyers. Housing experts say that the reluctance of homeowners to sell tightens the market more and ramps prices even higher.

The economic uncertainty brought on by the pandemic caused the Federal Reserve to lower its federal funds rate to stimulate borrowing and lending. That led to record-low interest rates of 2% and 3% for homebuyers or refinancers, Ruder with the Home Builders Association said.

But by 2022, rates shot up to about 7.1%, their highest level in 20 years. Now, interest rates hover around 6%. A Goldman Sachs report found that nearly three in four existing homes have mortgages at or below 4%. Reluctance to sell and take on higher mortgages is keeping homeowners in place. It’s called the “lock-in effect.”

“People are scared to sell their houses because they don’t have anywhere to go,” said Patty Farr, the owner of real estate brokerage RE/MAX House of Dreams. “They’re sitting in a house at 2.5% interest rates and if they buy a new house it’s gonna cost them anywhere from 6% to 8%.”

She doesn’t foresee rates going down drastically soon, so she tells her young homebuyers to purchase a house and refinance later.

But homeowners need to be willing to take on a larger financial burden — and to gamble that rates will fall quickly enough to align with their budgets.

Homebuyers and sellers are stuck

Maret Cissner owns two units within a four-plex cooperative and lives in one. She purchased her property in 2016 and she has spent the past year in search of a bigger space to be able to work from home.

But she’s a pianist and visual artist. And getting a loan is tough because banks don’t look at freelance income the same as a salary.

“They won’t look at any W2 income that hasn’t been at least two years,” she said.

Cissner makes about $50,000 and her mortgage is $400 a month with a 4.5% interest rate. But the artist wouldn’t mind paying more for a better quality of life.

“I’m less interested in building my wealth and more interested in our living situation,” she said.

February saw an uptick in existing home sales, data from the Heartland Multiple Listing Service found. But Ruder said that the winter months are typically slow. The selling season happens in the spring because families prefer to move between school years. Still, the early part of the year at least hints at a shift.

“As more people get comfortable with the fact that these interest rates are probably not gonna go back down to those historic lows,” he said, “then we’ll see more home-buying.”

Is new home construction the answer to Kansas City’s housing shortage?

Newly constructed homes are almost always more expensive than resale homes. And builders say they are more expensive to produce than they have been in the past.

Some empty lots in the Kansas City market run north of $100,000, Ruder said.

“And so if you’re in $100,000 just for the dirt, it’s increasingly difficult, if not impossible … to build something on there and to hit a price point under $350,000,” he said.

Farr with RE/MAX said the homes it sells typically cost $450,000.

Houses sold by Aspen Homes begin at $500,000, said Tony Libra, owner of the residential construction company.

Libra said rising labor and material costs keep pushing prices up.

“Concrete is really going up right now,” he said. “Lumber is going to go up this summer, too.”

Builders say navigating construction rules that vary from one city to the next make it hard to meet demand. Missouri is one of a handful of states without a statewide building code.

Ruder said Kansas City operates on a separate adoption cycle for residential building codes compared to surrounding suburbs.

He cited the 2021 International Energy Conservation Code for home building as an example.

The Kansas City Council approved that code in 2022, raising efficiency standards for new construction. Those IECC rules took effect in July 2023. But surrounding cities are on a 2018 energy code and are set to adopt a new one in 2024, Ruder said.

By September 2023, Kansas City saw a dramatic dip in building permits. Excluding Kansas City, the metro saw a 117% rise in single-family construction permits in January and February compared to the same time last year, MLS data show. Kansas City saw a 22% decrease in that same period.

Ruder says a dip in builds and permitting is expected after building codes change, but that typically resolves within six months. But in over a year, Kansas City has yet to recover.

Builders also say that the new code increases construction costs. Before, a housing plan could be duplicated so long as the original model received a permit. But the IECC’s focus on site-specific energy efficiency means a plan would need adjustments based on a lot’s orientation.

“It’s very labor intensive to satisfy all of those requirements and build at the volume that the market is calling for,” Ruder said.

Researchers with the U.S. Department of Energy have found the 2021 IECC codes to be cost-effective for families and state governments. A 2021 report states that it is significantly more expensive to achieve higher efficiency levels through later modifications once a building is constructed.

Builders sing a different tune.

They say depending on how far above code a construction company is already building, meeting a new metric can come with a wide range of construction costs. The Home Builders Association of Greater Kansas City found that it could cost anywhere between $8,000 and $30,000 to build exactly to IECC standards.

The code adds $35,000 to the price of a property at Aspen Homes, Libra said.

Alexander W. Richter and Xiaoqing Zhou

The benchmark 30-year fixed-rate mortgage increased from around 3 percent in December 2021 to nearly 7 percent two years later, a result of the Fed’s rapid monetary tightening.

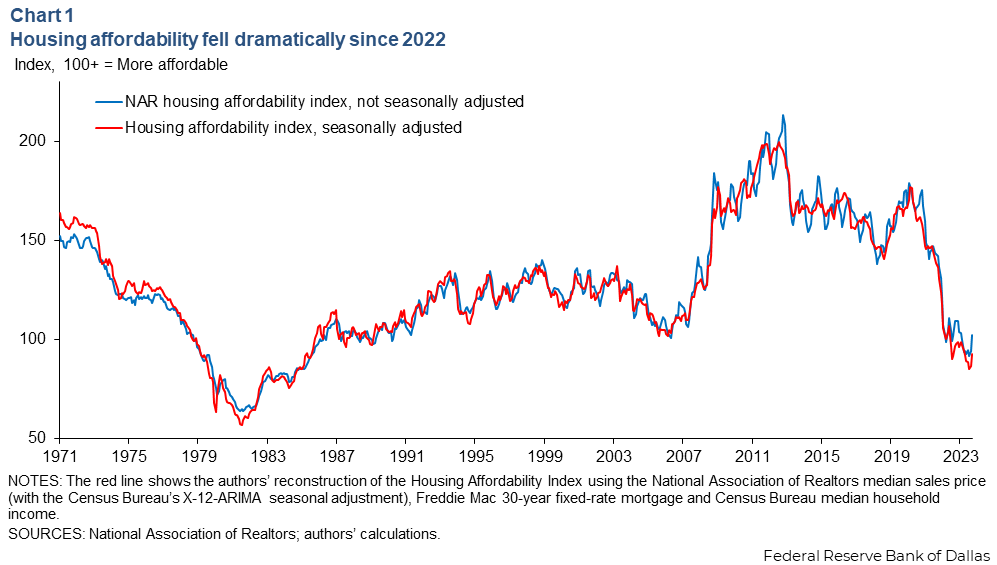

As homebuyers faced sharply rising mortgage payments, questions followed about housing affordability. According to the National Association of Realtors, housing affordability declined almost 30 percent since December 2021, close to levels last seen in the late 1980s (Chart 1).

The direct impact of higher mortgage rates on housing affordability has received much attention. We emphasize that housing affordability not only depends on mortgage rates but also on house prices, which have competing effects. For example, when interest rates increase, house prices tend to decline. We present decompositions of housing affordability, showing the relative importance of the two competing effects matters, and lower interest rates do not necessarily improve housing affordability.

Most homeowners largely unaffected

Before considering the changes in housing affordability, it is important to note that the fraction of homebuyers is small relative to the population of homeowners. In Black Knight McDash mortgage-servicing data, for example, the annual home-purchasing rate is between 3 percent and 10 percent.

Also, most homeowners locked in ultra-low mortgage rates before rates increased. As of September 2023, the rate paid by the average homeowner was only 3.9 percent, compared with 7 precent on new mortgages. This means most homeowners have been generally unaffected by higher mortgage rates.

How to measure affordability

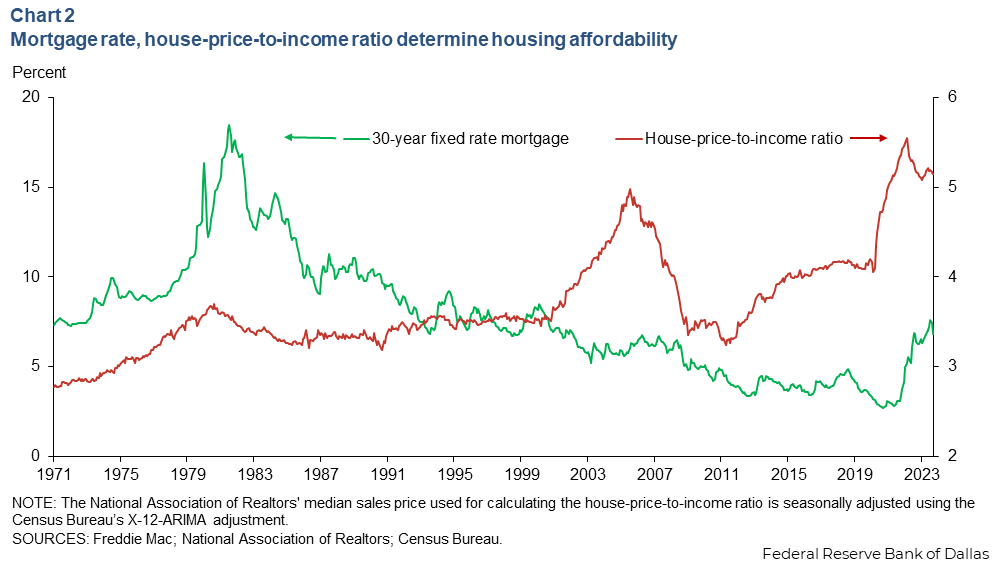

A common measure of homebuyer affordability is the Realtors’ Housing Affordability Index (HAI). The index measures whether a typical (median income) family would qualify for a mortgage on a typical (median price) home. Qualifying income is defined as the amount equivalent to 48 monthly payments on a 30-year fixed-rate mortgage with a 20 percent downpayment. More formally, the index can be written as

where f(r) depends only on the mortgage rate, r. When the mortgage rate increases, f(r) falls. Thus, the index is determined by two variables: the house-price-to-income ratio and the mortgage rate. A higher value of either variable reduces housing affordability. Chart 2 shows recent low affordability is driven by both variables.

Quantifying the drivers of affordability

As a first attempt to quantify the drivers of housing affordability, Chart 3 plots two counterfactual HAI paths. One fixes the house-price-to-income ratio at its average to isolate the interest rate channel, and one fixes the 30-year fixed-rate mortgage at its average to isolate the house price channel.

Before 2000, the house-price-to-income ratio was relatively low, supporting housing affordability. After 2000—except for the brief period of the housing bust from 2008 to 2012—the high price-to-income ratio lowered housing affordability. In the postpandemic period, there was such a large increase in house prices that housing affordability would have declined even if mortgage rates stayed at their average.

The drawback with these counterfactuals is that they assume house prices and interest rates move independently. For example, one could conclude that, had the Fed not raised the federal funds rate in early 2022, housing affordability would not have declined further, as house prices largely stabilized after mid-2022. This view ignores the effect of rate changes on house prices.

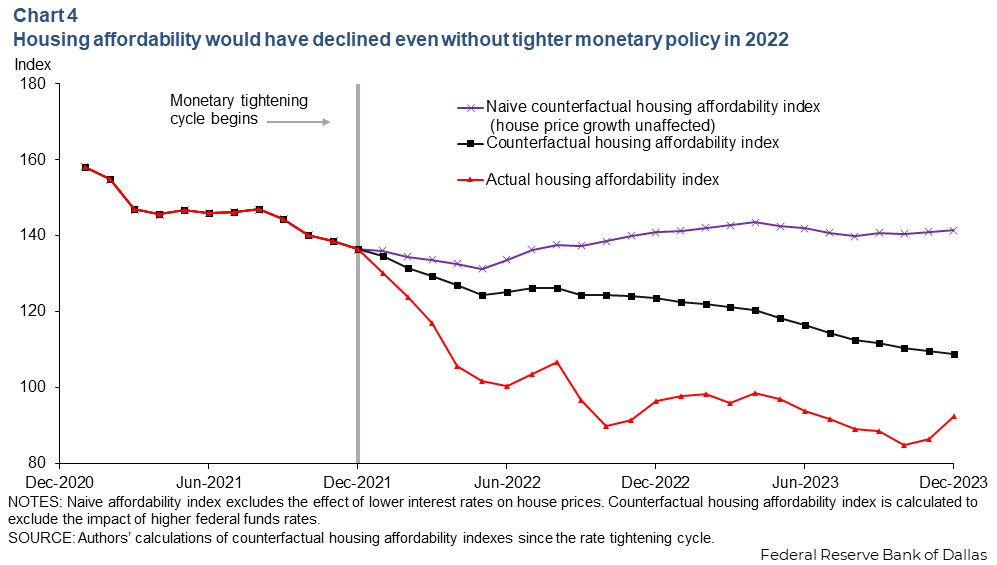

Recent estimates suggest a 1-percentage-point increase in the short-term interest rate lowers house prices by 7.5 percent over two years. We use this estimate to construct proper counterfactuals, focusing on HAI in the recent monetary tightening cycle. Specifically, we ask how HAI would have evolved if monetary policy did not tighten and the 30-year fixed-rate mortgage stayed at its December 2021 level.

In this counterfactual, house prices would have risen faster, lowering housing affordability. To determine the magnitude of this effect, we estimate the size of the monetary tightening shocks and calculate a counterfactual path of house prices without these shocks.

The size of the shock is defined as the difference between the actual federal funds rate and the median projection in the Fed’s Summary of Economic Projections the year before. For example, in December 2021, the federal funds rate was projected to be 0.9 percent a year later, whereas the actual rate was 4.1 percent. This difference implies a 3.2 percentage point shock in 2022. In 2023, the shock was 0.23 percentage points. Given a cumulative 3.43 percentage point shock over two years, the monthly growth rate of house prices would have been 1.1 percentage points higher (=3.43×7.5/24) than in the actual data.

Chart 4 shows the actual HAI, the counterfactual HAI using this estimate and the naive counterfactual HAI without considering the effect of the lower rate on house prices. The rate increase worsens housing affordability. However, in the absence of rate hikes, affordability would have still declined after 2022.

Larger-than-expected rate cuts don’t always improve housing affordability

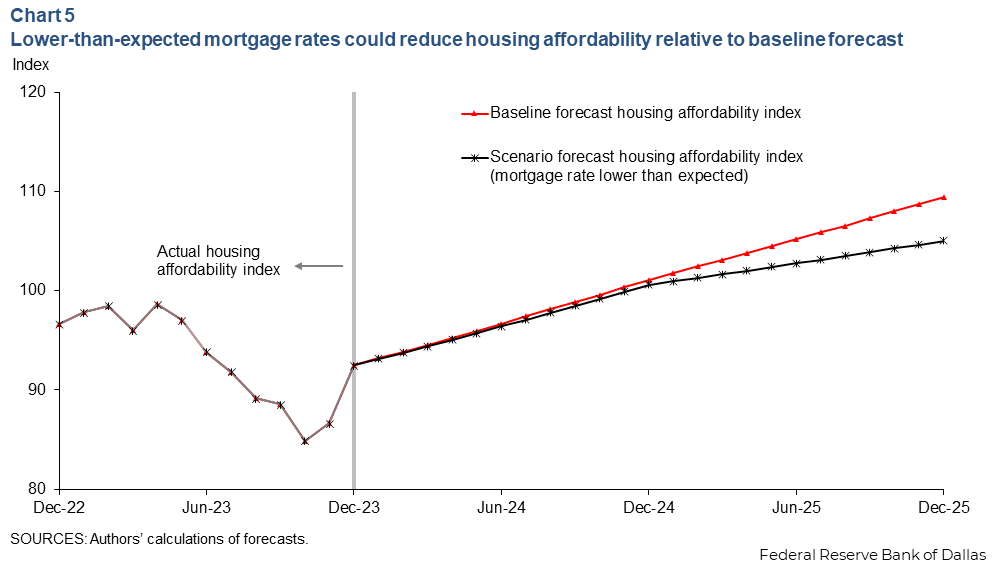

Given the current low affordability of housing, it makes sense to ask how the situation might change if interest rates fell and were lower than expected. To answer this question, we first need to develop a baseline HAI forecast.

We assume household income continues to grow at the 2023 rate of 4.2 percent and home prices rise 2.8 percent based on the 2024 forecast from CoreLogic, a real estate analytics firm. The 30-year fixed-rate mortgage will end 2024 at 6.1 percent and 2025 at 5.5 percent, based on Mortgage Bankers Association forecasts. Under these assumptions, there is a gradual increase in housing affordability.

For the counterfactual experiment, we assume income grows at the same rate as the baseline, but the federal funds rate path is 1 percentage point lower than expected. This implies the monthly growth rate of house prices would be 0.3 percentage points higher than the baseline (=7.5/24).

Finally, we assume the lower policy rate path translates to a 30-basis-point decline in the path of the 30-year fixed-rate mortgage, consistent with estimates in the academic literature. This implies a 5.8 percent mortgage rate in December 2024 and 5.2 percent in December 2025. Chart 5 shows the gains in housing affordability from the lower-than-expected policy rate path are offset by the reduction in affordability from higher home prices. In fact, the price effect is strong enough that housing affordability is lower than the baseline forecast.

Mortgage rates influence house prices

Changes in monetary policy directly affect mortgage rates, but there is also an indirect effect on house prices. When monetary policy is easier, mortgage rates tend to fall, while house prices tend to rise due to higher demand. These opposing channels imply that the net effect on affordability is ambiguous and potentially the opposite of what intuition based solely on mortgage rates would suggest.

About the authors

Alexander W. Richter

is a senior economic policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

Xiaoqing Zhou

is an economic policy advisor in the Research Department at the Federal Reserve Bank of Dallas.

The views expressed are those of the authors and should not be attributed to the Federal Reserve Bank of Dallas or the Federal Reserve System.

Homeowners are leaving the high prices of the capital in favour of Britain’s Industrial Revolution cities, MailOnline can reveal.

Thousands of people are ditching London and instead looking to buy homes in cities such as Leicester, Glasgow, Sheffield and Bradford.

There were more than 75,000 searches for ‘homes for sale’ in Glasgow in the last 90 days – nearly double the interest in London, data from Purplebricks showed.

Second on the list was Sheffield with 61,000 searches, followed by 58,000 searches for properties in Bradford, once a hotbed of Britain’s textile trade.

Some 52,000 searches were made for the industrial giant of Leicester, and 43,000 for the Welsh port city of Swansea, less than 10 miles from towering steelworks in Port Talbot.

Manchester, Liverpool, London, Stoke on Trent and Birmingham all feature at the top of the table, receiving more than 30,000 searches since mid-December.

Housing expert David Hall told MailOnline: ‘Anywhere that has a developed infrastructure for transport is a model for somebody to look for cheaper prices.

‘In London [there are] eye-watering prices for properties.

‘You will see loads more of [people leaving London] in major towns and cities in the UK coming soon.

‘Don’t forget the interest rate rises for mortgages. Anyone who was looking to get a mortgage who thought for one minute they were going to get one for primetime in London has realised that’s not going to happen.

‘When you’re at 4.5 per cent, you have to move outside the city to be looking at something that’s affordable.’

Leaseholds expert Linz Darlington added: ‘There is a real appetite to move out of the capital.

‘While people love the hubbub of the city, London is incredibly expensive, particularly to buy a property in.

‘During the pandemic, people realised that London wasn’t the be-all and end-all.’

Here, MailOnline takes a look at some of the most popular places outside of London where house hunters are looking to buy properties…

Glasgow

The Industrial Revolution poured wealth and prosperity into Glasgow, turning a relatively small town into a giant of the British Empire.

Now over £5billion of new investment is set to transform the Clyde waterfront over the next 25 years.

This four-bed semi-detached home on Leithland Road in Pollok is available to buy for £185,000.

Homeowners in Glasgow have enjoyed a 4.3 per cent rise in property values, according to the latest House Price index – one per cent more than the 3.3 per cent increase seen across Scotland in the 12 months up to December.

Some see Glasgow properties as a great investment with average homes priced at £183,494, some £6,500 lower than the Scottish average and more than £150,000 cheaper than the average home in Edinburgh.

Sheffield

This three-bed home located in a desired cul-de-sac in Sheffield is on the market for £220,000.

While steel was once the main industry in Sheffield, South Yorkshire, the city is now seen as a superb employer in the tech and creative sectors.

Sheffield house prices bucked the national trend by increasing 4.9 per cent in the last 12 months, making the average property worth around £220,000.

It means they are around £82,000 cheaper than the average in England.

Sheffield’s central location in the UK means it is ideally located for travel and accessibility and has national and international connections.

Bradford

Nestled in a quaint neighbourhood, this charming two-bed terrace £180,000 house presents an enticing opportunity for families seeking a place to call home.

Bradford was once known as the wool capital of the world.

Worth £11.6billion, Bradford’s economy is now powered by advanced engineering, chemicals, automotive components and food manufacture alongside financial services and digital technologies.

The West Yorkshire city also bucked the national downward trend, with homeowners enjoying a 0.7 per cent annual increase, with the average property costing £173,337 – nearly half the national average.

Leicester

This £230,000 two-bedroom semi-detached house in Leicester, boasts three reception rooms.

Leicester’s industrial success took place in the 20th century, led by the success of its hosiery and footwear industries.

While manufacturing has been in decline across the UK in recent decades there are many modern industries thriving in and around Leicester, beyond its traditional textile trade.

The city boasts industries ranging from professional and financial services, advanced manufacturing and engineering to life sciences, space and digital technology.

Leicester has been ranked as the top city in the East Midlands to live and work as part of an influential nationwide industry report.

The average house price for the area is still below the national average at £232,324, but more expensive than nearby Birmingham at £228,877 and Nottingham at £192,298.

Swansea

This modern semi-detached two-bedroom house, located in the sought-after area of Sketty, is on the market for £190,000.

Swansea has a proud industrial heritage centred on coal, manufacturing and heavy industry.

Today, a large proportion of the economic growth is provided by public administration, education and health.

With the average price of a house at £196,000, Swansea is an affordable option for those looking to get on the property ladder, and nearly £20,000 cheaper than the Welsh average of £214,000.

Homeowners in the city saw a 0.8 per cent rise in the value of their properties in the last 12 months, despite a downturn of 2.5 per cent across Wales.

However, the port city is braced for a huge financial and social fallout after Tata confirmed plans to close two blast furnaces at nearby Port Talbot in January this year. The move is expected to cost of 2,800 jobs.

- Average UK property prices increased £1,410 from December to January

- London properties enjoyed biggest rise in with 2.5% or £12,950 added to value

- Month-on-month increase comes despite annual plunge in prices across the UK

A new online calculator can reveal how much your property may could have gained or lost in value over the last year.

This comes as homeowners across Britain can finally see some signs of an upturn in the property market today, analysis by online estate agent Purplebricks reveals.

The biggest winners have been property owners in South Hams, Devon, where prices rose by around £47,500 (11%) in one year.The biggest losers were in Westminster where prices fell by nearly £196,000 (21%).

Average UK house prices increased 0.5% or £1,410 from December to January, making the average property now valued at £282,000, according to today’s House Price Index (HPI).

The figures, released today by the Office for National Statistics, will come as welcome news for millions of homeowners. An interactive tool has been updated to include the latest House Price Index data, released by the Office for National Statistics today.

To use the Purplebricks calculator, simply search for YOUR local area below and find out how house prices have changed over the last 12 months:

The new figures follow a miniscule rise of just £300 in the value of average UK properties from November to December last year.

London homes saw the biggest month-on-month rise, with around £2.5% or £12,950 added to the average property in the capital, now valued at £518,000.

However, the annual price change paints a very different picture, with another 3.9% drop in values in the capital, felt most sharply in the City of Westminster.

Homes in the exclusive City of Westminster lost a staggering £195,000 over the last year, with properties in the City of London shedding just over £160,000 of their value.

Kensington and Chelsea properties lost around £147,000, Hammersmith and Fulham lost nearly £80,000 and Camden properties just over £50,000 in the 12 months to January.

Average annual property prices in both England and Wales fell, with a typical house in England falling 1.5% in value to £299,000, and dropping 0.8% to £213,000 in Wales.

The North West of England was the best performing UK region, where house prices rose one per cent in the 12 months to January.

Properties in South Hams, Devon, saw the biggest increase in value, with homes rising just over £47,000 or 11% over 12 months.

Winchester homes increased more than £36,000, with East Cambridgeshire properties enjoying a boost of more than £32,000.

(AP) – A powerful real estate trade association has agreed to pay $418 million and change its rules to settle lawsuits claiming homeowners have been unfairly forced to pay artificially inflated agent commissions when they sold their home.

The National Association of Realtors said Friday that its agents who list a home for sale on a Multiple Listing Service, or MLS, will no longer be allowed to use the service to offer to pay a commission to agents that represent potential homebuyers. The rule change leaves it open for individual home sellers to negotiate such offers with a buyer’s agent outside of the MLS platforms, however.

NAR also agreed to create a rule that would require MLS agents or other participants working with a homebuyer to enter into written agreement with them. The move is meant to ensure that homebuyers know going in what their agent’s service will charge them for their services.

The rule changes, which are set to go into effect in mid-July, represent a major change in the way real estate agents operate.

The NAR faced multiple lawsuits over the way agent commissions are set. In October, a federal jury in Missouri found that the NAR and several large real estate brokerages conspired to require that home sellers pay homebuyers’ agent commission in violation of federal antitrust law.

The jury ordered the defendants to pay almost $1.8 billion in damages — and potentially more than $5 billion if the court ended up awarding the plaintiffs treble damages.

The NAR said the settlement covers over one million of its members, its affiliated Multiple Listing Services and all brokerages with a NAR member as a principal that had a residential transaction volume in 2022 of $2 billion or less.

The settlement, which is subject to court approval, does not include real estate agents affiliated with HomeServices of America and its related companies, the NAR said.

Copyright 2024 The Associated Press. All rights reserved.

By Prerana Bhat and Indradip Ghosh

BENGALURU (Reuters) – U.S. home prices will rise steadily over the next few years amid prospects for modest interest rate cuts by the Federal Reserve and as many existing homeowners keep their doors closed to selling, according to property experts polled by Reuters.

As aggressive Fed rate hikes have sharply pushed up the cost of standard 30-year mortgages to more than 7%, existing homeowners have held on to rock-bottom rates from the pandemic, some below 3%, limiting the supply of homes for sale.

That, combined with relentless demand for a place to live and a strong economy, cushioned a brief correction in the market. Average house prices soared around 50% during the pandemic and again hit a new record last year.

After rising about 6% last year, defying previous expectations of declines, average home prices are forecast to grow 3.3% this year and around 3.0% in 2025 and 2026, according to the median of 28 analysts in a Feb. 15-March 1 Reuters poll.

Forecasts were based on the S&P CoreLogic Case-Shiller composite index of 20 metropolitan areas.

That outlook was upgraded very slightly from three months ago, modestly outpacing expectations of headline inflation, seen averaging 2.7% and 2.3% this year and next, respectively, according to a separate Reuters survey.

“Despite rapidly climbing mortgage rates in 2023, record low levels of resale inventory have contributed to home prices’ resiliency… We expect to see some small gains in home prices as mortgage rates stabilize and reach a more terminal rate over the next year,” said Crystal Sunbury, senior real estate analyst at RSM, a U.S.-based consulting firm.

The 30-year fixed mortgage rate, which broke above 7.0% recently for the first time since December, was expected to average 6.50% this year and decline only modestly to 5.98% in 2025 and 5.75% in 2026, according to median forecasts in the poll.

“We may see more resale units come into the market, as mortgage rates ease, but resale inventory is not expected to climb substantially, as over 80% of current homeowners are estimated to have mortgages under 5% and the vast majority will not be willing to trade up their mortgage for a higher rate,” Sunbury added.

Average mortgage rate forecasts were broadly upgraded from a November poll and reflect retreating expectations for the number of Fed rate cuts expected later this year, currently due to start in June.

Shelter costs as a category, which is dominated by rental costs rather than home prices, comprise around one-third of the consumer price index. Although the Fed targets the personal consumption expenditure index – which is less driven by housing – higher house prices could delay Fed rate cuts.

On the prediction mortgage rates would decline only slightly, existing home sales, which comprise about 90% of total sales, were seen around current levels of 4 million units this year, much less than over 6 million during the pandemic.

A persistent shortage of previously owned homes pushes buyers into the new home and rental market, adding pressure on already lagging constructions and sales.

Responding to a separate question, 22 strategists were evenly split on whether the ratio of homeowners to renters would increase or decrease.

A further 15 of 23 said the gap between demand for affordable homes and supply of them would stay around the same or widen over the next 2-3 years.

“Overall, the main issue in the housing market is affordability, and mortgage rates are not going to fall enough to make a dent,” said Brad Hunter of consultancy Hunter Housing Economics.

“Newly-formed families used to be ‘entry level’ for the builders. Not anymore. Young families have essentially no hope of buying a new home for their first home. Even on the resale market, they will continue to struggle just to become homeowners at all.”

(For other stories from the Reuters quarterly housing market polls:)

(Reporting by Prerana Bhat and Indradip Ghosh; Polling by Maneesh Kumar; Editing by Ross Finley and Hugh Lawson)

- Homes in London saw average of £53,000 wiped from values in last 12 months

- Nine London boroughs lose value – with Kensington and Chelsea worst hit

A new interactive map shows how London homeowners have seen property values tumble, with an average of £53,000 wiped off the value of their properties in the last 12 months.

Nine London boroughs were hammered by price plunges, with Kensington and Chelsea being the hardest hit area, shedding an eye-watering £154,000 in 12 months, according to House Price Index (HPI) data and analysis by online estate agent Purplebricks.

But it wasn’t all bad news for people living in and around the capital, with properties in the London borough of Richmond upon Thames increasing £22,730 in value, and homeowners in the Surrey district of Mole Valley seeing a rise of £46,089.

Other homeowners just outside the capital have little to celebrate too, with homes in nine commuter belt areas losing an average of £35,000 in the space of a year.

In total, 18 of the top 20 worst-hit areas were either in the capital itself or a borough or district surrounding it – the average loss among them being £53,000.

The stark figures from the Office for National Statistics reveal average UK house prices fell by £4,000 or 1.4% in the 12 months to December, making a typical house worth £285,000.

Search for YOUR local area in this widget from Purplebricks below, and find out how house prices have changed over the last 12 months.

Click here to resize this module

The fall in prices is a slight improvement on the drop of 2.3% for the 12 months up to November.

Average property prices in both England and Wales fell, with a typical house in England falling 2.1% in value to £302,000, and dropping 2.5% to £214,000 in Wales.

The North East of England saw the biggest price change with an increase of 1.2%, while overall London was hit the hardest with a 4.8% slump.

However, homes in Scotland are now worth an average of £190,000 after enjoying a 3.3% rise in the last year.

And, average properties rose 1.4% to £178,000 in Northern Ireland in the year to Quarter 4, from October to December 20223.

In the capital, the City of London and Westminster lost around £142,000 and £141,000 respectively, while Hammersmith and Fulham properties dropped £70,000, Waltham Forest homes lost £42,000 and Haringey shed £28,000.

Outside London, the leafy stockbroker belt town of Tunbridge Wells took a bruising, with the average home losing around £47,000.

Homes in popular commuter areas like Runnymeade, Surrey Heath, Welwyn Hatfield, Tonbridge and Malling and St Albans lost an average of £37,000 in the last 12 months.

Sam Mitchell, CEO of Purplebricks said: ‘While these figures may appear quite striking, there is plenty of good news for homeowners, and plenty more on the horizon.

‘Homeowners in Scotland and Northern Ireland are continuing to see increases, and evidently the rate of decline is slowing across the UK in general.

‘As long as we continue to see inflation moving in the right direction so the mortgage markets continue to move, I predict this trend will continue, and by the end of the year average UK prices will be back on the increase – and that, of course, includes the capital.’

Listen to this article

Produced by ElevenLabs and NOA, News Over Audio, using AI narration.

When the Federal Reserve began jacking up interest rates in 2022, home sales cratered almost overnight; inventory dried up; the housing market “froze.” People who have mortgages with interest rates below 4 percent—which is more than 60 percent of homeowners—aren’t going anywhere. They’re not selling their houses. They’re staying put.

The current availability of homes for sale is about 36 percent lower than before the pandemic; this past October, home sales dropped to their lowest level in more than 13 years, and in November, the share of homebuyers looking to relocate to a different metro area was at its lowest level in 18 months. People who own homes have become so reluctant to move that they’re likely to pass up job offers in other cities, one study found.

If swapping a low mortgage for a much higher one is plainly undesirable, the way out of the problem—and into a new space—seems plainly obvious: renting. Now is a terrible time to buy a home, but renting would allow more Americans to relocate without becoming “house poor” at a 7 percent interest rate. A rental home could help a growing family break free of a too-small starter house. A national renting trend, in which owners put up their homes for rent and become renters themselves, could unfreeze the whole market.

“Why not just rent?” is a question I’ve asked myself (and my husband, and our real-estate agent) many times over the past couple of years, as we’ve tried and failed to sell our house and buy a new one. After a long day of touring gross, overpriced homes that would require thousands of dollars of renovation, all for double the interest rate we have now, I’d mutter, Why don’t we just rent a house instead of buying one of these dumps? Every time, they reacted like I’d suggested we live on an ice floe in the middle of the North Sea. Rent?

It turns out that deep cultural, regulatory, and financial incentives prod Americans toward the “homeownership ladder” and, once they’re on it, discourage them from hopping off. Although renting is often not any financially or psychologically worse than owning—in fact, it might be quite the opposite—renting after owning is just not something most Americans want to do.

It’s not that nobody wants to rent, of course. Demand for rental homes is healthy: In fact, rentals are becoming the new starter homes, as many would-be first-time buyers, who can’t afford to buy at today’s interest rates, rent houses instead. “Instead of moving from apartment to ownership, you move from apartment to renting a house and later on to ownership,” says Nicole Bachaud, a senior economist at Zillow.

But about 70 percent of people who sold a house recently also bought a home, according to a report by Zillow. (That doesn’t mean the other 30 percent all rented—they might have moved in with family, moved into a retirement home, or moved into another home they also own.) “Very, very few people make that transition back into renting,” Lu Liu, a finance professor at the University of Pennsylvania, told me.

Say someone does currently own a home at a low mortgage rate and wants to move. The first question would be what to do with that home. Financially, the ideal is to hold on to that house—and rate—for as long as possible. “Giving up a 3 percent mortgage in a 6.5 percent interest-rate environment is the equivalent of giving up 15 or 20 percent of home value,” Chris Mayer, a real-estate professor at Columbia University, told me. Nevertheless, renting your home out can be expensive and annoying. “You get a call at 7 a.m.—the hot-water heater is broken,” Mayer said. “Being a landlord is not that much fun or that easy.”

What’s more, the federal government, through regulations and incentives, practically begs Americans to buy homes, not rent them: Homeowners benefit from a slew of tax deductions that aren’t available to renters. Rents can increase, but fixed-rate mortgages never do. “During the pandemic, house prices went up by a lot, and that was very painful for renters and people who are trying to get onto the housing ladder,” Liu said. “But it wasn’t necessarily a problem for people who were already owning a house.” That means homeowners are shielded from inflation, their house payments a relic of the year in which they bought their home. Even if a current homeowner did opt to rent instead, they might find that typical rents are now even higher than their mortgage payment.

It’s not just fixed rates that make homeownership feel more stable than renting. In most cities and circumstances, a renter can get kicked out by a landlord who wants to move back into their house, or who simply wants to charge more rent. If you have kids, that raises the stakes of renting: What if they’re in a school they love, and the landlord decides you need to vacate?

Finally, homeownership has a firm hold on the American psyche—a preference that isn’t entirely rational. Though owning a home is often a good way to build wealth in the long run, in the short term, owners are on the hook for any repairs the home needs, which can be extremely costly.

Homeowners aren’t necessarily any happier than renters—one study of women in Ohio even found that homeowners are more miserable because they spend less time with their friends. But along with parenthood and marathons, it seems like one of those things that doesn’t make us happy but that we do anyway. “Homeownership in America is an ideal,” Daryl Fairweather, the chief economist of Redfin, told me. “And the ideal is that you don’t have a landlord, and you are the king of your own castle.” People want to paint the walls whatever color they wish—even if we all end up painting them Mindful Gray. We just want the option.

Perhaps more Americans would rent if renting weren’t so precarious. In countries where protections for renters are stronger, more middle-class people see renting as a long-term option for their family rather than as a temporary solution in their 20s. Take Germany, where only about 45 percent of households own, compared with two-thirds in the United States. There, landlords can’t terminate a rental contract for just any reason, and it’s extremely difficult for landlords to raise the rent. As a landlord you might “like to have a long-term renter leave, but you can’t,” Leo Kaas, an economist at Goethe University Frankfurt, told me. Rental contracts are open-ended, Kaas said, and that “makes it much more attractive for individuals in the first place to rent.” Some Germans move into low-income housing and stay there for years, even as their incomes rise and they technically no longer qualify.

For now, my husband and I have reached a détente in which I stare at Zillow rentals and he stares at Redfin’s for-sale listings. Neither of us much likes what’s on offer. So far, we’ve been doing what other homeowners have been doing: not moving.